BitMEX Founder: How to Value the Future of Ethereum?

The market has a very high price-to-earnings ratio for the transaction fees generated by an immature ecosystem.

The market has a very high price-to-earnings ratio for the transaction fees generated by an immature ecosystem.The author of this article is Arthur Hayes, the founder of BitMEX, and it has been compiled by Alyson.

How to value the Ethereum network has always been an industry-wide dilemma. Recently, Arthur Hayes, the founder of BitMEX, wrote about this issue.

In this article, Arthur Hayes estimates the value of the Ethereum network ecosystem by calculating the total fees charged to users by traditional financial services and the market share that Ethereum DeFi might capture from CeFi.

His conclusion is that if 0.5% of the trading volume from the CeFi system is transferred to the Ethereum ecosystem, the price of ETH will appreciate tenfold from its current level. To further present the logic of this article, Chain Catcher has translated and edited it without altering its original meaning. (The views expressed below are solely those of the author and should not be the basis for making investment decisions, nor should they be interpreted as investment advice.)

Humans tend to seek shortcuts in all aspects of survival. In the context of financial markets, everyone wants to find experts, insider information, or private equity projects. If this continues, it will lead to a transient, high-risk, and pathological state that exceeds the average.

Essentially, we all know that the aforementioned shortcuts carry significant risks, yet people still take the risk to chase them—I'm constantly asked questions like "Which coins should I buy?", "Is now a good time to buy?", "Can you provide some technical analysis?", etc. However, even for my closest friends, I wouldn't offer any advice to avoid them mistakenly thinking I'm a prophet.

I recently became a sponsor of the Tampines Rovers Football Club in the Singapore Premier League. Some football players are very interested in cryptocurrency, and one day during lunch, they asked me a few questions.

Among them, three players had engaged in cryptocurrency trading and made some profits, but they also asked me the series of questions mentioned above, hoping I could reveal the secret to wealth in the two-hour lunch.

Unfortunately, I disappointed them and instead asked them many questions. I made them think about why they wanted to invest and trade, how much time they planned to invest, and what their risk tolerance was. The inspiration for this article came from—when I asked if any of them had read the Bitcoin white paper, not a single one answered affirmatively.

The importance of the white paper is not because I am a Bitcoin researcher, but because almost all blockchain projects have drawn on the concepts in the white paper and used it as a benchmark.

Some projects may not directly borrow from the Bitcoin white paper but instead imitate other projects that have adopted the concepts from it. As a rule of thumb, almost every blockchain or crypto project has adopted some successful and proven concepts from previous projects, either imitating them or attempting to innovate upon them.

Of course, there are also some projects that superficially mimic others poorly, but they have a nice website filled with all the crypto jargon. If you take the time to read their white papers, you should be able to immediately identify them as a scam project (usually because they are either a haphazardly cobbled-together copy or completely nonsensical).

The 1,000 projects that followed Bitcoin are essentially imitations that aim to improve. While Ethereum has imitated Bitcoin in many ways, it has technically provided a substantial improvement, greatly expanding the potential applications of Bitcoin technology. Wouldn't you have wanted to buy some ETH during the presale in the early years? I know I would, even though I publicly stated early on that it was a garbage coin. Ultimately, any new project needs to answer the following fundamental questions to maximize the chances of success:

• Why are we trading in this magical internet currency system at this moment?

• What do we hope to achieve?

• What does the current financial system we are trying to improve or replace look like?

If you don't have a profound insight into the "why" and "how," you won't be able to distinguish fact from fiction. As digital currencies become more widely known, without a macro and comprehensive understanding of their essence, you won't be aware of the role that search engines and promotional content play in promoting false digital currencies, and you will often easily fall into traps.

In fact, the article I wrote in 2021 is fundamentally more philosophical than ever, with little focus on the feasibility of projects. This is because if you don't first understand why digital assets might pose a fatal threat to our existing financial system, you will never have the conviction to hold onto your assets when they drop 90% in a bear market and then rise tenfold in a bull market.

If you bought Bitcoin at a high price of $20,000 in 2017, by the end of 2018, your assets would have dropped nearly 90%. However, if you held on until today, your investment would have tripled overall, still exceeding the growth rate of the Federal Reserve's balance sheet. So I constantly remind everyone that the benchmark to surpass is the inflation of existing currencies. If you lack conviction, then you have already lost.

The entire decentralized finance movement aims to establish a peer-to-peer currency system that transfers money from one point to another without a centralized, trusted gatekeeper. The focus of this article is to examine the various aspects of the "intelligence tax" we pay for blindly trusting the financial system. If we imagine a future where some decentralized digital currencies can replace part of the demand for a centralized monopoly group, how much upside potential would the current crypto market have?

1. The Banking System

Let's start with some charts that show the market's view of traditional banking business models.

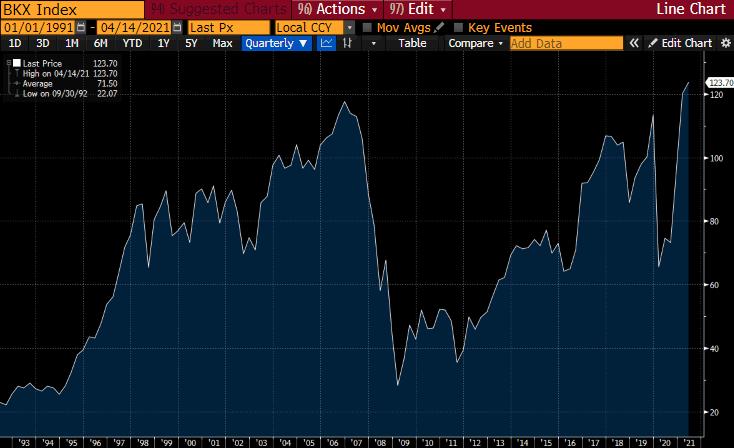

This is the latest chart of the KBW Bank Index, representing major commercial banks in the United States. As you can see, it recently just returned to its historical peak after reaching a peak in 2007. The Federal Reserve has taken every measure to save those banks that are too big to fail, yet it took these banks 14 years to recover to the 2007 high.

This is the latest index chart of EuroStoxx Banks, representing major banks in Europe. This chart shows that they have dropped a full 80% from their peak in 2007.

This is the index chart of the CSI300 banking sector. Major banks in China are still down 20% from their peak in 2008. State-owned enterprises are the recognized business model in China. However, even with government assistance, these banks have not exceeded their capabilities.

Japan is not much better off compared to China. The Tokyo Stock Exchange index has fallen over 90% from its peak in 1989.

This is the Nifty Bank Index chart from India. I never thought Indian banks would perform this well. When demographics are on your side, it's hard to mess up your banking system no matter how hard you try. India has an A+ performance, and I hope this price performance continues.

On the other hand, even after the tech bubble burst in 2000, tech leaders are still at an exponential high today. Given that integrated circuits and semiconductors are the technological cornerstones of our existence, the chart of Taiwan Semiconductor (TSMC and 2330 TT) represents the progress of innovation.

Those banks that privatize profits and socialize losses have not enriched their shareholders, which is quite sad. If they had adopted the technological innovations we have never seen in the past decade, they would have been able to achieve exponential growth like TSMC and other tech leaders.

The stock market is shouting that the traditional banking business model is being disrupted, and importantly, what can convincingly replace it in the future. Every product and service offered by banks can be replicated and improved through a decentralized service powered by blockchain. I believe this replication can be achieved at a macro level at a lower cost, but this remains to be discussed. I expect some empirical evidence to emerge in the near future.

Traditional banks are destined to become the primary service providers for the global baby boomer generation (specifically referring to those born between 1946 and 1964), who are relatively affluent but unable to understand digital finance. My mother would rather risk contracting COVID-19 to go to a physical bank than learn how to use online banking, and she is not alone in this. This business still generates billions of dollars in fee income, but it is certainly not a market share that is still growing.

Here are some common services provided by banks and examples of peer-to-peer services in decentralized finance (DeFi):

- Savings Account—An account that banks use to pay you interest.

This is equivalent to staking stablecoins on a DeFi lending platform to earn yields. For example, if you hold USDT (with a 1:1 exchange rate to the dollar), you can stake it on Compound and earn yields. As a reward, you will receive COMP tokens.

- Checking Account—An account that allows you to withdraw your balance on demand to pay for things.

This is equivalent to a digital wallet holding any cryptocurrency in DeFi. You can use your assets at any time without anyone's permission. For various reasons, banks can refuse you access to your hard-earned money. However, as long as you are connected to the internet, you can utilize decentralized functionalities.

- Loans—Banks charge interest to lend you money to purchase various things.

The problem is that banks often price credit differently based on non-monetary factors (such as race). This gives the impression that certain groups are restricted, and even if they can obtain loans, they must pay higher credit costs than other groups.

Moreover, in this era of global corporate socialization, large entities can essentially achieve free borrowing, while small and medium-sized enterprises are often excluded from the commercial credit market. This has sparked public outrage against banks, as they should be the credit channel for productive enterprises.

In DeFi, most loans are currently under-collateralized and there is excessive collateralization; under-collateralization means you have pledged more collateral than you have borrowed. Additionally, the only real demand for credit comes from speculators and miners. In this area, the traditional banking system, despite its flaws, still performs better than DeFi.

- Trust Services—A very important function performed by banks to verify certain situations of individuals or businesses.

They can verify your net worth based on your deposit history at the bank, prove you have a well-paying job and your total salary, and provide an address verification to show where your account statements are sent. Many of these services come at a cost, and you must pay to prove your personal information to others.

In DeFi, assets issued on public chains can usually be independently verified for free. If your income is in the form of digital assets, it becomes easy to prove how much your income is. Regarding address verification and other PII (Personally Identifiable Information), many projects are working to create a shared secure database of PII that other services can call upon to verify your identity.

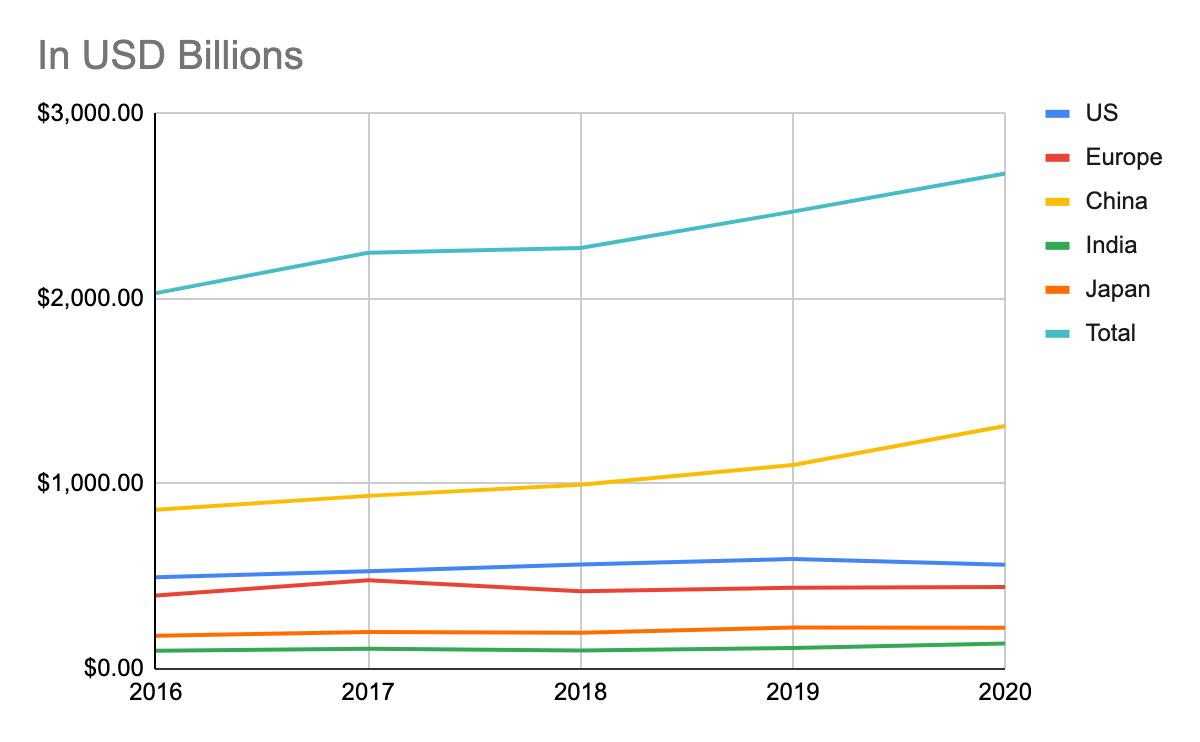

How much "tax" do we pay each year to the largest financial institutions to execute these services? I analyzed the following revenues:

KBW Bank Index (U.S. major banks)

EuroStoxx Bank Index (EU major banks)

CSI300 Bank Index (China major banks)

Tokyo Stock Exchange Bank Index (Japan major banks)

Nifty Banking Index (India major banks)

I looked at the highest revenue because this is essentially the "tax" we pay as customers for these services.

In 2020, the total tax paid by global users to these institutions was $2.68 trillion, which is 2% to 3% of global GDP. Any ability to reduce taxes while allowing more people and companies to access good financial services is a net benefit to humanity.

Clearly, for those speculators who can find suitable strategies in the face of these savings-promoting protocols, this is a tremendous opportunity to outpace the depreciation of fiat currency.

2. Eliminating Audits

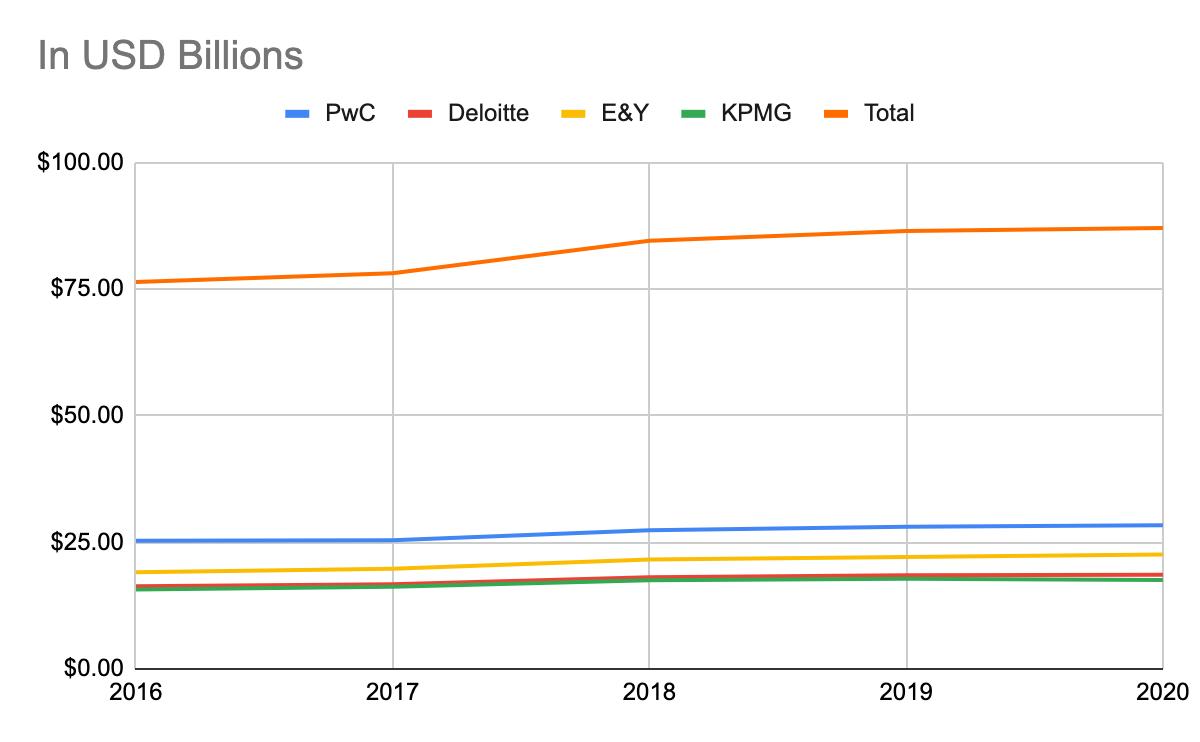

Why do companies need audits? Anyone interacting with a company that comes from banks, securities regulators, or even employees wants to know if the books are reasonable. Therefore, audit firms charge fees to verify the authenticity of the accounting statements generated by their clients.

In an ideal future, all flows of funds will occur on public chains. Imagine you are a durian farmer in Malaysia and you sell Musang King durians online. The only payment you accept is USDT, and all your agricultural material suppliers also accept payments in USDT, which means you can verify the payment amounts and profits for every fruit sold without needing to purchase services from an independent third party.

I've heard some people say that triple-entry accounting makes all professional accounting and auditing firms obsolete. These firms have no reason to continue charging this "trust tax."

I looked at the fees earned by the Big Four accounting firms—E&Y, PwC, KPMG, and Deloitte—from audit and accounting services. In 2020, we paid $87.09 billion in taxes to these bean counters. In the future, that number will be zero, and accounting statements will become completely accurate. It's that simple.

3. Ratios

Ethereum is the most developed decentralized smart contract network, and even though its current Gas fees are astronomical, it is still a good product.

Nothing in life is free, and this is doubly true in the crypto capital markets. Every operation on the Ethereum network requires payment, which we can view as revenue to keep the network running or as the tax consumers pay for using products and services supported by ERC-20 DApps.

I am using transaction data collected on Glassnode and plotting the revenue multiples of the Ethereum network over the past four years. The reason I look at this metric is that it represents the cost we have to pay to use these networks.

Any DApp user utilizing these protocols must pay to leverage the network, and any fees charged by DApps exceed the costs of using the base layer protocols, which will compete with certain natural prices that we can only observe in the near future. A portion of the fees charged by traditional financial intermediaries may eventually be allocated to these networks.

Clearly, DeFi aims to improve services at a lower cost, so we cannot assume that all the money spent in the CeFi world directly translates into revenue for the base protocols and their enabled DApps. Therefore, let's look at why this is such an amazing opportunity from a higher benchmark perspective.

Above is a time series chart of ETH price versus revenue, where revenue is defined as transaction fees excluding miner block rewards. This chart covers the past four years, with the initial peak coinciding with the ICO boom of 2017.

Both Y-axes of the two charts are on a logarithmic scale, allowing us to truly understand the exponential nature of the time series data. Most interestingly, as ETH price hits new highs, its price/revenue ratio is at the low end of its historical range.

If you are a follower of mean reversion, consider the following:

Price/Revenue on April 10, 2021: 98

Average Price/Revenue Ratio: 1528

Median Price/Revenue Ratio: 430

Standard Deviation: 3939

ETH/USD Price on April 10, 2021: 2071

Median Reversion Price: 9054

Mean Reversion Price: 32143

These are statistics based on optimistic analysis, which does not mean they will happen, but they indicate that if these figures align with large sample data performance, reaching these levels is not impossible.

Ethereum is a decentralized computer, and computational power costs money. The more useful DeFi applications built on Ethereum are, the more users will have to pay to escape greedy CeFi platforms. Currently, the price/revenue ratio is close to 100, at the low end of its range.

This ratio is a retrospective measure. Here are the price/revenue statistics for ETH from April 2020 to now:

Lowest: 86

Highest: 608

Median: 169

Mean: 255

Standard Deviation: 168

Let's use the median as a forward-looking approximation of the value of the Ethereum network, assuming that Ethereum can capture a certain percentage of the average earnings of banks and the Big Four audit firms over five years. In addition to the usage fees generated by the Ethereum base layer protocol, the top DApps will also charge some fees for using their services. Therefore, we must assume that the actual amount generated by Ethereum and DApps is relatively small.

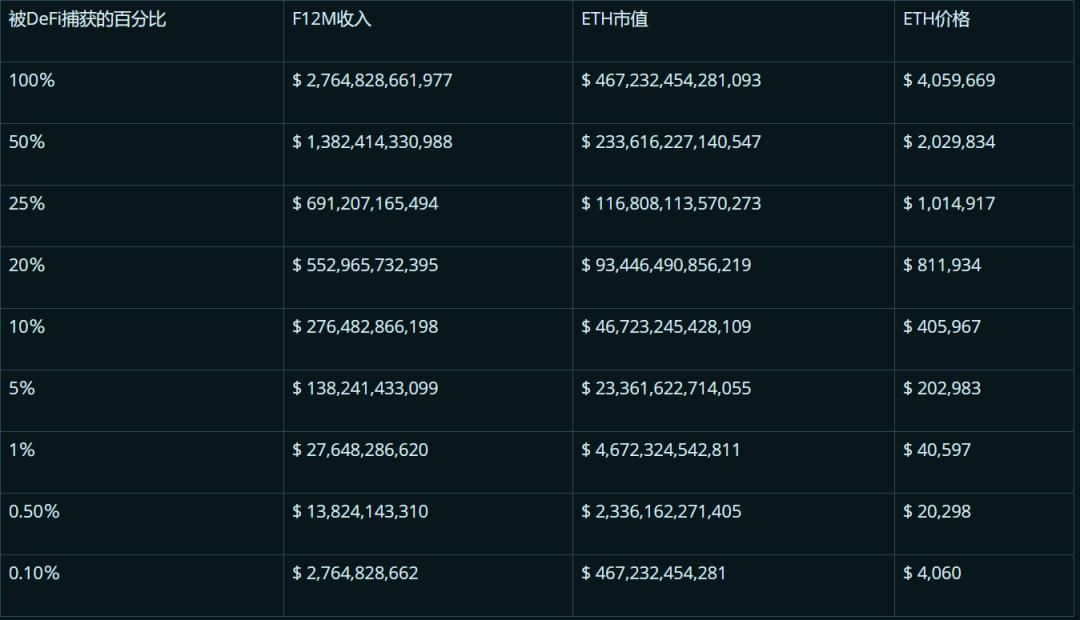

The table below describes a hypothetical scenario where a certain percentage of revenue will shift from centralized services to decentralized services over the next 12 months.

These numbers are quite unusual, but since this is a very rough, high-benchmark background analysis of an uncertain future, it is unlikely to be completely accurate. Assuming that 0.5% of the trading volume is transferred to the Ethereum ecosystem, the price of ETH will appreciate tenfold from its current level; if the transfer ratio is 0.1%, the price of ETH will double.

I am very confident that DeFi can capture at least 0.50% of the trading volume from CeFi. Can DeFi demonstrate a higher success rate? Absolutely. If I am satisfied with 0.50%, just imagine the potential if we open the floodgates and capture 10 times or 5% of the revenue.

When you make a high benchmark estimate indicating that you can still make money even in the worst-case scenario you assume, regardless of what metrics you value, go long.

The reason is simple: the current financial system has not adopted new technologies at the pace it should, and the market clearly shows a rigid financial service system in the stock valuations of its major participants. The solution may be DeFi, supported by public chains with smart contracts.

Although Ethereum is currently the best public chain, there are others trying to exploit its vulnerabilities and become leaders, including Polkadot, Solana, Cosmos, Cardano (when Godot arrives and smart contracts are finally available), etc.

Calculating 0.50% of the revenue from CeFi companies still amounts to $14 billion. As you can see from ETH, the market has a very high price-to-earnings ratio for transaction fees generated by an immature ecosystem. Therefore, at the portfolio level, even taking a "complain and pray" attitude towards the underlying public chain of smart contracts could yield high returns.

Another danger is that if you are intellectually lazy, you will invest in any project that superficially says the right things. Take the most-read Medium posts about DeFi as an example; if you put that content on a flashy website, I bet you will attract large sums of money from gamblers looking for the next Ethereum into your wallet.

This is why I urge the football players who have lunch with me to read the Bitcoin white paper and study it. Only when you witness and appreciate beauty can you protect your capital from the harm of ugliness.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles