Delphi Digital Report Overview: Trends to Watch in the Crypto World in 2022

The battle for scalability between public chains will continue to heat up before L2 solutions become available; more creators and brands are entering the Web 3 space.

The battle for scalability between public chains will continue to heat up before L2 solutions become available; more creators and brands are entering the Web 3 space.Written by: Delphi Digital

Compiled by: angelilu

Delphi Digital released the 2022 Foresight Report, analyzing hot topics, projects, and crypto trends. Foresight News has compiled this report, and below is an overview of the hot topics.

Scalability War: The battle for scalability among public chains will continue to heat up until L2 solutions are available.

Cross-chain DeFi / Interoperability / Bridges: The rise of the Cosmos ecosystem will indirectly benefit from the public chain scalability war through cross-chain bridges.

Stablecoins: Curve's TVL is expected to reach $23 billion, becoming the largest DeFi application.

Decentralized Derivatives: Decentralized derivatives exchanges will launch across various scalability solutions.

Metaverse, GameFi, and P2E: The play-to-earn concept opens the era of blockchain gaming, with gaming chains competing fiercely.

DAOs: The increase in the number of DAOs will drive demand for governance and coordination tools.

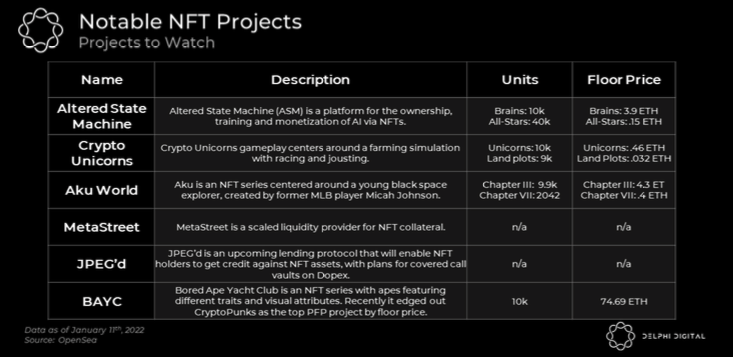

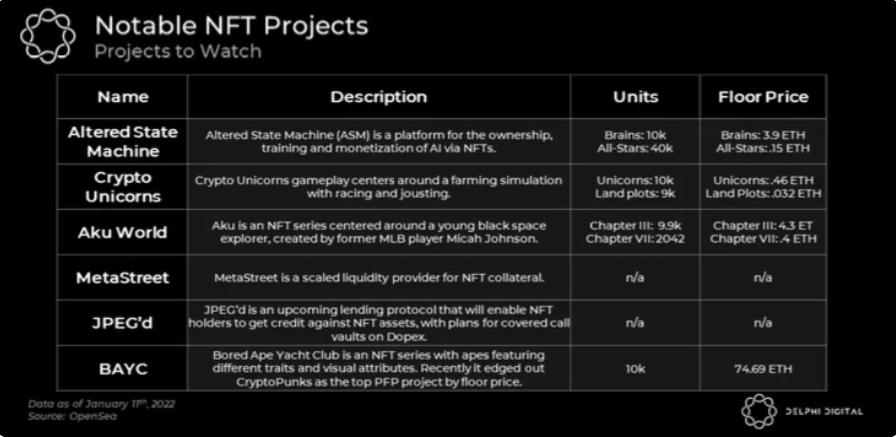

NFTs: 2022 has started with a bang, bringing NFT tools and infrastructure to the forefront.

Creators and Brands Entering the Web 3 Space: More influencers are connecting with fans through NFTs and tokens, and music NFTs are expected to explode in the coming years.

The "Homogenization" of the Crypto Market Will Change: Mainstream cryptocurrencies like BTC will gradually exhibit characteristics of traditional asset classes, while the broader cryptocurrency market will depend on whether assets or protocols are successfully utilized.

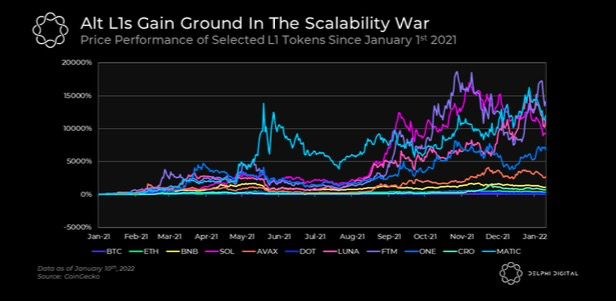

Scalability War

In 2021, major public chains emerged, with names like LUNA, SOL, and AVAX capturing significant investor attention. Despite the heavy promotion of Ethereum's L2 solutions and the transition to ETH 2.0, Ethereum still faces high fees. The "scalability war" will continue to heat up in 2022, as other public chains expand throughput and reduce transaction costs through various methods to attract talented developers and compete for market share.

Ethereum's high fees and congestion will continue to push developers toward other L1s until L2 solutions become more practical (i.e., StarkNet, dYdX for trading, Immutable X for NFT minting/trading).

Modular Blockchains and Data Availability: The rise of rollups has brought about the concept of modular blockchains. A mature blockchain consists of three core components: execution, settlement, consensus, and data availability. However, a blockchain does not need to execute all these functions independently.

Instead, modular chains specialize in one or more of these components and outsource the rest to other specialized chains for greater scalability. For example, a core element of the modular blockchain stack is dedicated data availability chains like Celestia, which have very high data capacity.

Many rollups can leverage this capacity, choosing to dump their data into Celestia for shared security while focusing on scaling their execution.

The ETH merge can be considered the most significant milestone in Ethereum's history, marking the transition from PoW to PoS. However, it has been delayed due to the lack of a hard deadline for the merge. It is publicly expected that the merge will occur by the end of Q2, but you can follow updates here.

From an investor's perspective, after EIP-1559, ETH fees are divided into base fees and tips. After the merge, the tip portion of the fees will go to validators/stakers, and this tip income, along with block inflation, will flow to stakers, making ETH a positive-yielding asset. Additionally, since Ethereum launched EIP-1559 last August, it has become a deflationary asset.

Notably, as more traditional institutional investors enter the crypto rabbit hole, institutional capital flows have begun to expand beyond BTC and ETH, potentially benefiting L1 assets with higher liquidity among the top 10 to 20 coins.

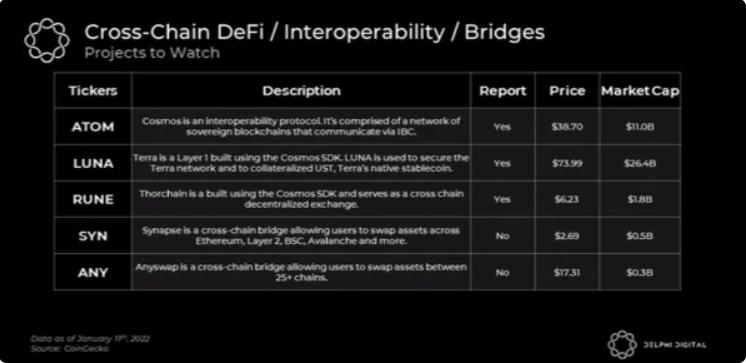

Cross-chain DeFi / Interoperability / Bridges

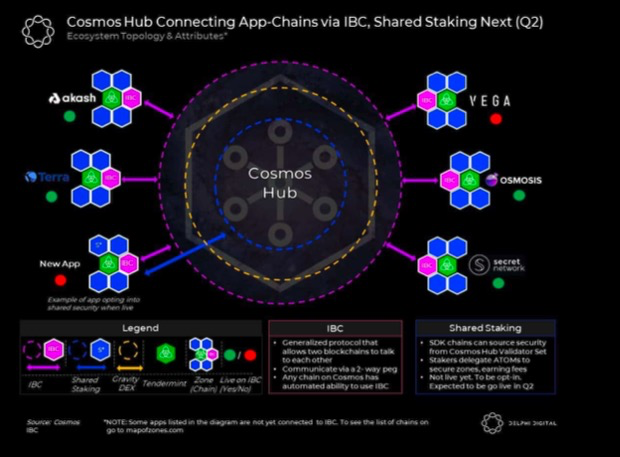

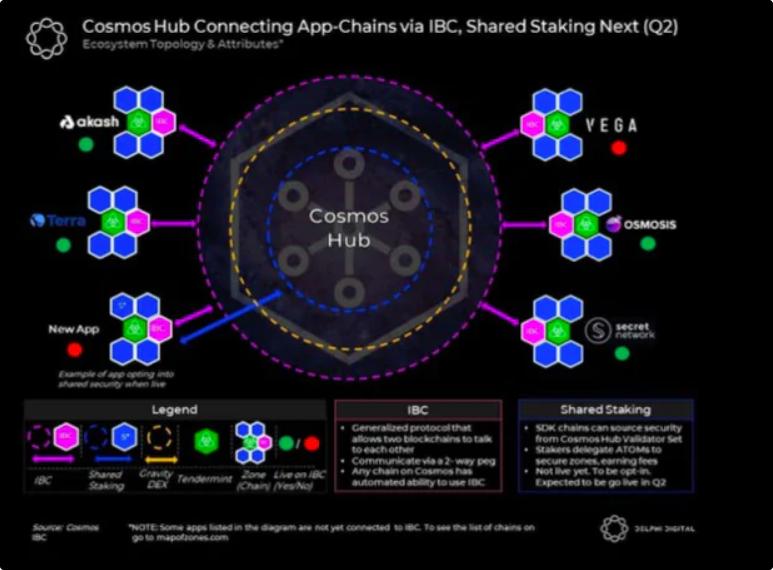

Interoperability and the Rise of the Cosmos Ecosystem

As mentioned in Delphi Digital's in-depth report on Cosmos, in an interoperable IBC world, once-isolated blockchains can communicate with each other. Looking ahead, Cosmos' roadmap for Q2 shows plans to launch Interchain staking, Interchain accounts, liquid staking, and better bridges to connect Cosmos, which will drive its next wave of growth. Notably, Interchain staking can significantly promote the incubation of the Cosmos ecosystem, as it allows developers to more easily launch applications.

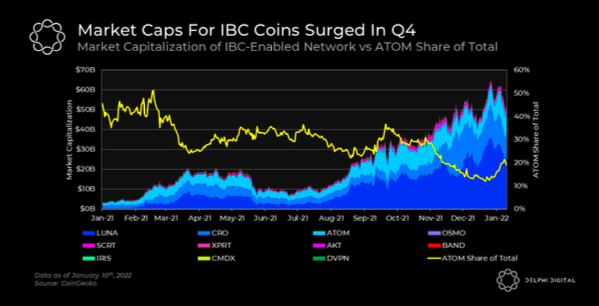

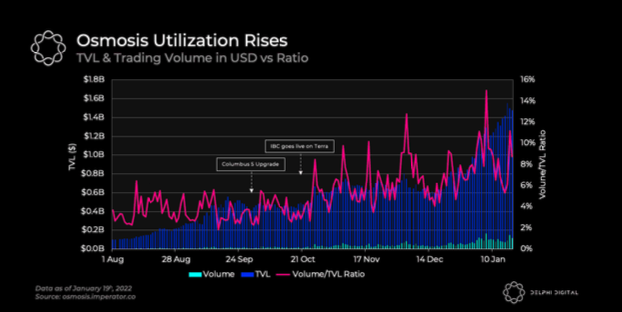

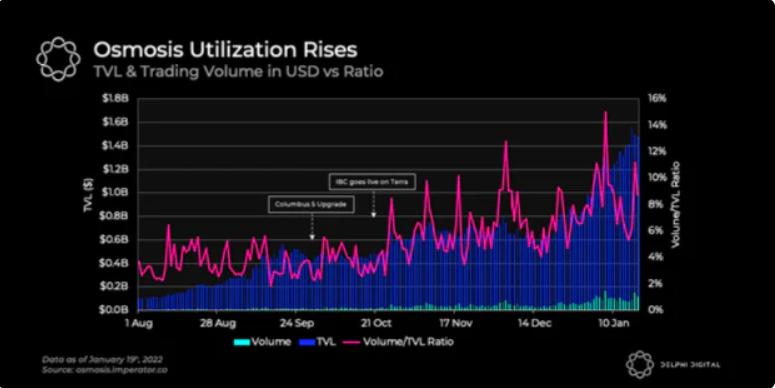

DeFi Supporting IBC: Cosmos Hub will have numerous competing hubs, such as Evmos, Archway, and Juno, which offer different value propositions compared to Cosmos Hub, further stimulating Cosmos DeFi. In fact, Osmosis has already been competing with Cosmos Hub, facilitating more than twice the number of IBC transfers in the past 30 days compared to Cosmos Hub. Delphi Digital believes that the Cosmos season will make the market large enough for players to coexist. Osmosis is handling Cosmos-native DeFi, while THORChain has chosen not to join IBC but supports Asgard, which still has a vast market to leverage native BTC and other assets.

New Liquidity Guides: The emergence of IBC-native DEXs like Osmosis will make it easier to facilitate liquidity guides for community-led and organic projects on IBC without relying on CEXs. Users, stakers, and liquidity providers of tokens like ATOM and OSMO may see more airdrops this year.

Dominance of IBC: While the fundamentals of ATOM are improving and the tokenomics will gradually improve in the future, it is expected that IBC will struggle to maintain its dominance in the ecosystem due to the influx of many new protocols. However, Cosmos does have a healthy start, with 3 million IBC transfers across 27 blocks in the past 30 days.

Bridges / Cross-chain

Another way to play alternatives to L1 and scalability solutions is through bridges and cross-chain infrastructure. Ultimately, the goal of cross-chain infrastructure is to seamlessly transfer assets on-chain in an efficient (and hopefully) decentralized manner. With the continuous emergence of more L1 and L2 solutions, it is still too early to pick a specific asset or even a group of assets that will ultimately win this race. However, it is certain that competition in this space will only intensify, as the multi-chain narrative that erupted in 2021 will not disappear anytime soon.

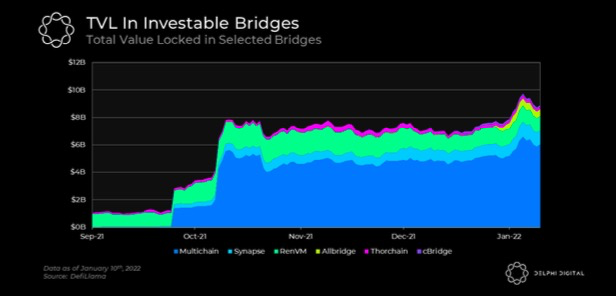

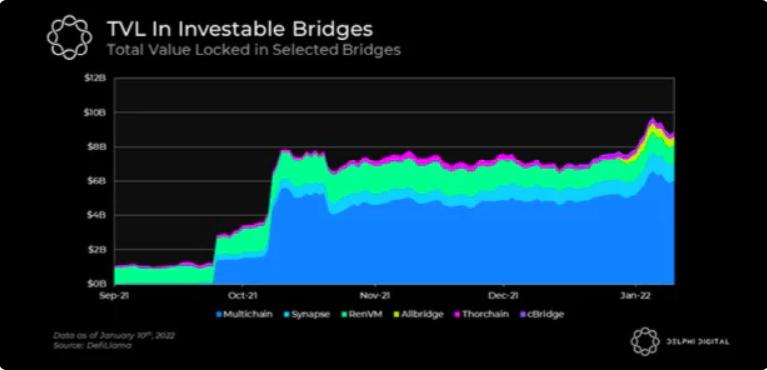

The table above shows that the TVL of some cross-chain bridges has surged since September, currently around $9 billion. From September 1 to early January 2022, this group of cross-chain bridges had an average return of 108%, while ETH's return was -1%, marking a strong performance for alternative L1s that took off in the second half of last year.

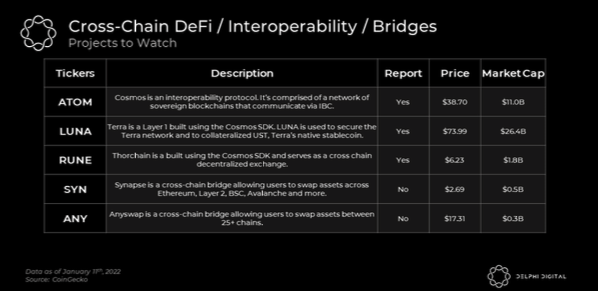

Below are some cross-chain bridges listed by Delphi Digital analysts:

Hop Bridge (Hop): Hop is a pioneer in cross-rollup development. Although its current TVL of about $100 million is relatively small, the protocol has not yet launched a token. Hop Bridge will become a fundamental component of Ethereum-centric rollups.

THORChain (RUNE): THORChain's most significant milestone is the introduction of liquidity pool nodes, allowing the community to combine in RUNE and contribute to the network's security. This will allow liquidity pools to grow without upper limits.

Synapse (SYN): Synapse connects different L1 and L2s. Since its launch in September, SYN has outperformed most other L1s but carries more risk than SOL, LUNA, AVAX, etc.

Cosmos (ATOM): In the scalability war among L1s and L2s, cross-chain liquidity bridges will become indirect beneficiaries. Cosmos is expected to shine in the multi-chain future, with more chains and protocols utilizing their infrastructure and IBC.

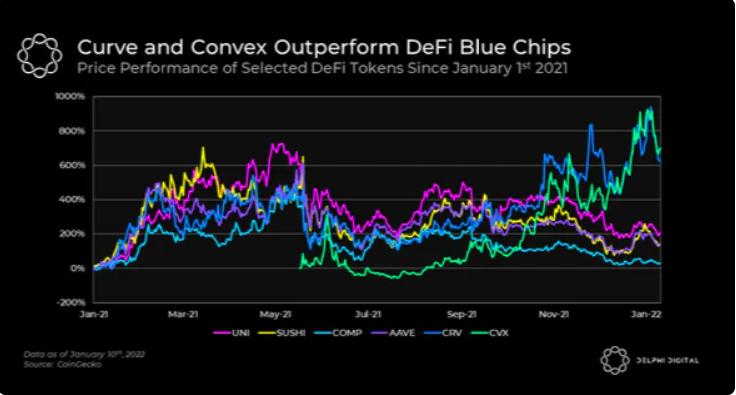

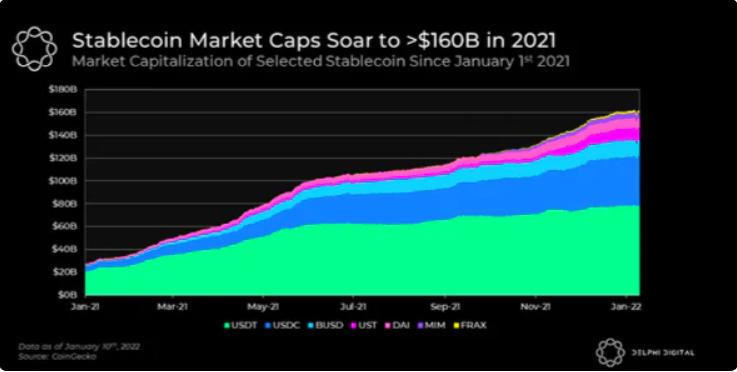

Stablecoins & Curve War

Stablecoins experienced explosive growth in 2021, with a total market cap exceeding $150 billion. This surge proves stablecoins as the "killer application" of cryptocurrencies, with products and markets highly aligned, making assets like USDC and USDT ubiquitous throughout the cryptocurrency ecosystem, a trend that will continue.

Decentralized Stablecoins

If regulators begin to crack down on stablecoins, it may drive users and builders to use decentralized stablecoins as alternatives. Click here to view Delphi Digital's article on LUNA and UST.

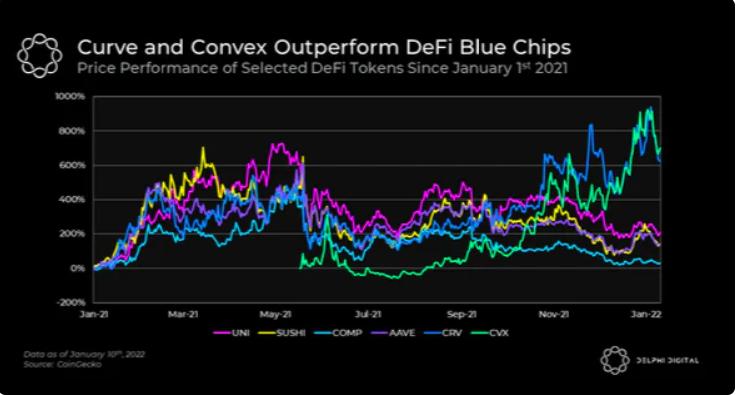

Delphi Digital also predicts that the symbiotic relationship between Curve (CRV), the king of decentralized stablecoin minting, and Convex will make it the largest application by TVL, reaching $23 billion (with the current TVL close to $19 billion at the time of publication), outperforming other DeFi blue chips.

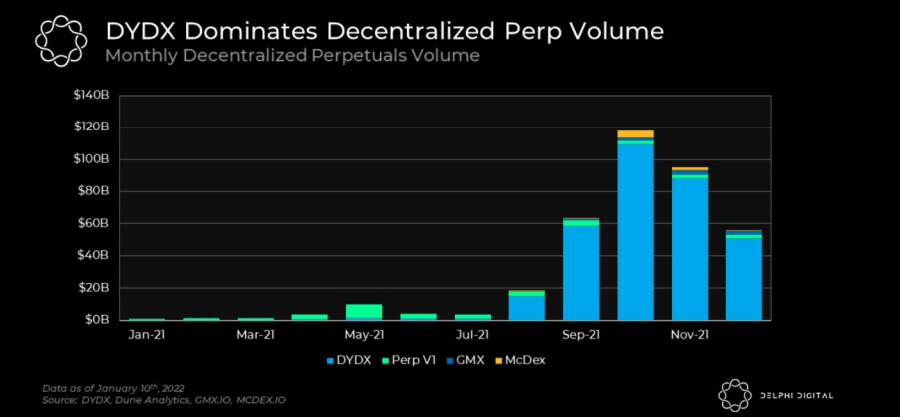

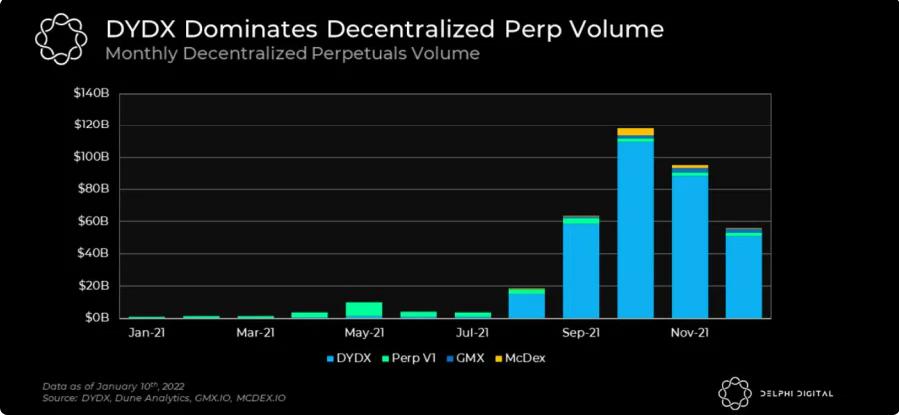

Decentralized Derivatives

Decentralized derivatives rapidly gained traction in 2021, with significant growth potential before surpassing their centralized counterparts. dYdX is a leader in the DeFi derivatives space, and Delphi Digital expects it to remain an important player. However, competition in decentralized derivatives may heat up in 2022 as more perpetual contract exchanges launch across various scalability solutions.

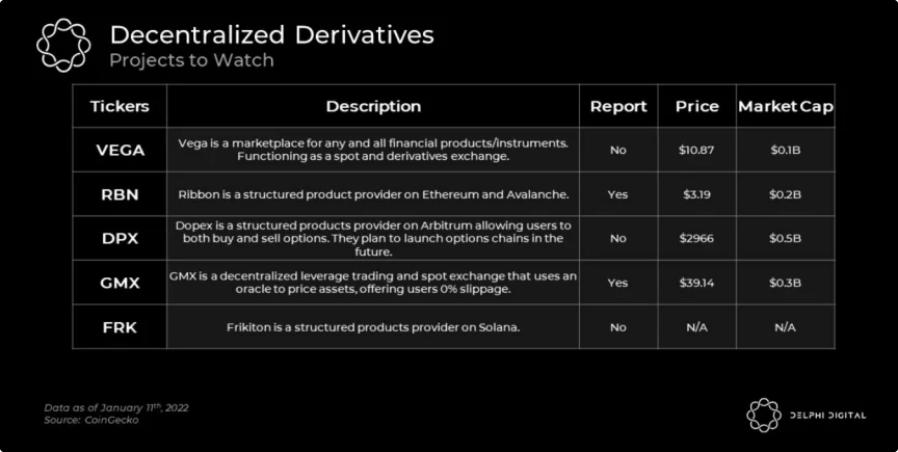

In its current state, dYdX's token lacks value accumulation beyond its governance capabilities, but this may change with the launch of dYdX V4. Below are some other perpetual contract protocols and DEXs listed by Delphi Digital analysts:

- Vega: Decentralized derivatives and spot trading market.

- GMX: Uses an oracle pricing model, serving as both a spot and leveraged exchange.

Additionally, the feasibility of emerging options and structured products is increasing in the development of various L1s and L2s. Ribbon and Opyn launched decentralized options products as early as April 2021. The integration of options protocols and perpetual contract platforms is another innovative area that allows for delta hedging and improves capital efficiency. Delphi Digital analysts list two options projects:

- Zeta Markets: An options exchange that uses the Serum order book and has a native Zeta AMM integrated, combined with Solana's high throughput, low latency, and low fees, making it a potential incentive for institutional participants to trade DeFi options seriously.

- Dopex: Uses a covered call strategy, where call options are not sold to market makers (who charge a spread) but are sold back directly to buyers of call options on the platform. Dopex is also developing an options chain similar to Deribit, with pricing based on the IV multiplier represented by market makers.

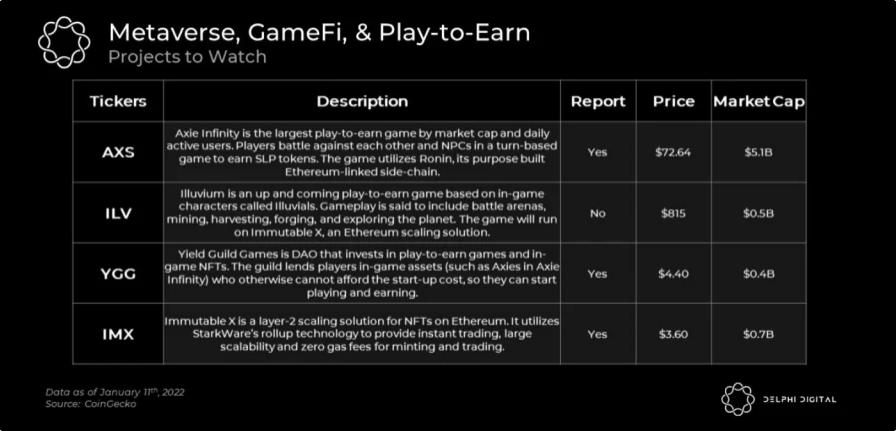

Metaverse, GameFi, and Play-to-Earn

Last year, Axie Infinity exploded and proved the concept of play-to-earn. Now, a series of P2E games are attempting to replicate Axie's success. As the ecosystem grows, filtering out noise from innovation will become an increasingly important and challenging task. Most projects will ultimately be eliminated, but this is just the beginning of a new era in gaming, with projects like Illuvium, Crypto Unicorns, and Ember Sword bringing AAA graphics and gameplay. Additionally, gaming chains are also in competition, with Immutable X, Ronin Chain, Solana, and Polygon currently standing out.

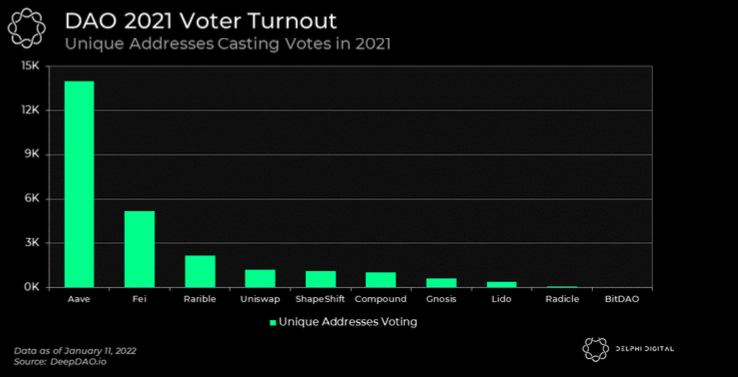

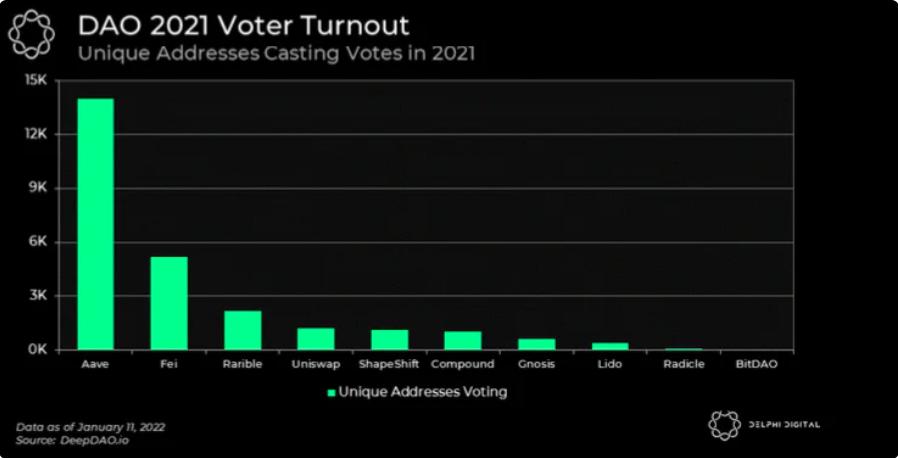

The Journey of DAOs

2021 was a year when DAOs gained prominence, and their definition has changed. Previously, DAOs were used by protocols like Uniswap to vote on grants and fund allocations. Now, DAOs are seen as instant entities coordinating groups with shared bank accounts and payment capabilities, enabling crowdfunding, capital deployment, and linking voting to tangible outcomes. Experiments like Constitution DAO have demonstrated that decentralized autonomous organization groups can accumulate tens of millions of dollars in weeks and collectively purchase assets. Some DAOs already possess hundreds of millions (or even billions) in funds and tens of thousands of users, with new DAOs continuously emerging.

DAOs need to accumulate a certain amount of secondary assets to establish a viable treasury; otherwise, they risk significant losses of native token capital during market downturns. Therefore, many DAOs are beginning to experiment with earning yields to manage their treasuries by acquiring voting escrow tokens, hoarding stablecoins, employing PCV, and deploying assets.

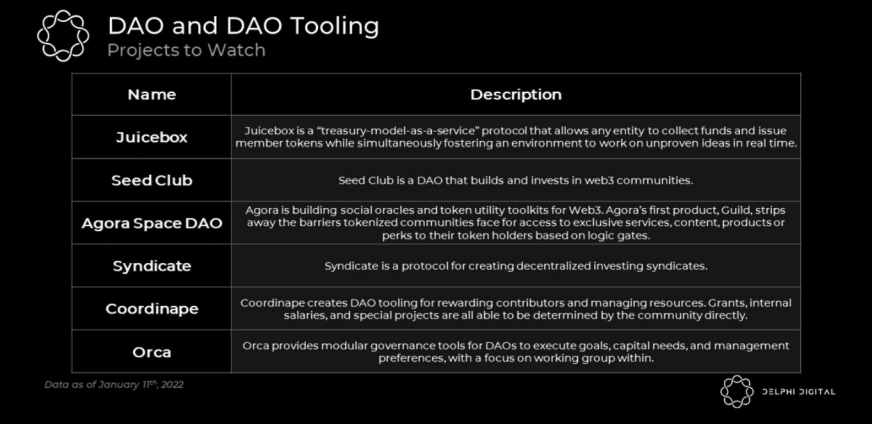

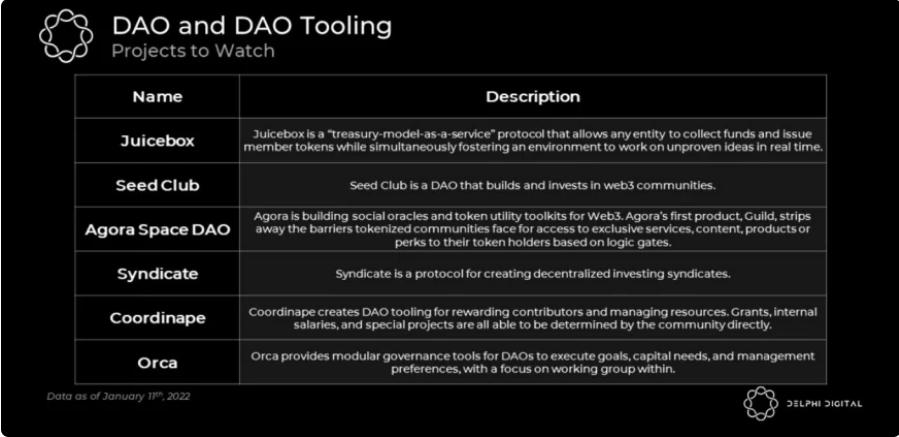

The increase in the number of DAOs will drive demand for governance and coordination tools, and smaller sub-DAO units will emerge within DAOs. It is expected that smaller autonomous units will surge and execute on tools like Orca Protocol and Squads. Additionally, the number of Meme DAOs may explode, with the biggest beneficiaries of this growth being the tools and platforms for DAO creation and management.

NFTs: From Static Collectibles to Interactive Digital Ownership

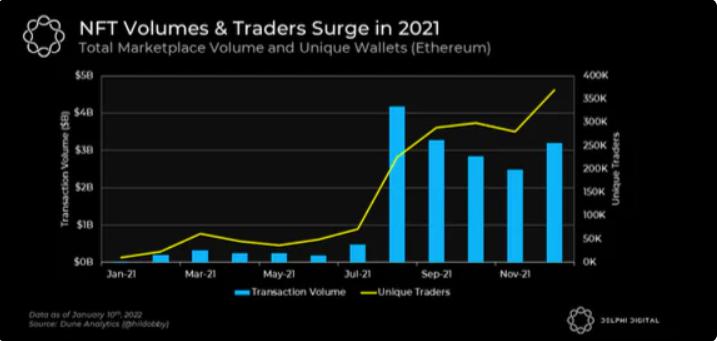

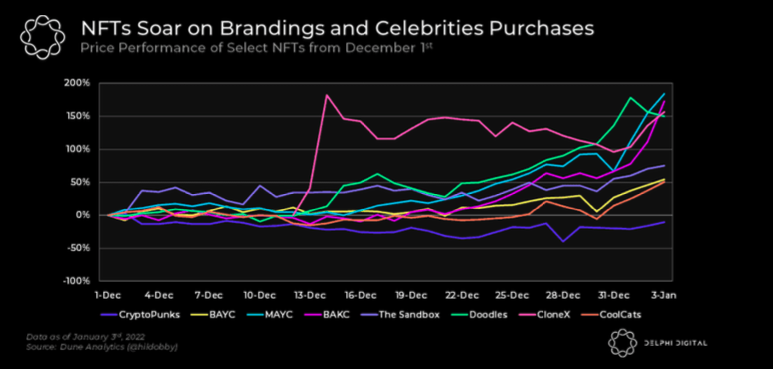

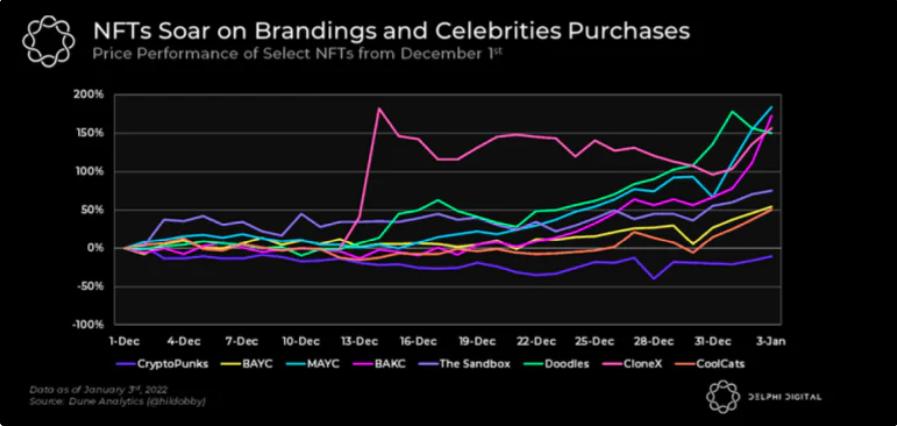

NFTs took off in 2021. Although NFTs have existed for a long time, 2021 was the year they entered mainstream discourse, with marketplace platforms like OpenSea experiencing explosive growth. The NFT market has attracted many traditional companies and celebrities. NFTs have also started 2022 with a bang, with January 2022 being the best month for NFT trading volume and quantity, and buyers remain highly excited about new projects.

NFT tools and infrastructure are also gradually coming to the forefront, enabling artists to launch NFT projects without technical knowledge by customizing and deploying smart contracts with just a few clicks.

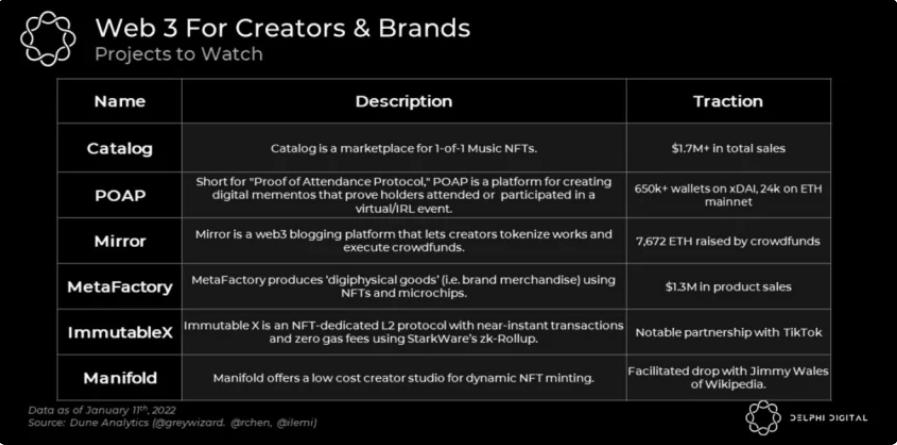

Creators and Brands Entering the Web 3 Space

Web 2 platforms like Patreon and Substack have changed the game for creators and brands, allowing them to own their distribution and monetization. However, with the emergence of NFTs and tokenized communities, this is being elevated to another level, as the tokenization of other intangible values (i.e., fans) will create a whole new category of investable assets for individuals. Artists, athletes, celebrities, and influencers are beginning to explore how NFTs and tokens can create stronger connections between them and their fans and followers.

Music NFTs provide a concept similar to copyright for music but without the legal red tape, representing a sub-industry that is expected to explode in the coming years. The 1-to-1 music NFT model of Catalog seems the most attractive, but models like Royal and Sound also have significant potential.

The "Homogenization" of the Crypto Market Will Change

Fundamentals will become an increasingly important performance driver, especially as cryptocurrencies attract more capital and investor attention. The performance of cryptocurrencies over the past few weeks shows how correlated assets can be, primarily driven by the recent spike in market volatility, which often strengthens the positive correlation between crypto assets, regardless of their fundamentals.

However, this is not a phenomenon unique to cryptocurrencies; traditional asset classes like stocks often see higher market correlations during periods of increased volatility. In these times of severe uncertainty, macro events still dictate much of the price action during these uncertain periods.

But just like mature financial markets, the performance of similar assets will not always remain highly synchronized. The cryptocurrency market will also mature further, and the long-criticized state of "homogenization" is expected to change, with the performance of segments like BTC, ETH, DeFi, NFTs, L1/L2 becoming more independent.

In the coming years, cryptocurrency investments will generally diverge more between "mainstream cryptocurrencies" and "Web 3 cryptocurrencies." "Mainstream" cryptocurrencies (like BTC) will continue to be influenced by key macro factors or gradually reveal characteristics of traditional financial market asset classes.

The impact on the broader cryptocurrency market will depend more on the type of asset or protocol and whether these events directly affect their value propositions. In other words, the success of these DApps and protocols will be determined more by adoption and usage activities.

This is not to say that macro factors will not affect the broader cryptocurrency market; specific industries and their related assets will benefit from strong fundamentals, and users who know how to spot trends early will be better positioned to manage their assets.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles