From SushiSwap to sushi.com: A Comprehensive Understanding of Sushi's Products and Valuation Logic

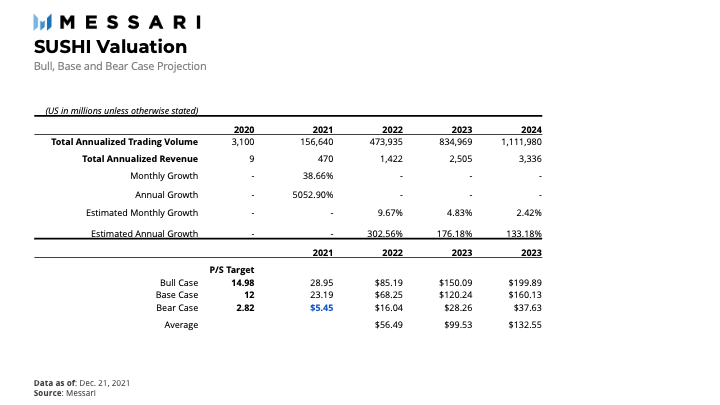

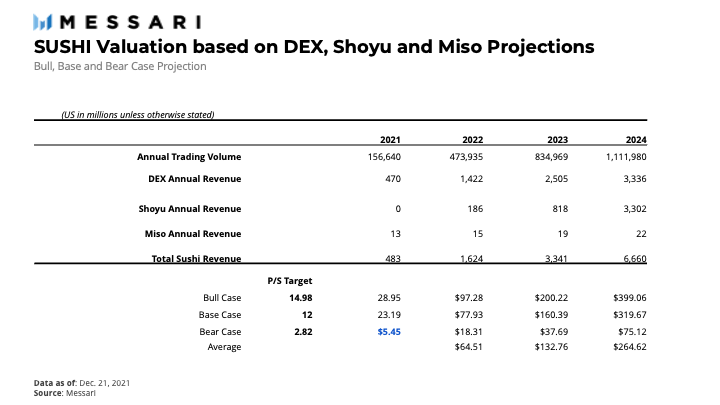

In a bull market, the reasonable valuation of SUSHI is $14.98; in a baseline scenario, the reasonable valuation is $12; in a bear market, the reasonable valuation is $2.82.

In a bull market, the reasonable valuation of SUSHI is $14.98; in a baseline scenario, the reasonable valuation is $12; in a bear market, the reasonable valuation is $2.82.Author: Naphat N, Messari

Original Title: 《The Evolution: SushiSwap to sushi.com》

Compiled by: Hu Tao, Chain Catcher

In recent weeks, global concerns over rising interest rates and COVID-19 variants have generally slowed the price increases of "risk" assets, with most well-known DeFi tokens plummeting over 50%. While the media focuses on prices, DeFi activity remains relatively unaffected. The total value locked (TVL) in DeFi has remained stable, hovering around $245 billion, only about 6% lower than its historical peak.

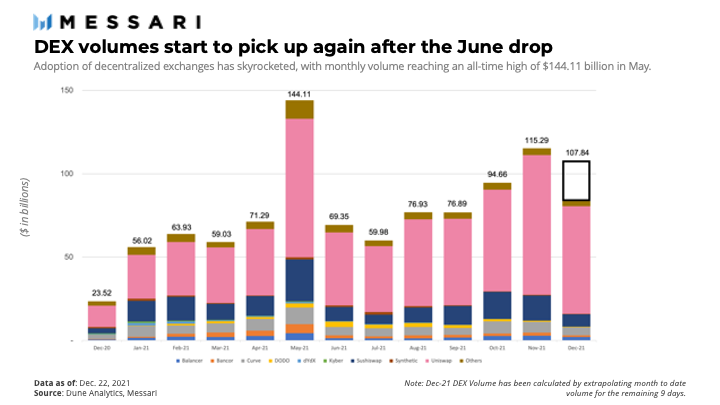

However, the growth momentum of decentralized exchange (DEX) trading volumes seems to lag behind other explosive DeFi activities. Monthly DEX trading volumes soared from $56 billion at the beginning of 2021 to a historical high of $144 billion in May, yet remain below the historical high since June. Since May, the overall DeFi TVL has grown by about 260%. Why hasn't DEX trading volume increased proportionally?

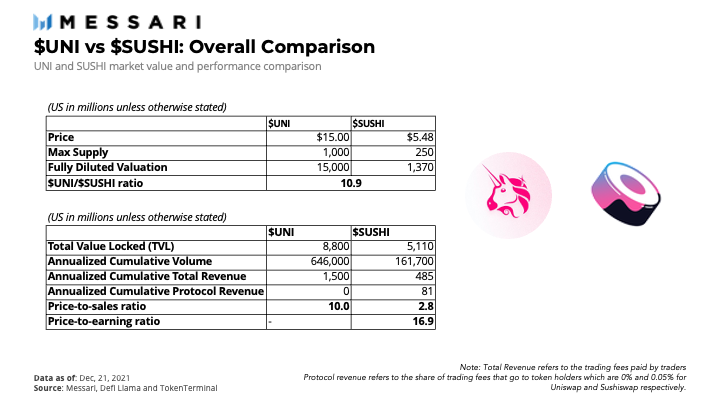

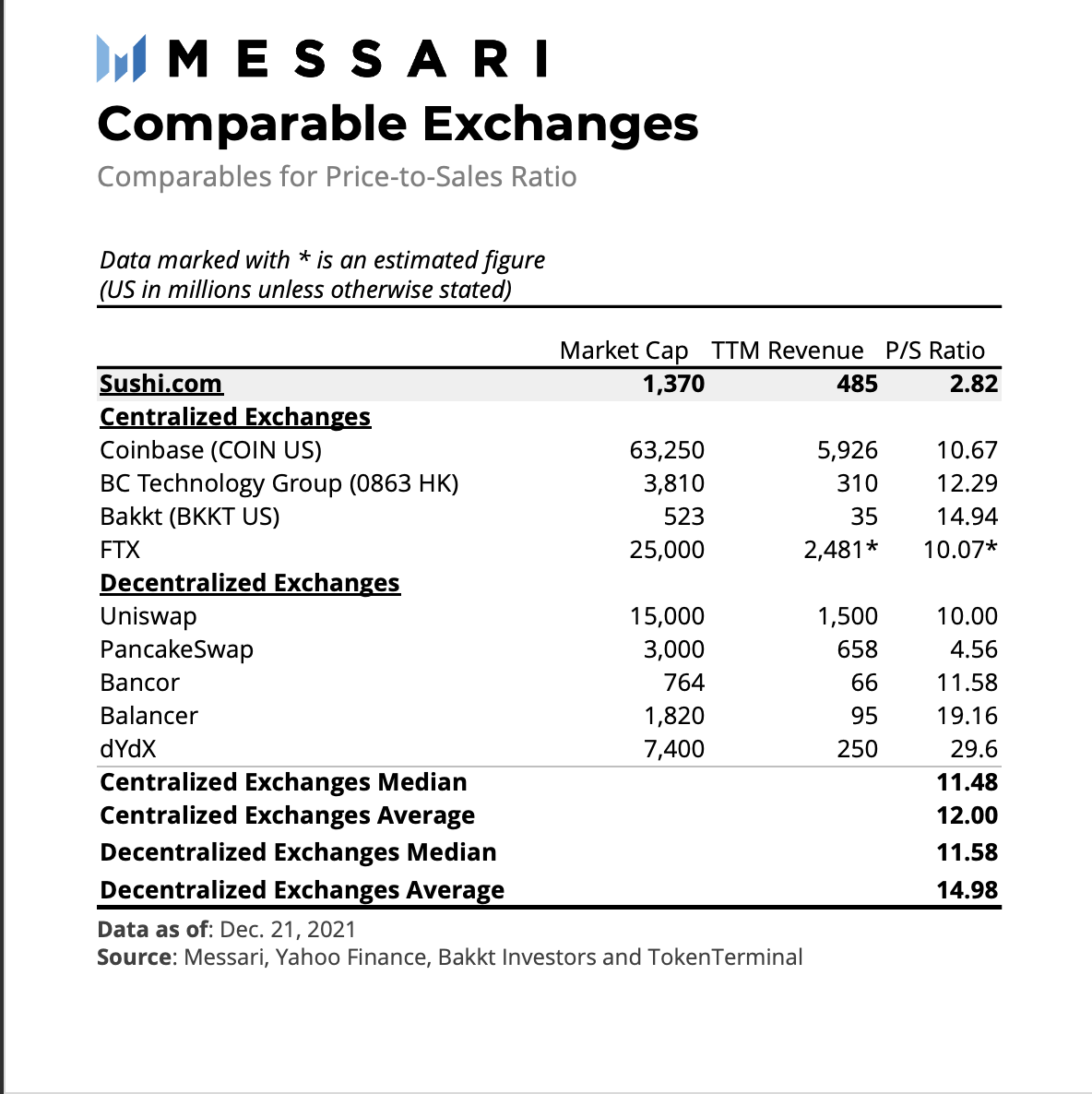

Given that DEX represents a small proportion of DeFi TVL, has the valuation of DEX changed, particularly for the top two market leaders, Uniswap and Sushiswap? At the time of writing, the fully diluted valuations of Uniswap and Sushiswap are $15 billion and $1.4 billion, respectively, with a valuation gap of up to 10.9 times. Over the past 365 days, Sushiswap has processed a cumulative trading volume of $162 billion, while Uniswap has processed $646 billion, four times the volume. Based on the liquidity provider (LP) fees charged by each platform, the price-to-sales (P/S) ratios for Uniswap and Sushiswap are 10.0 and 2.8, respectively.

This indicates that investors assign Uniswap a value 3.6 times greater than Sushiswap for collecting the same amount of LP fees. This may be due to investors perceiving Uniswap as having lower long-term risks in maintaining market share compared to Sushiswap's expansion strategy into other product lines. Below, we will further investigate whether the current valuations are reasonable and how Sushi's new product lines contribute to its valuation.

Sushi.com: Overview

Sushi started in August 2020 as a controversial fork of Uniswap, launching a vampire attack that successfully siphoned off $1 billion of Uniswap liquidity in less than a week. Sushi ran hot, capturing over 9% of total DEX trading volume in its first month, until pseudonymous founder Chef Nomi sold the entire development fund for 38,000 ETH (about $14 million at the time). Under community pressure, Nomi returned all funds to the community within the following week. Sushi faced many setbacks initially, but it has evolved into a community-driven protocol that is now expanding beyond just AMM platforms.

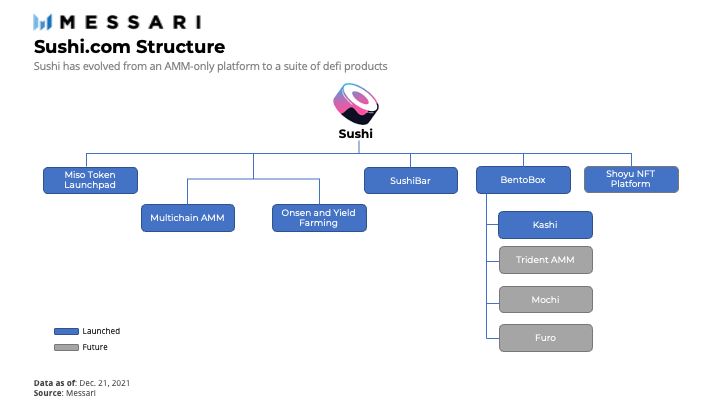

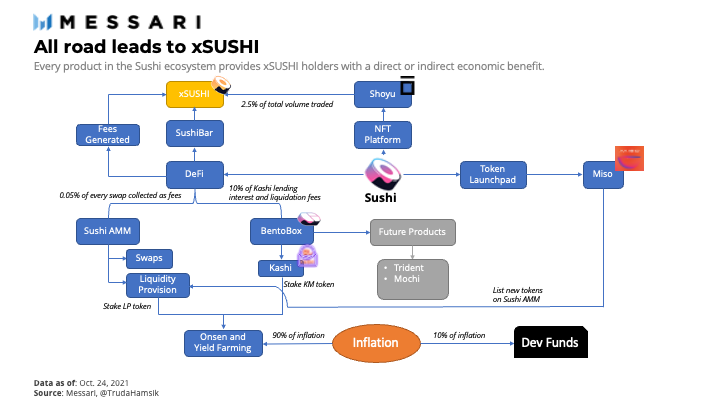

As Sushi expands its product line, the AMM DEX remains the primary product of the ecosystem, even as the project develops across various chains, Layer 2 solutions, and sidechains. The community is looking forward to the release of new BentoBox-based products like Trident AMM, Mochi, and Furo. We will detail each product and how they fit into the Sushi ecosystem below.

- Multichain AMM DEX - Users can pool two assets together and then trade, rather than matching individual buy and sell orders like traditional exchanges. Prices are determined algorithmically based on the ratio of the two. What makes Sushi's AMM DEX unique is its ability to operate across numerous public chains, as shown below. Regardless of which blockchain becomes the leader, Sushi positions itself to capitalize on the opportunity.

- SushiBar - A staking platform for SUSHI token holders. Instead of letting SUSHI sit idle, users can stake it and earn a portion of the platform fees. Users who stake SUSHI will receive xSUSHI tokens in return. xSUSHI will always appreciate relative to SUSHI, as it continuously accumulates value from the platform fees generated (details on fees discussed later).

- Onsen and Yield Farming - Onsen provides additional rewards to yield farmers (liquidity providers for DEX and Kashi) in the form of SUSHI tokens as a liquidity incentive program for new projects. New projects often struggle to guide liquidity in the early stages and initially allocate too many tokens. Thus, they can benefit from joining Onsen, while Sushi benefits from the liquidity and trading volume created by new trading pairs.

- Miso - A token launchpad provided by Sushi, launched in May 2021. Miso simplifies the process of launching new tokens for project creators in a customizable way. Notable projects that have conducted IDOs on Miso include Yield Guild Games (YGG) and BitDAO (BIT).

- BentoBox - A new foundational layer for future financial applications that Sushi intends to provide. Simply put, BentoBox is a vault that holds all assets deposited by users, which can be utilized by applications built on top of it. BentoBox aims to strengthen Sushi as a primary destination where users can interact with minimal gas fees and maximum capital efficiency. BentoBox can facilitate multiple transactions without requiring multiple token approvals. Imagine a user approving BentoBox to access their tokens in their wallet once and depositing them into the vault. The vault will allow these deposited tokens to be used in any BentoBox application without needing to approve wallet token access again. BentoBox optimizes capital efficiency by implementing yield-generating strategies on idle assets held in the vault. These strategies include lending, low-risk yield farming, staking, and flash loans.

- Kashi - The first product launched based on BentoBox. Kashi is a lending product where each lending pair is isolated from one another. This prevents the platform from suffering disasters due to rapid depreciation of certain collateral assets, as risks are contained within their respective lending markets rather than shared across all markets as implemented by major DeFi lending protocols like Aave and Compound. In addition to lending, users can borrow various tokens and short margin.

- Trident AMM (not yet released) - The next-generation AMM from Sushi based on BentoBox, aimed at improving capital efficiency. Trident will allow liquidity provision through four different pool types. The wide variety of pool types allows users to select the pool that best fits their risk profile and provides more flexible portfolio management.

- Mochi (future product) - A system for launching organizational contracts or DAOs on BentoBox. DAOs launched on BentoBox, such as Moloch DAO V2, will benefit from the yield generated by their vault assets without requiring additional actions or proposals. Essentially, a DeFi-based DAO.

Tokens

SUSHI token holders have governance rights over the protocol. The supply of SUSHI tokens can be summarized as follows:

Circulating Supply: 238,700,000

Max Supply: 250 million (expected to reach in November 2023)

Inflation: 10% of inflation is allocated to the development fund, and 90% of inflation is allocated to Onsen and yield farming markets to attract liquidity to the Sushi ecosystem.

Let’s break down how each product contributes to the income for xSUSHI

- Sushi AMM - Accounts for 0.05% of total trading volume on Sushi AMM

- Kashi - 10% of paid loan interest and 10% of liquidation volume

- Shoyu (future) - 2.5% of total trading volume on the Shoyu NFT platform

- Onsen and Yield Farming - Attract liquidity to Sushi through farming incentives. Higher liquidity reduces price slippage, thus attracting more trading volume to Sushi AMM.

- MISO - Encourages new listings on sushi.com. This attracts greater trading volume to Sushi AMM. In most cases, new token listings attract trading volumes above average.

- Trident AMM (future) - 0.05% of total trading volume on Sushi AMM. Only time will tell if the improved user experience due to enhanced capital efficiency and reduced gas usage will attract more platform trading volume.

Valuation

We use the price-to-sales ratio to derive the valuation of the SUSHI token. It is important to note that revenue/sales primarily depend on the fees collected from AMM trading. Other future revenue streams can be seen as added value, which will be discussed further in this section.

We adapted from Mira and Ryan's research article, selecting several comparable products for Sushi, including publicly listed centralized exchanges, private centralized exchanges, and decentralized exchanges. These comparable companies were chosen due to their similar business models. Sushi and other similar products act as intermediaries between buyers and sellers. Exchanges/protocols match buy and sell orders and charge fees from each order as their primary source of revenue. The liquidity provider fees for Sushi can be viewed as operational expenses, with the portion allocated to xSUSHI holders considered as earnings, similar to how companies distribute part of their earnings as dividends to shareholders.

The analysis will be divided into bull, benchmark, and bear cases:

- Bull Case - Average price-to-sales ratio for decentralized exchanges, which are growing rapidly and have greater growth potential, thus assigned high ratios.

- Benchmark Case - Average price-to-sales ratio for centralized exchanges, which are more stable and already have a larger user base.

- Bear Case - Sushi maintains the same price-to-sales ratio, with products unable to adapt to the market, and the only product users need is the AMM DEX.

Now, we use the average price-to-sales ratio, combined with estimated growth in Sushi DEX trading volume, to calculate the value of the SUSHI token as follows.

The above analysis assumes that after 2021, Sushi DEX will experience a slowdown in growth due to the cooling of the cryptocurrency market. Considering the slowdown in 2022, the estimated monthly sales growth is divided by four, and then halved each subsequent year. The target price is calculated by multiplying the total annual revenue for each period by the corresponding price-to-sales ratio.

Beyond DEX

At this point, you must be wondering how other products benefit the Sushi ecosystem, and whether we can derive any value from them?

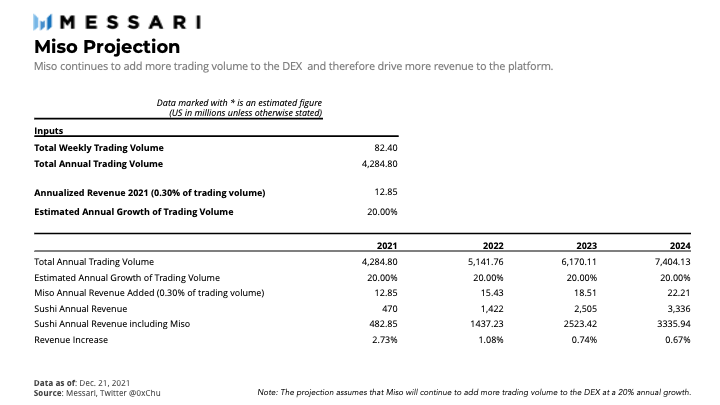

Well, new products provide users with new surfaces to interact with the protocol, thereby increasing revenue and user retention. Rachel Chu stated on Twitter that the 20 projects launching tokens on MISO generated over $82.4 million in additional trading volume for the DEX weekly. Beyond the increase in quantity, Sushi is likely to continue gaining new user bases that it otherwise would not have reached.

Based on Rachel's weekly trading volume, we calculated that Miso would deliver an annualized trading volume to the DEX in 2021. From there, we assumed Miso would continue to add more trading volume to the DEX at a 20% annual rate. Since the revenue charged is 0.30% of total trading volume, the income contributed by Miso can be calculated. According to the above projections, Miso will be able to generate over $5.1 billion in trading volume and $15 million in annual revenue in 2022, which is 1.08%.

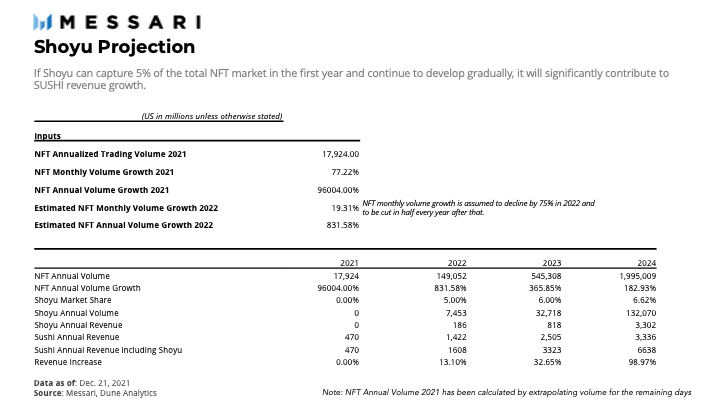

So far, three industries have found their product-market fit: DeFi, NFTs, and gaming. Future integrations of Shoyu will allow Sushi to cross-sell products to users. With the rise of NFTs and NFT-based games, it is reasonable to believe that Shoyu will be able to bring substantial cash flow to xSUSHI. According to the model, if Shoyu only grows to a 5% market share in 2022, it will bring over $186 million in revenue to xSUSHI holders, contributing to a 13.10% increase in revenue.

The revenue contributed by DEX, Shoyu, and the Miso Launchpad has been aggregated to calculate the SUSHI price in each scenario. The model assumes that Sushi's DEX will manage to facilitate over $474 billion, $834 billion, and $1.11 trillion as the entire DEX industry grows. Additionally, the model anticipates that Shoyu will be able to compete with other NFT markets and capture 5% of NFT trading volume. Finally, Miso will continue to create new revenue streams at a 20% annual growth rate. The forecasts provided here are very optimistic, but they are achievable given the current adoption rates in the industry.

Conclusion

AMM is a highly competitive industry. With the launch of Trident AMM, Sushi must ensure it retains or increases its share of DEX trading volume. This is crucial for Sushi's survival, as Uniswap V3 has so far effectively improved capital efficiency, increasing the ratio of daily trading volume to the total value locked in V2 by about 400%.

Moreover, caution should be exercised regarding industry risks. While AMMs are clearly the dominant model for DEXs, whether this trend will persist in the long term remains to be seen. Recently, conflicts among Sushi team members led to the resignation of engineer and CTO Joseph Delong amid infighting. After a period of chaos, discussions heated up, and several proposals created by Alex Woodard (Arca Funds) and Daniel Sesta (Frog Nation) have been released to potentially drive synergies and establish more organizational clarity for Sushi.

Sushi has proven that a community-driven movement can achieve the same success without VC backing. With various contributions from the entire community, Sushi continues to evolve not only across different industries but also across different chains, highlighting its key advantage - optionality. Sushi's ability to narrow the valuation gap will depend on its future DEX performance relative to the industry and whether new products will generate the expected substantial revenue streams.

Risk warning

Risk warning Risk warning

Risk warning