Opinion: Anchor struggles to sustain growth, how to improve token economics?

The interests of LUNA holders are not completely aligned with those of ANC holders.

The interests of LUNA holders are not completely aligned with those of ANC holders.Original Title: “Opinion: The Constant Injection of Capital Reserves Will Only Make Anchor Protocol ‘Too Big to Thrive’”

Written by: Luca Prosperi

Compiled by: Yangz

“My job is not to believe or not believe. It is to take action or not take action!” - Katsuhiro Otomo, “Akira,” Colonel Shikishima

We are living in a historical period marked by a severe lack of trust, where the system incites impulsive reactions through carefully designed stimuli. However, in every field of human activity, only a very few people's work is about taking action or not taking action. For all others, it should indeed be a matter of believing or not believing. A person's faith should not flutter in life like a flag in the wind.

I always remind myself of this whenever I think about what to do. And what is my job?

The next stop of token activism: Anchor Protocol. I want to thank @jofo_real for the valuable information that helped complete this issue. Open collaboration is our superpower.

This is not our first article about Anchor -- see here. Since the last time DR was obsessed with praising Anchor's 20% deposit rate, the protocol's TVL has risen from $4.3 billion to $11.6 billion (source: DefiLlama). A lot has happened since then: the volatility of the crypto market has surged, and mid-to-large tech companies that went public have been crushed by inflation data.

And the world is now on the brink of nuclear war. All of this provides good reasons to park liquidity in a 20% yield strategy, which masks volatility, pretending you don’t see the volatility, and it doesn’t exist. Meanwhile, Anchor's deposit yield has not responded to the world's volatile sentiment, lingering in the range of 19-20%.

Its pegged currency, UST, has also resisted cross-chain storms (Abracadabra), remaining quite faithfully pegged to the dollar at a 1:1 ratio for the benefit of all depositors. So why should we worry? Shouldn't we simply enjoy the beauty of trust and anchor our stable haven in a world full of uncertainties?

Skip the Review (Risk at Your Own Risk)

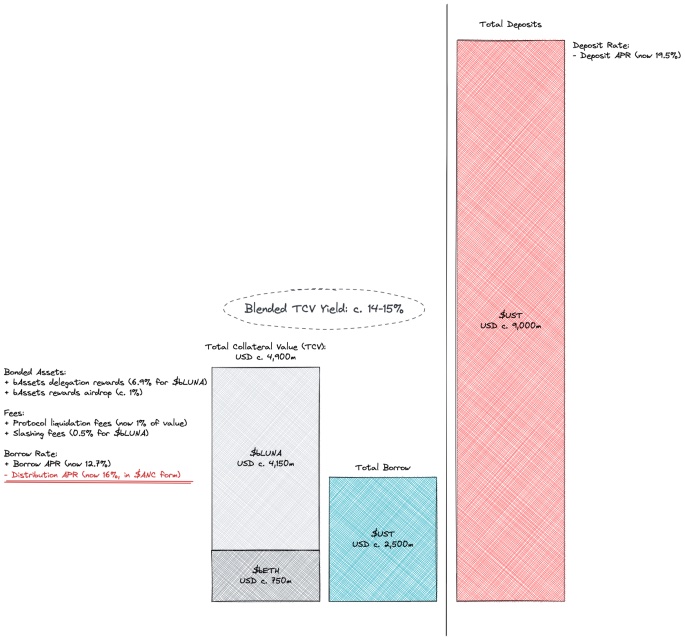

As a reminder, Anchor is Terra's lending protocol. This lending protocol is different from Maker because it is not the ultimate issuer of its own currency, and it is also different from Aave-Compound because it only lends one asset -- Terra's native stablecoin $UST. Like other protocols, it has chosen to whitelist only income-generating assets as available collateral: currently $LUNA and $stETH. The logic is simple:

- Anchor attracts depositors to deposit UST in exchange for a deposit interest rate → the protocol pays that rate from its reserves

- At the same time, Anchor attracts potential borrowers who will use income-generating assets as collateral (or better bonds deposited) → the protocol retains most of the generated income as part of its reserves

- Borrowers can borrow a certain amount of UST based on a parameterized loan-to-value ratio (or LTV -- for example, 50%) → the protocol retains the interest paid in reserves

- Anchor retains other auxiliary fees in reserves, such as a portion of airdrop rewards, liquidation fees, penalties, etc.

