Explore the intrinsic value of SSV from the perspectives of cost, positioning, and target audience

SSV is expected to officially launch its mainnet this year.

SSV is expected to officially launch its mainnet this year.Original Title: "A Brief Analysis of the Intrinsic Value of SSV"

Original Author: Blockchain Binary Knife

The merger of the ETH execution layer (originally 1.0) and the consensus layer (originally 2.0) is expected to be completed in the second quarter of this year. After the merger, ETH's consensus mechanism will officially shift to PoS and enable network sharding. SSV is expected to become an important infrastructure serving ETH staking. There was a long article written by Teacher Lu introducing the SSV project, which you can check out here, so I won't elaborate further. This article will analyze the intrinsic value and value capture of the SSV project from my own perspective.

Cost of Running an ETH Validator

Currently, if we want to prepare to run an ETH validator, we need to bear the following costs:

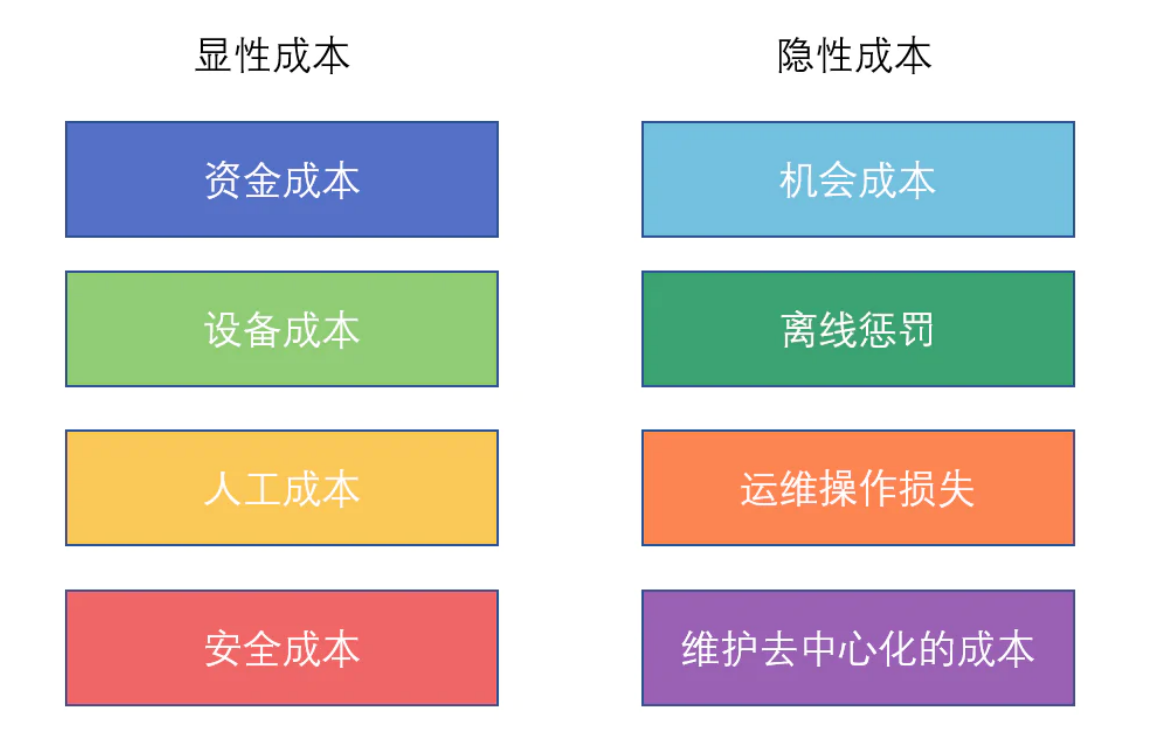

Cost Composition

Explicit Costs

Capital Cost: 32 multiples of ETH for staking

Equipment Cost: Cloud servers for running validator nodes

Labor Cost: Server operation and maintenance personnel

Security Cost: A series of costs to ensure security

Implicit Costs

Opportunity Cost: Opportunity cost caused by staking ETH

Offline Penalty: Penalties for node downtime or disconnection

Operational Losses: Penalties for cheating due to operational errors

Intangible Assets: Loss of network value caused by node centralization

Let's analyze the above costs one by one:

Capital Cost

The Ethereum consensus layer requires each validator to stake 32 ETH as collateral (non-divisible). An account can run multiple validators, so users need to prepare 32*N (N is the number of validators, an integer) ETH for staking. Currently, the cost of 32 ETH is approximately 90,000 USD, which is unaffordable for most retail investors.

Therefore, staking providers like Lido have started asset management intermediary businesses, where users provide their scattered ETH (less than 32) to Lido, which sends stETH staking certificates to users. Lido then combines the scattered ETH collected from various users into a 32 ETH asset pool, creating a validator for each pool, which Lido operates. Users can earn staking rewards, which is a way for many retail investors to participate in ETH staking indirectly.

Equipment Cost

Validators need to submit network blocks and vote on blocks, requiring them to remain online 24/7. Renting cloud servers is the most reasonable choice.

Labor Cost

It is necessary to hire operation and maintenance personnel to manage a large server cluster and respond to various unexpected situations.

Security Cost

Various security protections and network optimizations are needed for the server cluster to prevent external attacks. For example, CDN, firewalls, jump servers, sentinel nodes, system permissions, status monitoring, resource monitoring, server disaster recovery, etc.

Analysis of Implicit Costs:

Opportunity Cost

Staked ETH needs to be locked, and it takes 2048 epochs (about 9 days) of service to apply for redemption. After redemption, it takes about 27 hours to unlock. Therefore, during significant market fluctuations or when there is a need for funds, the lack of liquidity can result in a certain opportunity cost.

Lido's issuance of stETH addresses some liquidity issues, allowing staked users to exchange stETH back to ETH on Curve.

Offline Penalty

Validators need to vote on transactions in their respective slots. If a validator does not respond promptly, they will be penalized by losing part of their staked ETH.

Operational Losses

From the introduction, penalties due to operational errors mainly fall into two categories: double signing and surrounding voting. These actions will be regarded as malicious cheating and will incur significant penalties. For more details, click here.

Intangible Assets: The Consensus Value of Network Decentralization

Currently, Ethereum's TVL exceeds 120 billion USD, which is more than the total of the second to tenth places combined. On one hand, Ethereum has a first-mover advantage, possessing the most DeFi protocols and stablecoin assets, along with countless whales.

On the other hand, Ethereum is also recognized as one of the longest-running and most decentralized public chains. This consensus makes more stablecoins and financial protocols willing to deploy on Ethereum, and the wealth effect created by a large amount of capital attracts more users and funds, forming a positive cycle. This is also the brand premium brought by network decentralization.

Therefore, many projects spend a lot of costs (including marketing, grants, etc.) to incentivize users to stake and build nodes, aiming to keep the network relatively decentralized and avoid the concentration of power.

TVL of Mainstream Public Chains

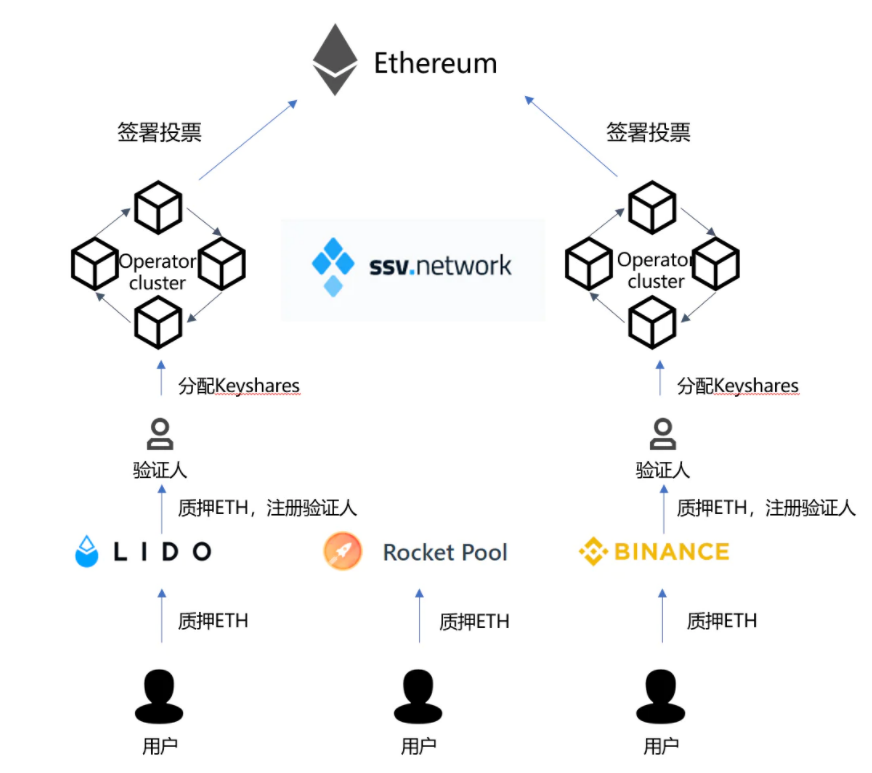

Differences Between SSV and Node Service Providers like Lido

Before discussing the value capture of SSV, many friends are unclear about the differences between SSV and Lido, which are both in the ETH staking space. Here, I summarize the differences: their positioning is different.

SSV itself is an infrastructure serving validators, but SSV does not engage in asset management, meaning SSV does not absorb users' ETH for aggregation.

Lido is a true staking service provider, where users provide ETH to Lido, which has the right to control user assets.

ETH Staking Ecosystem and SSV Positioning

Target Audience of SSV

At this point, we can see that SSV actually serves two groups of people:

Long-term holders who need to ensure the safety of their funds (not entrusting assets to third parties) but do not want to operate themselves.

A group of ETH staking service providers led by Lido, Rocketpool, and Binance, capturing the value of SSV.

From the previous discussion, we understand the costs required to run an ETH validator, and what SSV aims to do is outsource these costs from the original validators and staking service providers. All these costs will be borne by SSV's operators, making SSV a massive node operation service provider—an operator crowdsourcing network.

Professionals doing professional work benefits service providers like Lido in several ways:

Reduces operational pressure, eliminating the need to hire and build a node operation team, which can all be outsourced to SSV.

Reduces expenditure on equipment servers and their management costs.

Reduces security risks; under the original self-operation model, if hacked, it could lead to a large number of nodes going offline on their platform, causing user losses.

Staking service providers do not need to worry about network upgrades and operations; they only need to periodically pay SSV's operators, which is convenient and worry-free.

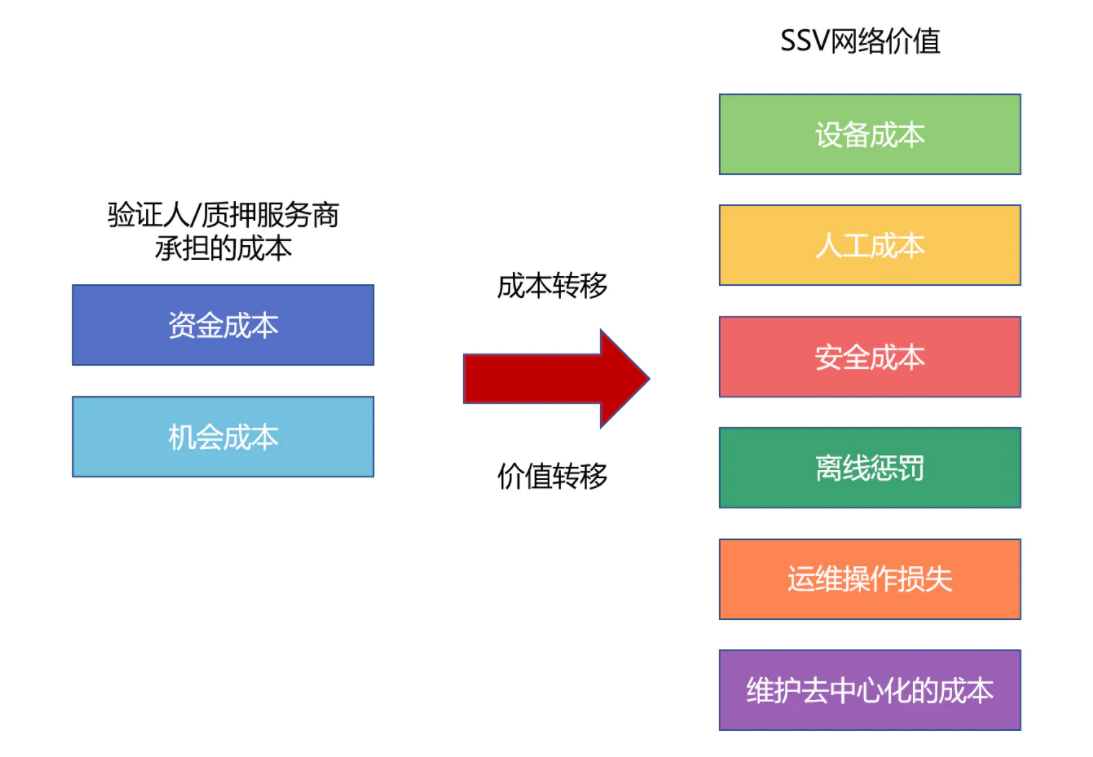

Value Capture of SSV

Thus, the true value capture of SSV comes from the cost savings it provides to staking service providers like Lido by taking on node operation work. Through the scale effect of the SSV Network, costs are distributed among various operators and ultimately paid to operators in the form of SSV tokens. In my view, the real value of SSV is the total of the various costs on the right side of the above image. As the network scales and the number of validators increases, SSV will capture a large amount of "cost value" and enjoy the market dividends of Ethereum.

Can This Technology Be Applied to Other PoS Chains?

First of all, it is technically feasible. Theoretically, as long as the consensus mechanism is PoS and the validator's operational keys and account private keys are independent, SSV can be integrated, such as in the Cosmos ecosystem.

However, there are significant differences between Ethereum and other PoS public chains in terms of mechanisms:

Ethereum pursues maximum decentralization, so its design philosophy is that all validators stake the same amount of ETH, and the rewards validators receive are unrelated to their staking amounts. Ordinary users cannot delegate ETH to validators, allowing more people to build nodes, making Ethereum nodes sufficiently decentralized.

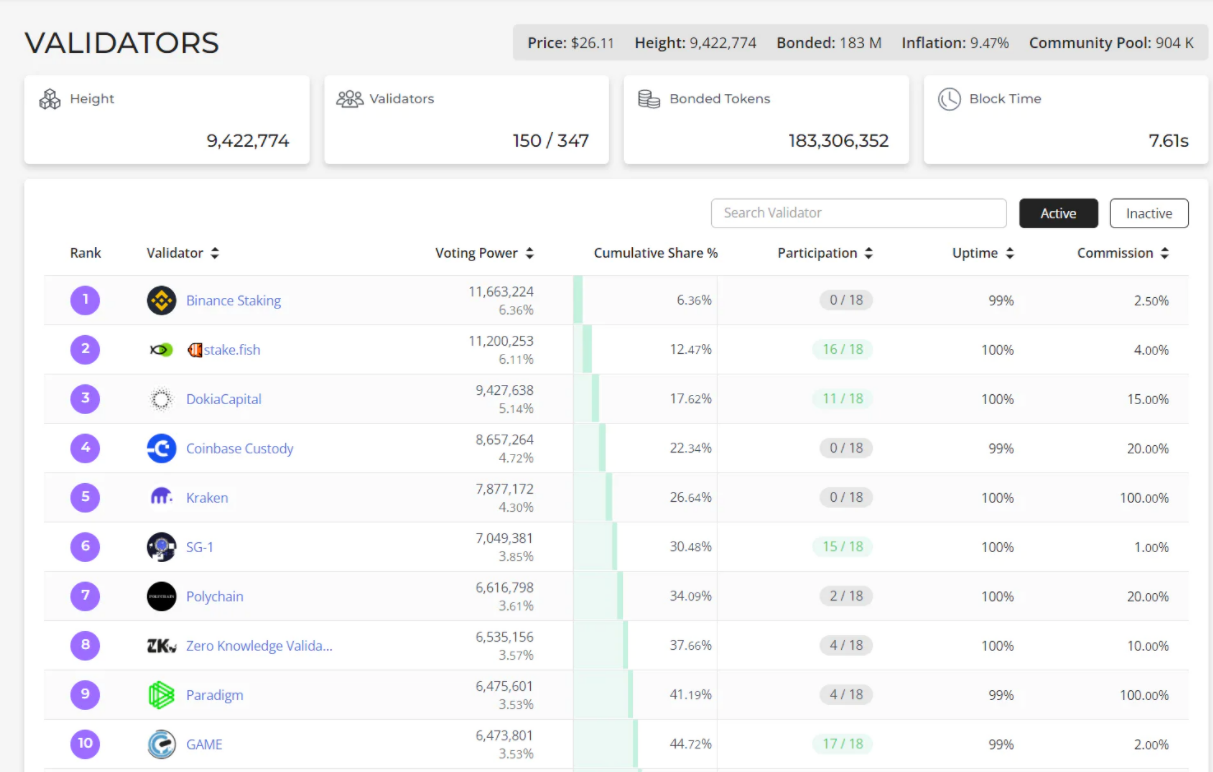

Other PoS public chains focus on performance (higher TPS), so their usual practice is to limit the number of active validators (for example, Cosmos initially has 101 active validators, increasing by 10% each year, ultimately not exceeding 300). Users need to delegate their tokens to active validators to earn staking rewards.

In this mechanism, a validator's income is directly related to the number of votes they can attract, so validators are motivated to attract a large amount of user staking, leading to the concentration of voting rights and chips. Therefore, for project parties, they can only reduce the degree of network centralization by dispersing voting rights, but the road to decentralization is still long.

The top 10 nodes in the Cosmos network hold nearly 50% of the voting power

Thus, SSV may not gain significant acceptance in these networks due to the limited number of active validators, making it difficult for SSV to achieve decentralization in these networks.

At the same time, many active validators are operated by professional node service providers, leading VCs, exchanges, and project parties. These nodes already have considerable brand endorsement effects and have formed professional node operation teams to varying degrees.

Additionally, the node configuration requirements of these PoS chains are much higher than those of Ethereum, meaning that if SSV is to be deployed in these networks, operators will also need to bear more costs. Whether these validators are willing to spend more to integrate SSV as a means of operational disaster recovery and to reduce the probability of being slashed still requires time to assess.

Conclusion

Currently, SSV is conducting a V1 incentivized testnet activity, which will last until April. The V2 testnet is also under development and is expected to be tested in April. SSV is expected to officially launch its mainnet this year.

In summary, with the significant process of Ethereum's merger this year, SSV is worth paying close attention to.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles