Reunderstanding Ethereum from Four Dimensions

Ethereum is the "world computer" and "value layer" of the internet, allowing people to build applications and products using code-based assets.

Ethereum is the "world computer" and "value layer" of the internet, allowing people to build applications and products using code-based assets.The author of this article is Packy McCormick, and it has been translated by Hu Tao.

Ethereum is the most talked-about topic in the crypto market recently, with EIP 1559 and ETH 2.0 set to bring a fundamental shift to Ethereum's narrative. What impact will this have on the industry? Overseas media person Packy McCormick recently wrote about Ethereum, analyzing its sources of value from multiple perspectives, which is quite valuable for reference.

What would you do if I told you about a company with strong network effects and 200 times year-over-year revenue growth, which is preparing to offer a 25% dividend and implement a permanent stock buyback program? Is this something you might be interested in?

This is almost what Ethereum is. It is one of the most fascinating and compelling assets in the world, but its story has become murky due to its complexity and the specter of crypto.

Ethereum encompasses many things, all of which promote each other. Ethereum is a world computer, a pillar of the decentralized internet (web3), and also the settlement layer of web3.

Bitcoin is simple; it is digital gold, a store of value. That is its value pillar. It is immutable and the most decentralized asset in the world. As long as others believe in its value, it will continue to hold value.

Ethereum is not just a cryptocurrency. It is the "world computer" and "value layer" of the internet. It allows people to build applications and products using code-based assets. If you believe that web3 will continue to grow, then you might believe that over time, Ethereum will become the settlement layer of the new internet. Various transactions will turn to Ethereum to exchange funds and maintain secure, immutable records.

A year ago, much of Ethereum's value existed in theoretical form. Personally, I found it interesting and bought ETH in 2017, but I sold all 15 ETH in June 2020. As you know, I was an idiot. Even after the recent drop, those 15 ETH are worth over $300,000. I missed out on about 10 times the upside.

Since then, several things have happened that have turned my moderate curiosity into strong curiosity and optimism:

1) Explosion of use cases. DeFi, NFTs, and DAOs have become real applications of crypto technology, growing astonishingly over the past year;

2) Deflationary currency. With EIP 1559 set to be implemented, the supply of ETH may become deflationary, eliminating its biggest monetary weakness;

3) ETH 2.0. Ethereum is currently running a test chain that will merge with the Ethereum main chain in about six months. When this happens, Ethereum will switch from proof of work (PoW) to proof of stake (PoS), and more value will be generated for ETH holders;

4) Narrative. The narrative surrounding Ethereum is becoming increasingly popular and mainstream.

Currently, Ethereum is at a narrative inflection point, and the reflexivity of the narrative is more important for blockchain than for almost any other company or asset. Owning ETH is like owning a share of the internet. Demand for ETH will rise as the usage of web3 increases, and the upcoming changes will reduce the supply of ETH and provide more value to holders. It’s like tech stocks, bonds, web3 tickets, and money merging into one.

To clarify the bull market, we need to understand why Ethereum will survive and see increased usage, how it actually makes money, and the differences between ETH and tech stocks.

1. Ethereum is the Excel of Blockchain

If you are bullish on Ethereum, you first need to believe that it will exist for a long time, that more and more people will continue to use it, and that others also believe these things to be true. Then you will be pleased to know that Ethereum is the Excel of blockchain.

This is not entirely accurate. The analogy breaks down in some places. But for our purposes, it is sufficient.

Ethereum is a Turing-complete, programmable blockchain that anyone can use to build sophisticated applications with smart contracts. People can build various decentralized applications on Ethereum, providing everything from security to identity to payments. Decentralized finance (DeFi) applications, NFT marketplaces, decentralized autonomous organizations (DAOs), as well as games and virtual worlds can all be built on Ethereum, all powered by ETH.

This flexibility is really hard to achieve. In the article "Excel Never Dies," Ben Rollert and I wrote about the persistence of Excel in the tech space, where we often see new products replacing old ones every few years. We wrote:

If there is one core product design lesson to be learned from EXCEL, it is that combining usability and flexibility is both extremely difficult and extremely rewarding;

The developer's design principle is to make any piece of software really good at one specific thing, deliberately limiting its functionality to a specific domain. Excel is a notable exception to this rule—it is akin to a phone with a vast array of options, and clearly, hundreds of millions of people actually want to compose for it.

You can replace "Excel" with "Ethereum," and it works quite well. Beyond the product philosophy, there are some specific similarities between the two, including Turing completeness and composability.

Turing completeness and composability together mean you can build smart contracts to compute anything and then link them together to build increasingly complex things faster. It takes time to get the engine revving, but once it moves, it moves quickly.

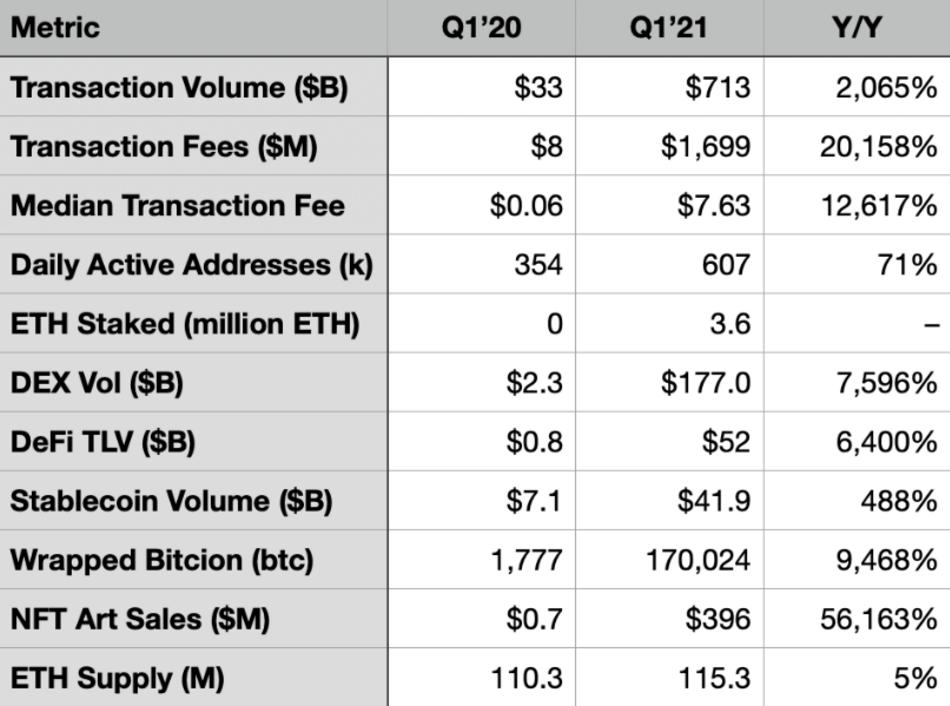

That is exactly what is happening. After years of relatively quiet building during the crypto winter, facing skepticism about whether these things have any real utility, 2020 and early 2021 witnessed an explosive growth in actual use cases within the Ethereum ecosystem. In the data announced by Ethereum for the first quarter of 2021, James Wang created a chart highlighting the progress made this year:

In the broad range of use cases, these massive numbers are a testament to the momentum and composability of the space:

1) The trading volume of decentralized exchanges like Uniswap grew 76 times, from $2.3 billion in Q1 2020 to $177 billion in Q1 2021;

2) The total value locked in DeFi increased 64 times, reaching $52 billion;

3) NFT art sales surged from $700,000 to $396 million, a growth of 562 times.

Ethereum's usage skyrocketed in the first quarter, although NFT sales slowed down, partly due to high gas fees and partly because the initial excitement had faded, but DeFi remained strong. Despite the surge in activity and trading volume, questions remain: what does this mean for Ethereum?

2. How Ethereum Makes Money

I have known about Ethereum for a long time. I first bought ETH in 2017, but that was speculative, and I ultimately did not get it. My biggest question about Ethereum is how it makes money. How does more activity on Ethereum translate into a higher ETH price?

In the near future, the answer will be that more transactions mean higher earnings for ETH holders, and the supply of ETH will decrease. But that is not how it works yet.

Let’s start with how it works today, look at the challenges of the current model, the proposed solutions, and what the future looks like.

Today, when you want to make a transaction on Ethereum, you need to use ETH. There are currently about 116 million ETH, and the price is loosely controlled by supply and demand. All else being equal, more transactions on Ethereum mean more demand for ETH, which means a higher price.