If we temporarily ignore the reflexivity occurring between Anchor and the broader ecosystem due to the involvement of certain crypto assets (like $UST and $LUNA) and rewards paid in $ANC, then Anchor is not much different from a commercial bank.

As a simplified bank, it should earn more from its assets than it spends on its liabilities. Banks typically charge a positive spread between the interest they demand from borrowers and the interest they pay to depositors; but is that the case for Anchor? Not at all.

This can be considered a “best-case” spread. If we think that some borrowed UST is deposited back into Anchor for some hedging strategy, then the negative spread is likely to be even larger.

Anchor is a negative spread bank. From the perspective of capital costs, Anchor is actually more like a private equity fund than a bank: banks make money by independently managing assets and liabilities -- although this concept has been stretched in a negative interest rate world.

Investment funds attract capital from limited partners (promising high returns) and need to actively manage assets to exceed the promised yield. The equation above implies that, from another perspective, for every unit of collateral provided, a maximum of 0.75 units of deposits can be attracted to break even.

Assuming a fixed LTV of 50%, this means a minimum deposit utilization rate of 65-70% -- Anchor has previously stated this number is 60%. When the asset-side equation grows rapidly, and there are many borrowers wanting to leverage their positions.

This number is reasonable. In 2021, LUNA was one of the best-performing assets, with an LTM return of about 750%. Until early December, the booming market was enough to ensure that Anchor's interest had positive cash flow.

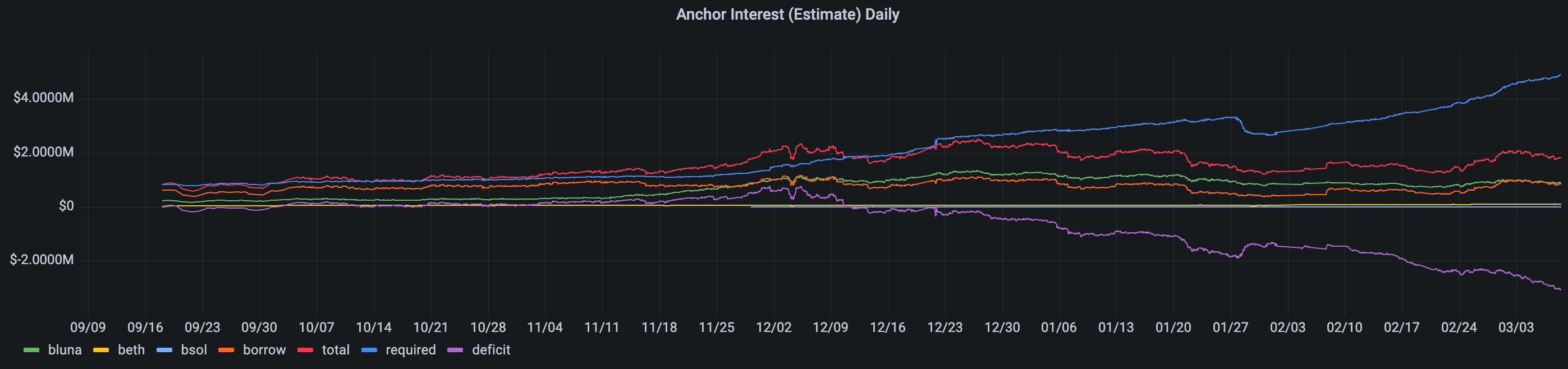

But in a negative spread situation, you are racing against time, and the protocol will be affected by its pro-cyclical nature; it’s only a matter of time. As volatility increases across all markets, the demand for leverage will stagnate, while on the other hand, this demand will shift to a demand for stability -- in the Terra ecosystem, Anchor's borrowing and deposits will decrease. Fast forward to today, our situation looks like this:

In Adam Smith's theory, market forces will reduce the motivation for deposits (by lowering deposit rates) and potentially improve borrowing motivation by lowering borrowing rates again. Anchor is not unfamiliar with the concept of algorithmic rates -- take a look at the documentation, where borrowing rates are based on a parameterized model of utilization.

Interestingly, the same situation has not occurred with deposits, where rates remain fixed at around 20%. Providing a stable and predictable rate is Anchor's ultimate goal. This indicates that there are two different issues, and we will try to address them separately: (1) How can Anchor maintain a sustained negative yield, and (2) Why is Anchor so resistant to adopting market forces?

How Does Anchor Maintain a Sustained Negative Yield?

Things get murky. In previous comments, we deliberately ignored the borrowing incentives deployed by Anchor in the form of $ANC minting. $ANC, the governance token of the protocol, is allocated to borrowers to incentivize them to provide income-generating assets to the protocol and borrow $UST.

At the current level, the yield for borrowers (in $ANC) exceeds the negative annual interest rate of the debt (12.7%) (16%). Borrowing, in other words, is currently happening as a mining strategy and a leveraged bet on the price of $ANC. Minting incentivizes the use of the protocol -- indirectly benefiting $ANC, but at the cost of value dilution and selling pressure -- harming current $ANC holders.

Like most (if not all) liquidity mining incentive programs, it is unsustainable. If you opened a savings account at a bank, you might get an iPhone now, but definitely not a continuous flow of the bank's own stock.

Aside from being unsustainable and harmful to current $ANC holders, the $9 billion in deposits compared to $2.5 billion in loans does not add up. The documentation states that Anchor's deposit rate is primarily adjusted by calibrating the ratio of $ANC released to borrowers. Given the current flow dynamics, it is clear that either the feedback mechanism is ineffective, or the target deposit rate is being maintained too high.

When $ANC mining is insufficient to parameterize the flow, the protocol relies on its reserves to directly subsidize. This is not necessarily a bad idea -- the function of reserves is to smooth out cyclical fluctuations around the protocol's long-term growth trajectory, but it becomes problematic when the protocol's reliance on reserves is structural. By early February, it became very clear how unsustainable the situation was.

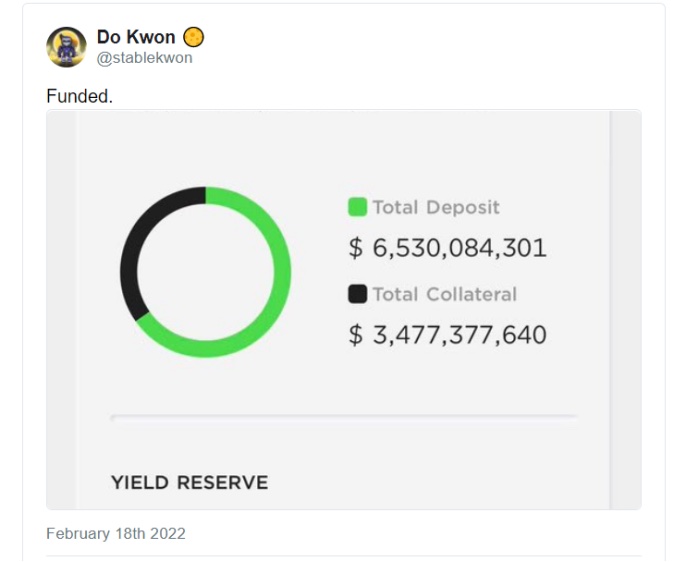

Interestingly, in a post on the @nrmo forum, someone proposed a long-term solution to the imbalance by modifying the borrowing model, which I find quite alarming, while the deposit rate was proposed to be maintained at 19-20%. Meanwhile, to keep the patient alive while continuing to bleed, a $450 million capital restructuring through the newly established Luna Foundation Guard (LFG) was suggested.

LFG was established to increase capital by $1 billion through a private token sale led by Jump and 3AC, with many others involved. The UST forex reserves created through the capital increase, and in the name of digital gold -- BTC, aim to serve as a stabilizer for UST and a last-resort reserve. Not many native stablecoins on chains have a $1 billion backing to protect their peg. No matter how good the algorithm is, it is not enough to earn our unconditional trust.

These are not small numbers, and I am impressed that the orthodox value of the 20% anchor rate exceeds $500 million. I am not the only one who dislikes this proposal. @Pedro_explore, a prolific Anchor commentator, strongly opposes using funds originally allocated to improve the sovereignty, security, and sustainability of the Terra ecosystem.

If Anchor is considered too big to fail, then making it bigger without addressing its issues will not make things better. Simply put, Anchor can indeed continue to be Terra's most powerful marketing machine, but no one can afford to sustain such a flashy marketing machine for too long. However, history does not care about the will of ordinary people; on February 17, Do Kwon announced an increase of $450 million in reserves.

But the capital increase is just a capital increase and does not change Anchor's trajectory. Since the day of the capital restructuring, the reserves have decreased from about $510 million to about $450 million in less than a month. And the deposit yield has not changed.

Why is Anchor So Resistant to Adopting Market Forces?

The importance of Anchor to the broader Terra ecosystem cannot be underestimated. Currently, there are about $14 billion in circulation, of which 9 billion is stored in Anchor. On this number, we should add about $150 million (50% of the $300 million pool) provided to the Astroport $ANC liquidity pool; I believe there are other Anchor-related matters I have not covered.

There is no doubt that Anchor constitutes the cornerstone of Terra today. But it may not always be this way in the future -- alongside Astroport, Prism, Mars, Mirror, etc., but that future has not yet arrived.

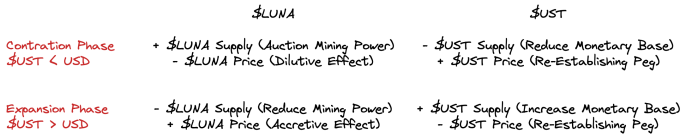

In Terra's comprehensive transparent monetary system, LUNA and UST are directly connected.

Terra is a financial center of the metaverse, interacting with other parts of the universe through capital flow in and out.

- Contraction phase → When capital inflows slow down, UST will be subject to decoupling pressure, while the system attempts to issue more Luna (trying to incentivize more external actors to interact with Terra) and use the proceeds to buy and burn UST. From a macroeconomic perspective, Terra hopes to increase external participation in the medium term while using these proceeds to stabilize UST in the short term -- but at the expense of current $LUNA holders.

- Expansion phase → When capital inflows accelerate, UST may become more expensive in dollar terms, and the system attempts to offset this effect by minting more coins and using these coins to buy and burn $LUNA. From a macroeconomic perspective, Terra immediately inflates the currency (representing the purchasing power of an economy) and uses the additional coins to drive up the price of $LUNA -- which benefits everyone.

In another way, Terra continuously shifts volatility between $UST (its system's liabilities) and $LUNA (its system's equity), which serve as reservoirs for each other. LUNA cannot withstand the aggressive outflow of UST caused by the decline in Anchor's deposit yield, as it would lose its ultimate stabilizer of price. The Terra ecosystem needs Anchor.

So What?

However, we need to take a step further and clarify that the interests of LUNA holders do not completely align with those of $ANC holders. Of course, unless we assume that a kind-hearted person injects $500 million into Anchor's reserves every six months (and is still increasing), thereby subsidizing the release of $ANC to infinity.

The result of this conflict is three unique proposals to improve Anchor's tokenomics. (A) veANC from Retrograde and ParaFi, (B) dynamic Anchor yield from bitn8, (C) tokenomics governance from Polychain and Arca.

(A) → veANC from Retrograde and ParaFi

On February 17, Retrograde and ParaFi published a proposal on the forum to expand the role of $ANC in Anchor. According to their first post on Medium, Retrograde intends to improve governance practices within the Terra ecosystem by “establishing a governance master key for Terra.”

How this will take shape is unclear, but looking at their proposal, we can speculate that Retrograde wants to become some sort of Convex-esque voting aggregation protocol -- for this reason, we cannot consider the proposal to be entirely conflict-free. The approach is not new (for DeFi and ParaFi) and is built around the Vote-Escrowed (or ve) token model. More specifically:

- $ANC can be locked in a voting-escrow contract for up to 4 years in a non-transferable form -- i.e., $veANC, which replaces staking and gives more weight to those who stake tokens for a longer time.

- Borrowers binding assets like $bLUNA or $bETH will receive an increased release of $ANC based on the amount of $veANC they hold -- up to 1.5 times, along with a portion of the protocol's revenue.

- $veANC holders will be able to vote on general governance issues as well as on the approved collateral types for future $ANC releases (standard voting).

This is Curve Wars 101 -- for a more detailed description of the Curve Wars, see here.

So, what problem does this solve? It is clear that the intent of this initiative is to create a vertical ecosystem similar to Curve's Curve→Convex→[REDACTED], which would positively impact the demand and price of $ANC. By benefiting the price of $ANC, the incentives for borrowing would increase, and the mismatch between borrowing and deposits would decrease.

This would have a positive effect on the entire protocol. However, no value is created out of thin air, and the interest generated in the short term must be compensated at some point -- the pyramid-like Curve Wars model merely increases the operational leverage of the protocol.

In a pyramid, the base is important: if this system may be unsustainable for a profitable protocol like Curve, then I find it hard to see how it would be sustainable for a non-profitable protocol like Anchor. We are borrowing time, and at a very expensive rate. I cannot say I like it.

In my view, this proposal has a negative impact on governance as well. The model exacerbates centralization by benefiting those who already hold a significant proportion of governance power in the system. If we believe that decentralization is a universal interest that needs to be defended -- at least I do -- then we cannot help but dislike it.

Additionally, there is a subtlety connected to the conflict of interest argument we mentioned above: it can be reasonably assumed that the core team of Terra controls a large portion of governance power -- my reverse estimate is about 30%, so I do not understand how these same actors would lean towards the interests of Anchor rather than Terra.

To become, some have raised another relevant point, including @Jae99 and @Pedro_explore. Should we really make the true source of income for the protocol -- the borrowers -- more difficult?

Why not uplift those depositors instead of staking veANC? Moreover, would the introduction of $veANC ignite a war with a positive impact on the price of $ANC (in the short term)? Among borrowers, Anchor has no natural competitors in the $LUNA market, and outside the ecosystem, its position is weak; a war for Anchor is hard to ignite.

(B) → Dynamic Anchor Yield from Bitn8

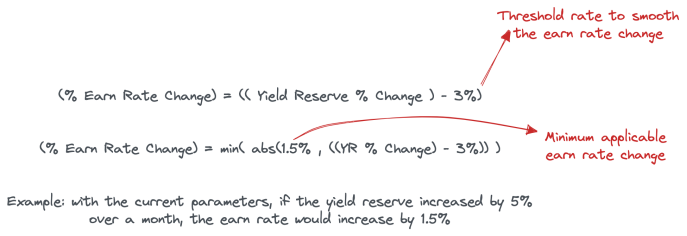

On March 1, @bitn8 published an alternative proposal to create a semi-dynamic yield for depositors, linked to changes in Anchor's reserves. If reserves decrease, then the yield should decrease, and vice versa. @bitn8 is defining a discrete dynamic system that will drive changes in interest rates, implemented monthly, as shown in the diagram below.

I do not intend to provide immature opinions on the discrete dynamic model proposed by @bitn8, as I believe there are more qualified individuals to do so, but I can say that I welcome a mechanism that helps reflect the reality in deposit rates. Interestingly, the purpose of this proposal is not to welcome market forces into the protocol but to allow the protocol to continue to develop without continuously relying on external resources.

(C) → Tokenomics Governance from Polychain and Arca

The third proposal comes from Polychain (@joshrosenthal) and Arca - @MattHepler. This is not the first time DR has encountered Arca as part of its research activities -- see Sushiswap. Their proposal was initially published on February 25 and underwent some revisions, being released in its final form just hours before this article was published.

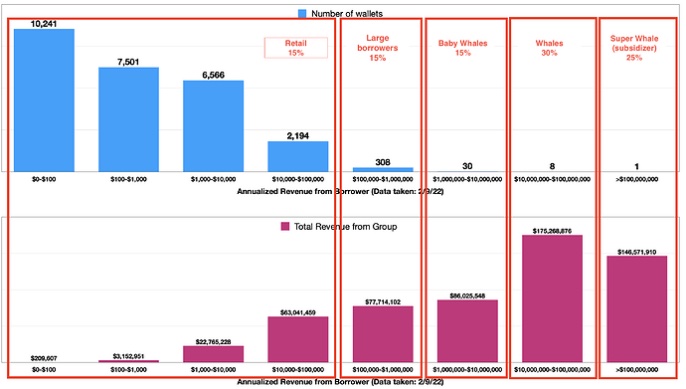

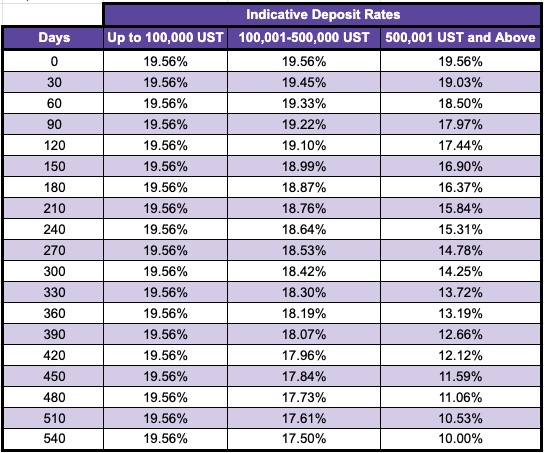

However, its core principle has not changed: supporters believe that the deposit rate is unsustainable, and they find it inappropriate for very large institutional participants to benefit from value transfer. In an era of mathematical complexity within DeFi, their proposal is very simple: below 100,000 UST, you can continue to benefit from a yield of about 20%.

Depositors exceeding the threshold will see their yield gradually decrease to 17.5% (for deposits between 100,000 and 500,000) or 10.0% (for deposits above 500,000) over 540 days -- the new rates will be finalized every 30 days.

Based on the table shared above regarding deposit concentration, the new mechanism can effectively target the large whales that account for 85% of the deposit volume. If Terra intends to become a distributed and decentralized financial services center, accessible to everyone, then do they really need these large depositors?

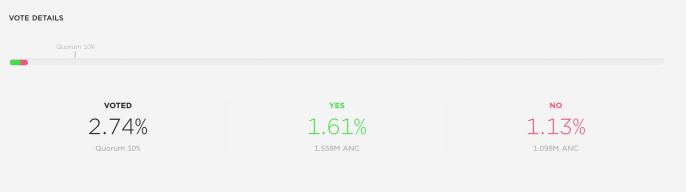

And how many of these large whales are also token investors in Anchor and the entire Terra ecosystem? Like in DeFi, conflicts of interest may be everywhere. The proposal is now live on governance.

We are still far from reaching a quorum or majority, but Arca is optimistic. In their words:

“Current attention and activity on Anchor governance are at an all-time high, helping to drive a 200% price increase. Through our proposal, we believe $ANC will gain significant, much-needed balance sheet sustainability, ensuring the Anchor protocol and the Terra ecosystem remain vibrant and create significant value. We believe the broad base of ANC holders will agree.”

As always, I maintain a considerable degree of skepticism, but the proposal lacks mathematical complexity, which may be a positive rather than a negative, as it paves a very clear path for the future of Anchor's interest rates. It is not surprising that some TradFi individuals behind the supporters believe that bleeding should be stopped before any fancy parameterized mathematical innovations.

Interestingly, in a sense, their proposal also marks the introduction of a forward-looking guiding concept within Anchor's ecosystem. In a DeFi environment dominated by short-term mathematical optimization for arbitrageurs, institutional investors have missed the clarity of sustainable long-term interest rates.

Visibility of the term structure, combined with trust in the makers, whether committees or AMMs, is crucial for extending DeFi use cases beyond trading, margin trading, and mining. Many projects are exploring this issue -- at DR, we are planning to explore this issue with several versions.

The Polychain-Arca proposal is a step in that direction, although it is not perfect, as it does not consider the dynamics of the market or the treasury when setting long-term rates, but it will be a healthy advancement for the protocol.

We are back to the starting point: conflicts of interest. Active investors, token holders, traders, depositors, farmers, enthusiasts, Anchor builders, Terra developers. It seems nothing has changed, but now everything has changed. The only thing we need to do is pay attention.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles