Messari interprets Serum: The cornerstone of the Solana DeFi ecosystem

In about a year, the project has established the first batch of truly decentralized on-chain order books, becoming a key driver of the entire Solana DeFi ecosystem, and has settled hundreds of billions of dollars in funds in the process.

In about a year, the project has established the first batch of truly decentralized on-chain order books, becoming a key driver of the entire Solana DeFi ecosystem, and has settled hundreds of billions of dollars in funds in the process.Original Author: Roman Ugarte, Messari

Original Title: 《Serum: Return of the Order Book》

Compiled by: Xiao He Loves Sharing

This article was first published in early December 2021

Decentralized finance (DeFi) has "remixed" various elements of traditional finance (TradFi) in just over a year, including lending, derivatives, structured products, and more. However, one element has yet to fully cross the chasm: order book exchanges.

Serum is a decentralized exchange based on Solana, aimed at reshaping the way assets are traded in the decentralized economy. Serum's "central limit order book" is a fully on-chain, highly scalable order matching mechanism. It can power the next generation of trading, from in-game markets to high-frequency trading. To better understand the prospects and risks of this ambitious project, let’s take a look at the broader decentralized trading environment, how Serum fits into it, and what the tokenomics of the protocol (SRM) means for investors.

A Brief History of Decentralized Exchanges

Most asset trading today, from stocks on Nasdaq to cryptocurrencies on Coinbase, is facilitated through order books. The mechanism of an order book is simple: traders can place an order specifying the trading pair, quantity, and price, and match with the other side of the order book. Overall, the liquidity of the order book effectively matches buyers and sellers.

There are reasons why the vast majority of assets are exchanged through this mechanism today. First, order books empower users to define their own prices and even allow them to place stop-loss and limit orders. They also typically provide efficiency advantages for traders (lower slippage) and liquidity providers (no impermanent loss).

In the early days of DeFi, many decentralized exchanges (DEXs) attempted to replicate this order book model in a trustless on-chain manner. Starting in 2012, LocalBitcoins launched one of the first DEXs for peer-to-peer trading of Bitcoin, supported by an on-chain escrow technology called Hashed Time Locked Contracts. In 2016, following Ethereum's smart contract capabilities, EtherDelta launched as an order book exchange. Many decentralized order book exchanges followed, including IDEX and 0x, which still handle hundreds of millions in trading volume today.

However, today, the vast majority of DEX trading volume is settled through automated market makers (AMMs) rather than order book exchanges. In fact, over 90% of trades are conducted through Uniswap, Sushiswap, or Curve, all of which represent AMM-based protocols. How did this come to be?

The answer lies primarily in implementation. Faced with high transaction costs and slow settlement speeds, AMM-based protocols are easier to implement on smart contract networks like Ethereum compared to order book exchanges. AMMs also have certain advantages, such as guaranteed trade settlement, constant liquidity (especially suitable for long-tail assets), and a familiar "vending machine" user experience. They also have drawbacks, such as higher slippage compared to order books, and most notably, impermanent loss reduces returns for liquidity providers.

However, with the progress of Layer 2 scaling on Ethereum and the adoption of high-throughput public chains like Solana, there is room for a new approach to address this issue. There is space for a fully decentralized, capital-efficient, and retail-user-friendly emerging order book trading.

Serum: A Paradigm Shift in Order Books

In August 2020, at the tail end of Ethereum's so-called "DeFi summer," Serum launched as one of the first major projects on Solana. It was incubated and heavily supported by the Solana Foundation, Alameda Research, Sam Bankman-Fried, and several other companies.

The project was built to address many of the issues the team saw in DeFi at the time. The limitations of Ethereum made it slow and expensive, many protocols were effectively centralized, and there was a lack of cross-chain functionality in the past (and still is). The white paper's section on AMMs noted this.

Uniswap had quietly revolutionized DeFi by allowing trading without an order book.

But more importantly, automated market making was necessary. AMMs are systems without limit orders, or even buy and sell orders; in an order book, you can decide the price, size, and direction of your trade. AMMs have many drawbacks; you cannot provide liquidity unless you provide both sides; you cannot choose to provide at a specific price; you cannot provide at a price outside the current market price; and you cannot choose the size provided there without providing more support.

There is a solution to this—what other financial sectors have done. But overall, DeFi lacks order books, and matching bids and asks involves a series of operations that the ETH network is too slow and costly to support.

At the core of Serum is a fully on-chain order book built on Solana. The protocol's first central limit order book (CLOB) is a technology that enables users to trade with each other in an efficient, trustless, and non-custodial manner. The protocol is also asset-agnostic, meaning any crypto asset (spot, derivatives, synthetics, etc.) can be traded on the order book. In fact, an upcoming upgrade called Serum Core will enable the order book to match orders with any financial asset, not just SPL tokens. This improvement to the protocol will make it easier to build derivatives and complex products on Serum.

The decision to build on Solana is central to the protocol's mechanics. Solana's fast settlement speeds allow for sub-second transactions, which are necessary for a well-functioning order book, while low network fees (0.00001 USD per transaction) make on-chain interactions extremely inexpensive.

While most of the protocol's mechanics are executed directly on-chain, Serum also plans to have a network of nodes responsible for "turning the crank," which involves order matching and occasionally running specific programs. In return for their work, nodes will be allocated a portion of the protocol's revenue and bear governance responsibilities.

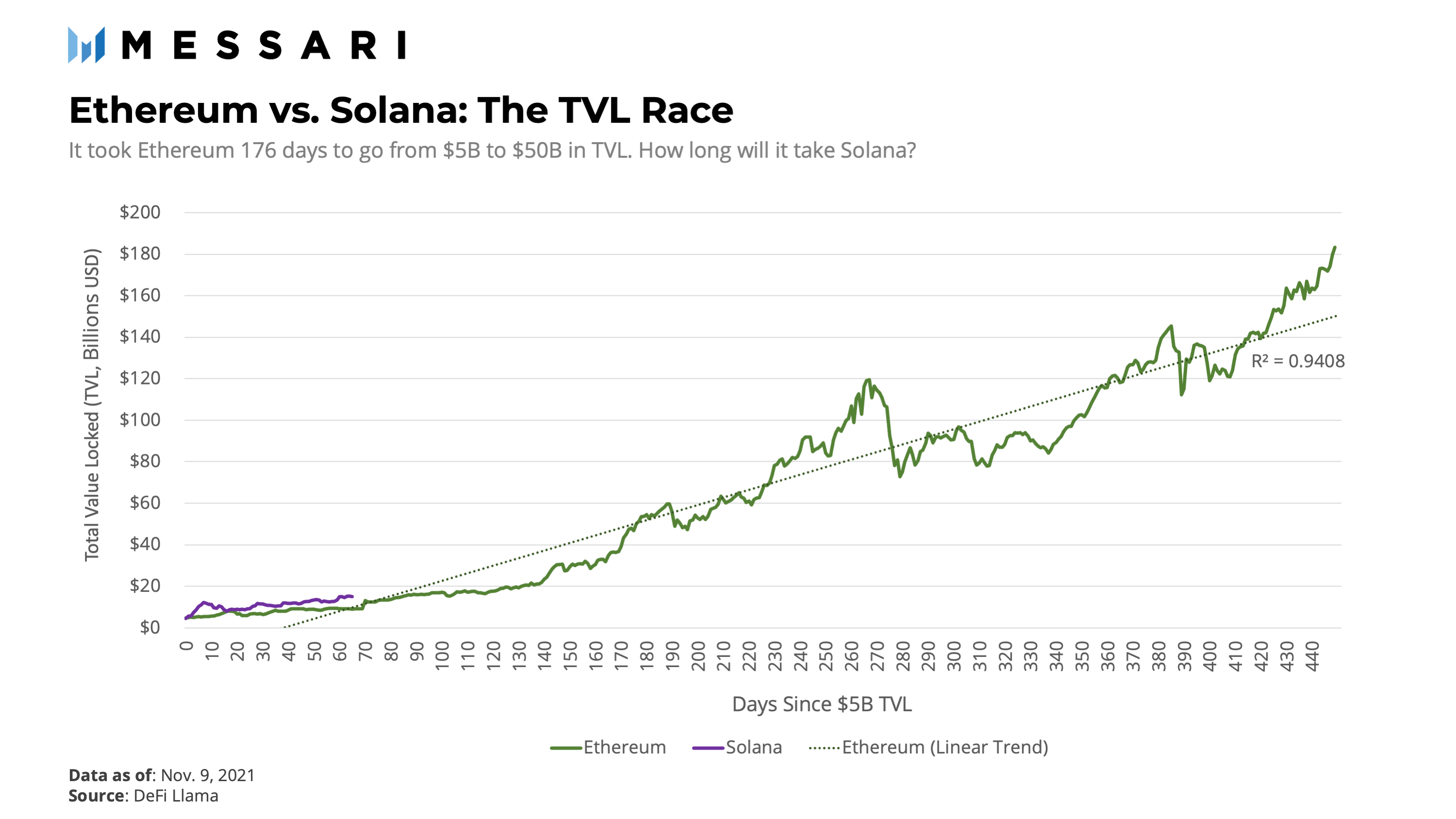

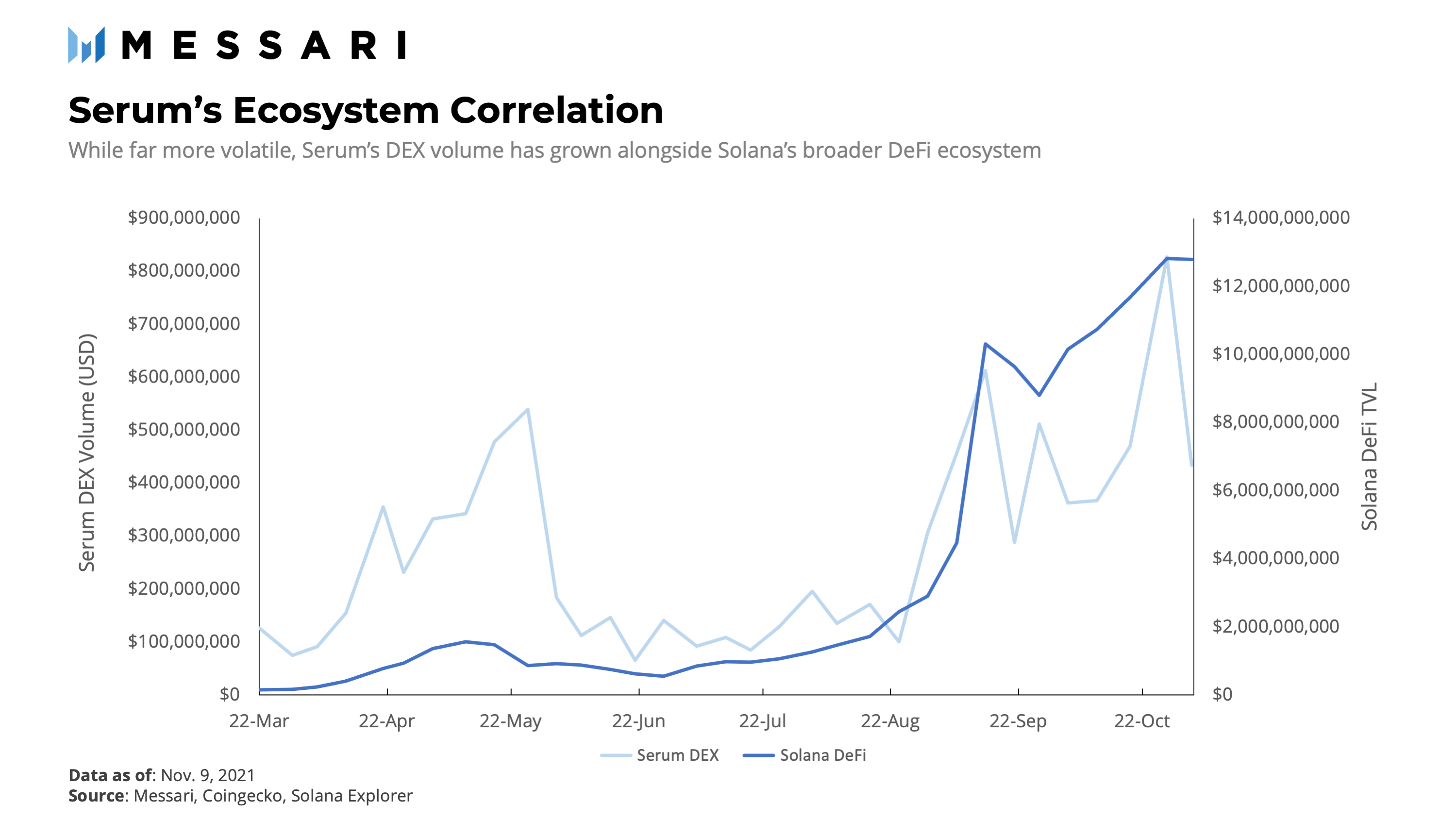

As one of the earliest and most successful DeFi projects on Solana, Serum has established a significant role in the ecosystem. The protocol's early bet on Solana seems to have paid off; the TVL of Solana's DeFi ecosystem has expanded from $500 million at the end of June 2021 to nearly $14 billion today.

Core Composability: Liquidity as a Service

To better understand Serum, it is useful to think of it as an order book middleware solution rather than a decentralized exchange itself. While Serum has many of its own exchange front-ends (known as Serum DEX), its open-source nature allows DeFi protocols, games, dApps, and other projects to plug into Serum's liquidity network to power their own exchanges or markets.

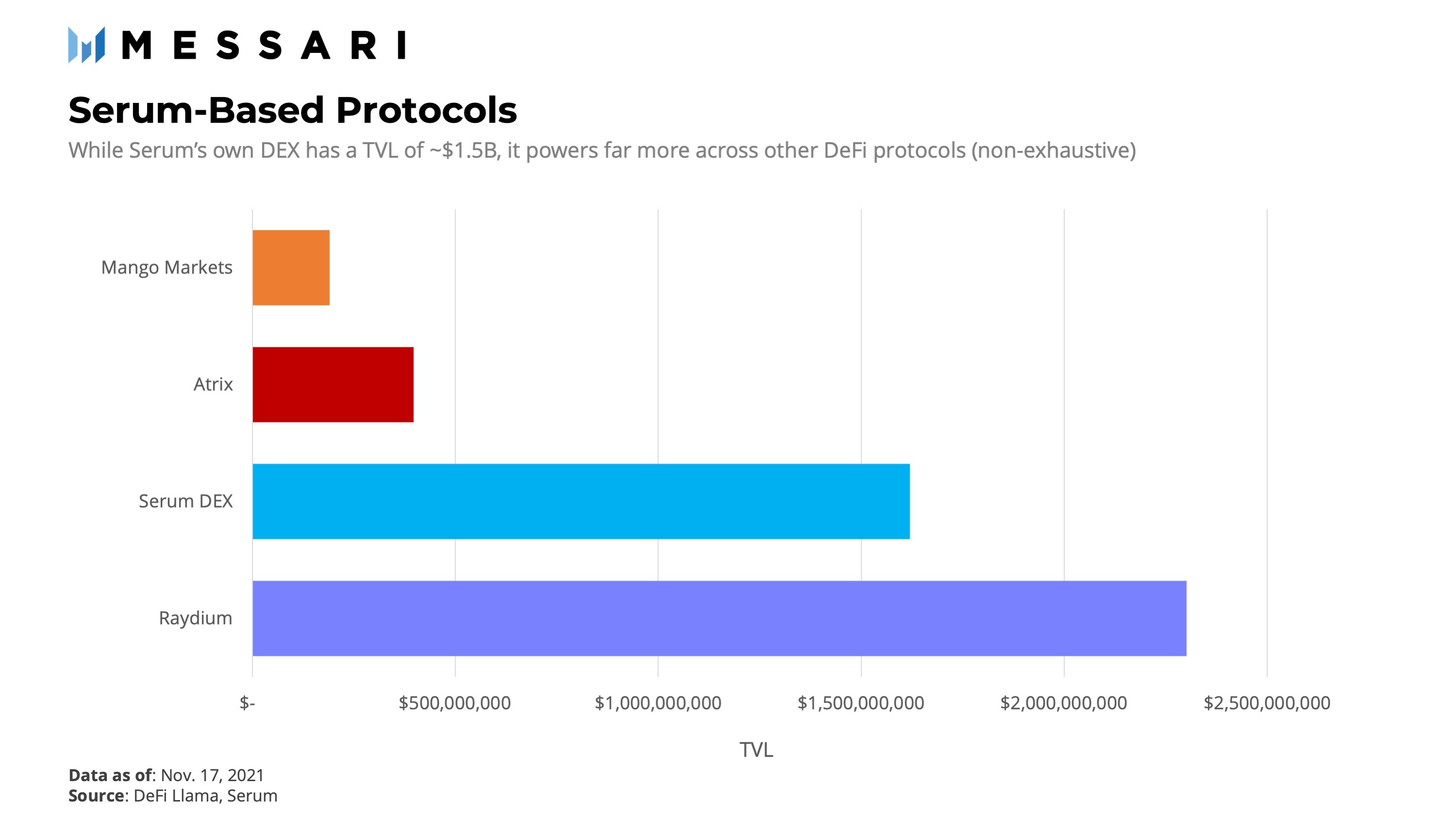

In fact, many of Solana's top DeFi protocols are supported by the backend Serum order book. For example, Raydium, Atrix, and Mango Markets are all built on Serum's open-source DEX infrastructure. While they have designed unique graphical user interfaces (GUIs) and implemented new DeFi features in many cases (AMM functionality, new asset types, cross-chain, etc.), Serum is an integral part of their protocol architecture. As DeFi on Solana continues to mature, many expect Serum's integrations to keep expanding.

Since Serum charges a small trading fee on its routed liquidity, this raises the question: why don’t these protocols build their own on-chain order books?

The answer is twofold. First, guiding an on-chain order book is not easy—the technical and liquidity challenges alone are enough to deter many teams from attempting it. Second, and where the true value of the protocol lies, Serum provides a liquidity network for DeFi protocols that each protocol can leverage, saving costs for users and improving the user experience.

To visualize this, imagine two Serum-driven protocols, DEX A and DEX B. Users of DEX A can place a sell order on the Serum order book, which can then be filled by users of DEX B, without them knowing they are interacting with each other. In fact, such cross-protocol interactions constantly occur among users of different projects in the Serum network, as they all utilize the same liquidity pool. This "liquidity network effect" increases market depth and capital efficiency for each participant.

On Traction and Defensibility

In just over a year since its launch, Serum has solidified its position as the most significant DeFi infrastructure on Solana to date. The protocol itself has directly accrued $1.6 billion in total locked assets, making it the second-largest DeFi project on Solana. Additionally, Serum's native token SRM is held by over 35,000 unique wallets, far exceeding many other protocols.

Most impressively, it has become the preferred DEX middleware for many of the ecosystem's most successful projects. Raydium is an order book AMM with a TVL exceeding $2 billion and total trading volume over $28 billion, powered by Serum. Atrix is another "Serum AMM" with nearly $500 million in TVL, also directly tied to the protocol. There are too many others to name.

By extending its reach to Solana-based projects, Serum has fulfilled its promise of becoming the core liquidity pool of the ecosystem. Moreover, as much of the project's value derives from these strong network effects, Serum is well-positioned to fend off new competitors.

As the ecosystem moves toward cross-chain, Serum will need to upgrade. The original white paper of Serum emphasized the commitment to cross-chain trading and contracts, identifying them as two of the project's "seven key elements." However, nearly a year later, these features have yet to be deployed.

Despite the delays, Serum may have new cross-chain initiatives. They recently announced plans to build cross-chain infrastructure with the Wormhole bridge to facilitate cross-chain liquidity, which would be a significant advancement for the ecosystem. They are also collaborating with Raydium to provide yields on cross-chain assets. While the cross-chain space is filled with both new and old competitors, Serum's existing liquidity and the advantages of the Solana blockchain can provide them with the necessary edge.

One thing is certain: we are preparing for the next phase of DeFi innovation in the coming quarters, and within Solana and beyond, Serum will have to continue fighting to maintain its position. Successfully executing their cross-chain strategy could be a decisive factor in their future trajectory.

Under the Protection of SRM Tokenomics

Serum has two types of tokens: Serum (SRM) and MegaSerum (MSRM).

Serum (SRM) is the primary native asset of the protocol. It is the native token of the Solana blockchain (as an SPL token) but can also be traded as an ERC-20 token. Three elements give the token value.

First, SRM token holders pay lower fees in Serum-powered trades, proportional to the SRM assets in their wallets. For example, non-SRM holders as recipients will pay 22 basis points, while a wallet holding 1,000 SRM will pay 18 basis points, saving 4 basis points.

Second, SRM is also the governance token of the protocol. While on-chain governance has not yet been fully deployed, SRM token holders have already begun to propose and vote on grant proposals, changes to the protocol fee structure, and more. The third and most direct form of token appreciation comes from the protocol's fee revenue. The revenue distribution of the protocol is as follows: 20% for GUI or projects (like Raydium), with the remaining 80% used to "buy and burn" SRM.

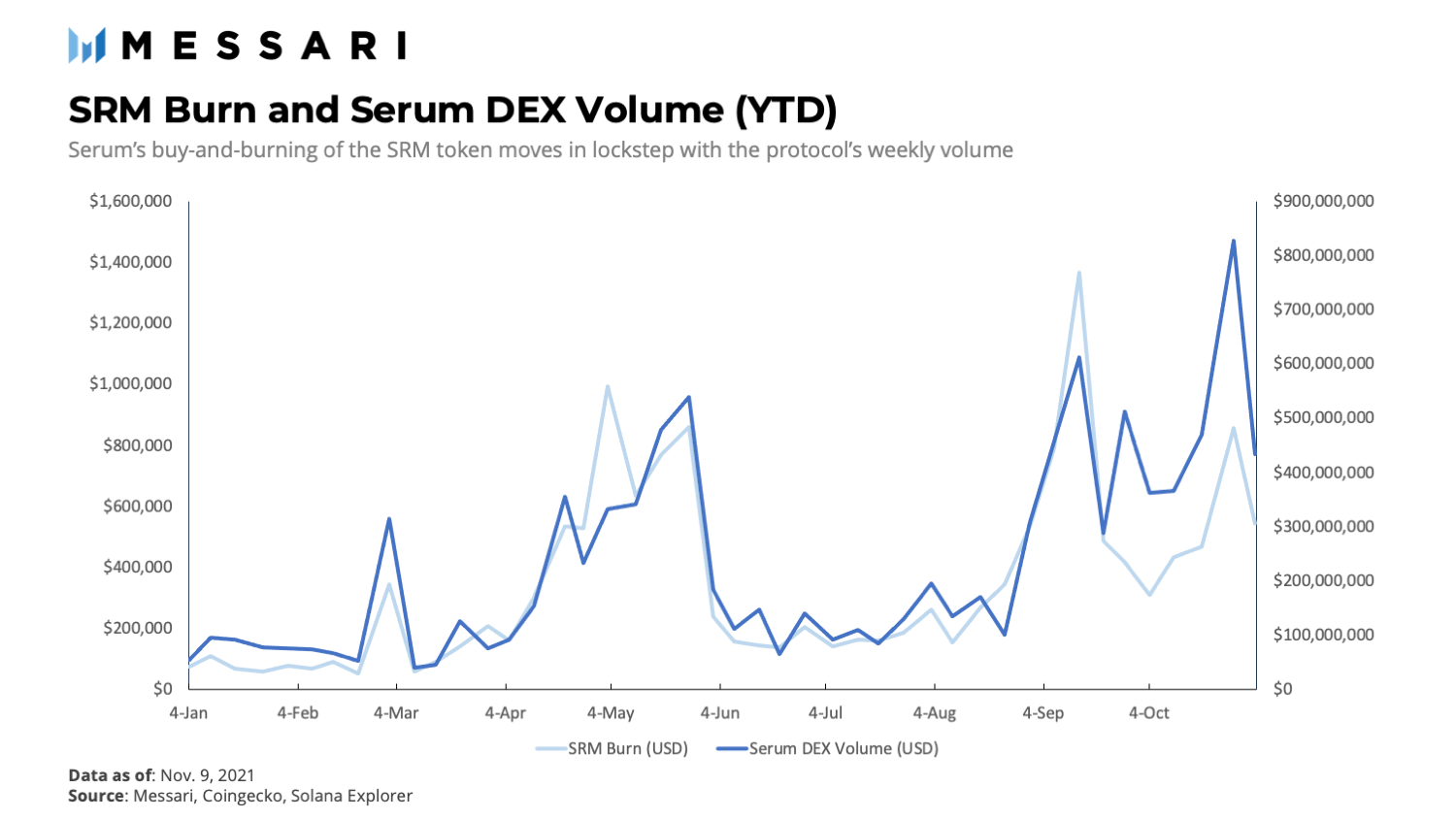

The buy-and-burn model is a simple yet powerful way to align the token's value with Serum's usage. Each week, a smart contract collects 80% of the revenue for that period, purchases SRM on the open market, and then burns the tokens. This provides some form of "dividend" for token holders, resisting token emissions and driving long-term value. Since Binance popularized the burn mechanism, it has been widely adopted by various protocols, especially revenue-generating exchanges like Serum.

As of the writing of this article, 2,437,373.95 SRM have been burned this year, equivalent to nearly $15 million in value (considering weekly price fluctuations). On average, about $350,000 worth of SRM is burned each week. As expected, the buy-and-burn program is highly correlated with the number of DEXs on Serum.

The second asset of the protocol is MegaSerum (MSRM). 1 MSRM is created by locking 1,000,000 SRM. The primary use of MSRM is for nodes; each node must hold at least 10,000,000 SRM and 1 MSRM to participate. Additionally, MSRM holders can earn higher rewards compared to those holding the same amount of "unlocked" SRM.

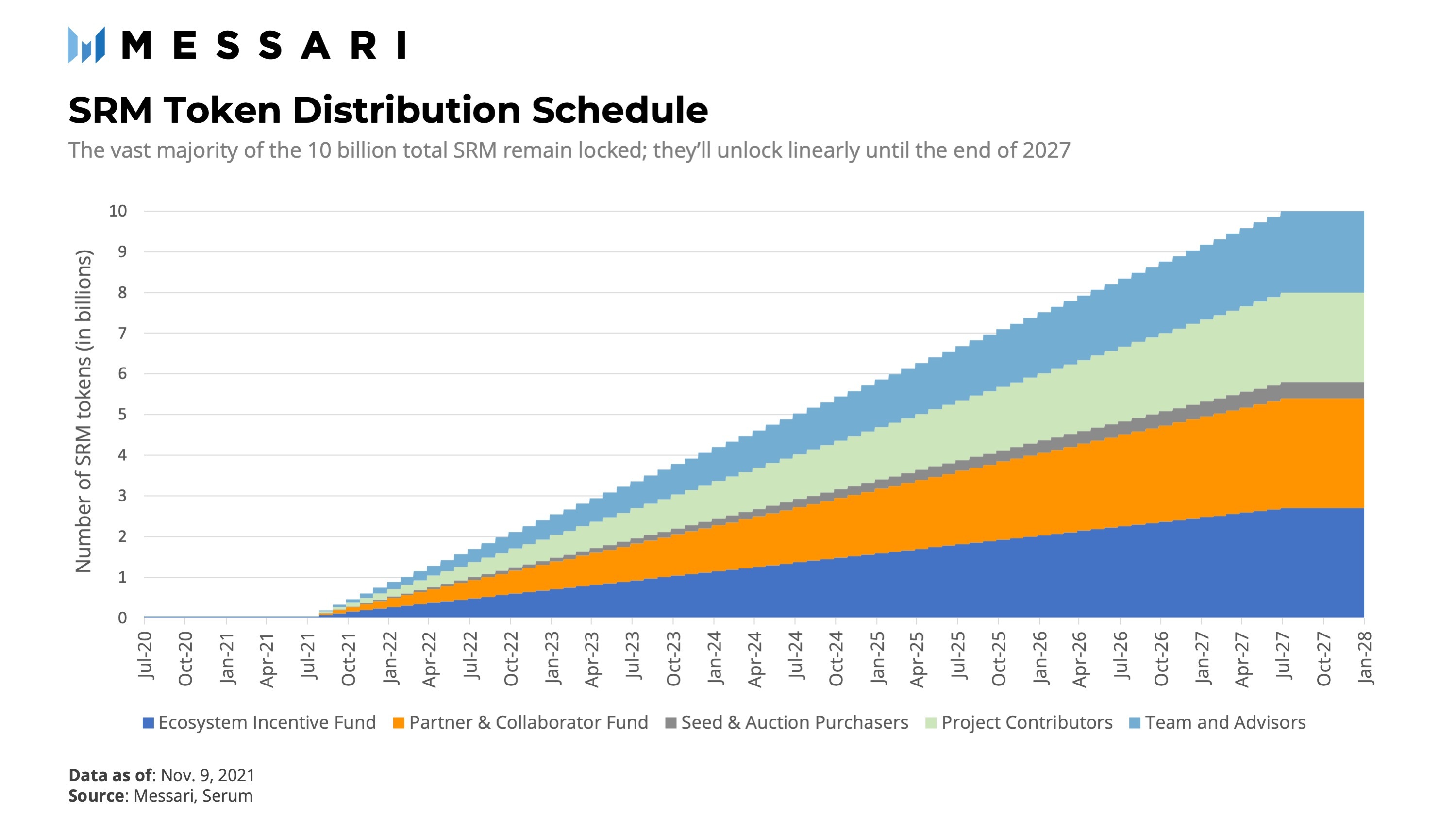

The token issuance schedule is particularly important for research. When the project launched in August 2020, 10% of the total supply (1 billion) was unlocked, while the remaining 90% (9 billion) was locked for one year. After the one-year lock-up period ended, the additional 9 billion SRM will be unlocked linearly over six years until August 2027, with a total of 10 billion SRM tokens in circulation.

Today, a few months after the vesting schedule, the total supply of SRM is 1.1 billion SRM (11% unlocked), but in reality, only 133 million SRM are in circulation. This means that in addition to the other 9 billion locked SRM, over 900 million SRM are still held by team members, allocated to early investors, locked in smart contracts, or otherwise halted from circulation. The currently circulating SRM accounts for only 1.3% of the future supply.

To understand how this figure compares to the broader ecosystem, just look at the circulating supply ratios of other DEXs' projected supply by 2050: Curve (18.23%), Uniswap (41.66%), DODO (11.16%), dYdX (5.63%), 0x (84.55%), and Raydium (13.61%), to name a few.

While it is difficult to make true apples-to-apples comparisons, as each of these protocols has very different tokenomics, what stands out about SRM is its particularly low ratio. This is somewhat concerning for current token holders: low liquidity can amplify market volatility, and future token unlocks will dilute existing investors.

Due to this low circulation ratio, the protocol's fully diluted valuation (FDV), considering the large amount of locked SRM on the sidelines, is approximately $75 billion. Despite a significant drop in trading volume, at current prices, Serum's value would exceed the total FDV of Uniswap, Sushiswap, and Curve (the top three DEXs).

This has sparked a broader conversation within the Serum community around the project's tokenomics, which has intensified in recent weeks. In particular, community members seem to be calling for clearer allocations of tokens (including for VCs and other insiders), any financial agreements or investments in other projects, and a decentralized governance plan as the DAO moves forward. The team has begun to address some of these issues, but more answers are needed.

Looking Ahead

When thinking about Serum's future, making specific predictions is foolish. However, from a broader perspective, there are two main questions that need to be addressed.

First, what is the future outlook for the Solana DeFi ecosystem?

The explosive growth of recent projects, the rise in usage, and the general excitement around Solana should not be underestimated; this nascent blockchain has achieved a balance in the blockchain trilemma, appealing to both users and developers. Solana is not going away; while an immediate "flippening" is unlikely, it is a worthy challenger to Ethereum and will continue to be a significant part of the smart contract space.

Using Ethereum's growth as a baseline, Solana is still at the very beginning of its curve, having only recently surpassed $5 billion in TVL a few months ago. If DeFi on Solana continues its current trajectory (as well as Ethereum's trajectory), it is conceivable that its TVL could exceed $100 billion in less than six months.

Second, how much of the growth of the Solana DeFi ecosystem will be captured by Serum?

This is a more difficult question to answer. It depends on several factors: the core team's continued innovation, addressing community criticisms, and defensiveness against new (and cross-chain) competitors, to name a few.

Over the past six months, Serum's trading volume (and the price of SRM) has more or less followed the growth of DeFi on Solana. While Serum's trading volume is certainly more volatile, it appears to directly benefit from an expanding Solana ecosystem.

So, in a bullish scenario, as DeFi on Solana continues to thrive, Serum will become an essential part of the entire ecosystem's liquidity infrastructure, earning protocol fees and accumulating SRM tokens. The protocol's liquidity network effect is a powerful moat that can solidify Serum as an important "Lego block" in DeFi for the coming years. This is also a bet on order book DEXs continuing to chip away at AMM dominance; it is not hard to imagine that decentralized order books themselves represent a multi-billion dollar market.

However, in a bearish scenario, either (a) Serum loses its market position as the primary on-chain order book for Solana (and cross-chain) with the entry of new competitors, or (b) concerns around the token supply and distribution of SRM hinder the project from delivering returns to investors.

Regardless of what the future holds for Serum, it is important not to forget the pioneering journey of this project. In just about a year, the project has established the first truly decentralized on-chain order book, has been a key driver of the entire Solana DeFi ecosystem, and has settled billions of dollars in funds in the process. By most standards, Serum has successfully fulfilled its ambitious promise.

Today, Serum is preparing for the next growth phase of the industry: the ever-expanding Solana ecosystem, novel DeFi innovations, and cross-chain interoperability. Whether Serum can continue to maintain its industry-leading position as a "liquidity middleware" remains to be seen. If they do, the opportunities are immense.

Risk warning

Risk warning Risk warning

Risk warning