To maintain operation, Ethereum uses a proof of work consensus mechanism (PoW) to reach consensus on the state of the blockchain. To do this, miners around the world compete to solve increasingly tricky cryptographic puzzles to create a new block on the blockchain that contains new transactions. These puzzles are often hard to solve—requiring a lot of energy—but easy to verify.

When a block enters the blockchain, the transactions in that block officially become part of the record. The miner who successfully creates the block receives 2 newly mined ETH and all the transaction fees within the block.

Those transaction fees, known as gas, are what people pay to submit transactions to be included in a block. When a user sends ETH to someone on Ethereum, or mints an NFT, or does anything that requires on-chain verification, they must pay gas fees. Gas fees incentivize miners to spend the necessary funds in hardware and electricity to solve the puzzles and create blocks.

So currently, the price of Ethereum is based on a combination of supply and demand, as well as the price miners spend to secure the blockchain. To participate in the Ethereum network, you need ETH and need to pay gas. Miners receive ETH in the form of newly minted supply and gas.

This system has many challenges:

1) It is slow. Ethereum currently processes about 19 transactions per second. In contrast, VISA processes about 1,700;

2) It is expensive. The simplest transactions require about $5 in gas fees;

3) It is unstable. Gas fees fluctuate based on demand. This makes it difficult to transact with confidence or predictability;

4) It is inflationary. Unlike Bitcoin, there is no hard cap on the amount of ETH that can theoretically be minted, and proof of work requires minting a lot of new ETH, which dilutes the value of existing ETH holders;

5) It is environmentally unfriendly. Mining requires a lot of electricity;

6) It is inefficient. Much of the money spent on transaction fees leaves the system—miners are forced to sell the ETH they earn to pay for electricity, hardware, and taxes.

Despite all these challenges, Ethereum's adoption rate is impressive, but they remain real challenges. When I tweeted asking why people do not buy ETH, many answers revolved around one of the issues mentioned above, most commonly gas costs and inflation.

Additionally, the increasing demand for Ethereum-based DApps—more DeFi, more NFTs, more DAOs, more games—means more transaction fees, but these fees do not really accumulate to ETH holders. They leak out of the system to cover the real-world fiat costs of miners in the proof of work process.

So today, the price of ETH is based on demand for more ETH, just like Bitcoin and the dollar. It is not tied to revenue like a company, but it will soon be.

Proposed Solutions: EIP 1559 and ETH 2.0

One thing Bitcoin extremists love about Bitcoin is that you cannot really change it. One thing they dislike about Ethereum is that you can change it. It is not easy, but it is possible.

Ethereum is undergoing two changes aimed at addressing the challenges mentioned above.

EIP-1559 is a proposal that changes how it charges fees by splitting gas fees into a base fee and a tip. With EIP 1559, each transaction consumes a base fee, and miners (and soon validators) keep the tip. This may sound dull, but it is significant because burning could make ETH deflationary.

Additionally, tips allow those who value better block positions to pay more. For example, this could be important for DeFi participants trying to arbitrage. The proposal was approved in March and will take effect in July (as part of the London hard fork).

ETH 2.0 is an upgrade to the Ethereum blockchain itself, transitioning consensus from proof of work to proof of stake and introducing sharding. ETH 2.0 is expected to make Ethereum more scalable, secure, and sustainable. The PoS chain, or beacon chain, is already live and is expected to merge with the main chain sometime in late 2021 or early 2022.

Proof of stake is a shift in how network security is maintained and who receives rewards. This means that no one in the world needs to solve mathematical problems to mine blocks; ETH holders can validate block transactions based on the amount of ETH they hold. Validators protect the network in exchange for tips and rewards in the form of newly minted ETH.

Ethereum claims that PoS will be more secure because validators will hold ETH, and if they try to cheat, the price of ETH could be compromised. Critics argue that staking will concentrate more power in the hands of those who hold the most ETH, reducing decentralization and thus security.

In terms of scalability, sharding aims to increase throughput or transactions per second by creating 64 shard chains that validate transactions in parallel. Each shard only needs to validate a small portion of the entire chain, rather than every miner needing to validate the entire chain today.

Additionally, second-layer solutions like Polygon and Optimism are already working to accelerate transactions and lower fees by batching transactions off-chain and settling them on-chain in one transaction, rather than in many transactions (there is complexity, but this is close enough).

L2 solutions could increase throughput another 100 times, and if the theory holds in practice, the combination of Eth2 and L2 solutions could lead to a 10,000 times performance improvement.

Overall, EIP 1559 and Eth2 could be revolutionary for ETH holders as they improve performance while significantly changing where value is generated in the Ethereum ecosystem.

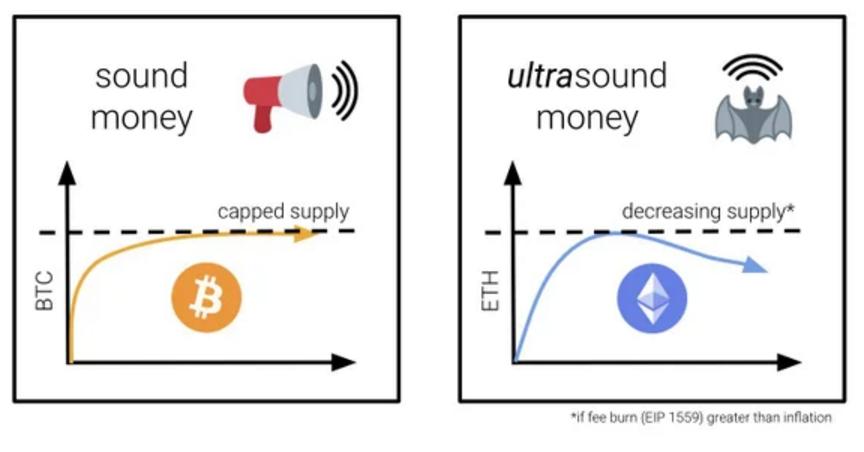

Future: Ultra Sound Money

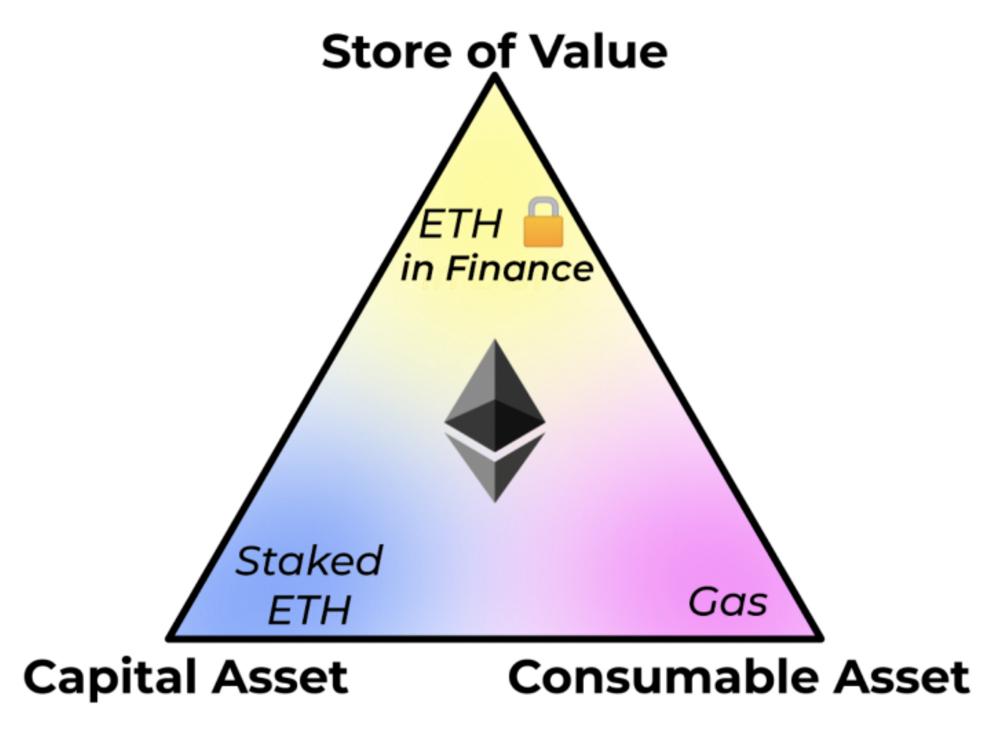

In 2019, David Hoffman wrote an article titled "Ethereum: A New Model of Money." In it, he quoted Robert Greer’s 1997 paper "What is an Asset Class Anyway?" and stated that there are three asset characteristics:

1) Capital assets are productive and generate value or cash flow. Examples include stocks, bonds, or rental real estate.

2) Convertible/consumable assets can be consumed once and converted into another asset, and their consumption generates economic benefits. Think of energy or commodities.

3) Store of value assets are scarce, cannot be consumed, only transferred, and their value persists over time and space. Examples include gold, currency, art, or Bitcoin.

Hoffman believes that Ethereum, as a Turing-complete, programmable currency, can simultaneously possess all three characteristics once EIP 1559 and Eth2 are implemented. He calls this the "triple point," a concept in thermodynamics where a substance can exist simultaneously in solid, liquid, and gas forms at the right temperature and pressure.

How they can occur simultaneously with Ethereum is beyond the scope here, but it is important to understand the three stages of Ethereum's existence:

1) Store of value. ETH is locked as collateral for DeFi transactions. For example, you can use ETH to obtain loans or provide liquidity for DEXs. Currently, nearly 10 million ETH are locked in DeFi;

2) Consumable asset. After EIP 1559 is implemented, gas fees will be like gasoline in a car. Anytime something happens on Ethereum, gas fees need to be burned, reducing the overall supply;

3) Capital asset. ETH acts as a capital asset in multiple ways. Owning ETH represents a share in the Ethereum network, just like owning equity in a company. Once staked, ETH grants its owner the right to work for the network by becoming a validator and collecting fees generated by the network.

3. Legitimacy and the Lindy Effect

Since Ethereum behaves somewhat like a company, along with the additional benefits of its own currency, we can analyze its strategic position like we would for a company. It benefits from branding and network effects.

In March, Ethereum co-founder Vitalik Buterin wrote an article titled "The Most Important Scarce Resource is Legitimacy," in which he stated that the true value of any crypto asset is not in truly owning that thing, but in its legitimacy. He defines legitimacy as:

Legitimacy is a higher-order pattern of acceptance. If people in a social environment widely accept and play a role in creating that outcome, and everyone does so because they hope others will do so as well, then the outcome in that social environment is legitimate.

If people believe that others believe in something, it makes more sense for them to believe in that thing and act accordingly. In the popular Ethereum podcast Bankless, hosts Ryan Sean Adams and David Hoffman refer to legitimacy as "the theory of everything in crypto." They list a series of questions people often ask about the space:

Why is the trading volume of cryptocurrencies over $2 trillion? Why are NFTs valuable? Why can't you fork your own Bitcoin and make it valuable? Why are we confident that Ethereum's monetary policy will only shift towards reducing inflation?

According to Adams and Hoffman, the answer to all these questions is legitimacy.

In this blog post, Vitalik highlighted six ways legitimacy is generated. Here are two particularly relevant ones:

Performance legitimacy: If the output of a process leads to satisfactory results for people, then that process can gain legitimacy (for example, successful dictators are sometimes described this way).

Continuity legitimacy: If something is legitimate at time T, it is by default legitimate at time T+1.

Performance and continuity create the Lindy effect, which states that the longer something has existed, the longer it is expected to continue to exist. Something that has existed for a year is expected to exist for another year, but something that has existed for 100 years is expected to exist for another 100 years.

This is an observable phenomenon. Amazon is more likely to exist in 30 years than a new startup, our children are more likely to listen to The Beatles than Olivia Rodrigo, and our grandchildren are more likely to read Socrates than Dan Brown.

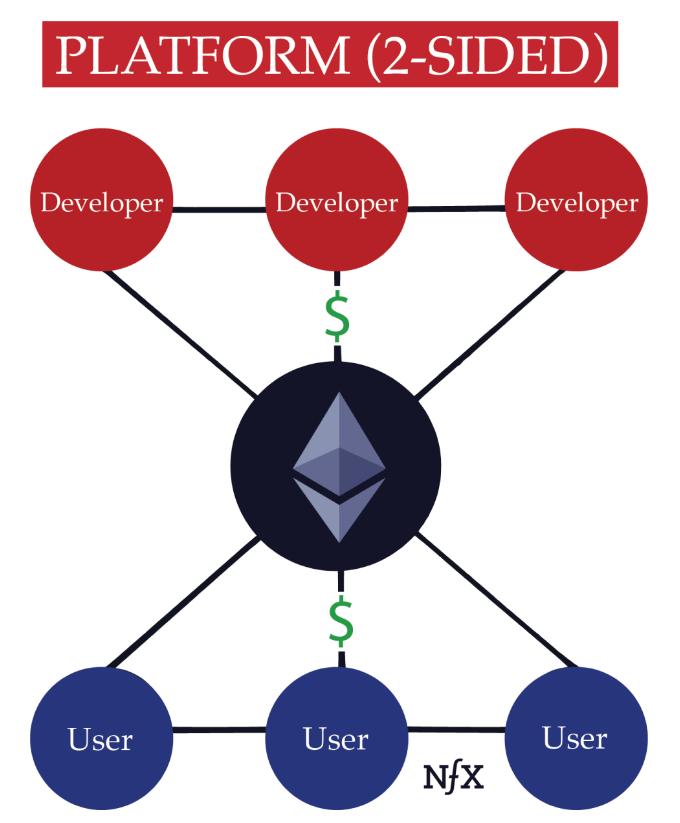

Legitimacy helps explain the Lindy effect, which states that the longer something has existed, the more likely people are to expect others to continue using it. In the case of Ethereum, more DApps on Ethereum mean more users on Ethereum, and more users mean it makes sense for more developers to build DApps.

iOS is an example of a platform with bidirectional network effects. The more people who own iPhones, the more likely developers are to create iPhone apps, and the more iPhone apps there are, the more likely people are to buy iPhones. In Apple's case, this network effect is so strong that it takes a 30% cut of all revenue from the App Store.

What makes Ethereum's network effect potentially stronger and more enduring is that it adjusts incentives in ways that traditional software does not.

Users and developers both hold ETH and benefit from its appreciation. As EIP-1559 and ETH 2.0 merge, the more ETH is used, the more value its holders will receive. Additionally, the more valuable ETH becomes, the harder it is to attack.

Hoffman, in "Ethereum: A New Model of Money," states that the fees paid to Ethereum validators act as a protective wall for Ethereum: "The height of the wall is highly correlated with the total fees generated by the network. The height of the wall is the cost of attacking Ethereum."

Ben Sparango from Solana took it a step further when we spoke, explaining that it is in the best interest of all parties for the value of the underlying blockchain to exceed the value of all DApps built on top of it. If this were not the case, it would incentivize bad actors to spend time attacking the blockchain to deplete the value of its DApps.

This means something very crazy: projects built on certain blockchains are financially incentivized to support the value of the underlying blockchain to protect their projects. They do not pay for AWS or security software; hosting and security are provided by the blockchain.

This is a different kind of platform network effect than others. It is hard to imagine an app voluntarily paying to boost Apple's stock price.

In the traditional software industry, the "Bill Gates line" created by Ben Thompson describes what makes something a platform:

A platform is when the economic value of everyone using it exceeds the value of the company that created it, and then it becomes a platform.

Ethereum has a built-in Bill Gates line. By owning and using ETH, and by using it to make ETH more valuable, the value of everyone using Ethereum exceeds the value of Ethereum itself. However, they are also incentivized to make Ethereum more valuable in the process. It makes the Bill Gates line irrelevant by tightly aligning incentives, blurring the Bill Gates line.

Importantly, this wall is also why narrative is so important and why the reflexivity of narrative is so powerful in cryptocurrency. More demand for ETH not only raises the price; it shifts some of the security burden from builders to investors, raising the wall, making the network more secure, and increasing the attractiveness of building on Ethereum, which makes ETH more valuable. This is a narrative-driven flywheel.

By definition, most of the value accrues to Layer 1 and to those holding Layer 1 tokens. It makes Layer 1, as the primary position in the value chain, the foundation of everything.

Thus, due to Ethereum's shortcomings so far, some L1 competitors have sprung up like mushrooms, trying to challenge Ethereum's dominance.

4. Ethereum's Bull Market Scenario

More demand and less supply lead to higher prices. The more fees, the fewer tokens.

EIP 1559 and ETH 2.0 will pass smoothly. This is certainly a risk, but people seem optimistic.

Ethereum will remain the primary L1 for Web3. At this point, Ethereum's network effect is too strong to overcome. Developers, users, and even other L1s are building or compatible with Ethereum.

If you believe all these things, then this is what the next bull market looks like.

Demand Will Rise

In the past year, demand across all categories, from DeFi to NFTs to the virtual world, has seen significant growth. Transaction fees have increased 200 times. All of this has happened in a context of poor usability and high gas fees.

The past year has been unprecedentedly bad for Ethereum. For several reasons, it will only get better from here. First, assuming EIP 1559 and ETH 2.0 merge as planned, transaction speeds will increase, and gas fees will become lower and more predictable. Transactions will be easier and cheaper. Lower transaction fees and faster transaction times should lead to more transactions.

Second, even if what we just experienced was a bubble, short-term bubbles can be useful in the long run. They attract money and talent to this space, and money and talent will merge to create new products that attract new users and more demand.

In just the past few months, I have seen dozens of strong teams leave traditional startups to build web3 products, many of which are on Ethereum. More products and better experiences will attract more users. ETH is an exponential bet on this growth, rather than betting on the success of any one project.

Strong trends, lower prices, better experiences, and new products = growing demand.

Supply Will Decrease

For many ETH bulls, this is the crux of the argument: EIP 1559 means ETH becomes deflationary.

Bitcoin has a capped supply of 21 million. This is the strongest bull case for BTC. You cannot print more money like an evil central bank; it is a mathematical thing and is limited.

Ethereum's supply currently has no cap. Theoretically, enough Ethereum users could decide to continue minting ETH and increase the supply. If you are going to have an inflationary asset, why not just use fiat currency?

But EIP 1559 and Eth2 disrupt this. With ETH 2.0, the new issuance to reward validators is expected to decrease significantly. With EIP 1559, by burning ETH in each transaction, assuming daily transaction fees are conservative and 70% of gas fees are burned, with 30% sent as tips, then the ETH burned daily will exceed the ETH issued.

Even crazier, if people and institutions hold BTC as a non-inflationary store of value, could they switch to Ethereum? Could Ethereum surpass Bitcoin to become the most valuable cryptocurrency?

Value for ETH Holders Will Increase

Owning ETH also grants the right to work for the Ethereum network as a validator and receive a portion of the fees.

In proof of work, miners need to sell the ETH they earn to cover costs. According to another model by Justin Drake, today this creates a daily sell pressure of 22.3k ETH, meaning about $50 million worth of ETH is thrown onto the market daily.

With proof of stake, the only cost is taxes; Drake assumes a 50% tax, and new issuance drops from 13.5k ETH to 2.1k ETH, leading to a reduction in net sell pressure from 22.3k ETH per day to 2.6k ETH per day. This equates to about $40 million in new demand daily.

Additionally, value will not leak out of the Ethereum system but will accrue to validators. Another model by Drake estimates that those staking their ETH (meaning locking it up to secure the network) could earn a 25% annual return.

5. Risks, Warnings, and Conclusion

Part of the reason I am so bullish on ETH assets is the potential of Ethereum technology excites me. Last weekend showcased the volatility of cryptocurrencies, and everything is still tied to Bitcoin. If you were trading ETH quickly, this weekend could be nauseating. If you are involved because you want to learn and explore web3, then this is a great opportunity to buy more tokens at half price to play the game.

While I am overall bullish, Ethereum faces real risks, both macro and specific.

On the macro level, what if Terra collapses? What if governments crack down on cryptocurrencies broadly? What if interest rates rise early and risk assets shrink? What if Musk tweets again? One of the scariest things about last weekend's sell-off was the lack of a clear catalyst. The crypto market can be crazy.

Somewhere between the micro and macro, there is a question: what if people outside early adopters really do not care about decentralization? What if more centralized solutions like Binance Smart Chain, which have millions of built-in users trading on Binance, are sufficiently decentralized and perform better?

On the micro level, Ethereum faces some real challenges. What if EIP 1559 does not pass as planned? What if Eth2 is delayed? What if sharding does not work as planned, and the problems it creates outweigh the improvements? A very real possibility is that sharding reduces the composability of Lego blocks built on Ethereum, weakening one of the most exciting aspects of the network.

Perhaps the biggest issue ETH faces is the adoption of decentralized second-layer scaling solutions. While L2 solutions have the potential to significantly improve performance, they pose a major challenge: adopting fragmented L2 solutions may make composability more difficult, as executing on L2, resolving on L1, and then returning to another L2 for the next part of the transaction.

Ideally, one or two L2 solutions will win out, but a world with multiple L2s may strengthen Ethereum's network effect while weakening the product experience.

If all goes well, I hope this article changes your perspective on Ethereum and makes you want to continue exploring it for yourself. That is the fun of it here.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles