Arthur Hayes: As the "bond" of Ethereum, it will break 10,000 USD by the end of the year

The success of Ethereum has spawned a group of competitors who trade on hopeful futures rather than concrete performances.

The success of Ethereum has spawned a group of competitors who trade on hopeful futures rather than concrete performances.Author: BitMEX Founder Arthur Hayes

Original Title: 《Five Ducking Digits》

Compiled by: Gary Ma, Wu Says Blockchain

I do not have a high opinion of the so-called "financial advisors" in traditional finance. Their goal may not be to genuinely provide you with financial advice, but rather to maximize their own management and performance fees, even if the final financial performance is not great; they can still earn that income.

Most of the "financial advisors" I have encountered generally have a negative attitude towards cryptocurrencies and tell their clients not to invest in them.

Of course, we do not need to "look down" on them; we should apply the financial knowledge they usually articulate to the cryptocurrency industry. This article is simply to illustrate the importance of classifying asset targets when providing investment recommendations to individuals, companies, and governments.

What is ETH?

This is a simple yet profound question.

If you say it is a commodity, then a certain type of investor will be interested.

If you say it is a currency, then another type of investor will be interested.

But what if you can convince the world that ETH is just a perpetual bond?

The post-merge Ethereum will transition to PoS, where the staking rewards for validators and network fees turn ETH into a bond.

If we can persuade financial advisors that the asset classification of ETH is a bond rather than a currency, then they might be swayed. Additionally, by that time, Ethereum will have more environmentally friendly and prosperous ecological data, making ETH significantly undervalued compared to Bitcoin, fiat currencies, and other L1 competitors.

Calculating the Staking Account of ETH

According to the predictive data from Ethereum researcher Justin Drake, in the early stages after the merge, the annualized staking yield is about 8--11.5%.

If you are a die-hard ETH fan, you may agree or disagree with these numbers. But for now, I will treat them as "facts." The focus of this article is not to delve into whether the yield is 5% or 10%, but to use scenario analysis to value ETH as a bond.

In this analysis, we will assume that you sell an equivalent amount of USD to purchase 32 ETH. This is extremely important; I am viewing this valuation from the perspective of someone who first invests in fiat currency. Therefore, the cost of USD funds is crucial, just like any arbitrage trade.

To make this analysis impactful, we must convince larger capital allocators to believe that ETH is a bond. Once this concept is successfully established, everything else will follow naturally.

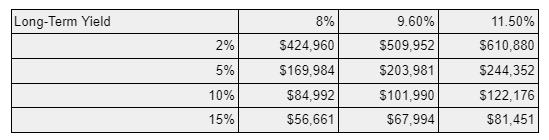

These funds can borrow money closer to the U.S. Treasury curve. That is why I will use the yields of 5-year, 10-year, 20-year, and 30-year bonds as my discount rates. I used the estimates of ETH rewards from the table above, which are the sources of the 8%, 9.60%, and 11.50% yields. I used the yields of these bonds at some point on March 28, 2022.

Steps:

- Borrow USD for a period, then purchase ETH at the current exchange rate.

- Stake 32 ETH to earn ETH-denominated rewards.

- After a certain number of years, sell 32 ETH and receive USD rewards.

- Repay the USD loan.

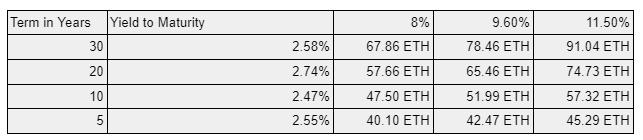

The table below shows the present value of ETH bonds in terms of ETH.

Remember, we start with 32 ETH. This is the bond value in ETH terms, including the initial principal of 32 ETH. Market convention is to quote bonds as a percentage of face value, which would be 32 ETH. But to highlight the amount, I used the nominal ETH amount. I also did not reinvest the ETH earnings through staking. If we adopted continuous compounding when receiving ETH earnings, the bond's value would be higher. Obviously, continuous compounding is possible and financially prudent, but for the sake of mathematical simplicity, I did not do so.

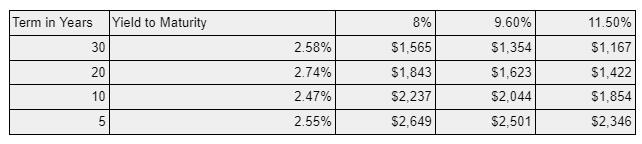

The table below reflects the breakeven price of ETH/USD. This is the price at loan maturity, from the USD perspective, where the trade breaks even. I assume all ETH cash flows are converted to USD at a constant ETH/USD price, allowing me to calculate the price at which this trade becomes uneconomical.

Below is another version of the same table, this time expressed as a percentage change from the current ETH/USD spot price of $3320.

Local Currency Bonds

Local currency bonds refer to bonds where the issuer's domestic currency is the same as the borrowing currency. If you are a USD-based investor, these bonds carry currency risk. Some investors prefer these bonds because they typically offer high yields. However, if investors hedge their currency risk, the effective yield usually decreases.

Typically, the non-deliverable forward (NDF) points for emerging markets are positive. This is due to the relationship of interest rate parity. But take a look at this example of the Malaysian Ringgit NDF.

The spot USD/MYR is 4.2148, while the 1-year NDF is 4.24/4.26, meaning its trading price is higher than the spot price. If I buy MYR local currency bonds and need to sell MYR for USD in the future, I will trade on the right-hand side (RHS) and effectively pay the forward points. This means I need to spend money to hedge my position.

Some investors are willing to take on currency risk, while others are not. As a good financial advisor, you are contradictory; you will simply offer two different products. One is hedged, and the other is unhedged. In both cases, you will charge a fee.

In the case of a 5-year ETH local currency bond, if we assume an annual yield of 11.50%, then the ETH/USD price must drop by 29.35% for investors to incur a loss in USD terms after 5 years.

But if investors want to hedge currency risk, they need to at least hedge the expected total cash flows through forward trading. Currently, the liquidity of ETH/USD listed futures has been very low over the past 3 months. I contacted a well-known broker on March 28, 2022, to ask what the mid-price of the premium or discount for a 1-year ETH/USD forward was.

If I go long on the ETH bond and get a quote for the ETH/USD forward, I trade on the left-hand side (LHS), selling ETH and buying USD. The broker quoted me a market mid-premium of +6.90%. This means that to hedge my local currency ETH bond, I actually received income. I sold the ETH/USD forward at a price higher than the spot. This is a positive arbitrage trade.

Few trades can give you a higher yield when investing in foreign currency bonds, while hedging back to your home currency actually earns you money.

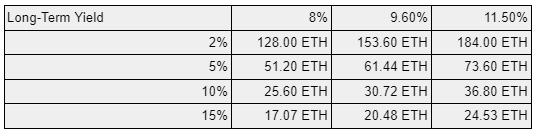

As the final part of this analysis, I valued a perpetual bond using the validator income obtained from staking ETH.

Initially, I thought of ETH as similar to a perpetual bond. That is a bond with no maturity date. Before delisting at the end of 2016, the British Consols were one of the longest continuously priced government bonds in history.

In the hundreds of years of history of this debt instrument, the nominal long-term yield in the UK has generally been 5% or lower. Therefore, let’s assume that the long-term yield from now on is 5%, while the return on ETH is at our predicted lower end of 8%. We derive the final present value of ETH cash flows to be 51.20 ETH. The required input for this ETH cash flow is 32 ETH.

If we use this to determine the implied value of ETH as a bond, we arrive at the following chart. These values are simply the multiplication of [spot * present value of ETH rewards].

This should not be viewed as a price prediction, but rather as guidance for a new way of thinking. If you believe that ETH can or should be valued as a bond, then as an investor, considering your long-term interest rates and ETH return assumptions, you should be willing to buy ETH at today’s price as long as its trading price is at a discount to its price derived from the perpetual bond.

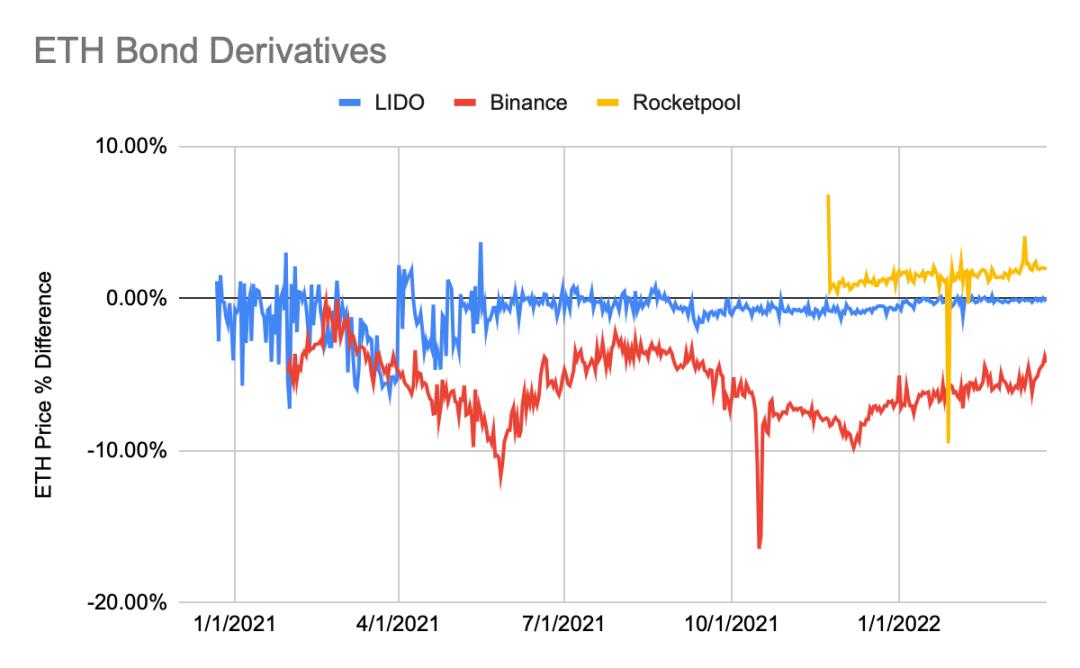

When we later discuss ETH bond derivatives, we will return to this perpetual ETH bond table.

Capital Efficiency

To utilize ETH bonds, capital needs to be locked indefinitely. This is because currently, once ETH is staked on the beacon chain, it cannot be unstaked. After the merge, when PoS validation begins, ETH yields will rise, but stakers will still be locked.

There are various validation pools that allow traders to easily contribute ETH and start earning rewards. To provide liquidity for those who are locked, these pools have issued their own tokens, which are pegged to the staked ETH at a 1:1 ratio.

For example, if you deposit 1 ETH into the Lido pool, you will receive 1 stETH, and its trading price is determined by the market. The three largest pools are Lido, Binance, and Rocketpool.

This chart shows the daily premium or discount percentage of a pool's token trading against ETH.

Pool token price premium = Rug risk + Implied ETH rewards + Liquidity preference

Let’s illustrate this:

Rug risk: This is the risk that there are some vulnerabilities in the validator code. If, for whatever reason, this smart contract is compromised, the staker's funds may become unrecoverable.

Implied ETH rewards: The tokens in these pools will receive ETH rewards. Therefore, the market will discount the future rewards that token holders will receive to the present.

Liquidity preference: This quantifies the desire of those who want liquidity today. The higher the preference, the higher the discount of a token in a pool to ETH. On the other hand, if a pool restricts the amount of ETH deposits it can accept, the liquidity preference may actually increase the price of the pool token, as in the case of Rocketpool.

My analysts have delved into the details represented by the Lido, Binance, and Rocketpool tokens, trying to understand why they trade at different premiums to ETH.

Lido: This pool has the largest market share (about 85%) and trades very closely to the price of ETH. When you stake ETH, you receive stETH at a 1:1 ratio. The ETH staking rewards will accumulate to stETH minus the fees charged by Lido for providing services. This token can be used as collateral in other DeFi applications without affecting the accumulation of ETH rewards.

Binance: This is the second-largest pool by market share, trading below ETH. When you stake ETH, you will receive bETH at a 1:1 ratio. The ETH staking rewards will be obtained by bETH, minus the fees charged by Binance for providing services. This token can be used as collateral in other DeFi applications, but when bETH is staked outside your Binance wallet, you will not receive ETH rewards. My analysts believe this is a significant reason why bETH trades much lower than ETH. In the DeFi ecosystem, it is not as good a utility as stETH or rETH.

Rocketpool: This pool has the smallest market share among the three. Its trading price is always above ETH. When you stake ETH, you receive rETH at a 1:1 ratio. The ETH staking rewards will accumulate to rETH minus the fees charged by Rocketpool for providing services. Rocketpool is decentralized, unlike the other two pools, and severely restricts the amount of ETH deposits it can accept. More deposits can only be accepted after more operators come online. This token can be used as collateral in other DeFi applications without affecting the accumulation of ETH rewards.

stETH is the best approximation of the present value of ETH bonds. I proposed a theoretical hypothesis about present value, while stETH is the concrete market performance.

The trading price of stETH is basically consistent with ETH, which is puzzling.

Liquidity preference: Coingecko data shows that stETH has a market cap of $9.8 billion and a daily trading volume of $100 million, about 1% of its market cap. The daily trading volume to market cap ratio of Ethereum is about 3%. If stETH holders truly cared about the liquidity of their lido investment's ETH balance that they cannot access, the trading volume of stETH relative to its market cap would be higher. Therefore, the liquidity preference of investors seems to be close to zero. As more DeFi platforms accept stETH as collateral, the demand to convert stETH into ETH decreases.

Implied ETH rewards: If we assume the annualized rewards for ETH post-merge are 8%, then the implied rewards are 8% multiplied by the time the staked ETH is released. We do not know how long this will take. If the market believes it will take another 6 months post-merge to release the held ETH balance, then the premium should be 4%.

Rug risk: It is nearly impossible to estimate what this risk actually is. We can only prove it by assuming the other three variables. However, it is certain that if you stake ETH on Lido and do not trust the integrity of the technology, you would sell your stETH. But considering that stETH trades at the same value as ETH and has a low average daily trading volume, the market certainly believes in Lido's technology.

My conclusion is that stETH either assumes the entire ETH 2.0 process will be completed very quickly post-merge, or it is extremely undervalued compared to the bond mathematics of ETH rewards post-merge. If, after reading this article, market participants agree with my view that ETH is a bond post-merge, then stETH should gradually trade at increasingly higher premiums.

Collateral Utilization Rate

Since these staking tokens exist, they should be used as collateral in the DeFi ecosystem, essentially unlocking trapped collateral. AAVE is a decentralized lending protocol that allows traders to use stETH as collateral. Currently, the LTV of stETH as collateral is 70%. MakerDAO also allows users to use wrapped stETH (WSTETH) as collateral to create DAI, which is its stablecoin pegged to the USD. The current collateral ratio is 160%.

This is huge. The cornerstone of the global fiat credit market is the ability to create debt assets, which are simply loans issued to certain entities, then using this debt asset as collateral to borrow more money. This is how leverage drives the global economy.

While this behavior has obvious benefits, it does pose systemic credit risks to the system. If protocols allow for increasing utilization of pool tokens as underlying collateral, and there is an event that renders staking tokens worthless, then all value built on that foundation will also be affected. As these tokens become more widely accepted, we must be mindful of this risk. The benefit of DeFi is that all activities are completely transparent because they are on-chain. Therefore, we can build very precise monitoring systems to measure the immediate credit risk in the DeFi system attributable to staking tokens.

In terms of interest rates and credit derivatives, the ways these staking tokens are utilized are almost limitless. However, before I get too excited, let’s first look at how the market is developing. In the future, I will have many promising projects that begin to utilize this new collateral pool to do innovative things and bring life to the ETH fixed income market in a decentralized manner.

What Would Michael Saylor Do?

Saylor is a "rogue" because he takes advantage of Microstrategy to use the corporate bond market as a financing tool to acquire Bitcoin. This is indeed a strategy, but Bitcoin is purely a currency with essentially no yield. ETH is the commodity that powers the world’s largest decentralized computer. Post-merge, ETH will have intrinsic yield.

What Saylor or any other high-yield issuer should do is issue debt and buy ETH. This is a positive arbitrage trade.

The above chart shows the average OAS of Bloomberg's U.S. corporate high yield. This indicates that U.S. corporate junk bond issuers currently pay an average of 3.41%.

Using the model above, let’s assume you are the CEO of a real company looking to achieve a high stock price through memes. Don’t worry about what your company should do; your goal is financial optimization.

Input:

3.41% cost of capital

5-year maturity

8% ETH rewards

$3,320 ETH price

Output:

The present value of this bond is 41.28 ETH.

The breakeven ETH price is $2,573, a drop of 22.48%.

Assuming no price changes in the ETH/USD exchange rate, the return in USD terms is 29%.

Would a lavish CEO really hedge currency risk? Absolutely not!

For any publicly listed CEO, announcing debt issuance along with a large purchase of ETH bonds can create double the value. First, because your stock is now a company tagged with "DeFi," "web3.0," "metaverse," etc., which will excite Reddit meme stock traders. Second, the trade has a positive spread; therefore, putting this at a scale of $1 billion, according to accounting treatment, $290 million in income can be recognized immediately or later. You won’t lose money!

ESG: The Green Investment Theme

The ESG investment theme is now very popular in traditional finance, and while this concept is correct, who knows if it is just a gimmick for financial advisors to better sell you products. While many funds previously wanted to allocate some capital to cryptocurrencies, the energy consumption of PoW contradicts the ESG concept. However, Ethereum's transition to PoS through the merge is a response to ESG, which will change their view on ETH, making it accessible to a broader audience of funds. Although many other public chains also use PoS, as traders, this marginal change in fundamentals is a huge positive.

Ethereum Killers

Ethereum's performance issues have always been a point of criticism from competitors. The prices of these Ethereum killers have skyrocketed since last year, and their valuations have greatly increased. Now that Ethereum is at the forefront of the merge, which may or may not bring performance improvements, will ETH perform better compared to other L1 tokens?

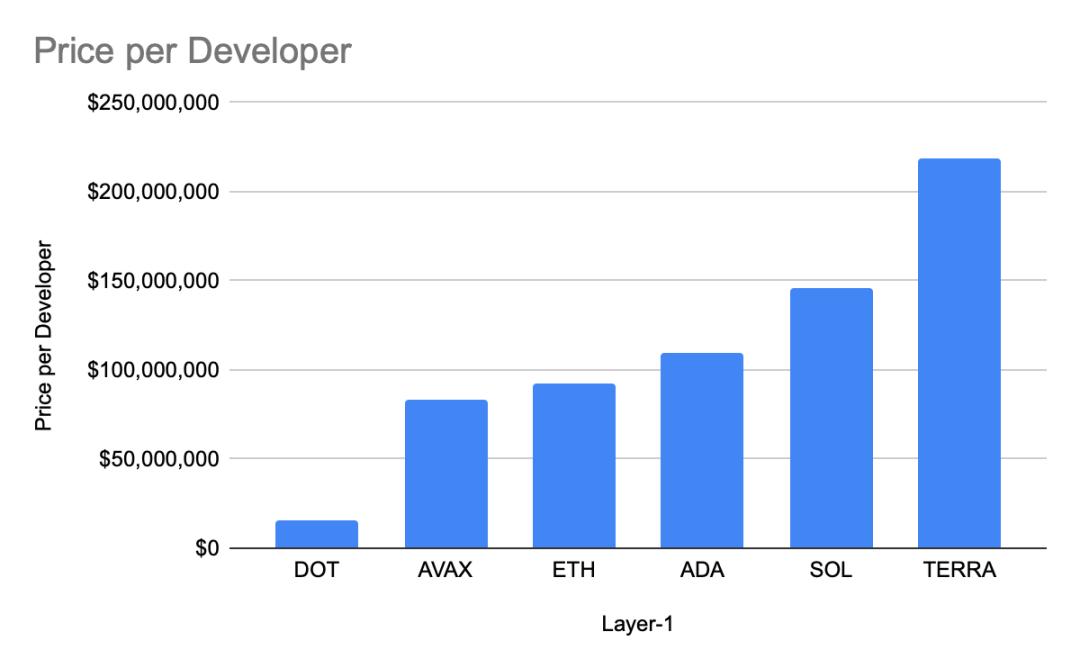

This "price/developer" ratio chart reflects the market cap of some L1s divided by the number of active developers.

Electric Capital published a very important and insightful research article estimating the number of active developers on each mainstream public chain. A public chain is built to be used. If only a few developers are creating new projects on a chain, that chain will never become valuable.

Most Ethereum killers have much higher multiples because they hope to attract talent to develop on their chains.

According to this report, Ethereum has about 4,000 developers, three times more than Polkadot, which has the second-largest developer group.

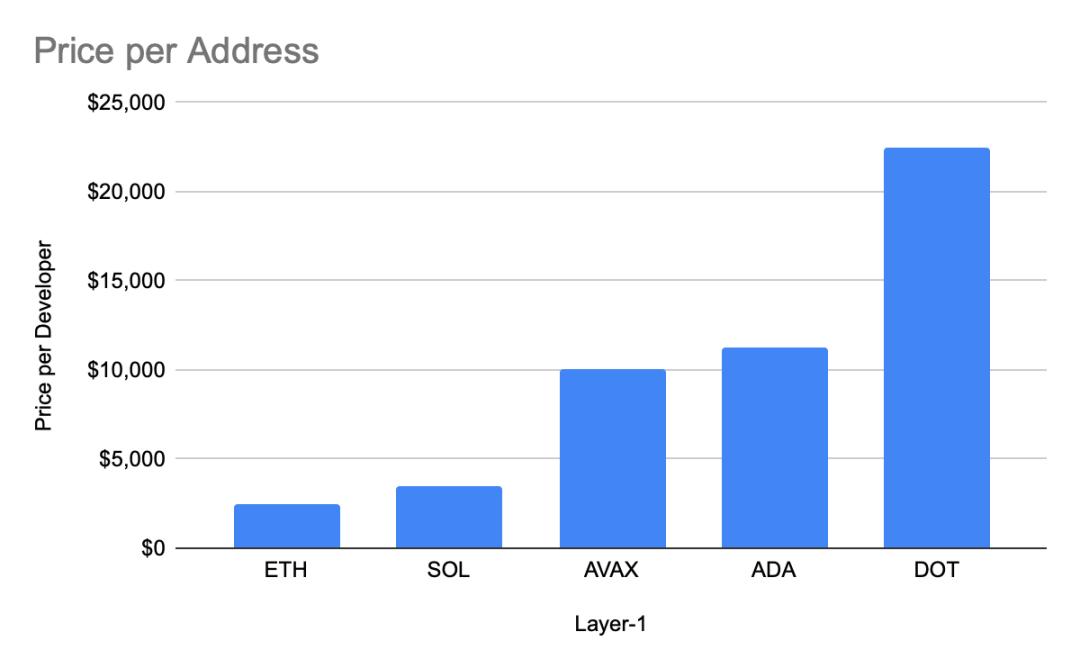

This "price/address" ratio chart reflects the market cap of selected mainstream L1 protocols divided by the number of addresses.

The number of addresses on a chain is another rough but useful metric for assessing the health of a public blockchain. Ethereum's number of addresses is 16 times that of Solana, but when calculated by price/address, it is still cheaper.

This is another good indicator of hype. Those blockchains that exist solely to capture market share from ETH have much higher multiples.

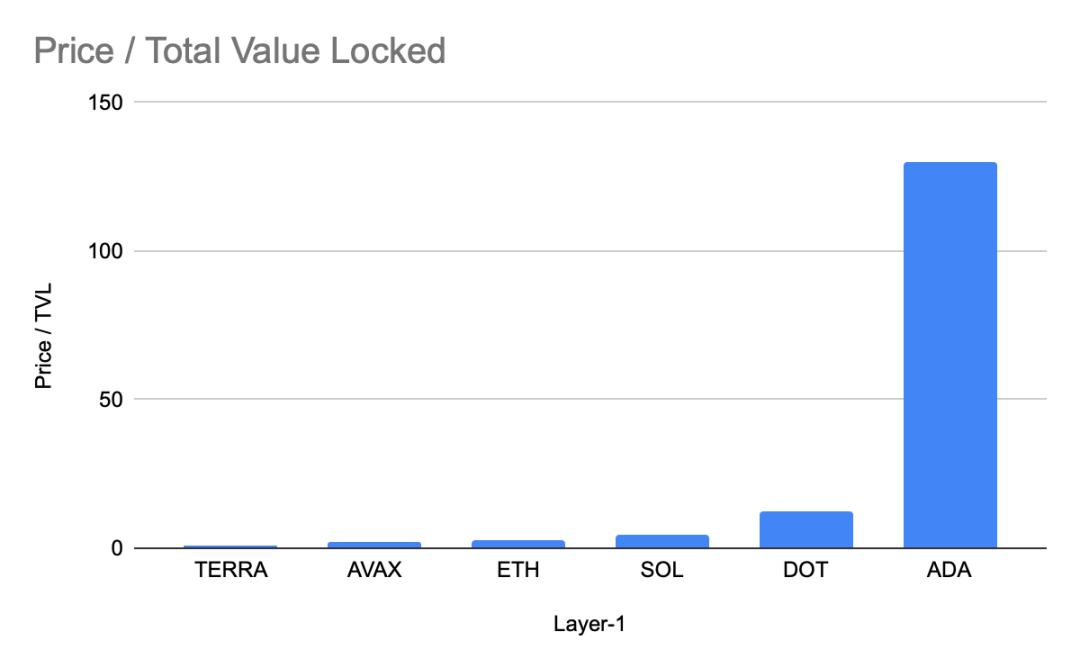

"Price/TVL" is the market cap divided by the total value locked in dApps on the protocol.

This ratio is the simplest way to identify the level of attractiveness of DeFi. ETH is the third cheapest, behind TERRA and AVAX. I am not even sure if ADA should be included; if there is a coin that purely trades on hope, it is Cardano.

In light of these fundamental ratios, ETH may be the cheapest L1. Ethereum's success has spawned a batch of competitors that trade on hopeful futures rather than concrete performance. There is nothing wrong with that, but as ETH is about to feel the love from bond and ESG investors, can these other coins keep up?

If you are a capital allocator, either already holding some of these coins or needing to choose which L1 token to invest in, wouldn’t you want to buy the cheapest one? Although ETH's market cap is several orders of magnitude larger than its competing chains, it is still cheap from a network fundamental valuation perspective.

As this year progresses and the merge approaches, I expect ETH to significantly outperform any L1 chain built. This statement has held true from 2020 to the end of 2021, but now, from the perspective of capital flow and returns, Ethereum supports extremely positive price fundamentals.

Please do not mistake this sentiment as me believing that these L1 chains cannot retest the historical highs of November 2021. This is purely a relative argument. ETH could rise to $10,000, about a 3x return, while Solana could rise to $200, about a 2x return. Would you be happy to own Solana? Capital will flow to where it is treated best.

Three Ways to Allocate ETH

There are three ways to consider how to allocate ETH: fiat & Bitcoin & other L1s.

Fiat

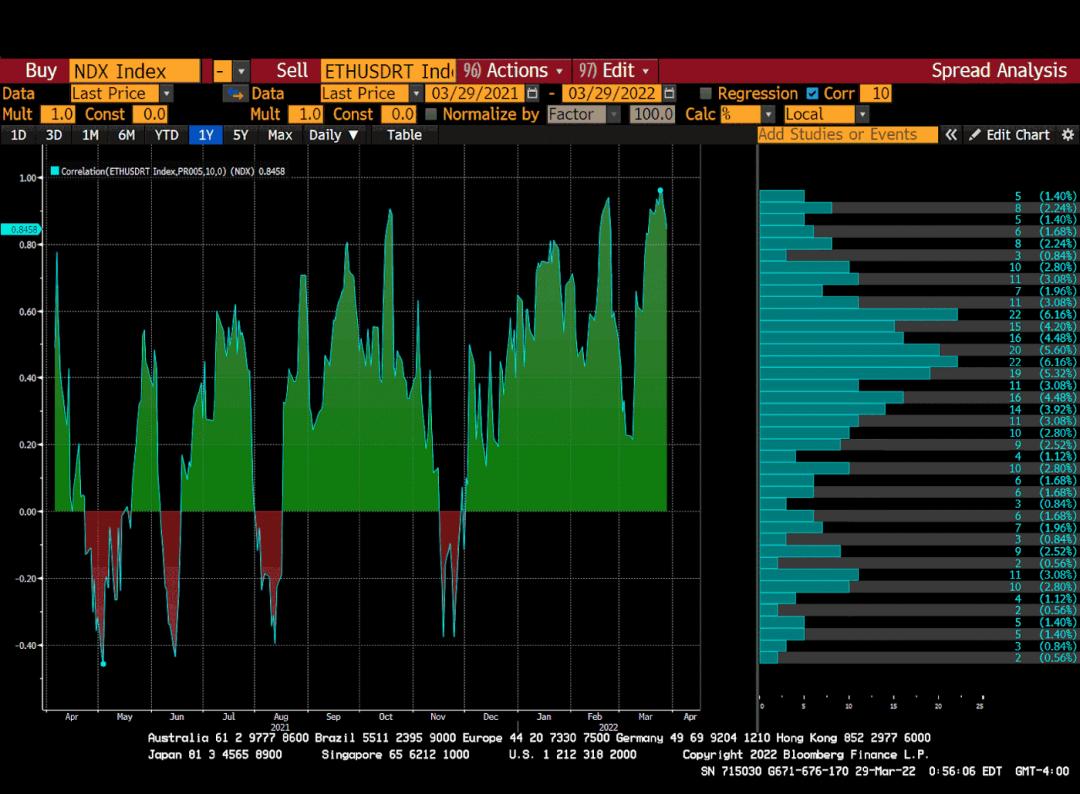

This is the 10-day rolling correlation chart between ETH and the Nasdaq 100 index, with a correlation coefficient as high as 84%.

ETH (and Bitcoin) are risk assets, just like large-cap U.S. tech stocks.

As the Federal Reserve continues its path of raising nominal interest rates, and with the 2s/10s curve inverted, pointing to a future U.S. economic recession, stocks will be crushed (down 30% to 50%) until there are problems in the credit market, and the Fed restarts the money printing machine.

If I wholeheartedly believe this, then I must also believe that ETH in USD terms can drop by 30% to 50%. Unless the broad risk asset market collapses, or the short-term correlation of ETH with the Nasdaq 100 index or S&P 500 begins to decline, I will not sell fiat and buy ETH.

No matter what I think of ETH's strong fundamentals, macro conditions do not exist.

BTC vs ETH

My cryptocurrency portfolio at the beginning of 2022 was 50% Bitcoin and 50% Ethereum. I firmly believe that ETH is cheap relative to other areas of the crypto world. Therefore, my target allocation is 25% Bitcoin and 75% Ethereum.

Bitcoin needs to change the narrative to become the "worst rock star" again. Like Ethereum, Bitcoin is viewed as another risk asset, but it is a massive risk asset because it trades around the clock and is the last remaining free market globally.

Bitcoin must again be viewed as a store of value and an inflation hedge because it is the hardest form of currency to create in history. Ethereum is not a currency; it is a commodity that powers the world’s largest decentralized computer. The Ethereum community has explicitly decided that ETH is a commodity used to drive this computer, not a purely monetary tool.

At the protocol level, Bitcoin has no implied yield, while post-merge Ethereum does. Therefore, Bitcoin is a currency, while ETH is a bond linked to a commodity.

Given that global real interest rates are negative, I want to own an asset with positive yield in its currency terms. Currently, that is ETH; Bitcoin itself does not generate yield. Therefore, from a pure spread perspective, I should own more ETH than Bitcoin. With the new rewards and validation system in place, this situation will change when the price of ETH rises sufficiently to include future ETH cash flows.

Finally, funds from environmentally friendly investment theories like ESG will also "safely" invest in ETH post-merge rather than Bitcoin.

ETH vs L1s

I hope the charts published earlier clearly indicate that feeling ETH is undervalued is based on network fundamentals, while its competitors are more based on brighter futures. Similarly, other L1s may realize their dreams of overthrowing ETH, but they still find it difficult to do so. With the upcoming implicit yield of ETH and the ability of ESG investors to allocate ETH, the hopes of surpassing ETH will become increasingly dim. They better trade something they can prove is undervalued on network fundamentals.

Finally, let’s talk about cross-chain bridges for assets. Wormhole and Ronin (Axie Infinity) were hacked for nearly $1 billion worth of ETH, other cryptocurrencies, and stablecoins. Essentially, these bridges are ecosystems trying to import all the amazing DApps originally built on ETH to new chains. If traders grow tired of worrying about whether their bridge will become the next implosion, they may simply migrate their TVL and business back to ETH, which is marginally negative for any competitive L1. Trust in V God, rather than putting your feet in the River Styx, flirting with the wrath of Hades.

ETH Price Breaking Through Five Digits

A few years ago, I wrote an article predicting that the price of ETH would break into double digits, which quickly came true.

Then, when I saw a chart showing that the total value of DApps built on Ethereum exceeded the market value of Ethereum itself, I further allocated ETH, which was a strong buy signal.

I have experienced the current ups and downs and am very satisfied with the relative scale of my ETH allocation in my cryptocurrency portfolio. The remainder of 2022 will be the performance time for ETH.

When the dust settles at the end of the year, I believe the trading price of ETH will exceed $10,000.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles