From "DeFi Summer" to "DeFi 2.0", improvements in liquidity incentive programs

Title: DeFi 2.0 and Liquidity Incentivization

Author: Chainlink

Translator: Yangz, The Way of the Metaverse

## Abstract:

The first "money legos" of the DeFi ecosystem, such as LP Tokens and decentralized Stablecoins, have created conditions for the further development of DeFi.

DeFi 2.0 is a new term in the ecosystem, primarily referring to a subset of emerging protocols built on the initial money legos to advance the current DeFi ecosystem, mainly in the form of liquidity supply and incentivization.

With the addition of these new financial primitives, the entire DeFi economy is rapidly becoming more user-friendly, secure, and accessible.

Decentralized finance, commonly known as DeFi, is one of the most influential and successful waves of innovation based on blockchain technology. Driven by blockchains with built-in smart contract capabilities and secure oracle networks like Chainlink, DeFi refers to a wide array of decentralized applications that disrupt existing traditional financial services and unleash entirely new financial elements.

DeFi protocols are continuously advancing and iterating mature models based on financial protocols, propelled by their inherent advantages of permissionless combinations and open-source development culture. The DeFi ecosystem has developed at lightning speed, and the rise of liquidity-focused DeFi projects in recent months has ushered in a new wave of DeFi innovation known as DeFi 2.0.

DeFi 2.0 is an emerging term within the larger blockchain community, primarily referring to a subset of DeFi protocols built on previous DeFi advancements, such as yield farming and lending. A notable focus of DeFi 2.0 protocols is to overcome the liquidity constraints faced by many on-chain protocols that have native tokens.

This article considers the past innovations that have created conditions for the DeFi 2.0 movement, introduces the liquidity issues that DeFi 2.0 protocols aim to address, and then delves into the utility and new financial models introduced by the DeFi 2.0 ecosystem.

## 1. Early Development of DeFi

Early DeFi pioneers, such as Uniswap, Bancor, Aave, Compound, and MakerDAO, established a solid foundation for the developing DeFi economy, introducing many key and composable "money legos" to the ecosystem.

Uniswap and Bancor were the initial decentralized automated market makers (AMMs), providing users with the ability to seamlessly swap tokens without relinquishing custody. Aave and Compound introduced decentralized lending, offering on-chain yields for deposits and obtaining operational funds in a permissionless manner. MakerDAO enabled users in the ecosystem to hold and trade decentralized Stablecoins, providing a hedge against the volatility of cryptocurrencies.

Through these protocols, users gained access to reliable trading platforms, frictionless lending, and stable pegged currencies—three core financial elements that are widely present in traditional financial markets. However, the infrastructure behind these familiar DeFi-based services is fundamentally different from centralized organizations in terms of transparency and user control. The various technical implementations behind these decentralized services are the cornerstones of DeFi innovation.

Interconnected DeFi Innovations

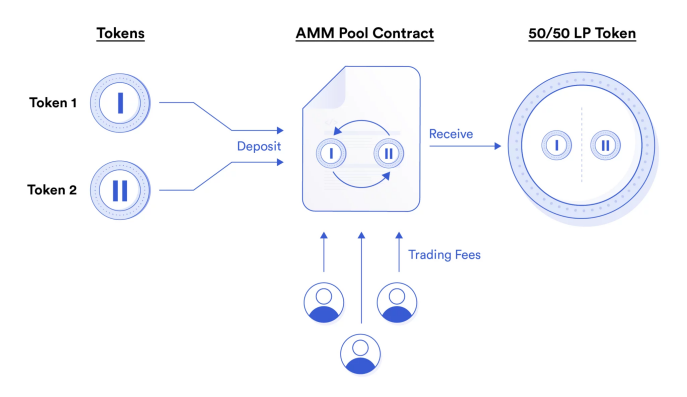

A core example of DeFi innovation unique to blockchain is the liquidity provider (LP) tokens in decentralized exchange (DEX) protocols with automated market makers (AMMs). While DEXs effectively serve as alternatives to centralized order book trading platforms, the most popular DEXs adopt a model known as constant product automated market maker (CPAMM).

The decentralized liquidity pools in AMMs are used to facilitate token swaps, where individual liquidity providers typically contribute equal amounts of each cryptocurrency to contribute to a liquidity pool for a trading pair. In return, they receive an LP token that represents their share in the liquidity pool and the fees earned from facilitating swaps.

LP tokens triggered a cascading flow of DeFi innovation as they were quickly adopted by other DeFi protocols in various ways. For example, lending protocols like Aave and Compound iterated on the idea of providing users with receipt tokens representing their underlying deposits, now known as aTokens and cTokens.

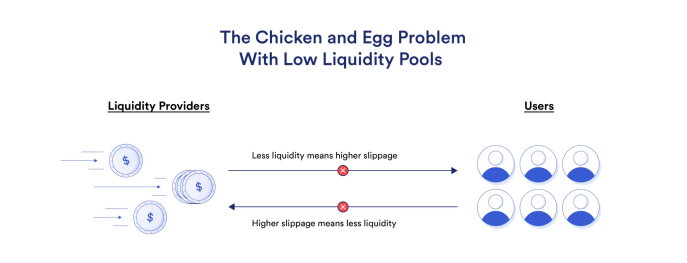

The permissionless nature of AMMs and LP tokens also empowered DeFi startups, which no longer needed to go through the listing process of centralized exchanges to launch tokens. If there is sufficient liquidity, newly launched tokens can be traded immediately on DEXs. However, without enough liquidity, the token swap functionality of DEXs becomes limited in utility, as users may have to pay astronomical prices for large swaps due to slippage. This has led to one of the most prominent issues currently facing DeFi: the liquidity problem.

## 2. The Liquidity Problem

Since the early days of the DeFi economy, liquidity has been a source of frustration for many emerging DeFi projects. The entire ecosystem is token-driven, with tokens serving as a means for teams to align participant incentives, collect rewards from user fees, and become part of the larger DeFi ecosystem. However, to provide users with robust sources of liquidity for trading their tokens on AMM protocols, DeFi teams need to secure large liquidity pools.

Part of the answer to this problem can be found in third-party liquidity providers in AMM protocols, through which any individual with sufficient funds can provide liquidity for a token pair, allowing teams to obtain enough liquidity from others rather than providing it themselves. However, end users are rarely incentivized to provide liquidity for new tokens, as this exposes them to the risk of impermanent loss in exchange for minimal fee income from swaps. They need a compelling economic reason to take on this risk.

This leads to a chicken-and-egg problem. Without sufficient liquidity, the slippage caused by swaps makes users reluctant to participate in the ecosystem of DeFi protocols. Without users participating through token trading, there isn't enough fee volume generated to incentivize third-party actors to pool their tokens and provide liquidity.

As a result, another key DeFi innovation was born. LP token-based rewards became the primary means for new DeFi protocols to guide liquidity, a process known as yield farming.

Yield Farming

The emergence of yield farming (also known as liquidity mining) in the summer of 2020 triggered a surge of DeFi activity, referred to by blockchain enthusiasts as the "Summer of DeFi."

The idea behind yield farming is simple. Users provide liquidity for a trading pair on an AMM protocol and, after receiving LP tokens, stake those LP tokens to earn rewards distributed in the project's native tokens. This implementation addresses the chicken-and-egg problem by providing third-party liquidity providers with a compelling economic reason to provide liquidity for tokens: namely, greater yields. In addition to generating larger cumulative fees in AMM swaps, they can earn more rewards by staking and obtaining more of the project's native tokens under deeper liquidity incentives.

With the introduction of yield farming, new DeFi projects were able to guide sufficient liquidity to start and sustain operations, reducing the slippage for users entering their ecosystems. This led to an exponential increase in the number of DeFi protocols, confirming that yield farming lowered the barriers to entry for users and DeFi project founders.

Limitations of Yield Farming

Despite being highly effective, yield farming alone cannot fully resolve the liquidity problem due to the specific limitations of long-term yield farming programs. Yield farming excels at guiding initial liquidity, but it must be predicated on long-term plans to ensure sustainable liquidity.

This is because yield farming has an inherent characteristic of supply dilution. Founding teams allocate native tokens to liquidity providers and offer additional sources of yield to incentivize liquidity providers to lock their liquidity in AMM pools. However, as more tokens are allocated to third-party liquidity providers, an increasing proportion of the total token supply is given to rented liquidity, and liquidity providers can remove their liquidity at any time and sell their earned LP staking rewards. DeFi teams cannot ascertain whether liquidity providers will remain if staking rewards dissipate, and keeping staking rewards at high levels for extended periods increasingly dilutes the supply of native tokens.

As projects increasingly seek to expand across different cross-chain AMMs, or even AMM protocols on the same chain, various yield farming measures need to be adopted across different trading platforms to establish deep liquidity pools for each project. This exacerbates the aforementioned limitations, as emerging DeFi projects must delicately balance the supply expansion to numerous AMM protocols—but they often lack the manpower, means, or information to do so effectively.

Third-party liquidity providers must be adequately incentivized to provide liquidity for higher-risk holdings. Since newly launched tokens often exhibit high volatility, the risk of impermanent loss increases, offsetting the trading fees and yield farming rewards from AMM protocols. This represents an inconsistency in the incentive structure for third-party liquidity providers, who have limited options to manage the risks of providing liquidity and yield farming.

Yield farming is an influential way to guide liquidity for DeFi projects, but it is not without long-term risks. For most DeFi projects, running yield farming programs and guiding liquidity is necessary and healthy, but project teams must be mindful of their token supply and long-term strategies to avoid negative impacts.

## 3. DeFi 2.0 and the Pursuit of Sustainable Liquidity

In terms of liquidity, DeFi 2.0 refers to a number of emerging DeFi projects that aim to thoroughly address common issues related to liquidity supply and incentivization. They provide alternatives and supplements to the yield farming model, offering projects a way to maintain a source of liquidity sustainably over the long term. But how can blockchain-based native token projects maintain healthy liquidity and allocate it ideally?

OlympusDAO and Protocol-Owned Liquidity

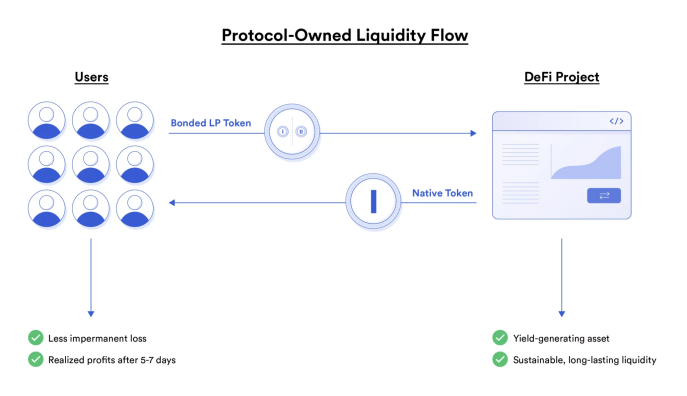

In 2021, one solution that emerged in the DeFi community was the bonding model of OlympusDAO, which focuses on protocol-owned liquidity (POL).

Through its bonding model, OlympusDAO flipped the script on yield farming. Instead of renting liquidity through supply expansion initiatives, OlympusDAO utilizes bonds to exchange LP tokens from third parties at a discounted rate in exchange for the protocol's native tokens. This provides advantages for the protocol and any projects using the protocol (e.g., bonds as a service). Through bonds, the protocol can purchase its own liquidity, eliminating the possibility of liquidity exit and establishing a lasting pool, while also generating revenue for the protocol.

On the other hand, users are incentivized to exchange their LP tokens through bonds, as the protocol offers discounts on the tokens. For example, if the price of Token X is $500 with a 10% discount, users can bond LP tokens worth $450 to receive $500 worth of Token X. The result is a net profit of $50, depending on a short vesting schedule (typically around 5 days to a week) to prevent arbitrageurs from extracting value.

Another key aspect of liquidity-focused bonds is that bond prices are dynamically changing and can have a hard cap. This serves an important purpose for the protocol, allowing it to control two levers: the speed of token exchange liquidity and the total amount of liquidity exchanged.

As a way to control the speed of the protocol's token supply expansion, if too many users purchase bonds, the discount rate will decrease, potentially even turning negative. The protocol can also determine its desired amount of liquidity through a hard cap, at which point bonds are no longer available, further controlling supply expansion based on precisely defined parameters.

Realigned Incentives

This multifaceted model helps realign the incentive mechanisms between third-party liquidity providers and on-chain protocols. Compared to independent third-party liquidity providers, protocols are better positioned to absorb impermanent loss. While third-party liquidity providers face opportunity costs representing every other liquidity pool and yield farming protocol in the market, protocols have additional motivation to maintain liquidity, as it helps ensure low-cost swaps for users trading with their native tokens, reducing the cost of entry into their respective ecosystems.

Ultimately, OlympusDAO's bonding model allows protocols to better mitigate the risks of low liquidity in a long-term, sustainable manner. Combined with yield farming, DeFi protocols now have more tools at their disposal to meticulously plan their growth phases, from initial liquidity guidance to sustainable long-term growth.

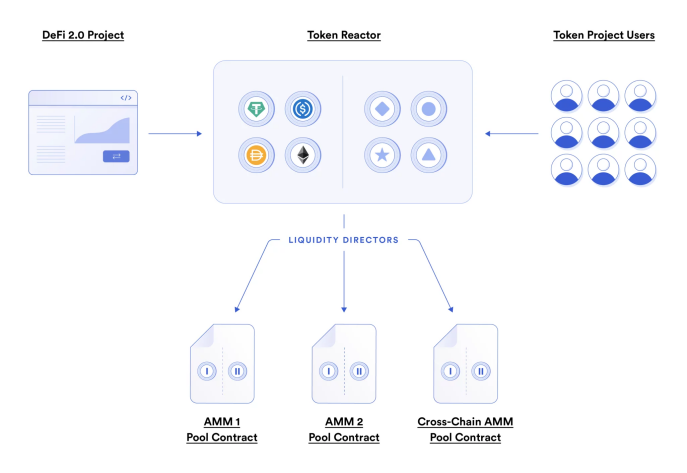

Guiding Liquidity with Tokemak Reactors

Another liquidity-focused DeFi 2.0 project is Tokemak, a DeFi protocol designed to optimize liquidity and liquidity flow. In short, Tokemak's scale aims to facilitate liquidity through two different parties—the Tokemak protocol and liquidity providers (LPs)—with the goal of effectively decentralizing liquidity through liquidity directors (LDs).

Here’s how it works. Consider the contents of LP tokens. Liquidity providers are required to submit equal amounts of two currencies in a given trading pair, which can lead to impermanent loss due to weight shifts and price changes. To address this issue, the Tokemak protocol holds reserves of stablecoins and first-layer assets as the underlying pairs for emerging tokens. This constitutes one aspect of the liquidity pair. For the Token X-ETH liquidity pool on Uniswap, Tokemak reserves contribute ETH.

Independent third-party liquidity providers and DeFi projects can then come together to form the liquidity side of Token X. At this point, liquidity directors (LDs) become the focus. Liquidity directors control the flow of liquidity by staking Tokemak's native tokens, utilizing these two one-sided liquidity pools, and then directing liquidity to a wide range of AMM protocols.

Balancing Liquidity Flow and Direction

The ultimate result of this system is that liquidity flowing through Tokemak is dedicated to achieving the goal of efficient and sustainable liquidity direction across the entire DeFi ecosystem.

Liquidity directors move liquidity based on a voting mechanism, while liquidity providers earn Tokemak's native tokens for providing one-sided liquidity. The variable returns earned by each party balance each other to achieve an optimized ratio between liquidity directors and liquidity providers, ensuring that the amount of liquidity provided has an optimal number of directors.

This can benefit emerging DeFi projects—especially those run by DAOs—as well as farmers and liquidity providers. At a foundational level, Tokemak's one-sided asset allocation allows DeFi projects to guide initial liquidity using only their native tokens, without needing liquidity from stablecoins and first-layer assets. Tokemak reactors can also provide a structure for collective decision-making liquidity for DAO-based projects while offering alternative yield options for third-party liquidity providers and yield farmers with mitigated impermanent loss.

Other DeFi 2.0 Advances

Another subset of DeFi 2.0 protocols builds on previous yield-generating mechanisms and assets to create new financial instruments.

A major example in this regard is Alchemix, a self-repaying lending platform with a "no liquidation" design. The protocol lends out representative tokens pegged 1:1 to the collateralized assets. For instance, by depositing DAI Stablecoin as collateral, users can borrow 50% of the amount as alDAI. The associated collateral is then deposited into a yield-generating protocol, allowing it to gradually increase.

Through the combination of representative tokens and yield-generating collateral, Alchemix can offer a no-liquidation lending platform that enables users to consume and save simultaneously, with the loan principal decreasing as the collateral continuously earns yield.

Abracadabra, another DeFi 2.0 protocol, employs a similar mechanism but is associated with MakerDAO. Users can deposit yield-bearing collateral and receive MIM Stablecoin in exchange, maintaining exposure to the collateral while earning yield and unlocking liquidity for users.

Without the early innovations that initially brought vitality to the decentralized economy—AMM protocols, decentralized Stablecoins, and oracles—there would be no liquidity bonds, liquidity flow mechanisms, or yield-generating collateral. From the early stages of AMM LP tokens and decentralized Stablecoins to today's DeFi 2.0 protocols, each project represents a valuable iteration in building the decentralized economy.

## 4. Money Legos in DeFi

When conceptualizing how the DeFi economy moves as a unit, money legos serve as a useful metaphor. Cutting-edge innovations and new technologies can be combined, with each piece building on another, leading to the creation of something greater than the sum of its parts.

DEXs and LP tokens are among the most prominent money legos in the blockchain industry, enabling the scalable on-chain exchange of tokens and making yield farming possible. The initial wave of decentralized Stablecoins laid the groundwork for newer Stablecoin designs and decentralized lending platforms through airtight over-collateralization processes and risk mitigation. Chainlink's off-chain data and computation services provide the underlying infrastructure needed for countless DeFi applications, helping to realize these innovations.

These money legos cannot be considered in isolation but should be viewed as an interconnected ecosystem that supports, connects, and emphasizes other components to create new possibilities. By combining Chainlink Price Feeds with AMM LP tokens, dynamic yield farming becomes feasible. By integrating Stablecoins into AMMs, users gain the stability needed for trading on decentralized trading platforms.

With the advent of DeFi 2.0, a new generation of money legos is building upon its predecessors to make the decentralized financial environment more effective, user-friendly, and useful for its participants. Money legos continue to stack up—each additional block brings new value and opportunities to the DeFi ecosystem.

Risk warning

Risk warning Risk warning

Risk warning