Use data to debunk the investment myths of a16z and Coinbase

You do not own Web3! The Curse of Coinbase and How Venture Capital Firms Sell Cryptocurrency to Retail Investors

You do not own Web3! The Curse of Coinbase and How Venture Capital Firms Sell Cryptocurrency to Retail InvestorsAuthor: brown guy in fintech. (Fais)

Source: Old Yuppie (WeChat public account ID: laoyapicom)

Even though venture capital firms claim to promote "decentralization," former Twitter CEO Jack Dorsey has been calling for venture capital firms to profit from altcoins. This made me think of how Marc Andreessen actually has a seat on the board of Coinbase, while Coinbase publicly discloses the tokens he has invested in. Isn't that a conflict of interest?

I wonder how these coins perform in the long term, especially when layered over Bitcoin and Ethereum, making it difficult to calculate relevant return metrics.

If tokens, especially VC-backed tokens, consistently underperform Bitcoin/Ethereum after listing on Coinbase, it suggests to me that insiders are waiting for a major, dollar-based crypto exchange listing opportunity to sell—venture capital profiting at the expense of retail investors.

These insiders include venture capital firms like a16z, and incredibly, Coinbase's own venture capital department, which has publicly disclosed many of its portfolios. Other exchanges like Kraken, FTX, and Gemini are also actively involved in venture capital and have listed their own portfolios.

Why is this important, and not just a step-by-step, nerdy investment? First, Coinbase is like the New York Stock Exchange for cryptocurrencies—being listed there brings massive trading volume and typically huge profits for every participant. But unlike the NYSE or NASDAQ, Coinbase can use its own criteria to choose any crypto asset it wants to list.

Second, the returns from a16z and Coinbase themselves are particularly interesting because a16z is said to be one of the best investors in the field, and there may be conflicts of interest. Is this financial game rigged?

Third, Coinbase shifted its strategy last year from being cautious to boldly aggressive. This raised the stakes for them and their users.

Thus, I began digging, but what I found shocked me: most cryptocurrencies underperform over time, with returns getting worse, while VC-backed coins perform the worst.

Over the past few years, Coinbase has announced the names of coins it is considering for listing, yet they have not been listed. I analyzed these coins—finding that they performed even better than those that successfully listed on Coinbase.

Let's dive deeper.

Coinbase Effect or Coinbase Curse?

For years, being listed on Coinbase has been the holy grail of cryptocurrencies—equivalent to an IPO on Wall Street. Messari, a cryptocurrency research firm, documented that the average Coinbase listing gained 91% in the first five days.

But I believe this analysis has two flaws.

This is an extremely short time frame. If you, like me, believe that most coins' returns come from illiquidity rather than intrinsic value, then the sudden influx of buyers after listing will create a hype, but as insiders' lock-up periods end, the returns will ultimately turn negative.

What do I mean by illiquidity? Essentially, many people have large supplies locked up or "locked" in DeFi protocols. Project developers and investors will hold large amounts of tokens, but over time, the supply will be released.Showing returns on an absolute basis is meaningless. If you are a hedge fund, you must beat a benchmark. The benchmark for any cryptocurrency should be Bitcoin (BTC) and/or Ethereum (ETH). In my view, Ethereum makes sense because most of these "web3" tokens are built on Ethereum's vision rather than Bitcoin's.

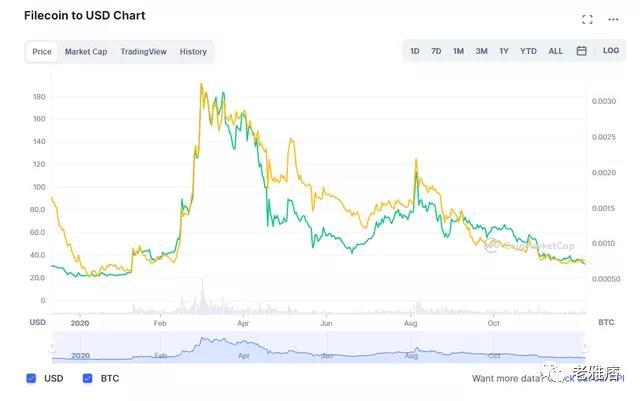

For example, the Coindesk article above cites Filecoin's "sixfold" return. However, investors who chose to buy Filecoin instead of Bitcoin at the time of Coinbase's listing on December 10 actually performed poorly relative to Bitcoin, quickly declining in the first month (yellow line).

Note: The yellow line represents performance relative to Bitcoin, while the green line is in USD.

Most of the returns they cite are due to Bitcoin's rise, while Filecoin's performance has actually severely lagged behind Bitcoin since then—by 55%!

At this point, most people with cryptocurrency trading experience are looking at the price of BTC or ETH rather than the price in USD for evaluation.

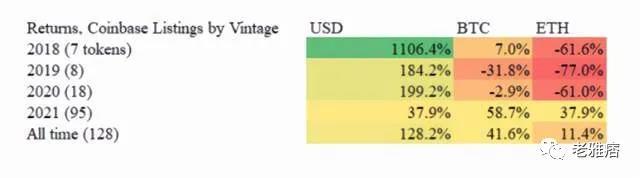

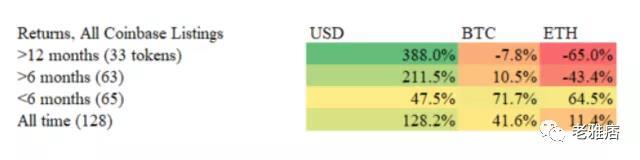

How does Coinbase's listing performance look? I obtained 128 listings from Coinbase (excluding stablecoins and algorithmic stablecoins) and separated them by year.

Note: In most cases, I used the dates published by Coinbase for Coinbase Pro. Most tokens typically start trading within two days, often on the same day.

In my view, these results largely confirm my argument. Coinbase and venture capital firms may tout dollar returns, proving that cryptocurrencies allow retail investors ("the community") to participate in the growth of these networks.

But the reality shows that most returns occur very early after listing—coins from 2021 performed well, but all coins from 2020 and earlier performed poorly! What does this indicate? The return rate for 2021 was also lower than the 91% popularity rate cited by Messari, suggesting that they all lost value after the hype.

Once a coin has been on Coinbase for a year, it seems to consistently lag behind Bitcoin and Ethereum.

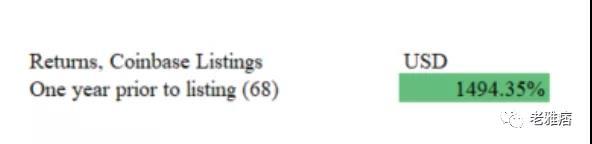

I also found some coins for which I could find return rates from the year before listing (68 out of 128) just to illustrate that these coins did not perform poorly since their inception.

If we break down the coins listed last year, we still see the same pattern: coins from the last six months (65 coins) performed better than those from the previous six months, yet the recent six-month coins also lagged behind the average 91% of coins.

If you take just two coins (Polygon and Solana) from the 63 coins over six months, Coinbase's returns also turn negative (down -10.5% relative to Bitcoin, and -55.0% relative to Ethereum).

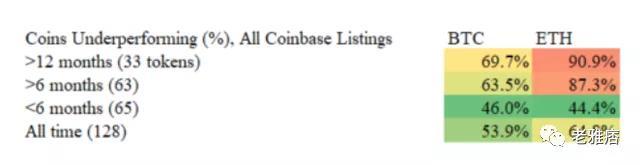

Looking at the hit rate, 91% of the listed tokens lagged behind Ethereum in returns over a year ago, and 70% lagged behind Bitcoin. These coins also performed worse the further back you go.

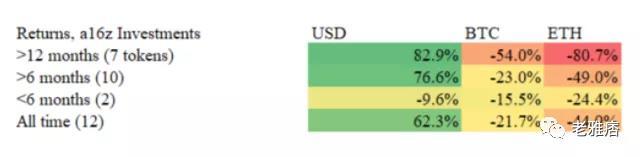

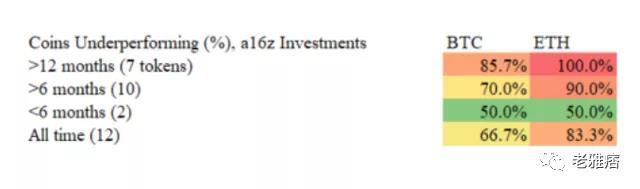

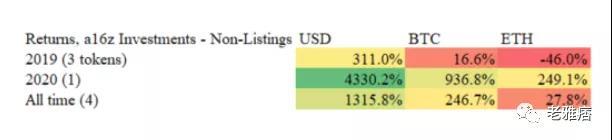

Of course, if we filter a16z's listings on Coinbase, do we get better results? Quite the opposite…

A16z's overall return rate is much worse than Coinbase's listings. To me, this smells like insider trading. Given a16z's access, these should be the best tokens, yet conversely, 100% of the tokens over 12 months and 90% of those over six months lagged behind Ethereum.

1) Retail investors cannot create a complete portfolio like venture capital firms can.

2) This is a publicly traded project, so returns should resemble stocks, with a positive average return rate.

3) VC's "hit rate" should be "100x" returns to compensate for dozens of failures, yet among a16z's listed projects, only one (Solana) has successfully doubled in BTC terms.

Back in 2018, when I was trading tokens, looking at the cap tables of big-name investors like Andreessen Horowitz was the best way to avoid falling into "rug pull" investments: when a token suddenly turns into a scam, I would say it was useful.

However, when I tried to deploy a similar strategy on Coinbase in 2021, I continuously lost money. I think I now have a vague understanding of why.

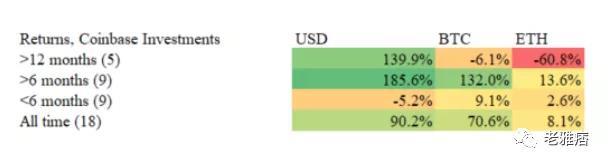

I also looked at Coinbase Ventures' investments. They seem to perform better—though older coins also perform poorly. Coinbase's portfolio is relatively young, and its strong performance is driven entirely by two coins: Polygon and Wrapped Luna. Without these two, the average return rate of Coinbase Ventures' other 15 coins is -6.0% BTC and -42.6% ETH.

My favorite angle is to look at when Coinbase and a16z invest together. This seems to be the darling of the industry (the darling of DeFi? (If you're curious, these five are Uniswap, Celo, Keep Network, Rally, and Compound).

As a VC investor in the U.S., there are good reasons to sell on Coinbase. (1) You don't want to be double-taxed; trading into non-dollar currencies can lead to double taxation. (2) You are a U.S. entity and cannot open accounts on Binance or other exchanges that list these coins first. (3) Hosting and trading on Coinbase is safer, as you may need to use hardware wallets on other exchanges, etc.

I also researched why Coinbase's investments might perform exceptionally well. One thing I noticed is that Coinbase seems to announce its investments at lower market caps (see below).

For 7 out of the 18 Coinbase-supported coins, I checked whether it was Coinbase or Binance (a more regulatory-friendly exchange) that listed first. In 7 cases, Coinbase acted first—this ratio is much higher than normal. One can't help but wonder if Coinbase knows that Binance's listings would harm their profits by siphoning off returns?

(If you're wondering whether a16z's poor return rates can be explained by larger listing market caps, the answer is no—they appear to be worse.)

Evidence

Their spokesperson might say that these numbers alone do not prove anything about Coinbase or a16z. Newer cryptocurrencies perform better because they have better technology! Now, before we sue you, please shut up.

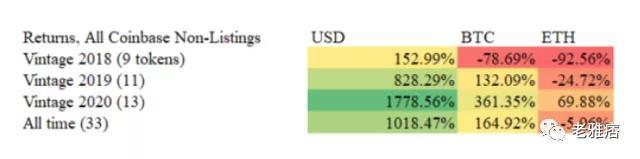

But we are fortunate to have what economists call a "natural experiment." Until 2020, Coinbase would announce that they were considering listing a group of tokens. Some received the green light (including those in my analysis above), while others did not.

How did the returns of those unlisted tokens fare? Many of them are exploding. Based on both USD and BTC, the performance of unlisted coins significantly outperformed listed coins, while slightly lagging behind ETH's performance (consistent with my view that ETH is the best benchmark).

Importantly, as the age of the coins increases, returns also worsen—even worse than Coinbase's coins. I believe there are several reasons for this. (1) Coinbase's selection criteria may have excluded the worst of the bad coins. (2) Unlisted coins have been around longer, meaning they have more time to degrade.

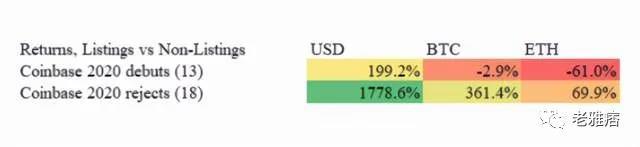

If we only look at 2020, we have a fairly average comparison (17 Coinbase listings vs. 13 non-listings), and the difference in return rates is astronomical. Four non-listed tokens outperformed ETH, while only one of the 17 actual listed companies did.

This negative effect is so strong that in 2019 and 2020, if you picked coins that were not listed on Coinbase, your chances of beating BTC or ETH returns were significantly higher—for 2020, the odds of beating ETH were as high as five times (94% of Coinbase's tokens performed poorly in 2020, compared to 69% of those rejected by Coinbase). This strongly suggests that the liquidity of dollars seems to outweigh Coinbase's "halo effect"… or that people are selling off.

This provides good support for my two arguments. (1) Most coins' appreciation is due to illiquidity rather than value (as both listed and unlisted degrade over time). (2) The liquidity on Coinbase leads to poor performance of these coins, perhaps partly due to insider selling.

Insider selling? You didn't mention that part…

Lock-Up

We have looked at a16z coins and found that they underperform BTC, ETH, and the average of Coinbase's listings.

So how about the unlisted tokens? The sample size of four coins is much smaller, but the results are quite striking.

The returns of a16z's unlisted investments actually managed to outperform Bitcoin, which is not the case for listed coins. Arweave has investments from both a16z and Coinbase Ventures but has never been listed—so far, it has performed the strongest, having increased tenfold since Coinbase said it was "evaluating" whether to list it!

We can essentially tell our story with three coins from the "DeFi Summer" of 2020.

These tokens have all experienced the same "macro" environment. The unlisted tokens are the best; the listed non-VC tokens are better; while the listed VC-backed tokens are the worst.

What does all this mean?

The first thought I have upon seeing this is that I personally would not buy anything listed on Coinbase, especially after the initial hype, and I would stop trusting VC-backed tokens. It turns out I haven't lost all my trading skills.

The logical conclusion is to only buy BTC and ETH, although these return rates have also declined year over year (including last year), yet they still carry much less risk than these small coins. Overall, they seem to offer a greater opportunity than buying "web3" tokens. (Please reread the disclaimer at the top).

I believe this has significant implications for some major debates in cryptocurrency.

A rebuttal to "Balaji's" argument. Balaji likes to emphasize repeatedly that one of the main value propositions of "web3" is to help "the little guy": allowing users to participate in value creation (for example, owning some equity in projects). However, the vast majority of users are buying on Coinbase, so they are simply not keeping up with Bitcoin's performance.

Supporting "Jack's" argument. Jack's argument is that most tokens are owned by venture capital firms, which use the rhetoric of "web3" to siphon off the liquidity created by the demand for deflationary assets, thereby ruining Bitcoin. Jack is a Bitcoin mogul, and this is his own viewpoint, but so far, he seems to have a point.

Other thoughts: Coinbase may also be losing its brand here. They may need new assets to encourage trading, but others believe that stepping away from a cautious approach may be Balaji's influence—given his rhetoric about "helping" investors, this makes sense, but the data suggests he may be wrong. Additionally, Balaji has worked at a16z and Coinbase—so no one can really clarify his motives.

Finally—do I think something improper is happening between these two companies? Actually, I don't think so—they may not have even looked at these numbers themselves. They may just be transparent because it's hard to get data from other investors and exchanges. But so far, their influence is also the largest.

On the contrary, I think this is a microcosm of how bad the incentive mechanisms are in cryptocurrency—venture capital firms and private investors, who used to have to wait a decade for liquidity, can now achieve it within a year. The last time this happened was in 1999, and we know how that ended. This is a secret of risk, and then the risk quickly gets passed on to the public.

Readers may raise objections to my analysis:

You don't hold cryptocurrencies. No, I am long on BTC, ETH, and NEAR, hedging some recent volatility with a March 22 $26 BITO put option.

You're a Bitcoin whale. No, I worked for Joe Lubin and ConsenSys for three years.

You haven't looked at other exchanges. Given that Coinbase has had the most "blockbuster" listings so far, I think the dilution of liquidity there is also the strongest. I also think the relationship between a16z and Coinbase is the best subject for study because a16z and Coinbase are closely linked and have the most influence. I also suspect a16z has accounts at Kraken or Gemini, and given their vested interests in Coinbase, I am interested in doing an analysis with Binance, so that may be a future analysis.

These aren't bad returns. The return rates for coins listed last year (basically 2021) are still decent, with positive returns in USD. That's good, but I want to say, if these coins only went up because of Bitcoin, what happens when Bitcoin goes down? And if you are just losing to Bitcoin, then what is the point of Coinbase?

Before writing this article, I ran the original data in December (when BTC was around $50,000), and all the same trends held.

Proposed Solutions (Hello, Gary Gensler)

The first question I want to ask is, is this legal? Both NASDAQ and the New York Stock Exchange have risk funds, but before going public, the SEC must approve their investments! There are no regulatory bodies checking every Coinbase listing. Of course, maybe they have processes, but if no one audits, would you trust the financial statements of any old company?

Think of it this way: it's like Google investing in Goldman Sachs, then Goldman publishes a research report on Google's work, and then Google does an IPO on its own investment. And no one needs to disclose their trading content. In such a terrible incentive mechanism, would you get any valuable information?

Here are some solutions I believe are necessary to better protect investors and correct some of the bad incentives.

- Fund disclosure. Hedge funds and mutual funds are regulated by 13F and 13D: for 13F, they must disclose their holdings quarterly, and for 13D, whenever they acquire more than 5% of a public company.

My point is that venture capital firms and other cryptocurrency investors should do the same for cryptocurrencies. Want to sell to the public? Act according to public market rules. Otherwise, it is unfair to those big players clicking on Coinbase's billion YouTube ads.

Some might say that 13F and 13D are ineffective and may not help small investors who won't read the documents. But I say this will allow professional investors to assess the tokens of those who have taken on rapid liquidation, which will enhance or damage reputations.

- Fix investor rules—but not just by relaxing regulations. Populists will say, "Abolish accredited investor rules! This hinders people's participation in economic growth!" I say sure. But do you know that public companies (you know, "unaccredited" investments) are also subject to regulatory and disclosure rules?

These advocates want to relax regulations on venture capital (necessary) without public market rules (also necessary). This means S-1 style public filings. S-1 typically discloses relationships between investors and directors, risks, and importantly, ownership of management and major investors.

I believe the Balaji and Ryan Selkis of the world would say this idea would "kill" innovation. Contrary to popular belief, I do not believe companies have extended their time in privatization due to cumbersome rules (though they are cumbersome), while public markets have become more tolerant of losses.

This means you can go public with increasingly larger losses. As a founder or investor, if you can avoid dilution and achieve greater (liquidation) returns, why wouldn't you?

- Close the loopholes for utility and governance tokens. The SEC inadvertently created a huge loophole when it said Ethereum is not a security because Ethereum's coin has utility.

Most DeFi uses a "governance token" model, where one token equals one vote.

Take Celo as an example: "Between 2018 and 2020, Celo raised over $46.5 million by selling approximately 120 million CELO tokens." It later stated that the total supply of tokens would never exceed 1 billion, of which only 6% (60M) were circulating at launch.

Subsequently, it was listed on Coinbase on September 3 (with investments from Coinbase and a16z), with about 12% of coins circulating, which has increased to 37% today over the following 15 months!

The value of this coin lies in its ability to "vote on the generation of stablecoins," so we certainly need a billion of such coins.

If utility/governance coins remain an open loophole, issuing companies need to make a fair estimate of the actual number of tokens users need in their disclosures—so investors can hold them accountable.

Look at the performance since the timeline was significantly accelerated in April 2021 (to 1.2% per month).

- Stricter (non)listing rules. Coinbase currently has no rules regarding minimum market cap, minimum number of shareholders, or minimum daily trading volume. This means that air coins can drop, drop, and drop again.

The New York Stock Exchange and NASDAQ have many such rules, which is why they have the best reputation in the world. These also include rules about how much stock management teams can control. If cryptocurrency exchanges have to delist repeatedly due to lack of liquidity or price drops, it will damage their reputation.

Conclusion

In Urdu, we call a sycophant a chamcha, "spoon"—because they can meet your needs. Ultimately, I am someone on Substack—but unfortunately, I think the current state of crypto investment is that all the "research" you get comes from someone's chamcha.

I don't know if Balaji or Jack will prove correct in ten years, but all of this supports what I call the theory of "Charlie Lee" (the creator of Litecoin): there may be huge demand for deflationary assets like Bitcoin, but the biggest problem is that anyone can create another similar cryptocurrency, so it isn't truly deflationary.

What will the returns of Coinbase's 2021 coins look like next year? I would bet that the same pattern will continue, with coin prices skyrocketing, then underperforming Bitcoin. At the very least, I hope Coinbase users eventually see this—just like you can see it with ETFs or mutual funds.

At best, investors and exchanges want to reshape finance but underestimate its complexity. As Matt Levine says, many cryptocurrencies are just repeating the mistakes of financial history.

At worst, it is the wealthy teaming up with their partners to exploit the bubble, helping them buy $100 million mansions. It is time for these big companies and regulators to step in and ensure everyone has the same standards and data. Until then, buyers should be cautious.

Notes:

In 8 cases, the unlisted tokens had not traded at all before Coinbase's evaluation. In these cases, I used the earliest market data from Coingecko. Interestingly, among these 8 coins that had not traded anywhere and were evaluated for listing, 5 had investments from a16z or Coinbase! I used a16z and Coinbase.

I used a16z and Coinbase Ventures' own investment lists, but in one case (Livepeer), I found an external source indicating Coinbase had an investment, but it was not recorded on their website (it is possible they later withdrew this position).

For the market cap comparison of Coinbase-supported vs. unsupported, I could not find the listed market cap amounts for the following companies: Braintrust, Clover Finance, Jasmy, Kyber Network, Loom Network, Moss Carbon Credit, Voyager Token, Wrapped LUNA, Orchid-protocol.

Risk warning

Risk warning Risk warning

Risk warning