Exploring the Definition of NFT Prices

NFTBank is an algorithmic asset valuation product that uses machine learning to predict NFT prices based on the past pricing of similar assets.

NFTBank is an algorithmic asset valuation product that uses machine learning to predict NFT prices based on the past pricing of similar assets.Article Author: Gringotts DAO

Article Translation: Block unicorn

Original Title: "Exploring NFT Price Distribution Across Collections"

Categories of NFTs such as virtual land, PFPs (NFT avatars), and gaming assets are common frameworks for evaluating projects and collectibles. However, one less discussed and sometimes counterintuitive attribute of these assets is their price "tiers" within collections, and how assets of the same price tier perform across collections and NFT categories.

The mission of Gringotts DAO is to be a one-stop shop for NFT holders to obtain liquidity. With the rapid emergence of new NFT financialization protocols, we set out to evaluate the effectiveness of different approaches in the context of the types of NFTs users seek liquidity for. We did not focus solely on asset categories, but rather examined the common attribute shared by all these assets—their prices.

More specifically, we aimed to answer three questions:

How is the price distribution of NFTs across the entire market?

Are there observable patterns in price distribution, and if so, how prevalent are they?

From these distributions, how can we define price "tiers" that may make a given NFT more suitable for certain liquidity methods compared to others?

One of the main findings is that projects within collections and NFT categories may behave more similarly than projects within the same collection. Therefore, price distribution analysis can provide users and developers with a more comprehensive understanding of where to best find liquidity and the potential market for financialization methods.

Methodology

NFTBank is an algorithmic asset valuation product that uses machine learning to predict NFT prices based on past pricing of similar assets. We extracted over three months of data from NFTBank. The first dataset was from December 15, 2021 (279 collections, approximately 2.4 million NFTs, approximately 3.7 million ETH market cap), followed by January 13, 2022 (540 collections, approximately 14.2 million NFTs, approximately 8.9 million ETH market cap), and most recently on February 27, 2022 (538 collections, approximately 14.8 million NFTs, approximately 6.5 million ETH market cap).

This article delves into four observations we found:

1. Price distributions are generally very concentrated both between and within collections.

2. There are five main "shapes" of price distributions that appear to be unrelated to NFT "categories" (PFPs, gaming, virtual land, etc.).

3. The shapes of price distributions generally remain stable. For 75% of collections, the price distribution remains unchanged across different time points. For those that do change, it tends to evolve towards a "related" shape.

4. For collections with exponential decay and log-normal distributions (60% of collections), we can define and examine the behavior of bottom, middle, and top-tier assets.

Concentrated Price Distribution

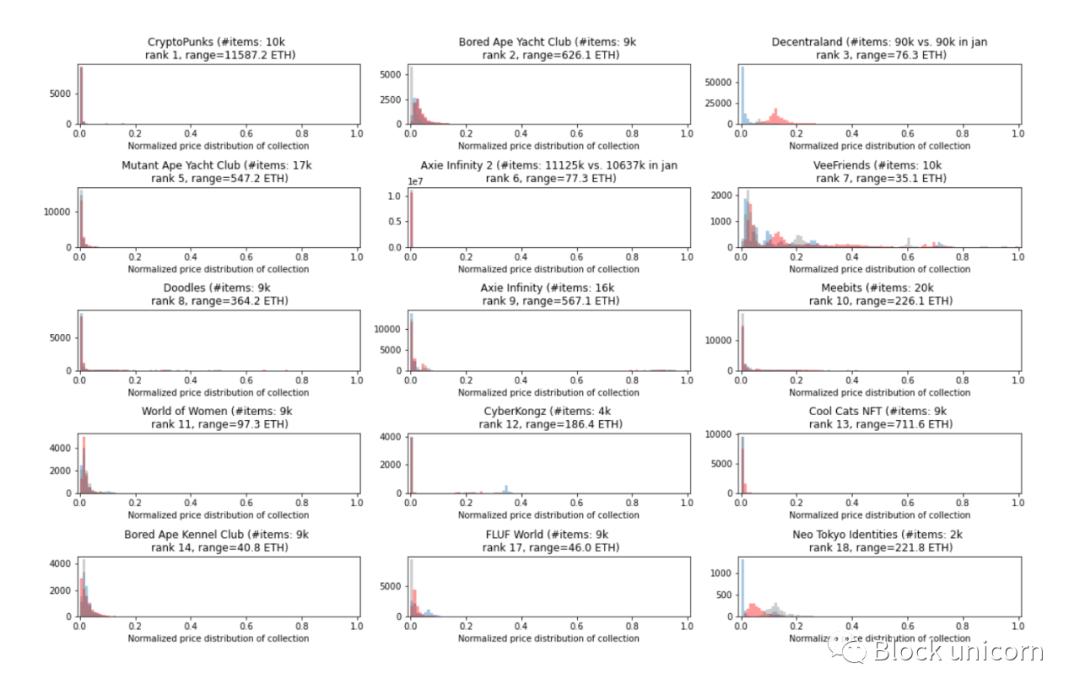

Across various series, the market is concentrated in the top 10 series, which account for over 60% of the market cap, with a (normalized) Gini coefficient of approximately 0.9.

