Messari interprets MakerDAO: How should the decentralized stablecoin protocol build a moat?

MakerDAO has generated over $72 million in net income for MKR holders in the past 12 months, and the total supply of DAI has increased by 46 times.

MakerDAO has generated over $72 million in net income for MKR holders in the past 12 months, and the total supply of DAI has increased by 46 times.Original Title: "MakerDAO Valuation: How to Build a Moat?"

Written by: Francois-Xavier Lord, Messari Hub Analyst

Edited by: Nan Feng

Source: messari.io

Introduction

Due to the recent boom in DeFi, the demand for stablecoins has surged, pushing the total supply of stablecoins beyond the $100 billion mark. While the necessity of stablecoins in DeFi for liquidity and hedging against volatility has become evident, the long-term sustainability of centralized stablecoins is now increasingly concerning. Centralized stablecoins face growing regulatory uncertainty and opaque reserves, forcing many users to seek more transparent alternatives.

In this context, MakerDAO and its stablecoin DAI have become the most successful decentralized stablecoin protocol to date, with DAI's total supply growing 46 times over the past 12 months, generating over $63 million in net income since 2021.

In this article, we will focus on the core building blocks of the DeFi infrastructure stack, the Maker protocol, and the metrics behind its governance token MKR.

About MakerDAO

History of MakerDAO

Founded in 2015, MakerDAO is a stablecoin project operating on the Ethereum blockchain based on an over-collateralization model. The inception of MakerDAO was based on the recognition that early cryptocurrencies were highly volatile, making them not very useful as a medium of exchange. The project's development was initially led by the Maker Foundation but is now controlled by a DAO organization.

The protocol was officially launched in 2017, initially as a single-collateral DAI system (also known as SAI), allowing users to mint the stablecoin DAI using ETH as collateral. That same year, Maker raised $12 million by selling MKR tokens to Andreessen Horowitz (a16z), Polychain Capital, and other cryptocurrency-focused venture capital firms.

Following the successful launch of single-collateral DAI, Maker introduced the multi-collateral DAI (MCD) system in 2019, accepting a wider variety of collateral types beyond ETH.

In May 2020, seven months after the launch of MCD, the total supply of DAI reached $100 million. More than a year later, in June 2021, the total supply of DAI has now exceeded $5 billion.

Project Description

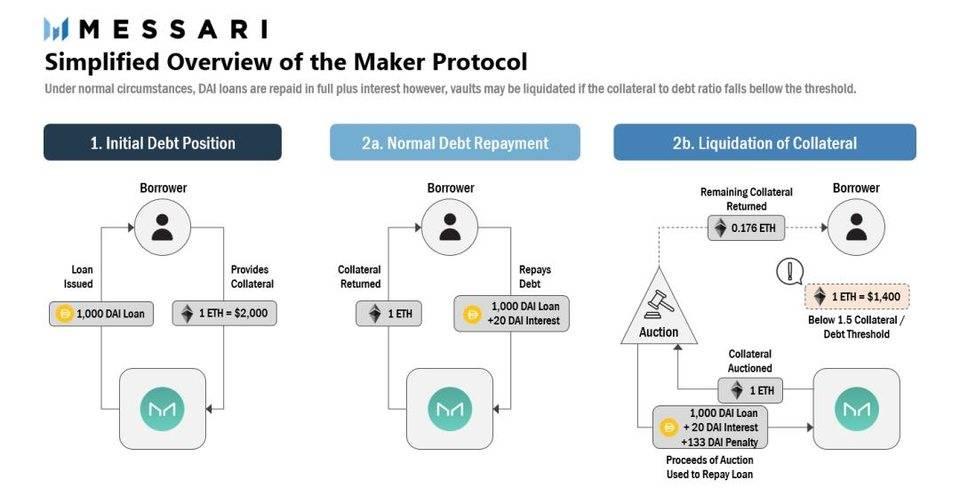

The Maker protocol allows users to issue and borrow DAI, a stablecoin pegged to the US dollar, by over-collateralizing assets in a system vault. Maker currently supports various types of collateral, including volatile crypto assets, other stablecoins, liquidity tokens, and real-world assets (RWA).

DAI combines the advantages of low-volatility currencies with the key attributes of cryptocurrencies (permissionless, borderless, transparent, peer-to-peer, etc.). DAI is generated, backed, and maintains its value stability through collateral assets stored in Maker protocol vaults, such as requiring $1,000 worth of ETH to be deposited in the vault as collateral to issue 500 DAI. This, along with the adjustable interest rates on DAI loans, ensures that the value of DAI remains equal to $1.

When DAI is issued, the vault owner takes out a loan against their deposited assets as collateral, similar to any other form of mortgage. If the value of the collateral in the vault falls below a certain threshold, the position (i.e., collateral) can be liquidated according to the Maker protocol to repay the DAI debt. Under normal circumstances, the vault owner will repay the DAI loan with interest to regain control of their collateral.

The revenue generated by the Maker protocol primarily comes from three sources:

- Interest income from over-collateralized loans;

- Liquidation fees charged on liquidated vaults;

- Stablecoin trading fees generated by the Peg Stability Module (PSM).

Note: The PSM module of the Maker system allows users to directly exchange other stablecoins for DAI at a fixed exchange rate (including a 0.1% fee). The main purpose of the PSM is to help maintain the peg of DAI to the US dollar. Additionally, the PSM allows Maker to adjust the collateral structure based on market demand for loan services.

Maker Token Economics

MKR is the governance token of the Maker protocol, allowing its holders to vote on protocol changes, such as adding collateral types, changing governance parameters, approving budgets, and more.

In cases where liquidations do not fully cover outstanding DAI debts, MKR tokens are also responsible for the capital restructuring of the protocol. In such cases, the protocol will mint and auction MKR tokens (which will dilute the supply of MKR) to repay the protocol's outstanding debts and ensure the system's solvency.

The revenue generated by the Maker protocol indirectly belongs to token holders. Currently, the cash flow generated by the protocol is primarily used for three purposes:

- Paying for the development and operational costs of the Maker protocol;

- Establishing a safety buffer to cover potential liquidation losses;

- Buying back and burning MKR tokens from circulation.

Thus, conceptually, holding MKR can be compared to holding equity in a bank that is continuously repurchasing its stock.

Of the initial supply of 1 million MKR tokens, approximately 907,000 MKR are still in circulation. This is due to the protocol having repurchased and burned about 9,000 MKR, and the Maker Foundation transferring 84,000 MKR to its DAO organization as part of its dissolution process in May 2021.

Recent Developments

Here are some notable recent developments of the Maker protocol:

Dissolution of the Maker Foundation: As of now, the Maker Foundation, which was responsible for most of the development of the Maker protocol, announced in May 2021 that it would gradually transfer development and governance responsibilities to the DAO, thereby accelerating the dissolution of the foundation. As of the end of July, the dissolution and transition have been largely completed.

Real World Assets (RWA) as Collateral: In April 2021, Maker began issuing loans collateralized by real assets (RWA) to real estate investment loan service provider New Silver. This bridge connecting traditional finance and the decentralized finance world is an important milestone for Maker and DeFi as a whole.

With strong community support, RWA-backed loans provide Maker with a $1 trillion growth opportunity, which also helps diversify the risk of DAI collateral into assets unrelated to cryptocurrencies.

- Liquidation 2.0 Module: Since the Black Thursday event in March 2020 (which led to $5.67 million in under-collateralized DAI loans), Maker has made several improvements to its liquidation system. In the first half of 2021, Maker released a new Liquidation 2.0 module. This module has proven to be very effective in reducing losses.

On May 19, 2021, amid a 45% drop in ETH value, this module settled $41 million in debt through 177 auctions, generating $5.1 million in liquidation fee revenue, but only incurred a total of $12,000 in liquidation losses.

Traction

Supply and Demand for DAI

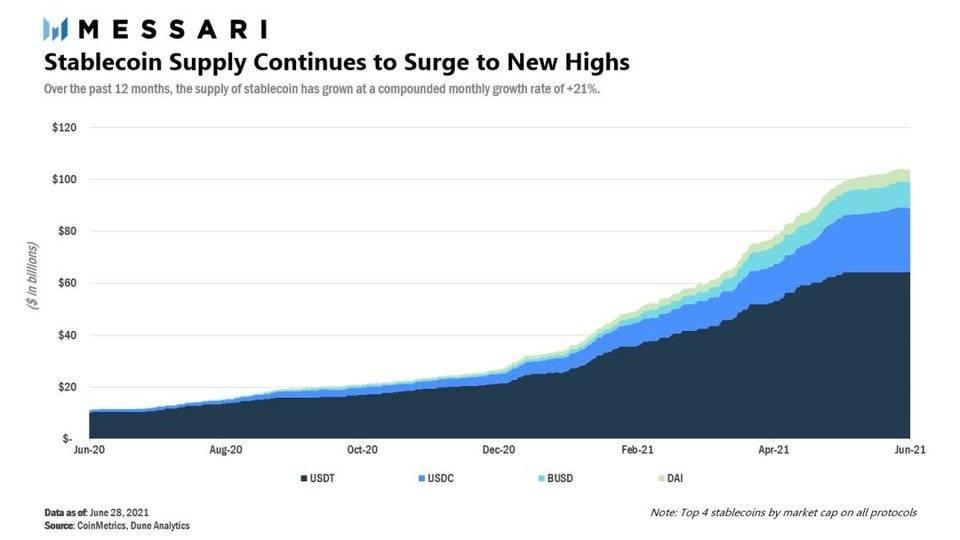

With the rise of the DeFi ecosystem, stablecoins like DAI have experienced tremendous growth as key drivers of decentralized lending and trading activities. Over the past 12 months, the stablecoin market has grown from $11 billion to now over $100 billion.

Above: Growth trend of stablecoins USDT, USDC, BUSD, and DAI since June 2020.

The total supply of stablecoins has surged tenfold year-on-year, driven by continuous capital inflows into the crypto economy and the expansion of DeFi scale. The popularity of stablecoins can also be attributed to their inherent characteristics, providing a low-volatility safe haven for investors while retaining all key attributes of cryptocurrencies.

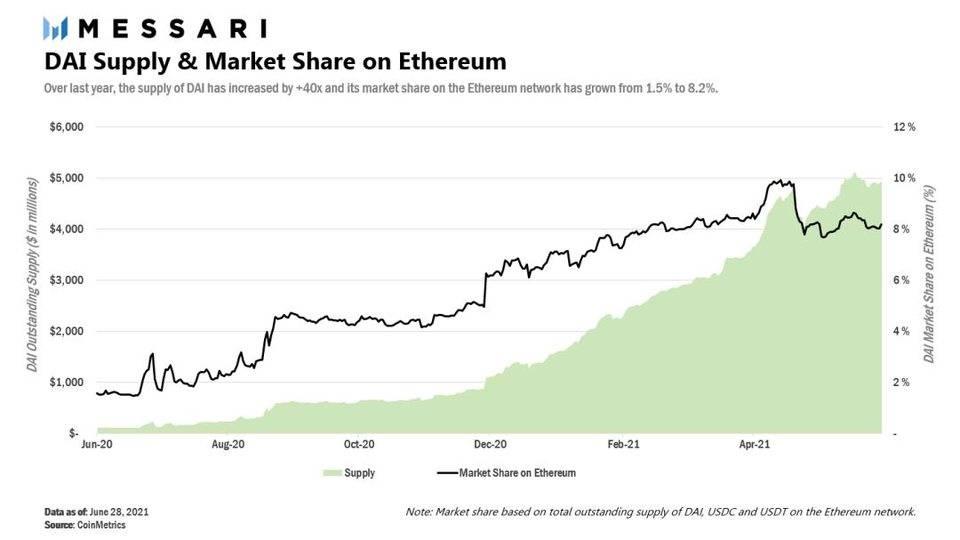

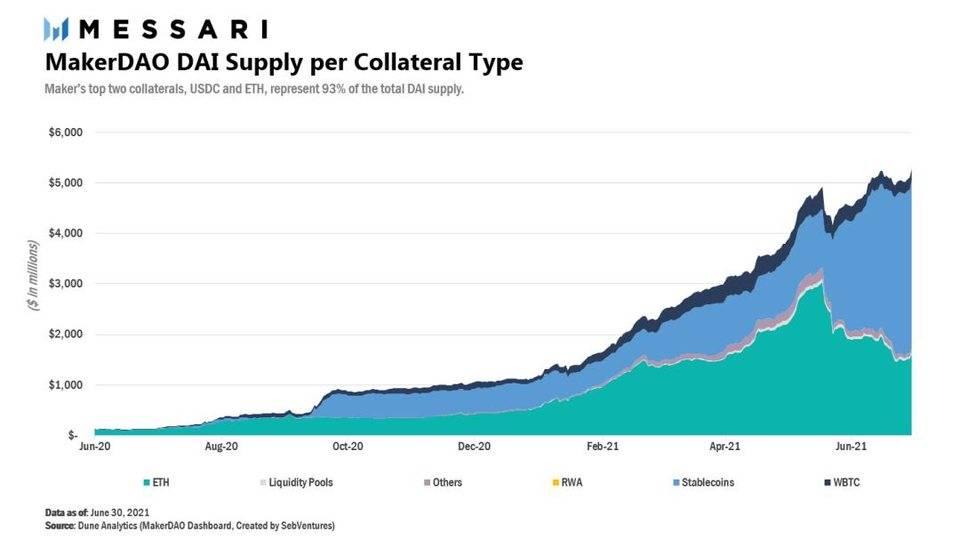

Maker has been able to benefit from this growth, increasing its outstanding DAI supply from $127 million to over $5 billion in the past 12 months. DAI currently holds an 8.2% market share in the stablecoin market on Ethereum. By market capitalization, DAI is the fourth-largest stablecoin.

Above: Growth trend of DAI's supply (green area) and its market share in the stablecoin market on Ethereum (black line) since June 2020.

Given the increasing regulatory risks surrounding stablecoin issuance and reserves, particularly from the EU, the US, and China, DAI has a strong competitive advantage over larger centralized stablecoins. The reserves of MakerDAO can be audited on-chain, while projects like USDC and USDT must rely on external audits. For example, USDT has recently faced increasing scrutiny as the sources and credit quality of its reserves have come under question.

There is a trade-off between the centralized risks of fiat-backed stablecoins (like USDT) and the volatility risks of trust-minimized crypto assets (like ETH). So far, Maker has demonstrated a strong ability to withstand volatility through its liquidation module, thereby gaining user confidence.

Performance of the Maker Protocol to Date

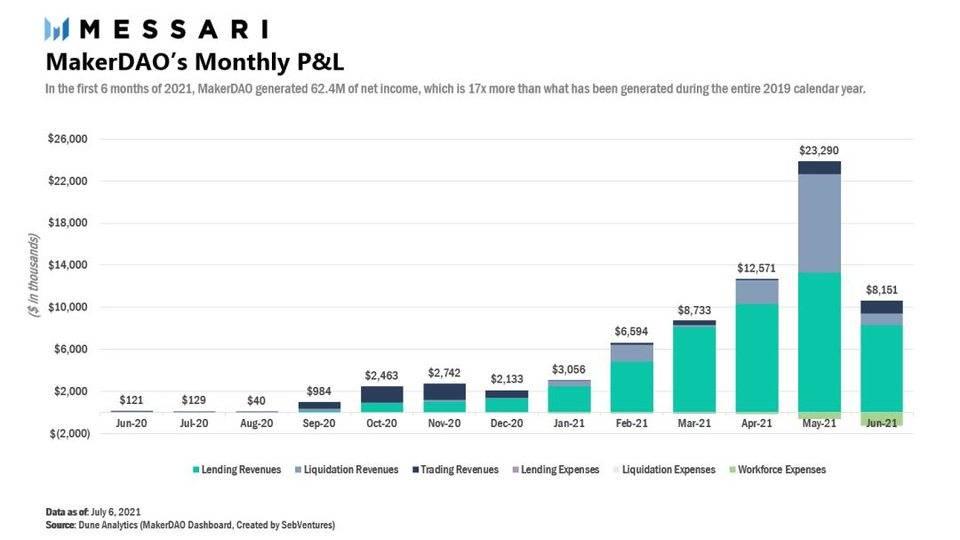

The demand for loans and DAI has driven Maker's monthly net income to soar, with profits exceeding $63 million in the first six months of 2021, representing more than a sevenfold increase compared to the last six months of 2020. This performance can be broken down as shown in the figure below:

In the first half of 2021, the Maker protocol earned an average of about $7.7 million per month in interest income from DAI loans, a 13-fold increase compared to the second half of 2020. This growth is directly attributable to the increase in loan volume and higher loan rates.

The interest rate on DAI loans has gradually risen from 2% at the end of 2020 to 5% in April/May 2021; due to a decrease in market demand for leverage, the current interest rate on DAI loans is at 2% (for the ETH-A vault). The interest income from DAI loans is the most frequent and stable source of revenue for the Maker protocol.

For liquidated vaults, the Maker protocol charges a 15% liquidation fee as a penalty, which contributes significantly to the protocol's liquidation revenue. Liquidation revenue has also contributed considerably to Maker's strong performance. Thanks to significant market volatility, the monthly liquidation revenue in May 2021 soared to $9.4 million. By charging liquidation fees (assuming orderly liquidations), MKR tokens also benefit from the decline in collateral value.

Over time, this means that MKR tokens may have a lower downside correlation with the overall market. However, it should also be noted that as third-party loan management solutions improve and collateral volatility decreases, we expect the volume of liquidations to decrease over time.

Trading revenue refers to the stablecoin exchange fees generated by Maker's PSM (Peg Stability Module). The fee income generated by the PSM significantly increased in May and June 2021 due to rising demand for DAI, while the demand for borrowing DAI through collateralized cryptocurrencies decreased. As a result, the protocol has directly exchanged over $3 billion of USDC for DAI to meet the demand for DAI.

Thus, DAI is a dynamic system that adjusts its collateral according to market conditions and demand. As the crypto market expanded in the first half of 2021, the system fully leveraged the demand for leverage, using ETH as its primary reserve for loans. After the recent decline from the market peak, the system adjusted its reserves by flowing into other stablecoins to maintain and continue growing the supply of DAI.

This flexibility and resilience are core advantages of the Maker protocol, representing the unique characteristics of DAI compared to other stablecoins.

Roadmap

Here are some key initiatives and upgrades that the Maker protocol is set to implement:

Implementation of the Flash Mint Module: After being voted in on July 1, 2021, the Maker protocol activated the Flash Mint module. This module allows users to mint up to 500 million DAI, with the only condition being that users must repay these DAI loans in the same transaction and pay a fee of 0.05%. This will allow anyone to take advantage of arbitrage opportunities in the DeFi space without upfront capital and create new revenue streams for the Maker protocol.

Multichain Sidechains: The community is developing a multichain strategy for Maker to ensure the protocol remains significant across multiple blockchains. Additionally, developers are working on an Optimism DAI bridge that will allow users to quickly withdraw from Optimism (L2 rollup chain) to the Ethereum main chain, expected to be fully deployed in Q3/Q4 of 2021.

Aave D3M: Maker is collaborating with the Aave team to launch the Maker Direct Deposit Module (D3M). This module will allow the Maker protocol to implement the maximum borrowing rate on the DAI market on Aave. Ultimately, this will help MakerDAO achieve capital efficiency, increase the supply of DAI, and make DAI the preferred choice for stablecoin borrowers on Aave.

Competition

Maker faces competition in both the stablecoin market and the collateralized lending market.

As emphasized earlier, DAI has achieved significant growth in market share over the past 12 months compared to other centralized stablecoin competitors. We believe this trend will continue in the future. DAI has a strong competitive moat due to its decentralized nature, transparent reserves, and increasingly prominent position in the DeFi ecosystem.

The regulatory and transparency risks faced by fiat-backed stablecoins, along with the low reliability of algorithmic stablecoins, may further drive DAI's competitive advantage over time.

DAI also has the potential to create a low-volatility currency backed by physical assets (crypto assets, RWA, etc.). In the long term, DAI could decouple from the US dollar and be pegged to a specific basket of commodities.

In terms of competition in the lending market, Maker can provide more certainty in the rates charged by the protocol compared to variable-rate competitors like Aave or Compound. Furthermore, as long as the variable rates of lending protocols like Aave or Compound are higher than Maker's stability fee, Maker can benefit from these lending protocols: market participants can borrow from Maker and lend at higher rates in these lending protocols, and if their collateral value declines, they can repay the loan at any time.

Risks

Since MKR token holders are responsible for the capital restructuring of the Maker protocol, if liquidations do not fully cover DAI loan debts, MKR holders will need to bear a certain degree of credit risk. As of the time of writing, Maker's surplus buffer ($48 million) is serving as a mitigating factor, while the largest collateral types USDC, ETH, and BTC are valued at $3.3 billion, $1.6 billion, and $230 million, respectively.

MKR token holders also face counterparty risks due to allowing USDC and RWA as collateral, although the current exposure to RWA remains small.

DAI's increasing reliance on USDC presents Maker with significant regulatory and blacklist risks, as Circle may blacklist some of Maker's USDC reserves. This also highlights a particular dilemma faced by Maker, where the current demand for DAI exceeds the demand for loans.

We believe that the reliance on USDC is a necessary temporary setback for Maker, as broader DAI adoption is crucial for the overall success of the protocol. We note that the Maker community is currently exploring alternatives to address this issue, such as investigating the use of new Uniswap V3 liquidity tokens.

Maker also faces risks related to protocol development and technology. We believe these risks are relatively low, given the external smart contract audits that have been conducted and the reputable core development team.

As changes to the Maker protocol now depend on its DAO organization, MKR holders will face governance-related risks. Although there are some built-in safety mechanisms to mitigate potential governance attack vectors, we believe that the governance process needs improvement and streamlining to minimize governance risks.

In particular, the DAO organization often has to address the issue of low voting participation rates among MKR token holders. This may limit Maker's ability to respond quickly to market changes and pose security risks, as attackers may borrow MKR to conduct unfavorable votes. The DAO is currently developing an improved voting delegation system to help address this issue.

Conclusion

Maker positions itself as a top competitor in the stablecoin and lending markets, which are two fundamental components of the currently active DeFi ecosystem. This enables Maker to scale and has generated over $72 million in net income for MKR holders over the past 12 months.

With strong support from its development team, community, and growing user base, we believe Maker will continue to maintain its growth momentum in the coming years.

However, to achieve the valuation outlined in this article, the protocol needs to overcome various challenges, such as narrowing the gap between DAI demand and loans through innovative solutions like RWA (real-world assets). We expect to see the market supply of DAI continue to grow and the burning of MKR tokens.

This report was prepared by Messari Hub analysts at the request of Messari Hub member MakerDAO, with some content omitted in the Chinese translation. All content is independently produced by the author and does not represent the views of Messari, Inc. or the organization requesting the report. The author of this article may hold cryptocurrencies mentioned in this report.

Risk warning

Risk warning Risk warning

Risk warning