Analyze the competitive landscape of the three major lending platforms from the dimensions of TVL, outstanding loan balance, and capital utilization rate

Aave, Compound, and MakerDAO, who will become the king of lending platforms.

Aave, Compound, and MakerDAO, who will become the king of lending platforms.Written by: Bella, Analyst at the crypto data analysis platform Footprint

Original Title: "With Such Great Changes, Who Will Be the King of Lending Platforms?"

As user demand for lending grows, the development of lending DeFi has been rapid, and competition among platforms is fierce. The significant drop in cryptocurrency prices in May has led to a reshuffling process for leading lending platforms. More than two months have passed since the price drop in May. Below, we analyze and evaluate through multiple indicators which of the leading lending platforms—Aave, Compound, and MakerDAO—will become the king of lending platforms.

1. TVL

Changes in TVL across different platforms __ Data source: Footprint

Lending platforms are rapidly developing, Aave has surpassed MakerDAO

The lending platforms experienced a period of rapid growth in 2021. Although there was a slight setback in May that slowed the pace of development, it did not affect the overall momentum. At the beginning of the year, the total TVL of the top three lending platforms was $6.88 billion, which continued to grow. By mid-May, TVL had reached $39.06 billion, setting a new historical high. From the beginning of the year to the peak on May 12, the total TVL increased by 5.67 times, with a growth rate of 467.7%.

Due to the impact of the significant drop in cryptocurrency prices in May, the total TVL returned to the levels of April, hitting a low on May 23 with a decrease of 42.7%. Although there were some fluctuations at the end of June, by the end of July, Aave had surpassed MakerDAO and exceeded the peak created in May. Starting in August, all platforms showed strong growth momentum, especially Aave, which had a TVL of $13.35 billion before publication, making it the platform with the highest TVL in current DeFi applications.

Changes in TVL across different chains Data source: Footprint

Aave's cross-chain deployment helps it rank first

To reduce the trading congestion and high transaction costs on the Ethereum chain that negatively affect user trading experiences, Aave was the first to attempt deployment on the Polygon chain, which offers a similar user experience but lower transaction costs. This move undoubtedly attracted more users active on the Polygon chain and drew in more novice users who were new to lending transactions.

In April, Aave completed its deployment on the Polygon chain, and the TVL on the Polygon chain gradually increased. In just over two months, it achieved a breakthrough from $0 to $3.8 billion, accounting for 76% of the total TVL on the Polygon chain. This achievement significantly contributed to Aave surpassing MakerDAO in June, ranking first among lending platforms and leading the DeFi TVL leaderboard.

Changes in TVL share across different platforms Data source: Footprint

Intense competition among leading lending platforms, Aave surpasses Compound and MakerDAO

According to the TVL market share data provided by Footprint, the competition for the top market share platform this year has been fierce. From January to March, MakerDAO ranked first, with its TVL accounting for 40%-43% of the market share during that period. Starting in April, as Compound's token price rose rapidly again, it leveraged its pioneering "lending mining" model to provide mining subsidies to depositors and borrowers, increasing depositor returns while lowering borrowing rates, attracting more users and gradually eroding the market shares of MakerDAO and Aave to reclaim the top position. Subsequently, as Aave also activated its liquidity mining program and expanded cross-chain, capital in the lending platform shifted again, and Compound gradually lost its market share, allowing Aave to overtake it. As of the time of publication, Aave's market share was approximately 42%.

2. Deposit Volume

Changes in Deposit (funds on deposit) across different platforms Data source: Footprint

Compared to the beginning of the year, Aave grew by 567.6%, Compound by 299.5%, and MakerDAO by 112.9%

For lending platforms, the amount of funds on deposit is a key indicator for assessing a platform's capability. This indicator not only affects the platform's locked-up amount but also the amount of funds available for lending. As lending platforms diversify and improve security and compliance, the number of users and the amount of funds deposited to earn returns continue to grow.

Compared to the beginning of the year, with $8.89 billion in deposits, by the end of July, the deposit amount had reached $36.75 billion, which is 4.13 times that of the beginning of the year. MakerDAO, focusing solely on stablecoin DAI lending, had a growth rate of only 112.9%, far below the average; Compound, which focuses on lending mining, had a growth rate of 299.5%, higher than MakerDAO, but this growth rate was mainly limited by the limited variety of listed assets, with only 15 assets available at the time of publication; Aave, due to its wide range of business types (including floating rate lending, fixed rate lending, AMM loan markets, flash loans, credit delegation, etc.), a large variety of listed assets (up to 28), and the launch of liquidity mining to provide subsidies to users, achieved a growth rate of 567.6%.

Changes in Deposit (funds on deposit) share across different platforms Data source: Footprint

Platforms with continuous innovation in development models see sustained increases in deposit amounts

Looking back at the trend of deposit market share changes over the past seven months, Compound has maintained a relatively stable share of around 37%-40%. Although it showed an expanding trend in April, peaking at 48.5%, it later returned to its original level due to Aave's new model attracting more deposited funds.

In contrast, the market share division between Aave and MakerDAO has varied significantly. Aave has continuously eroded MakerDAO's market share, increasing from only 27% at the beginning of the year to 45% by July, with a trend of further expansion. This indicates that Aave's continuous innovation, optimization, and iteration play a significant role in the platform's development. Meanwhile, MakerDAO, focusing on stablecoin lending, has not updated or iterated its development model significantly, leading to a gradual reduction in its market share.

3. Outstanding Balance Performance

Changes in Outstanding (loan balance) across different platforms Data source: Footprint

Aave surpasses Compound in outstanding balance

From the development trends of each platform's Outstanding (loan balance), the lending market has seen a surge in demand as DeFi develops. At the beginning of the year, the Outstanding balance was only $3.52 billion, but by the end of July, it had reached $19.66 billion, achieving a growth rate of 458.5% in just seven months. Although the cryptocurrency market was affected by policies in mid-May, causing various token prices to plummet, this event did not have a significant impact on lending DeFi applications. The drop in token prices triggered liquidation rules across platforms, reducing outstanding balances, but subsequently, all platforms showed growth, and two months later, the outstanding balance had surpassed the levels seen in May, indicating that the growing demand for lending has enhanced resilience in extreme situations.

The significant drop in cryptocurrency prices in May can be seen as a good opportunity for lending platforms, as the outstanding balances of each platform essentially returned to the same starting line. In the subsequent phase, MakerDAO maintained a relatively stable outstanding balance, while Aave stood out, with its outstanding balance by the end of July being comparable to Compound's, and by early August, it had already surpassed Compound.

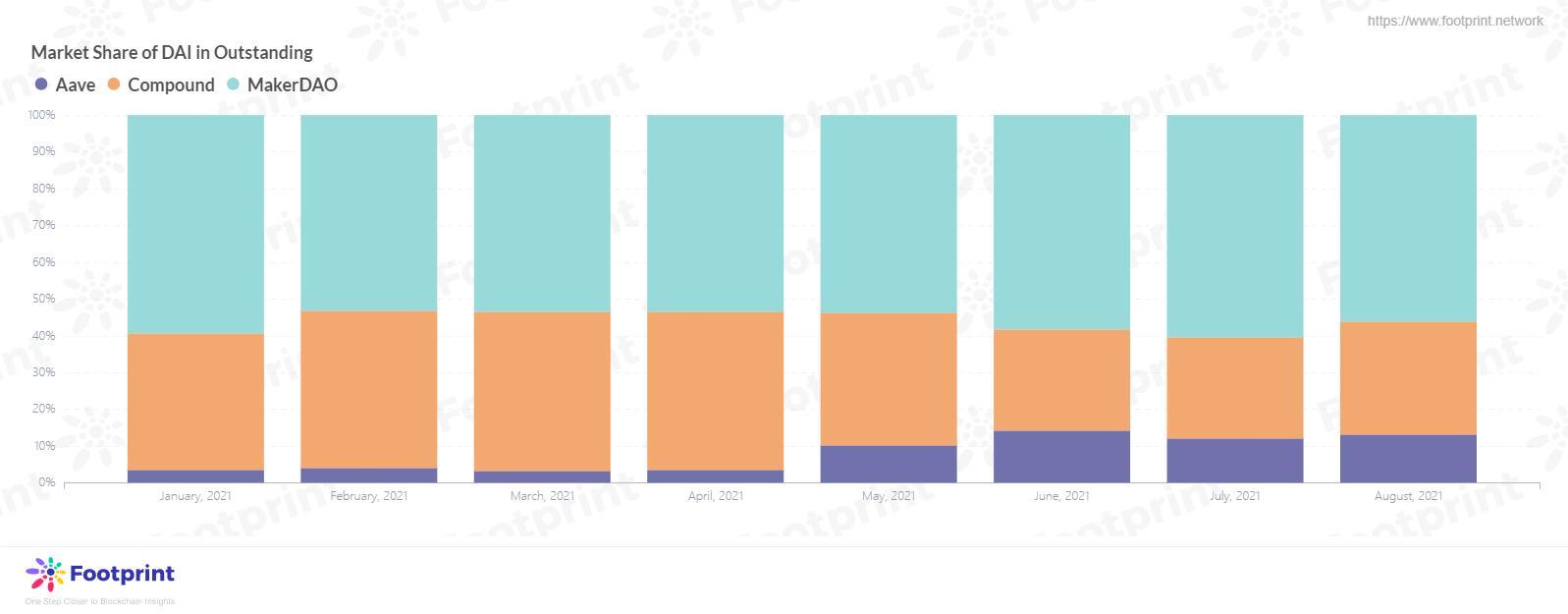

Composition of assets in outstanding balance Data source: Footprint

USDC & DAI become the main competition among leading lending platforms

We break down the asset composition of the outstanding loan balances of the top three lending platforms. By the end of July, the most borrowed asset was DAI, with an outstanding loan balance of $9.88 billion, accounting for half of the total outstanding loan balance; closely following was USDC, whose demand has grown rapidly, increasing from only 20.1% of the total at the beginning of the year to 36.5% by the end of July. This rapid market capture poses a strong competitive threat to the leading DAI; USDT ranked third with 8.1% of the total; WETH ranked fourth with 2.5%; the remaining asset categories accounted for 2.5% of the market share, which will not be detailed here.

From the breakdown of asset category shares above, it is evident that the current demand for stablecoins exceeds that of other types of tokens, primarily due to the high liquidity and wide applicability of stablecoins. This situation has led lending platforms to continuously add stablecoin asset pools, providing higher returns to users who supply stablecoins, thereby expanding their market share.

Share of leading assets DAI & USDC in outstanding balance across different platforms

Data source: Footprint

Changes in share of leading asset DAI in outstanding balance across different platforms

Data source: Footprint

Changes in share of leading asset USDC in outstanding balance across different platforms Data source: Footprint

Data source: Footprint

MakerDAO holds a major market share of DAI, while Aave maintains strength in USDC

Overall, at the beginning of the year, platforms Compound and MakerDAO held the vast majority of the loan market share for assets DAI and USDC. With Aave launching liquidity mining, its share has gradually expanded. Currently, the shares of the top three lending platforms are becoming more balanced. For future development trends, it is expected that MakerDAO's share will gradually be eroded by the other two platforms.

Why do I say this? First, MakerDAO currently focuses on DAI lending. Although it holds about 58% of the total outstanding DAI, Aave has been accumulating strength, making it challenging for MakerDAO to maintain its current market share. Second, the demand for USDC has surged, and whether USDC can occupy the same market share as DAI and surpass DAI is just a matter of time. However, MakerDAO does not provide a USDC asset pool, which increases the likelihood of a reduction in MakerDAO's market share.

In contrast, Aave continues to expand its outstanding balance share for both DAI and USDC, especially USDC, which will be a strong competitor to MakerDAO.

4. Asset Utilization Rate

Composition of assets in deposited funds Data source: Footprint

DAI maintains the highest asset utilization rate, followed closely by USDC

When discussing asset demand, one must mention the amount of assets deposited. For users, the greater the demand for asset pools of each category on the platform, the higher the returns for depositing that category of assets, and the higher the costs for users borrowing those assets. This is related to the asset utilization rate of the pools.

From the categories of deposited assets, the most deposited asset is WETH, accounting for 36.2% of the total. The high deposit amount of WETH is mainly due to borrowers depositing WETH as collateral to borrow other asset categories. The second and third positions are stablecoins, with USDC accounting for 28.7% in second place and DAI accounting for 16.2% in third place; WBTC occupies fourth place with a market share of 7.1%.

Considering the deposit and borrowing amounts of various asset categories, the demand for stablecoin DAI ranks first, but its deposit amount is only in third place. Therefore, the utilization rate of this asset category is the highest. In lending platforms, the interest rates for depositing and borrowing DAI are also the highest among many assets, followed closely by USDC.

Changes in asset utilization rates across platforms Data source: Footprint

MakerDAO has a high asset utilization rate, followed closely by Aave and Compound

From the comparison of asset utilization rates among leading platforms, it can be seen that MakerDAO has the highest asset utilization rate, while Compound and Aave have similar asset utilization rates, maintaining levels around 45%-50%.

The distribution of asset utilization rates can also be linked to the operational models of the platforms. For MakerDAO, users can deposit and stake different types of assets to obtain DAI, and the deposited assets are generally converted into DAI based on the staking rate, resulting in a higher asset utilization rate. In contrast, Aave and Compound both provide liquidity mining rewards to users who deposit and borrow funds, which means that users with idle funds who may not necessarily need to stake or borrow can deposit funds to earn relatively higher returns compared to other types of DeFi, resulting in lower asset utilization efficiency.

For platforms, a relatively high asset utilization rate can attract more funds to be deposited, activating the platform's liquidity pool, and increasing the platform's revenue, achieving a win-win situation. However, this is also a double-edged sword for the platform, as a significant security incident could lead to insolvency, putting the project at risk of bankruptcy.

Conclusion

Through the analysis of multiple indicators above, it can be determined that Aave has surpassed Compound and is in a leading position. However, whether the indicators underestimate Compound or whether Aave can continue to maintain its current advantage is uncertain. In addition to targeting individual users, Aave and Compound are gradually developing products aimed at institutional clients. Aave has launched the Aave Pro program, allowing institutions and enterprises to earn DeFi yields based on the Aave protocol; Compound has introduced Compound Treasury to allow institutions holding USDC to earn fixed returns. Who will become the king of lending platforms in the future? Let us wait and see.

What we can hope for is that various lending platforms can achieve the best in security and compliance, ensuring that the funds of users participating in DeFi lending do not suffer unexpected losses; and as participants, we should maintain a certain level of risk awareness and not blindly follow the crowd.

Risk warning

Risk warning Risk warning

Risk warning