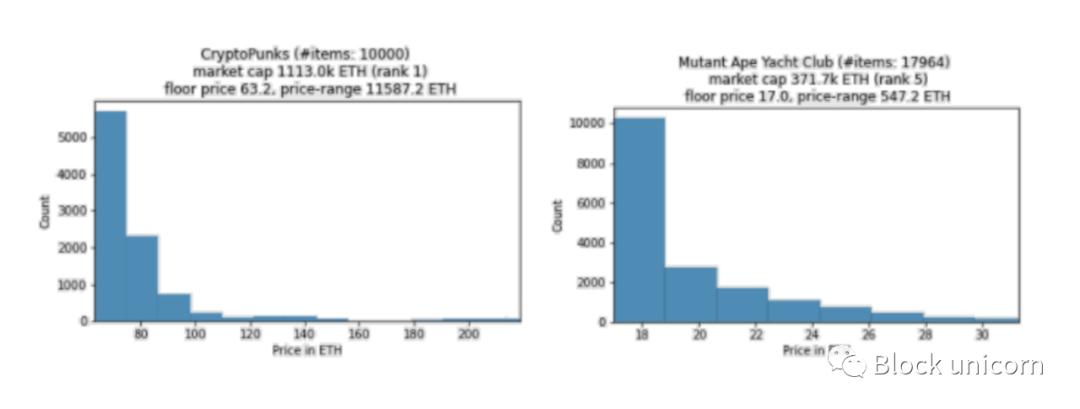

In collectibles, most price distributions follow a pattern where the majority of items are priced close to the floor price. The remaining few items make up a significant portion of the price range, thus contributing significantly to the market cap of the collection.

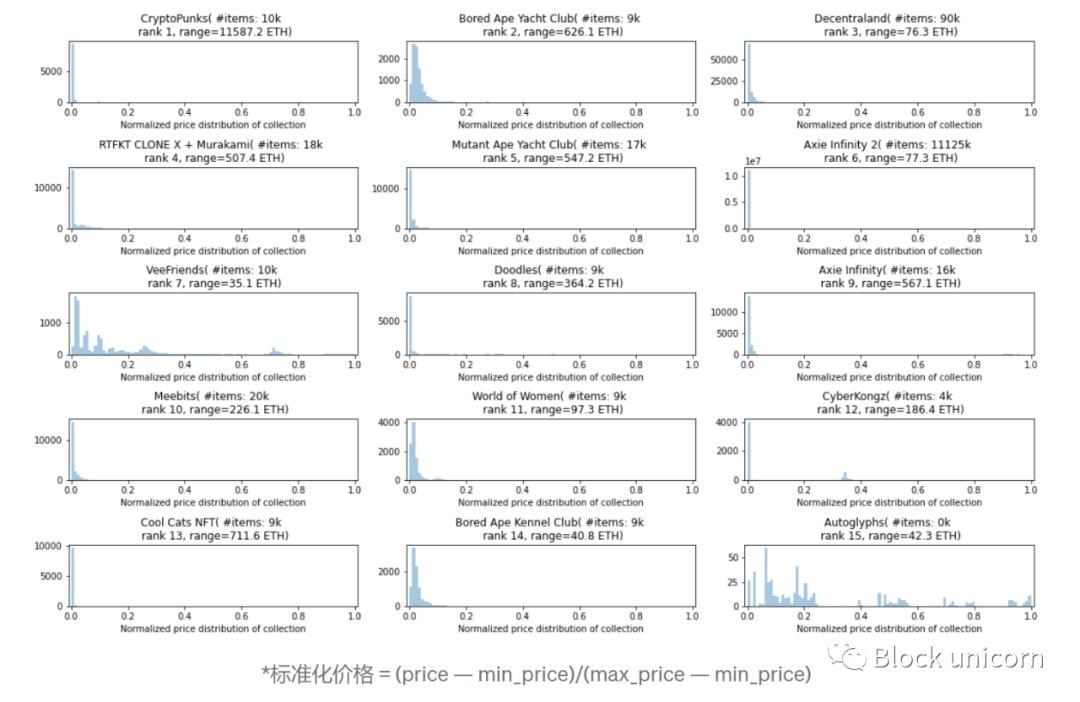

Example of a normalized price distribution chart:

In these charts, the x-axis is divided into 100 equal parts, so for example, the first chart (CryptoPunks) indicates that almost all punks are priced within the top 2% of the full price range.

This is promising for NFT financialization products best suited for on-chain projects, such as liquidity pools like NFTX, which can act as "on-chain AMMs," providing instant liquidity to NFT owners who can trade on-chain assets with the pool.

Collections with a large number of on-chain items and reliable price feeds (those frequently traded across many different unique addresses) can also serve as collateral for P2Pool lending products. This is because floor assets can often be treated as "identical," thus eliminating the need for manual valuation. Once automated means of inserting price feeds and assessing risk are in place, loan terms can be automated.

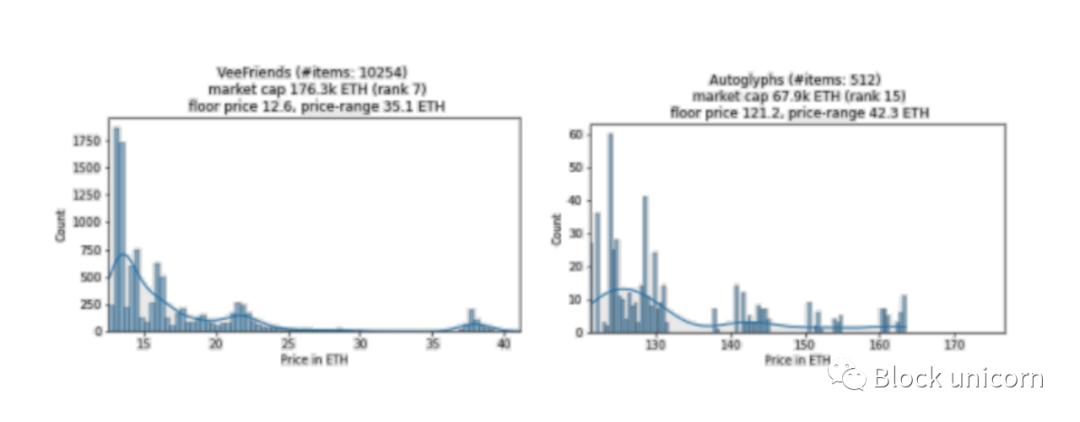

However, in the above example, note that certain collections (e.g., VeeFriends and Decentraland) do not fit this "pattern equals floor price" model. In fact, the price distribution patterns belong to one of five different shapes, leading us to the next observation.

Price Distributions Have Five Main Shapes

Across various series, the observed shapes of price distributions are:

1) Exponential decay. These are collections where most items are priced at the floor, with a long tail of high-priced items. About 40% of the collections we sampled exhibited this profile. Examples include Cryptopunks, RTFKT Clone X + Murakami, and Mutant Ape Yacht Club.

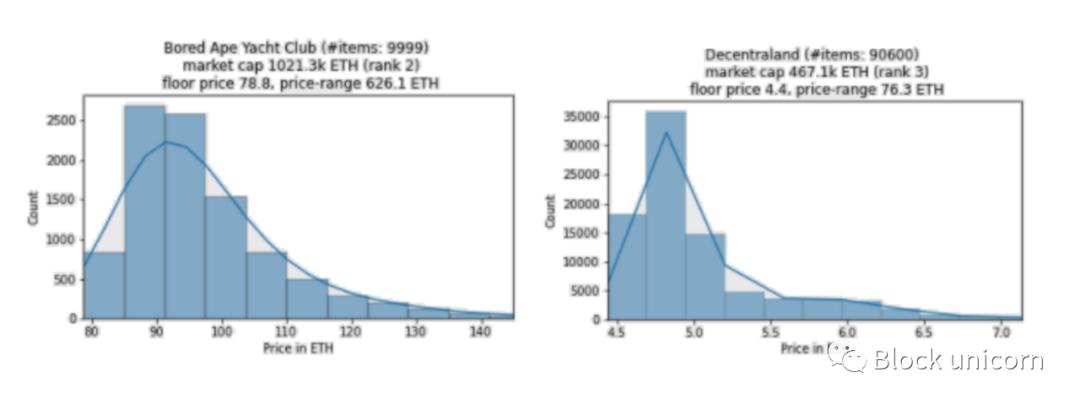

2) Log-normal distribution, which has a shape similar to exponential decay but is slightly elevated above the floor price. About 20% of the collections we sampled exhibited this profile. Examples include Bored Ape Yacht Club, Sandbox LAND, and Decentraland.

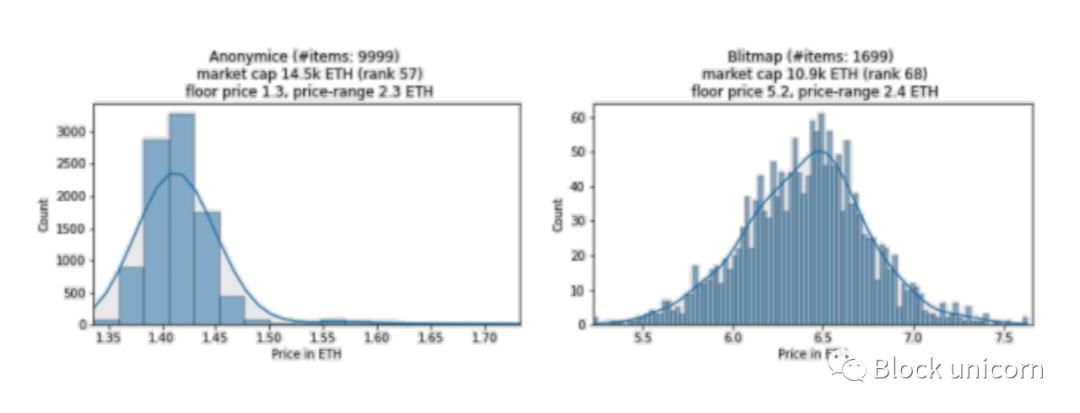

3) Symmetrical (or near-normal) distribution refers to assets being highly concentrated around the average price, tapering off gradually on both sides. About 5% of the collections we sampled exhibited this profile. Examples include Anonymice, Blitmap, and Rollbots.

4) Multimodal distribution shows multiple bumps and peaks across a broader range. About 20% of the collections we sampled exhibited this profile. Examples include VeeFriends, Autoglyphs, and FLUF World.

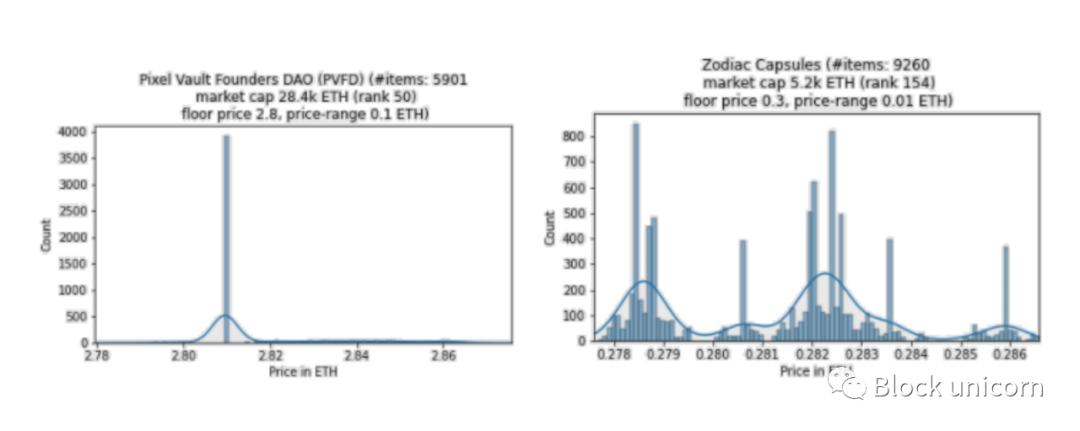

5) Point distribution patterns have one of the above shapes, but the price distribution is

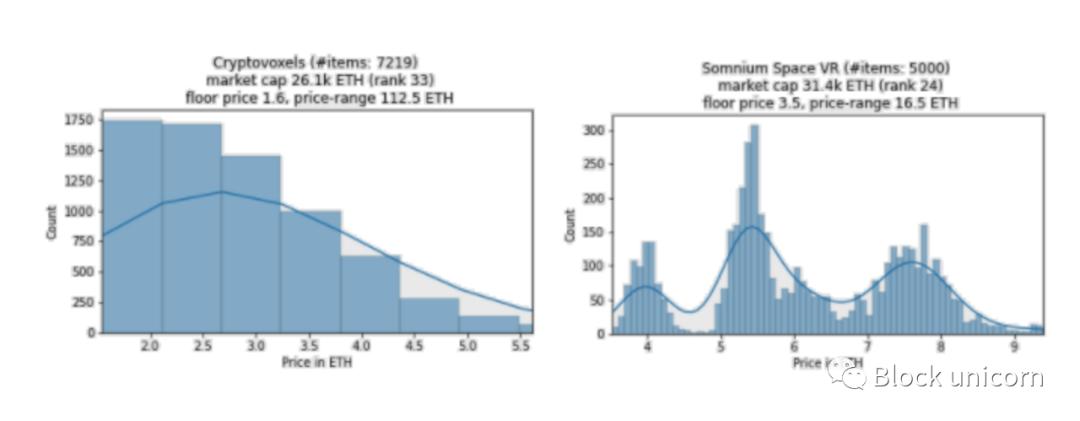

Interestingly, NFT categories (PFPs, virtual land, gaming assets, etc.) are unrelated to the shapes of price distributions. For example, virtual land NFTs in Cryptovoxels, Decentraland, and Somnium Space have different distributions (exponential distribution, log-normal distribution (symmetrical in Jan/Dec data), and multimodal distribution, respectively).

Price distributions are likely a function of the inherent characteristics of the collection itself, rather than the NFT category it belongs to. For land, this could include location, plot size, foot traffic (revenue potential), and land that has already been built on and thus sold at a premium.

Next, we examined whether these price distributions change over time.

Price Distributions (Generally) Remain Stable

Due to the limited data here (three data points), only time will tell if the analysis here will hold true in the future. Looking again at the normalized prices, we can see that the price distributions in December (gray) and January (red) generally (but not always) align with the price distribution in February (blue) or at least have similar shapes.

Among the 537 collections included in both January and February data, 166 price distribution shapes changed (30%). From January to December, we also saw a similar proportion of change (25%). This may sound like a lot, but keep in mind that the classification of distribution shapes above is somewhat fuzzy, as we are not too strict about cutoff dates.

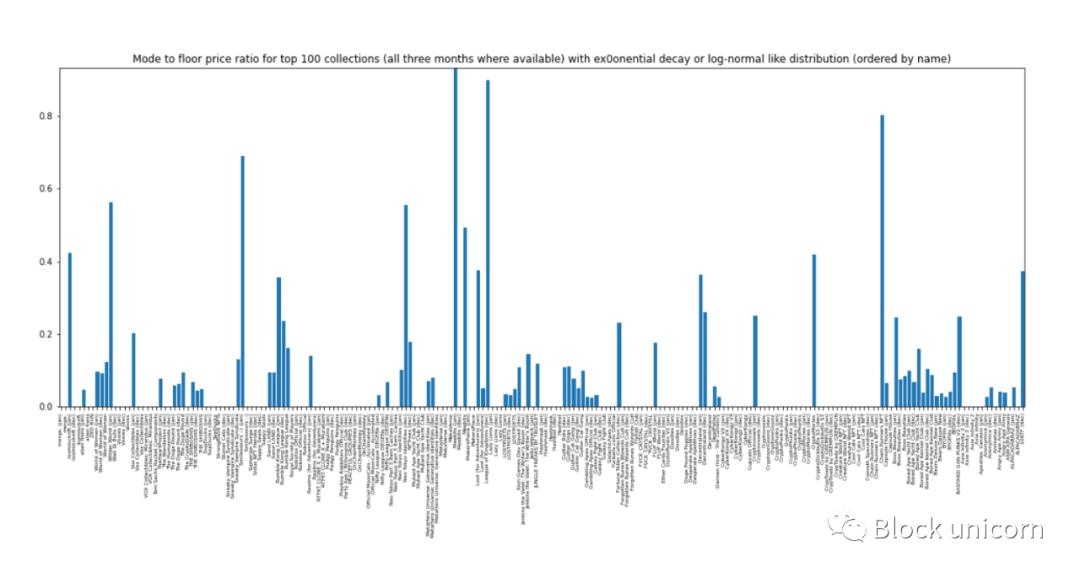

For example, one can differentiate between exponential decay and log-normal: "If pattern > floor price => log-normal." Looking at the ratio of patterns to floor prices below, we chose a more lenient definition and allowed patterns to even be 10%-20% above the floor price, as we looked at fitted distributions to classify their shapes.

On this basis, we consider exponential decay distributions and log-normal distributions to be "related."

For cases where changes in price distribution were observed:

~42% changed to point distribution or changed from point distribution. Point distributions are one of the other four forms, just with a very narrow price range.

~26% changed from exponential decay or log-normal to multimodal. The definition of this class is also somewhat lenient, as our releases typically only have one mode. We define this shape to separate distributions like VeeFriends and its several bumps (modes) from other shapes.

~22% changed from exponential decay to log-normal distribution/from log-normal distribution (this number would be much higher if we took a strict approach).

~10% of the remaining changes were all symmetrical distributions, with log-normal distributions making up the majority (6%). This is also due to the fairly loose linear definition between log-normal and symmetrical distributions (i.e., these two shapes are also "related").

Defining Price Tiers

Based on the observations above, we look for collections with exponential decay and log-normal shapes to define price tiers, as the floor price can serve as a reasonable anchor here. Of course, since the "absolute" lower limit may simply be the lowest-priced item, we want to find an appropriate multiplier to classify more items as floor items.

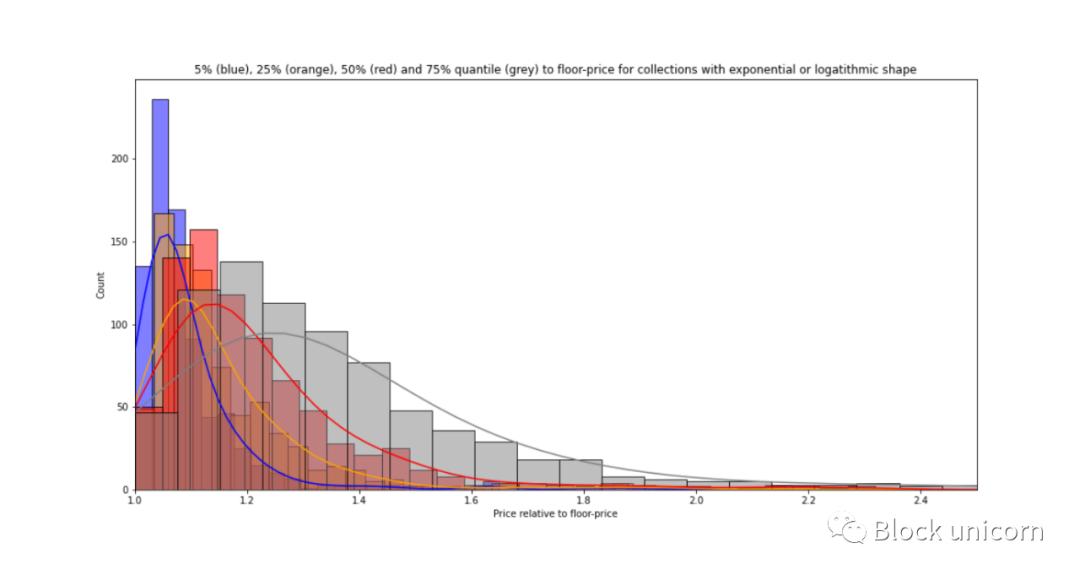

Defining the lower limit: We examined different lower limit percentiles and their ratios to the floor price.

Among these 800 collections, about 90% of the medians are below 1.4*floor price. Choosing a threshold here depends more on the use case we are considering: if we include a larger share of collection items further to the right, we will run the cost of expanding its price range, making this collection less homogeneous.

To make the threshold applicable to about 90% of collections, the thresholds are:

1.3 gives a 25th percentile (thus covering 25% of items).

1.4 gives approximately the 50th percentile/median.

1.75 indicates ~75% percentile.

Less than 30% of collections may be too few, while the price range of [floor price, floor price1.75] may be too wide. Therefore, we choose the multiplier of 1.4 as the lower limit. In other words, "floor" items refer to those priced within [floor price, floor price1.4]. For two-thirds of the collections, this includes 75% of the items.

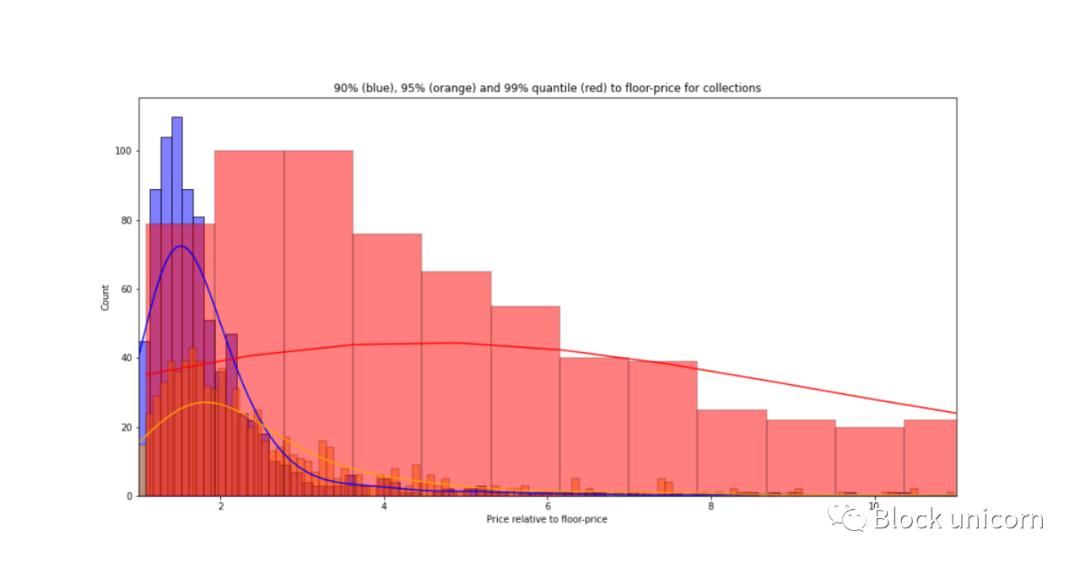

Defining top-tier items: We can follow a similar route using the top-tier percentiles:

A threshold of 2.5 covers 90% of the collections—85% of these 800 collections. It also includes 95% of the collections within two-thirds of the collections, and even 99% of the collections within ~20% of the collections. In other words, a threshold of 2.5 will place the top 10% of assets in the "top-tier" bucket of 90% of the collection.

Similarly, we can apply more exclusivity to this collection, such as increasing this threshold to 4.

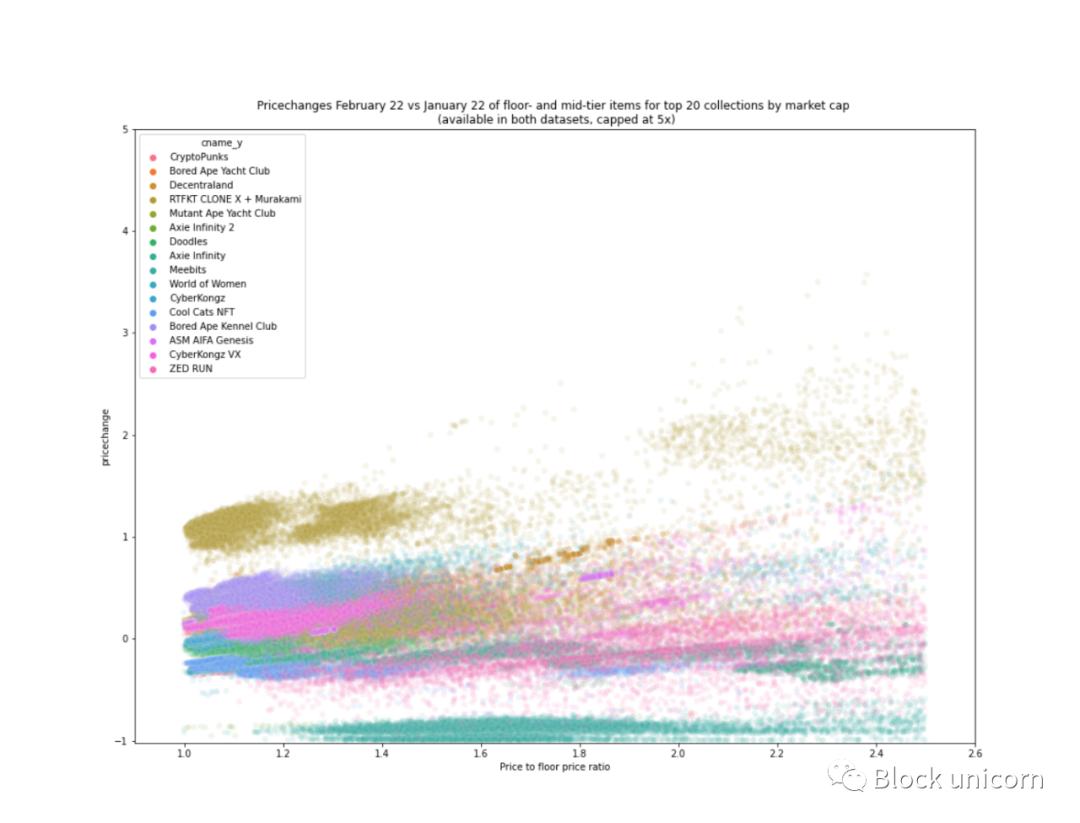

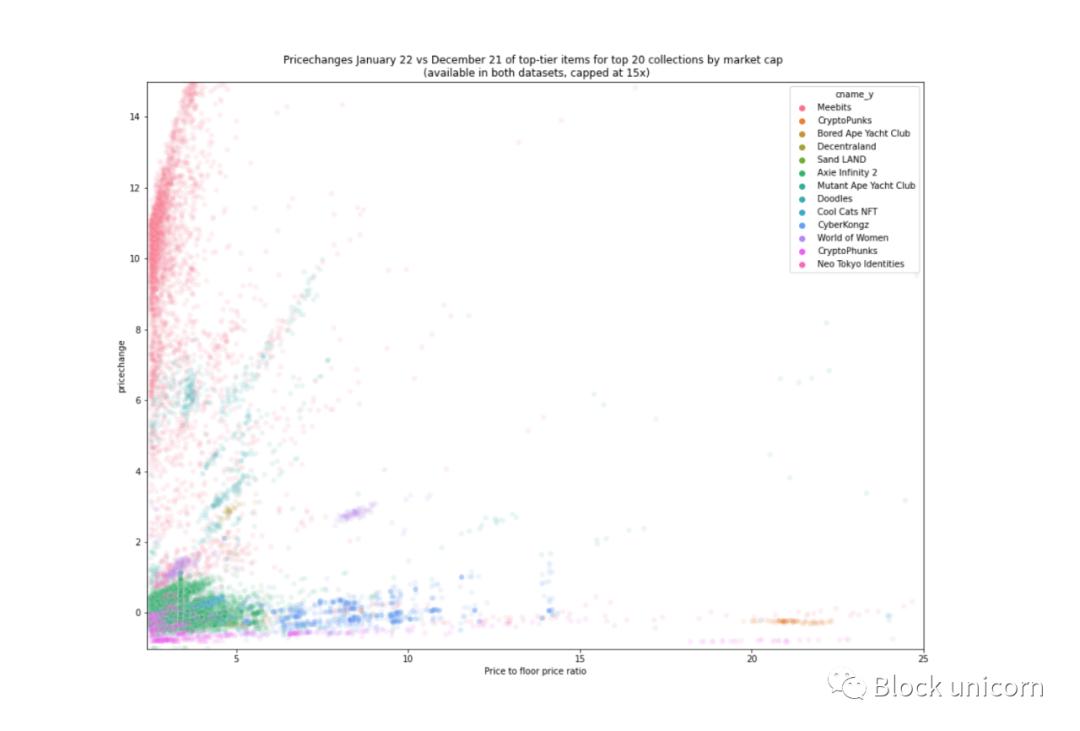

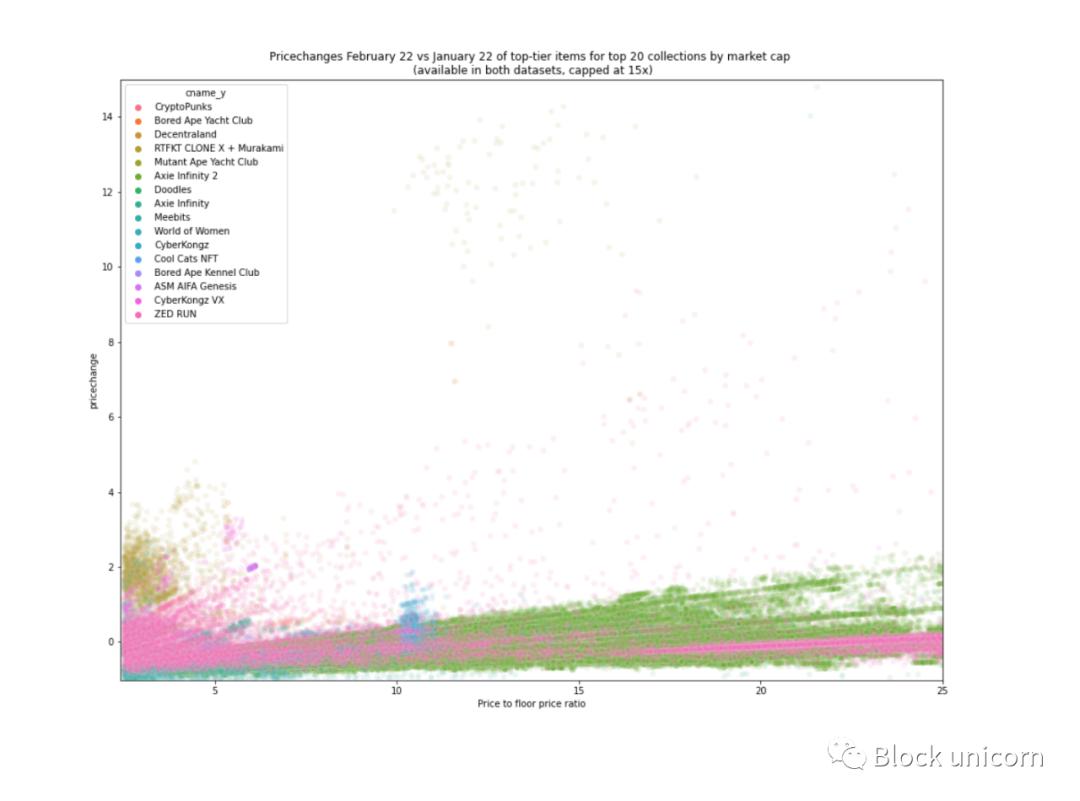

Under these definitions of lower and upper limits, we can define mid-tier products as those priced between [floor price1.4, floor price2.5]. Now let's look at the characteristics of these price tiers.

Characteristics of Defined Price Tiers

Items priced at floor price to floor price*1.4.

Floor items typically account for 50-75% of the collection, making up 25-50% of its market cap. Their quantity and homogeneous behavior make them suitable for liquidity pools, effectively acting as "on-chain AMMs," where users can earn from trading activities of on-chain assets and enjoy the deepest liquidity compared to other price tiers.

Items priced from floor price1.4 to floor price2.5.

Mid-tier items typically account for 20-40% of the products, making up 10-20% of the collection's market cap. Currently, mid-tier products may be the least profitable trading variety, as they require less liquidity than on-chain trading and have less exposure to reflexive increases compared to Grails. Collections where the mode is mid-tier (those with symmetrical price distributions) may be collections where many users are more interested in the attributes or utility of the asset itself rather than the price. For example, virtual land floors may be too small or located in unprofitable positions, while larger, high-traffic land may be too expensive or not for sale. Therefore, land buyers look for assets that are well-priced in terms of location, land size, and price.

If it turns out that the floor price includes some "temporary" items, i.e., those with rising floor prices or falling prices, then this could be a layer for speculative and related hedging applications.

Top or head items, priced > floor price*2.5.

Top-tier items typically account for 5-10% of the products, making up 20-40% of the collection's market cap. The sales of these items are very noisy, with significant price fluctuations, and their performance is similar to high-end items in "traditional" art or real estate. While their trading volume and velocity are low, they have good potential to serve as collateral or gain liquidity through fractionalization.

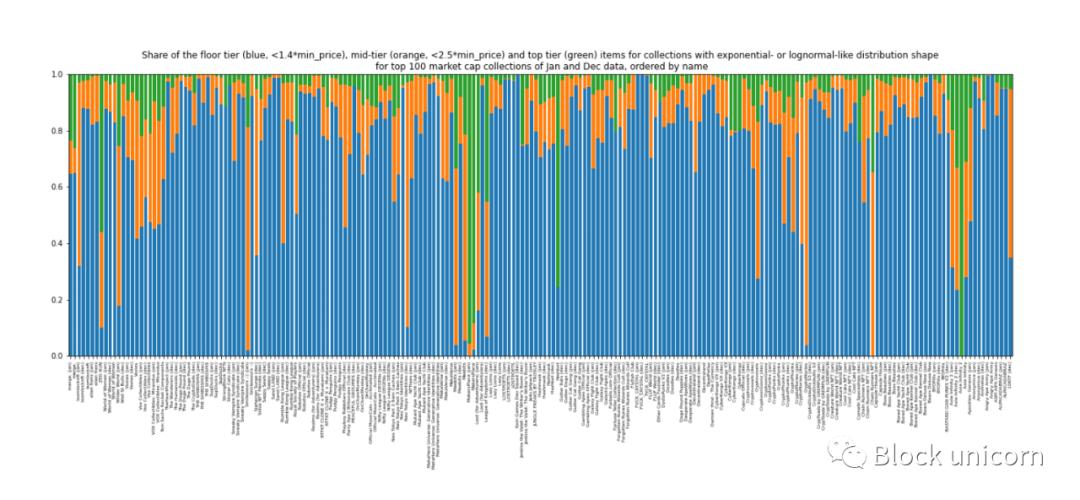

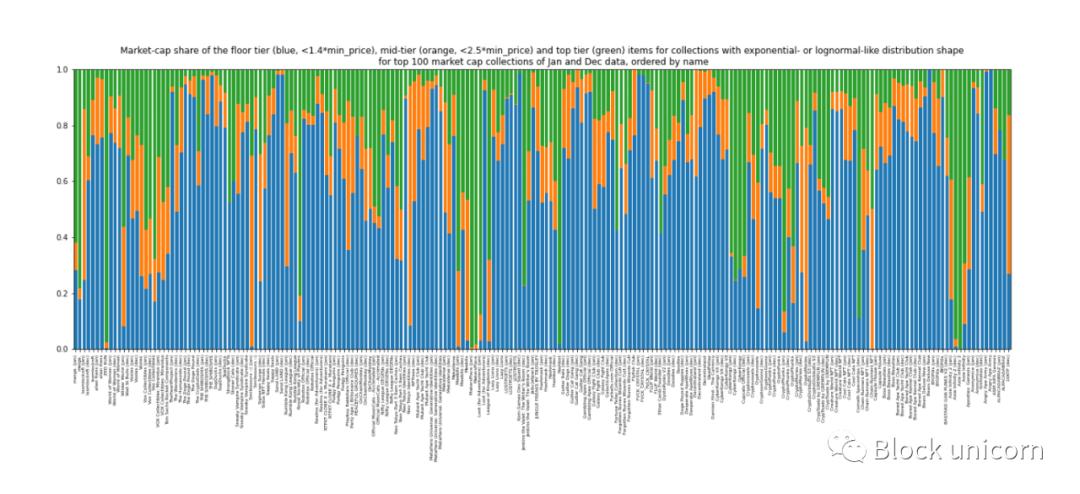

Regarding the share of items in each of the three tiers, we see a large share of floor items (blue). There are small shares here and there, but this relates to the fuzzy definitions of our shapes, such as Meebit (first column) not fully following our tier logic, as it has these additional bumps we further illustrate above:

The collection names are small, but the suffixes (Jan) or (Dec) indicate that they come from the January or December datasets, respectively.

When we look at the market share of each price tier, the situation becomes a bit noisy regarding the market cap shares of these tiers. While the floor seems to occupy most of the market share, it is common for cup items to be 10-1000 times higher than the floor, eroding the market cap of the collection.

Overall, about 25%-50% of the market cap belongs to the lower tier, 10%-20% to the mid-tier, and 20%-40% to the top-tier:

Future Work

In this article, we took some preliminary steps to classify NFTs based on their price movement behavior and the respective tiers within their collections. As we mentioned above, the boundaries of the tiers can be adjusted based on use cases. For us, one of the goals is to derive common behaviors and characteristics of NFTs across collections and asset categories to inform holders of the best ways to seek liquidity, and this analysis helps to inform that evaluation matrix.

Now that we have a high-level overview of how assets behave within collections, we can zoom in on the significant observations we made here and analyze them further, such as:

What key attributes of a given collection might lead to the price distribution patterns they exhibit?

What internal (e.g., project development) or external (e.g., market sentiment) factors might cause a given series to change its price distribution shape over time?

Can price distributions serve as leading indicators or analytical metrics for a given financialization protocol to load a given asset (e.g., collateral or launching an NFT AMM)?

We hope to explore these questions in future articles. For now, we provide a quantitative mental model for defining price tiers, as well as a preliminary framework for assessing our hypotheses regarding NFT liquidity methods in the coming months.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles