Viewpoint: Web3 does not truly exist yet, and we must be wary of greedy speculators

"The wealth effect has driven the prosperity and arrogance of market participants, while the self-referential ironic nature of crypto culture is alienating non-natives."

"The wealth effect has driven the prosperity and arrogance of market participants, while the self-referential ironic nature of crypto culture is alienating non-natives."Author: Cobie, a well-known Twitter KOL

Original Title: 《Wtf is web3》

Translation: Hu Tao, Chain Catcher

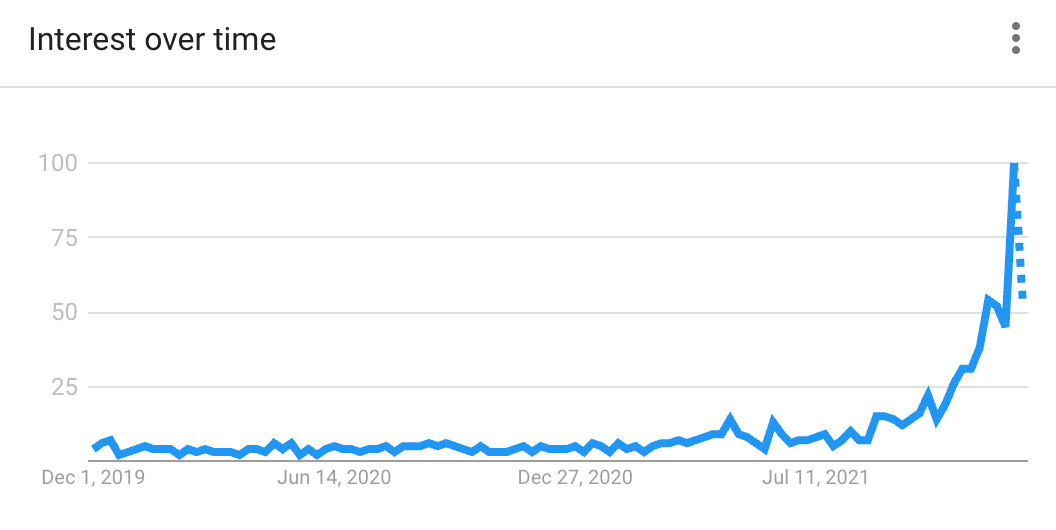

Web3 is a very popular term this year, mainly aimed at alternative finance markets and super Twitter thread authors in the tech world.

This is one of the two cheat code phrases you can use to bypass LP critical thinking when raising your first round of funding in 2021, the other being "metaverse." Congratulations, you now have a billion dollars to deploy because you learned the buzzwords and went to a good school.

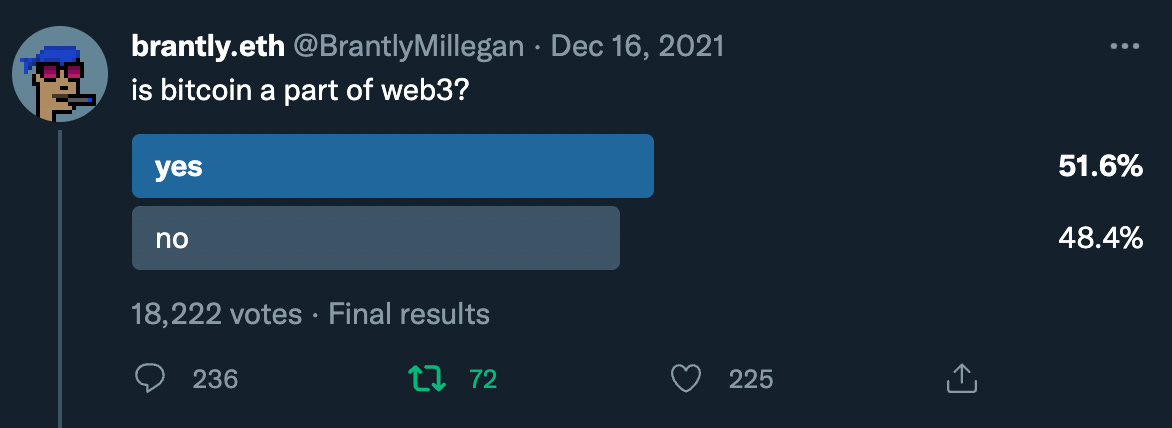

Despite the KOLs at the time publishing a plethora of obscure ideas, no one really agreed on what web3 actually is. Depending on which tribe you belong to, web3 is a scam, web3 is the future, web3 is tagging the world, web3 is VC exit liquidity, web3 is just another name for crypto, you get the idea. Even the crypto community can't agree on whether Bitcoin is web3.

If no one really agrees on what web3 is, and the term has only truly become popular in the past six months, I think we can conclude that web3 doesn't really exist yet. However, it is clear that there are many ideas and experiments circulating around a unifying theme that is inspiring, creative, or completely frustrating to observers.

What is the focus of web3?

To avoid the futility of accepting this debate, might it be more useful to consider what web3 could be? Do we even need to move on from web2? What problems does web3 solve?

I think there are two important themes:

Decentralization — There is an increasing distrust of centralized power. Whether it’s governments, central banks, or global corporations that have become stronger than nations. The trends of de-platforming, behavioral authorization, and censorship have sparked new interest in building trustless and censorship-resistant platforms that can empower ordinary people and disrupt existing power structures.

Ownership of value — With Web2, the web shifted from "read" to "read and write." The web became social and participatory; the era of user-generated content began. Modern tech companies host content from users and then monetize it privately. They exploit our desire for social interaction, mixing it with addictive product models, interweaving advertisements and extracting all the value created by these users for shareholders. By the time you can become a shareholder in these companies, their value has reached billions, and insiders have become wealthy.

An open and fair web

I understand the excitement of supporters.

An idealized future web might be able to address these social issues in a way that not only solves them positively but also allows founders with strong growth and retention tools to compete with incumbents.

We could build a web that enables users to share the value they create and increase adoption. A technocratic majority cannot decide what we can talk about, nor can they determine how many ads we see each day.

Perhaps it can empower ordinary people who have spent thousands of hours acting as batteries for large companies, converting attention into profits for private shareholders.

Maybe the web can become more collaborative rather than extractive.

Everything turns to dust

Perhaps more importantly, I understand the fears of critics.

A pessimistic future web could be filled with tokenized microtransactions that seek rent on every possible user action, requiring users to hold native tokens to operate their toasters correctly.

It could be a network built on selling worthless ERC20 tokens to retail investors to fund failed projects, extracting value more directly than spending years selling ads.

It might be a network with fewer tools to deal with harassment or evils like child abuse content. Online crime becomes harder to prevent.

Perhaps the financialization of everything will only benefit complex algorithmic hedge funds and massive early-stage venture capital firms that become major shareholders of these tokens in private seed rounds.

Which path to take?

If you can imagine a pleasant future and a dystopian future, I wouldn’t blame you for expecting the worst to be the most likely to become reality. Modern corporations clearly often make the web more… annoying. Cookie permissions, GDPR requests, banner ads, paywalls, loot boxes, and pay-to-win games — it’s easy to see suboptimal or anti-user changes.

And if you observe cryptocurrency from the outside, you can't really blame outsiders for seeing things that resemble scams. The wealth effect drives the prosperity and arrogance of market participants, and the self-referential irony of crypto culture is alienating to outsiders.

I get it. The past was sometimes terrible, and the present is sometimes terrible, so the impulse to reject ideas that could puncture theoretical holes is strong. You don’t have to think very hard to imagine ways decentralized systems could be exploited, and you don’t have to look far to find examples of ordinary people being exploited by token projects.

But at the same time, you don’t have to look too far to see the power of ownership and autonomy in the operational systems of existing owners.

Without central authority guiding it, Bitcoin transformed from "dark web transaction medium" to institutional-grade value storage asset in a decade.

Ethereum evolved from "tech Ponzi scheme" to a massive owner-operated network trading billions of dollars in value daily.

Businesses, users, and third parties contribute incremental value to these two networks, sharing the rewards of doing so. Anyone can participate, and value can be returned to them rather than only to founders or financiers.

Even purely fun social consensus projects like ConstitutionDAO could be an example of user-generated value creation shared by everyone. Although it ultimately failed to acquire a copy of the Constitution, the DAO became more valuable, and that value returned to the participants.

Perhaps this shared ownership could become a compelling function to break existing conventions about how tech companies operate or should operate.

Inequality

The intensification of inequality is becoming increasingly apparent. During the pandemic, asset prices skyrocketed, making the already wealthy even richer. Meanwhile, small businesses struggled, and the working class almost immediately spent their stimulus funds. Clearly, over 50% of Americans have less than three months of emergency savings.

Wage growth has stagnated, but housing costs have risen by over 400% in the past 40 years. People are starting to feel trapped in a manipulated system where their chances of affording the future they want slip away quickly.

No wonder there has been an increase in retail options traders on Robinhood and Dogecoin buyers. For those who see no path to achieving financial goals through saving and investing, lottery-style investing has become a viable option.

Perhaps a more socialist model of equity or token ownership could serve as capitalism's answer to universal basic income. Rather than the state printing a little cash for families, taxing future generations to pay for current money, perhaps people sharing the wealth they create could create a fairer world.

If users vote with their wallets to choose companies that reward them for the value they have already participated in creating, those companies will discover tremendous network effects tools to grow rapidly and replace existing businesses. Real people could choose to own some of the value they co-create rather than giving it all away to founders and investors.

If all other conditions are equal, then users of two identical services will be incentivized to use the one where the value returns to them.

Perfect conception

When Bitcoin was created, it was another perfect concept. Satoshi delivered what could prove to be one of the most important creations in history to the world on fair terms for everyone to participate. They did not privately share tokens or offer any tokens to private investors. They mined their tokens under the same conditions as all other participants. Yes, they mined millions of coins because they were early, but they had no extra advantage compared to others who understood Bitcoin.

When Ethereum was created, they pre-mined tokens and held an open free ICO. They sold 60,000,000 ETH to anyone who wanted to participate. Ethereum was priced at about $0.30 per ETH. The founders of Ethereum did retain some tokens for themselves and the Ethereum Foundation. Vitalik is the founder of ETH and the largest single pre-mined recipient, receiving less than 1% of the total ETH supply, which is a very small ownership share compared to traditional stocks.

Although Ethereum's birth was "fair for everyone" slightly worse compared to Bitcoin, it still had a relatively fair and open participation model. By 2017, ICOs replicated this model, but with pre-sales and private sales to insiders, ICOs began to degrade.

By 2018/19, the free fair terms for participants had become a thing of the past. The SEC enforced ICO projects to protect retail investors. Regulatory pressure and lack of clarity led crypto builders to privately raise funds from venture capital firms rather than the public. Non-insiders could no longer purchase early cheap terms that VCs can now buy.

You could focus on a trend of free fair launch networks without founder rewards transitioning to privatized gains with large founder allocations funded by venture capital and be extremely pessimistic. It seems the purity and beauty created by Satoshi have been corroded by greed.

But the fact is, crypto is only now becoming popular. When Bitcoin was launched, it was not so obvious to many that crypto could have value. Bitcoin proved it could. Ethereum deepened that belief. The price charts have attracted a massive amount of risk-seeking capital in just ten years.

When Satoshi launched Bitcoin, the mining difficulty was so low that people could mine 50 BTC block rewards with personal computers. The undiscovered nature of Bitcoin made it a fair issuance for hobbyists rather than a playground for hedge funds. If a project today tried to launch in the same way, the already wealthy would simply take over all the hash and accumulate all the coins, paying the power suppliers their share in this new project. In such an environment, founders might as well sell directly to them and secure long-term funding.

I would prefer to sell openly to everyone on the same terms, but I understand that founders do not want to risk unnecessary regulatory trouble, so dealing with professional investors is often easier and less costly. Not to mention the abusive vehicles, and most ICOs from 2017 have gone to zero.

Is it important that some people get rich while building the future?

I don’t think anyone would argue that Vitalik shouldn’t own 0.7% of the ETH supply for his contributions to Ethereum. I don’t think anyone would argue that Satoshi’s 1 million BTC were unfairly mined.

However, it cannot be ignored that the biggest supporters of web3 are ironically successful venture capitalists in history. Yes, it’s no surprise that these entities are trying to become super financiers of this apparent utopian shared community economy by purchasing majority stakes at discounted seed rounds.

It cannot be overlooked that cash-grabbing founders and investors are exploiting existing market dynamics to create Ponzi-like asset bull market projects to enrich themselves.

Therefore, I think four things are true:

There is a consensus that it is natural for founders to get rich when they create immense value in the world.

There is a rough consensus that early-stage venture or angel investors are providing a service, and they should be rewarded when what they fund creates immense value in the world.

Many believe these funding opportunities should be open and fair, rejecting existing accredited investor rules as overly paternalistic or counterintuitive (yes, now we can buy top products from venture capital firms!).

When founders or venture capitalists get rich from something that contributes nothing to the world, everyone fucking hates it.

Undeniably, the latter point has become prevalent in cryptocurrency now. Many former product CEOs have become billionaires overnight by launching tokens and making some promises about NFT-driven video games or building "web3" platforms that attract only a handful of active users.

Conclusion

Web3 does not yet exist. However, assessing its value on the excess of a bull market Ponzi scheme may be damaging, just as ignoring these market dynamics is also dishonest.

I believe the social issues of the world and web2 are valid and worth solving, and there are many exciting things to consider in the promise of web3.

I believe that open, transparent, and permissionless systems replacing trusted central authorities would benefit the world and could rebalance and decentralize power.

I hope the financial prosperity of the cryptocurrency market can attract smart people away from pushing ads to people and instead build a fairer and more collaborative future.

However, if cryptocurrency founders become too wealthy and no longer care, and the new networks are built by late-stage capitalist greedy groups, leaving you buying fractional micro-payment NFTs on Cardano to operate an electric toothbrush, I wouldn’t be surprised.

I know I am being lured into a philosophical and somewhat unoperational debate, with all of them being tech billionaires who got rich in the Facebook era of the web. And to be honest, the outcome of their debate doesn’t matter because they are no longer the adventurous builders of the future. Perhaps they are financiers, but their power law curve models have assumed they are wrong more often than they are right.

Risk warning

Risk warning Risk warning

Risk warning