Why is it said that the 0X protocol is severely undervalued?

At first glance, 0x seems like a small fish in the vast ocean of DeFi, but as you delve deeper, you'll find that 0x's reach has extended throughout the entire DeFi ecosystem.

At first glance, 0x seems like a small fish in the vast ocean of DeFi, but as you delve deeper, you'll find that 0x's reach has extended throughout the entire DeFi ecosystem.This article is from DeFiToday, authored by Danial Abbasi, and compiled by Chain Catcher.

0x ($ZRX) is a lesser-known project that supports nearly all top protocols and services in DeFi. While it has generated significant revenue for its users, ZRX token holders, developers, and market makers, its true value is obscured by misinformation and confusion, and even the facts are misrepresented. At first glance, 0x appears to be a small fish in the vast ocean of DeFi, but as you delve deeper, you'll find that 0x's tentacles have extended throughout the entire DeFi ecosystem.

Let's start from the beginning.

1. 0x and Matcha

0x first emerged in 2017, aiming to address a major issue faced by many DApps: guiding liquidity requires real trading data to enhance liquidity. 0x identified a potential fix and launched 0x Labs, subsequently introducing a developer-centric product—Matcha, a DEX aggregator powered by the 0x API.

Matcha quickly established itself as the DEX offering the best prices for ERC-20 token swaps. Even when competitors seem to provide better pricing, they often achieve this by omitting forward slippage and similar factors. This means that traders lose out on the marginally improved pricing across multiple trades by giving up the forward slippage on a single trade.

Imagine there are 10 trades, each selling 1 ETH for approximately 1300 USDC at a price of 1 ETH.

A quotes 1,301 USDC; B quotes 1,299 USDC. There seems to be an obvious good choice here. But A has forward slippage, while B does not, so after 10 trades:

A: $13,010

B: $13,021

In this example, A represents 1inch, and B represents Matcha, and the effect would be magnified as trade size increases.

We can see that choosing a better quote without considering forward slippage can lead to a significant loss for traders. At its core, this highlights the importance of the execution price versus the quoted price, a realization that traders are gradually coming to understand. This pricing model is less cost-effective, but more importantly, it reflects the kind of hidden fees that should be penalized in our society, akin to banking practices.

This is not an exaggeration; documented cases show that in a single trade of 38 ETH, there was 8 ETH of forward slippage. As trade size and volume increase, the likelihood of at least one trade experiencing forward slippage approaches 100%. If you make a sufficiently large trade, you will almost certainly use 1inch or any aggregator employing this pricing method, and it will at least appear that the gains from using Matcha are greater.

This is not coincidental; hiding these small print details is also not a good practice. The 1inch aggregation protocol provides 1inch fees through so-called forward slippage, as explained by Messari.io (or what 1inch refers to as "Spread Surplus"). This is a business model predicated on traders' disdain for calculating the difference between quoted and execution prices. When traders realize this, 1inch will lose its reputation and traders.

Is Matcha's market share significantly lagging? No, that's a reporting issue.

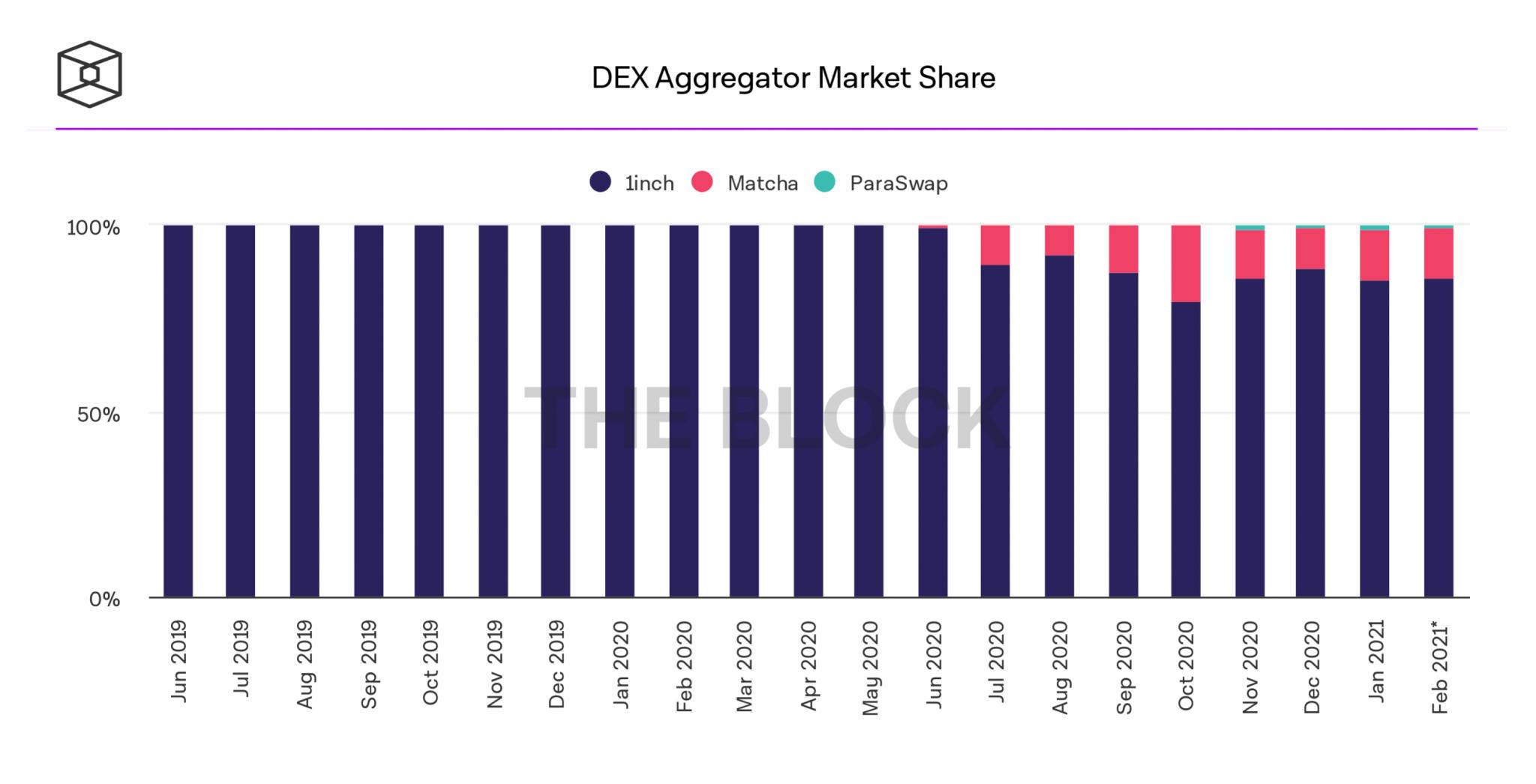

Most importantly, Matcha is an excellent product. However, a great product does not automatically win more market share, and most reports indicate that Matcha's market share lags behind 1inch. Matcha is growing rapidly, but an initial look at this market share chart from The Block simplifies and misleads the facts.

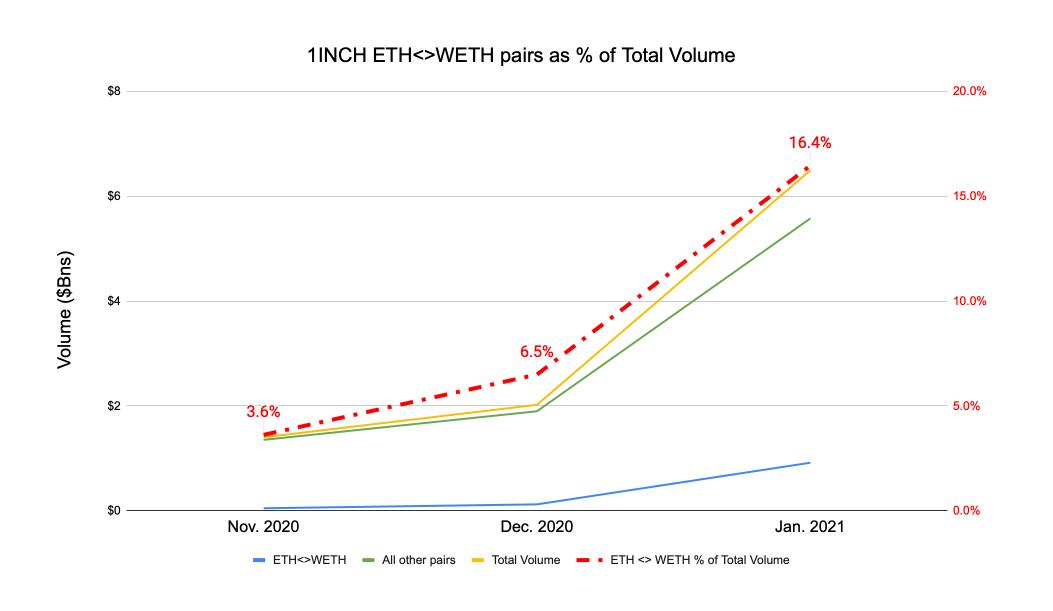

1inch's report is also not very rigorous. It includes the trading volume of WETH, while Matcha does not. This is not an industry standard. Coinbase does not include the USD-USDC trading pair in its volume reports. Why does 1inch do this? It may be because the ETH to WETH trading pair accounts for nearly 20% of 1inch's monthly report trading volume.

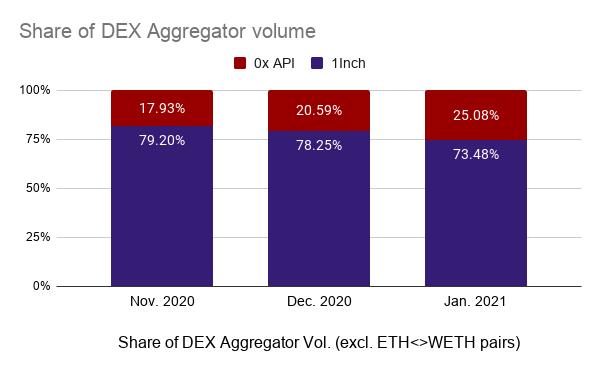

Moreover, what we really need to compare is the trading volume of the 0x API with that of 1inch. This is the only reasonable way to do so, as both are similar products. When we make this comparison, the growth and market share appear significantly different from before.

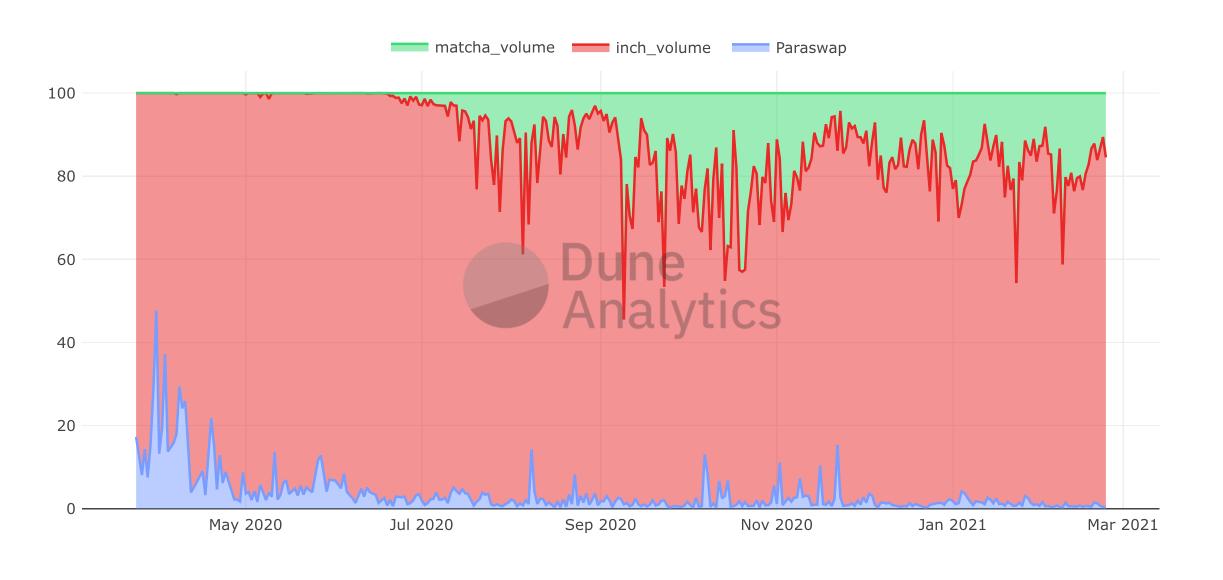

We omitted ParaSwap (which accounts for about 1% of our total trading volume) for a direct comparison. Therefore, when you use erroneous comparisons between apples and oranges and exaggerated self-reported trading volumes, you see the following picture, where 1inch is the undisputed market leader. Adjusted, we see a markedly different picture:

With an accurate perspective, it becomes clear that Matcha is growing rapidly and steadily: its market share is about 25%, while it was generally reported to be around 13% in January of this year. Notably, the chart also shows that this number has seen strong growth over the past few months.

That's all for Matcha. This means that 0x will have more trading volume.

2. 0x market makers' revenue is also higher than reported figures

0x has been misunderstood as being somewhat old-fashioned or outdated (by crypto standards), a remnant of an earlier stage of crypto evolution. For example, CoinMarketCap refers to Uniswap as a "modern alternative" to 0x, but there is no evidence that Uniswap represents the modernization of 0x, nor is Uniswap a substitute for 0x. In short, Messari.io states that the competition for traders is among aggregators, while the competition for trades is among AMMs. They complement each other rather than compete.

While Messari can be insightful, their information can sometimes be outdated or incomplete. Messari states that 0x does not manage decentralized exchanges, but in fact, 0x manages Match; it discusses the 0x Launch Kit, which was abandoned six months ago.

Other sites' erroneous reports stem from their reporting models not aligning with Matcha's operational model in certain aspects. For instance, CryptoFees is a common site for collecting project fees. However, its reports do not accurately reflect 0x's fees because it focuses on on-chain fees, while most of 0x's fee model operates off-chain.

Correcting this yields results that are far more dramatic than the market share data we previously assessed. It shows that 0x participants earned approximately $510,000 within 24 hours, ranking fifth after Bitcoin, Ethereum, Uniswap, and SushiSwap, which is 32 times different from the data reported by CryptoFees.

3. 0x utilizes multiple sources of liquidity, making it an ideal choice for the emerging hybrid MM/AMM DeFi market

Lastly, a point that is somewhat abstract but equally critical: 0x is often confused as merely an order book protocol; in fact, it derives from a super set of liquidity models such as RFQ, aggregation, etc. This makes 0x's positioning very suitable for serving various traders and market makers.

What does this mean?

It means that the DeFi space is attracting more professional market makers and seeing a rising demand for more competitive pricing.

Hasseeb Qureshi articulated this regarding Uniswap: the future of on-chain market makers.

"Fully algorithmic AMMs will always have a place in DeFi. They will be crucial for adding trading liquidity and astonishing for guiding liquidity for incentive pools and long-tail assets. But most of the trading volume in cryptocurrency will always be power-law distributed among core trading pairs; today, almost all traffic in DeFi comes from retail investors buying and selling conventional assets from a single interface. I expect that most of DeFi's trading volume will become dominated by professional market makers through such mechanisms."

As trading volume grows, professional market makers will enter DeFi because there are too many retail investors who will benefit from it; this is an opportunity that cannot be ignored. It is a matter of when, not if, and it is already happening. When this occurs, 0x will provide them with the best service because it focuses on a collection of liquidity models.

4. Conclusion: We have been silent on this issue for too long

0x has been misunderstood by many crypto media and traders, with other voices repeating what they believe to be authoritative viewpoints and accurate narratives, but the facts tell a different story. Part of this can be attributed to "reverse holder bias," where investors who bought at the peak of ZRX in 2017 are now at a loss. As the market sheds this bias and the performance of 0x products like Matcha becomes impossible to ignore, investors will recognize this and take action. Like everything in the crypto space, when it happens, it will happen quickly.

Risk warning

Risk warning Risk warning

Risk warning