CICC: What changes have occurred in the cryptocurrency market over the past year?

A systematic analysis of the trend changes in the cryptocurrency market in 2020.

A systematic analysis of the trend changes in the cryptocurrency market in 2020.Huang Le Ping, Wei Xin et al./Text, the article comes from the WeChat public account "Zhongjin Dianzhen"

In the soon-to-be-past year of 2020, we have seen significant changes in the ecological environment surrounding digital assets such as Bitcoin (the crypto world). The direct feeling is that the price of Bitcoin has nearly tripled over the past year, reaching a historic high of $27,000, as well as the issuance scale of stablecoins expanding 3.5 times to a historic high of $27 billion.

We believe that (1) the regulatory policies of various countries regarding digital assets are becoming increasingly clear, (2) the emergence of financial products/channels such as GBTC and PayPal has lowered the entry barrier for traditional investors to invest in digital assets, and (3) the rise of decentralized financial services based on blockchain are three intrinsic factors driving the development of Bitcoin and stablecoins. In the short term, the prices of digital assets will certainly experience significant fluctuations due to factors such as market liquidity, but in the long run, digital assets and blockchain-based financial services are expected to achieve sustained growth. For details, please refer to our in-depth report published in October 2019 titled “Blockchain and Digital Currency: How Technology Reshapes Financial Infrastructure.”

1. Traditional investors continue to join, driving Bitcoin's price up nearly 3 times in a year Bitcoin price has risen nearly 3 times. The price of Bitcoin rose from $7,200 at the end of 2019 to $27,084 (as of 2020/12/28), an increase of nearly 3 times, becoming the asset class with the highest increase since the beginning of the year, even surpassing the FAAMNG tech giants index. In addition to the impact of global liquidity easing, we believe that the financial innovations by financial institutions represented by PayPal, Robinhood, and Grayscale in broadening digital asset channels are the structural reasons behind the nearly 3-fold increase in coin prices over the past year. In the short term, coin prices may experience significant fluctuations driven by liquidity and speculative capital inflows and outflows, but in the long run, the continuous expansion of the traditional investor base is favorable for the stable rise of prices of digital assets such as Bitcoin.

Chart: Performance of major asset classes since the beginning of the year

Source: Bloomberg, CICC Research Department Note: Data as of 2020/12/28

Chart: Bitcoin price and daily trading volume since January 2014

Source: CoinMarketCap, CICC Research Department

The scale of stablecoins has expanded 3.5 times. Over the past year, the total issuance scale of stablecoins represented by USDT has risen from $6 billion at the end of 2019 to $27 billion, an increase of 3.5 times. We believe that the rapid development of decentralized applications (DApps) based on Ethereum, represented by collateralized lending (MakerDAO) and decentralized exchanges (Uniswap), has driven the continuous rise in demand for stablecoins. Looking ahead to 2021, we believe that stablecoins such as USDT will increasingly solidify their position as universal payment methods in digital asset transactions. However, whether global stablecoins (GSC) like Libra can achieve large-scale commercial use remains to be seen.

Chart: Changes in the scale of stablecoins since January 2015

Source: Coin Metrics, CICC Research Department

2. Digital asset regulatory policies are becoming increasingly clear, and new regulations in Hong Kong and Singapore are expected to promote the rapid development of compliant exchanges Digital asset regulatory policies are becoming increasingly clear, and new regulations in Hong Kong and Singapore are expected to promote compliant exchanges rapidly. Over the past year, the G20 has led the formulation of a regulatory framework for global stablecoins (GSC) represented by Libra to prevent financial risks. The Hong Kong Securities and Futures Commission established regulatory rules for licensed asset management companies investing in virtual assets in 2019 and issued the first cryptocurrency exchange license (Type 1 license for securities trading and Type 7 license for providing automated trading services) to OSL in December 2020. Singapore has established the Payment Services Act, laying the foundation for the development of exchanges, asset management companies, OTC, and other digital asset-related financial services in Singapore.

Chart: Current regulatory attitudes towards crypto assets in various countries (as of 2020/12)

Source: HuChain Pulse, CICC Research Department

Source: HuChain Pulse, CICC Research Department

3. Digital asset investment channels: from Coinbase and Huobi to GBTC and PayPal In the past, buying and selling digital assets required going through professional exchanges like Coinbase, which had high entry barriers and insufficient investor protection. Over the past year, we have seen Grayscale launch the BTC trust GBTC, as well as well-known payment/securities trading platforms like PayPal and Robinhood introduce Bitcoin trading services, significantly lowering the entry barrier for institutional and retail investors to invest in digital assets. According to disclosures on Grayscale's official website, GBTC's AUM has reached $14 billion, and from the end of last year to 2020/11/30, the newly added Bitcoin holdings in GBTC accounted for 65% of all newly mined Bitcoin in the market. Traditional institutions such as Fidelity and DBS have also successively established digital asset service platforms. Traditional financial institutions are gradually becoming important participants in Bitcoin investment.

► The emergence of trust-type investment products represented by Grayscale GBTC allows investors to participate in investments without worrying about the storage and security of crypto assets; at the same time, GBTC is traded on the OTC market and regularly disclosed to the SEC, enhancing the product's liquidity and transparency, and providing a convenient entry channel for U.S. investors;

► PayPal (payment software), Robinhood (stock trading software), and other influential terminal players in the financial payment field have opened trading interfaces to users and provided custody of crypto assets by cooperating with compliant crypto asset brokers, allowing a large number of users to access crypto assets with one click without opening additional accounts, thus lowering the investment threshold.

Chart: Business landscape of digital asset entry channels

Source: CICC Research Department

Chart: Grayscale Bitcoin Trust holdings since January 2020

Source: The Block, CICC Research Department

Chart: GBTC principle diagram

Source: Chain Hill Capital, CICC Research Department

Chart: Illustration of users purchasing Bitcoin on PayPal

Source: PayPal, CICC Research Department

4. Ethereum enters a new stage of development, becoming the most active public chain network The Ethereum ecosystem is maturing, and financial services are becoming mainstream. Unlike Bitcoin, which is mainly used as a digital asset, Ethereum supports smart contracts, PoS, and other functions, making it suitable for developing distributed applications based on blockchain. Over the past year, we have seen the rapid maturation of the Ethereum ecosystem. The daily trading volume of the Ethereum ecosystem has increased by 90% over the past year. Financial services such as MakerDAO (decentralized lending) and Uniswap (decentralized exchange) have also become mainstream applications in the Ethereum ecosystem. Although the legal status of decentralized finance (DeFi) is still unclear, its development over the past year has shown efficient and transparent technological advantages, and whether it can become an important supplement to traditional finance remains to be seen.

Chart: The proportion of various types of Ethereum applications has gradually changed since December 2019

Source: State of the DApps, CICC Research Department

Chart: Top 10 Ethereum applications from October 2019 to December 2020

Source: State of the DApps, DAppTotal, CICC Research Department

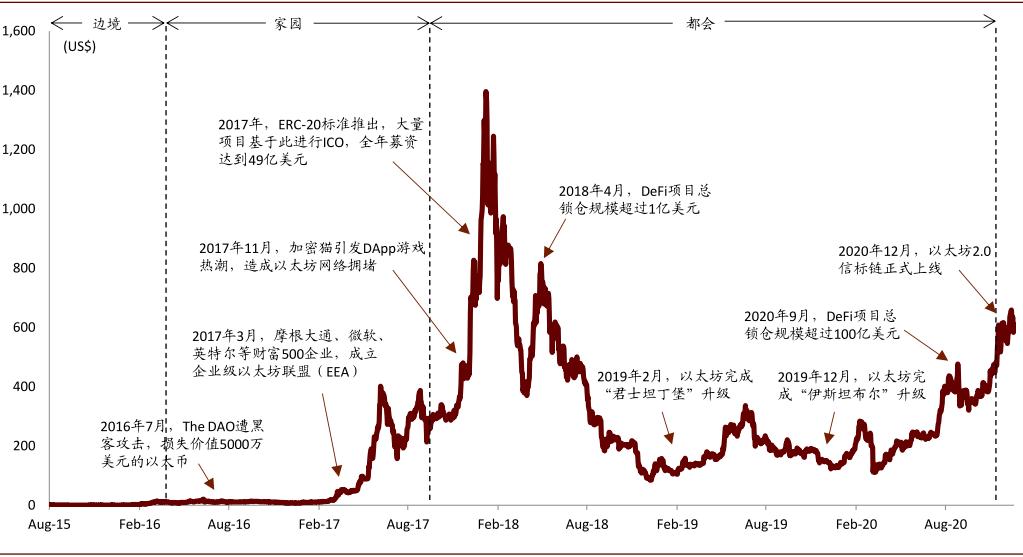

Chart: Major development milestones and historical prices of Ethereum

Source: CoinDesk, CICC Research Department

Chart: Total number of Ethereum addresses and daily active addresses since 2019

Source: Etherscan, Coin Metrics, CICC Research Department

Chart: Daily on-chain transaction counts of Ethereum since January 2019

Source: Etherscan, CICC Research Department

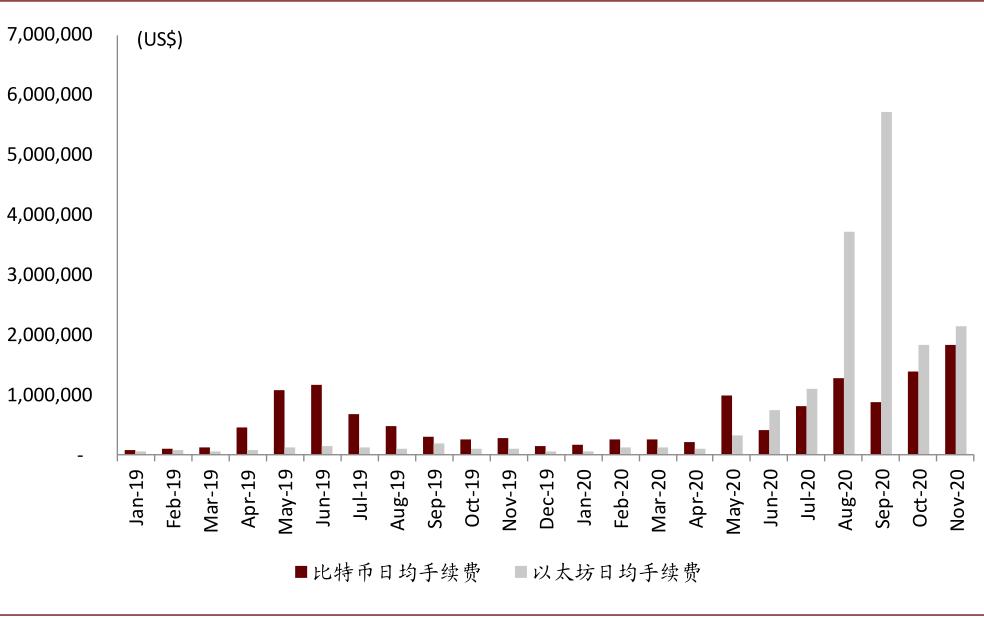

Chart: Ethereum transaction fees have exceeded Bitcoin for six consecutive months

Source: Coin Metrics, CICC Research Department

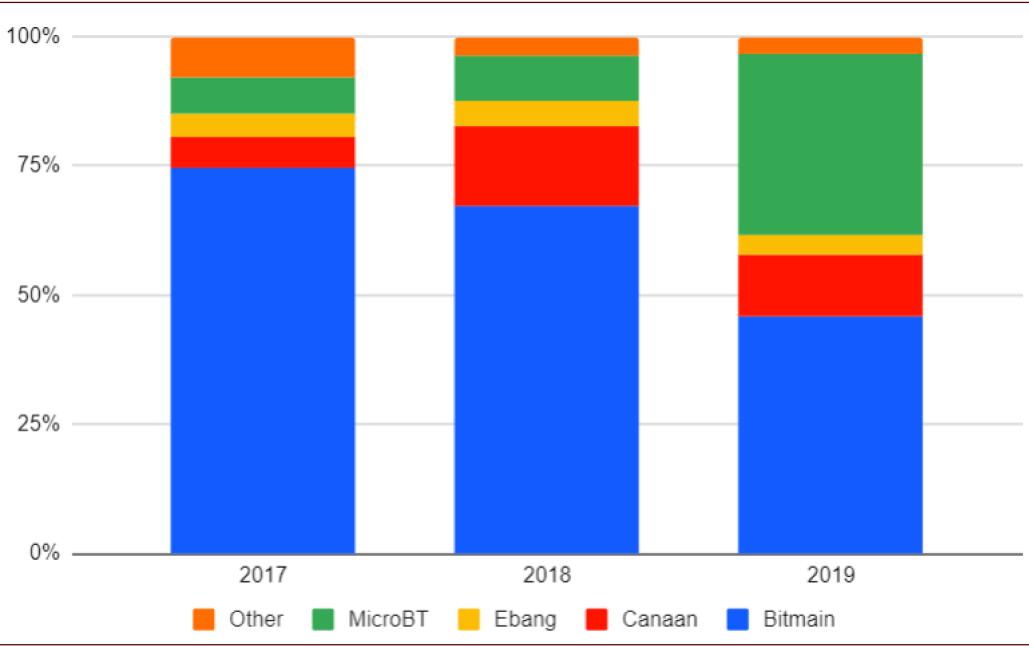

5. Mining machines: from 16nm to 7nm, from a single dominance to multiple strong players Chart: Evolution of mainstream mining machine performance

Source: Zhongguancun Online, CICC Research Department

Chart: Market share of ASIC mining machine manufacturers from 2017 to 2019 (calculated based on sold TH/s)

Source: BitMEX Research, CICC Research Department

Risks Risks of cryptocurrency price volatility; regulatory risks of digital currencies and blockchain; the implementation of blockchain applications may fall short of expectations.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles