The New Public Chain War Without Gunpowder: Where Are the Top 70 Blockchain Games Built?

Traditional gaming giants entering the blockchain space have initially chosen long-term partnerships with public chains. Some industry insiders believe that behind this seemingly decisive move lies a tense competition among new public chains.

Traditional gaming giants entering the blockchain space have initially chosen long-term partnerships with public chains. Some industry insiders believe that behind this seemingly decisive move lies a tense competition among new public chains.Source: Chain New

Author: Liao Yu

On March 23, 2022, Krafton (Bluehole), the developer of the "PUBG" series of games, announced on its official website that it has signed a long-term cooperation agreement with the blockchain technology platform Solana Labs to provide blockchain-based games and services.

In the announcement of the agreement, Johnny Lee, head of game business development at Solana Labs, said: "We see an increasing trend of players in blockchain games and are ready to respond quickly to this demand. Bluehole is a well-known innovator in the gaming industry, and we are excited to be part of their next level."

As Johnny Lee mentioned, Bluehole, as a leading global video game publisher, considers it crucial to explore the use of NFTs and develop Web3 games based on the Crypto ecosystem. It is puzzling that Bluehole did not "engage multiple partners and focus on development" like Konami and Ubisoft, but instead chose to collaborate long-term with Solana from the outset.

Traditional gaming giants entering the blockchain space have chosen long-term public chain partners right from the start. Some industry insiders believe that this seemingly decisive move reflects the tense competition among new public chains.

A public chain, simply put, is a network that supports the development of various types of applications such as DeFi. Since Vitalik Buterin (V God) created ETH (Ethereum) in 2013, the birth of new public chains has never stopped, with the number of active public chains currently exceeding 100.

In terms of landscape, Ethereum remains the absolute top public chain, but new-generation public chains like BNBChain, Solana, and Avalanche are gradually expanding, forming a pattern of "one strong and many robust."

In the complex world of blockchain, how will blockchain game projects choose public chains, and what characteristics will public chains have to attract excellent blockchain game projects? This not only affects the development prospects of individual public chains but also influences the changing landscape of the blockchain world.

Where are the top blockchain games distributed? Two major tiers + numerous non-mainstream public chains

To understand the appeal of public chains to blockchain game projects, we must first clarify which public chains excellent blockchain game projects are concentrated on.

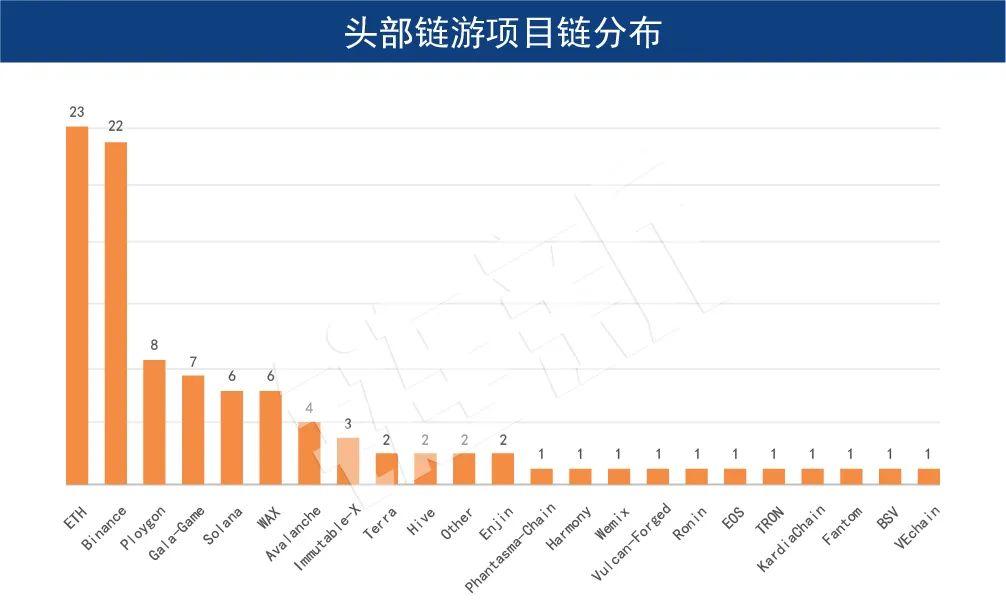

According to real-time data from the Play to Earn website on March 19, 2022, Chain New analyzed and compiled a ranking of the top 70 blockchain game projects globally and their corresponding public chains.

First, among the global top 70 blockchain game projects, 24 games have multiple public chain positions, accounting for as much as 34.29%, with some projects even having 4 different main chain addresses, and these "multi-chain projects" are showing a gradually increasing trend.

Deng Bo, a senior researcher at Cool Link Technology, told Chain New that there are two main reasons for the formation of multi-chain projects: first, the development of blockchain game projects is limited by the main chain, forcing project teams to "move"; second, project teams build multi-chain addresses specifically to attract users from different chains.

"For example, Axie Infinity was initially on ETH, but later due to the cost and efficiency issues of ETH, they started anew on Ronin. The behavior of building multi-chain addresses to attract users from different chains is quite common; many new blockchain game projects consider multi-chain plans from the outset, which is also a manifestation of the competition within blockchain games," said Deng Bo.

However, from the perspective of public chains, among the 23 public chains involved in the top 70 game projects, nearly half of the public chains have only 1 blockchain game project. The "many chains but few projects" situation leads to "competition for positions" among public chains, forming a distinct tiered structure.

Senior gamer C3 PO told Chain New: "User migration is mutual; blockchain games can build multi-chain addresses to attract users from different chains, and some niche public chains will also establish partnerships with top blockchain game projects to create public chain addresses for them, thereby attracting blockchain game users to enter niche public chains."

Among the 23 public chains involved in the global top 70 blockchain games, they can be categorized into three tiers based on their frequency of appearance, indicating the popularity of public chains.

The first tier shows a clear head effect, being bound by more than 20 blockchain game projects, namely ETH (23 blockchain game projects) and BNBChain (22 blockchain game projects); the second tier is bound by 6-8 blockchain game projects, including Polygon, Solana, WAX, Gala-Game, and Avalanche.

The third tier consists of public chains that appear less than 3 times, totaling 16 public chains, of which 11 public chains have only appeared once. This means that these 11 public chains only support the daily operations of one top blockchain game, and while there are chains like Ronin that serve only one project, most public chains also host other medium and small blockchain game projects, such as Harmony and Wemix.

The numbers 20, 8, and 3 delineate the three tiers of public chains, with little difference within the same tier, but a significant difference in the attractiveness to top blockchain game projects between different tiers.

Such a "tiered concentration" distribution of blockchain game projects is closely related to public chains and their characteristics.

New public chains compete, who will take the lead?

In the 8 years of blockchain development, Ethereum, created by V God, has been the dominant player for a long time.

It wasn't until the DeFi Summer in June 2020 that the explosive growth of DeFi application development raised new demands for network operational efficiency, making Ethereum's congestion issues increasingly apparent. The high Gas fees led every developer and investor to seek and establish other public chains to reduce user costs and supplement Ethereum's functional shortcomings.

Following this, the continuous growth of the DeFi market in 2021, along with the boom of NFTs and GameFi, further spurred the explosion of the entire public chain ecosystem, leading to the rise of Ethereum's competitors.

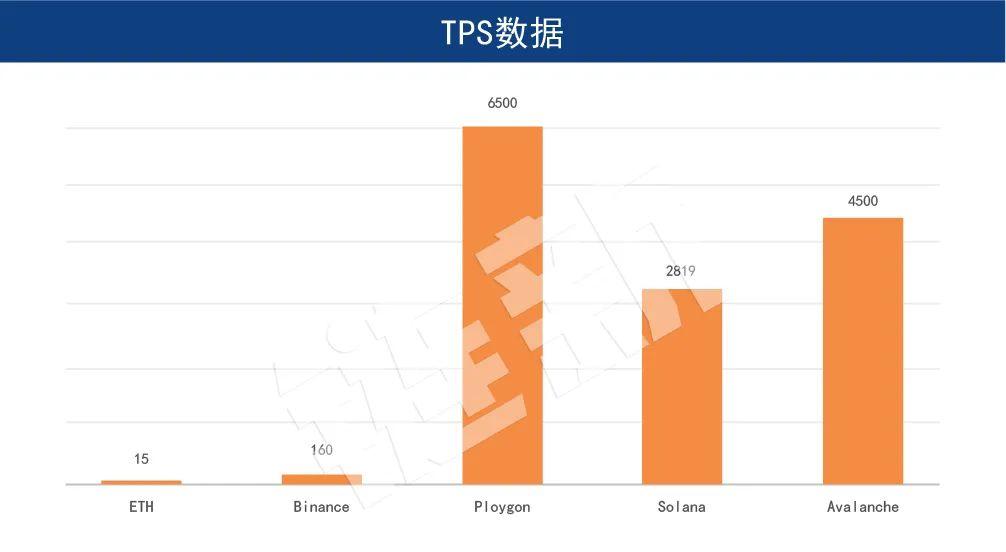

Based on the phenomenon of "tiered concentration distribution" of excellent blockchain game projects, Chain New selected five public chains—ETH, BNBChain, Polygon, Solana, and Avalanche—for data comparison (as of April 1) to analyze the reasons for the concentration of top blockchain games.

・1. TPS Performance: Polygon > Avalanche > Solana > BNBChain > ETH

TPS (transactions per second) refers to the number of transactions a network can process per second and is an important indicator of public chain performance. The higher the TPS, the higher the efficiency of the public chain.

However, DeFi faces the "impossible triangle," meaning that high performance, security, and decentralization cannot be achieved simultaneously. High transmission rates can also lead to network instability during peak times, and there is currently no good solution.

・2. Token Price: ETH > Solana > BNBChain > Avalanche > Polygon

The price fluctuations of a public chain's native token affect user transaction fees and also reflect users' valuation of that chain.

From the real-time public chain price data on April 3, 2022, from Nonce, the ranking of token prices and total market capitalization of the five public chains is exactly the opposite of the TPS ranking, with the highest TPS, Polygon, ranking lower in both token price and total market capitalization, occupying the 13th position globally.

(Data source: Nonce)

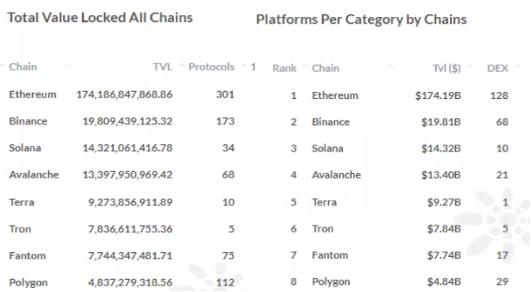

・3. Ecosystem Completeness: ETH > BNBChain > Polygon > Avalanche > Solana

When evaluating the value of a public chain, the completeness of ecosystem construction is an important assessment criterion. The types and numbers of on-chain projects reflect the activity level of developers and the popularity of the public chain.

From the number of projects on Footprint, ETH leads the way, followed closely by BNBChain and Polygon, while Avalanche and Solana lag behind. In terms of compatibility between ETH and other chains, specifically the distribution of cross-chain bridges with new public chains, Polygon has the most (21), followed by BNBChain (15) and Avalanche (13), while Solana ranks last with only 3 cross-chain bridges.

Footprint Analytics---TOP10 Public Chains in DeFi, Number of Public Chain Projects

Overall, in terms of ecosystem completeness, apart from ETH, BNBChain and Polygon each have their strengths as the second tier, while Avalanche and Solana, as new public chains in the third tier, still have room for development.

・4. Incentive Measures: Solana > BNBChain > Avalanche > Polygon

The main goal of public chains is to build ecosystems. To provide a friendly development environment, various public chains have launched incentive programs and ecosystem development funds to attract more developers to deploy projects.

Previously, Chain New explored the "new track trend" and compiled data on 108 funds from October 2021 to February 7, 2022, which included 17 ecosystem funds from various public chains, raising a total of over $2.285 billion.

According to the table, Solana and Avalanche's ecosystems are favored by investment firms, with the number of projects funded by their ecosystem funds accounting for 35.29% of the total ecosystem funds during the same period. In terms of investment scale, although BNBChain's $1 billion is substantial, Solana excels in the number of projects funded and has also attracted established giants like Grayscale and FTX to support it, showcasing its formidable strength.

New public chains "dividing" Ethereum?

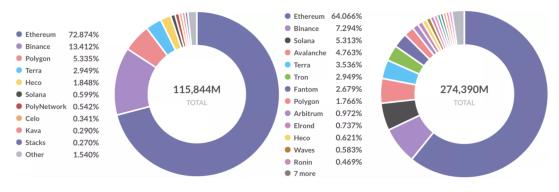

According to Footprint Analytics data, from June 30, 2021, to November 23, 2021, Ethereum's market share fell from 72.87% to 64% in just six months, a decrease of nearly 9%, indicating that emerging public chains are continuously dividing the Ethereum market.

(Footprint Analytics - Public Chain Market Share Distribution on June 30, 2021, and November 23, 2021)

From the table, it can be seen that beneath ETH, BNBChain, Solana, and Avalanche follow closely, while Polygon's market share has contracted, dropping from third place in June to eighth place in November, highlighting the intense market competition and the emergence of a "one strong and many robust" competitive landscape.

Currently, Ethereum remains the first choice for most DeFi projects, but compared to Ethereum's congestion and high Gas fees, new public chains generally offer faster speeds and lower costs, gradually breaking through in areas such as cross-chain bridges, compatibility, and exploration of new fields, attracting strong alliances among giants. The collaboration between Krafton (Bluehole) and Solana Labs is the best proof of this.

At present, there are still many who oppose the development of traditional game manufacturers in the blockchain game field. For instance, developers like GSC Game World have publicly opposed plans to use NFTs in games.

Projects like Axie Infinity point out that the decentralized production relationship is the real innovation brought by blockchain games, and the creator economy sparked by this is more sustainable, thereby squeezing market share. Traditional gaming giants may find it difficult to truly understand and influence this "evolution."

The effective realization of decentralized creation is not easy, and the advantages of AAA game manufacturers should not be underestimated. Whether the two can "join forces" will influence the exploration of new models for the integration of blockchain and traditional industries.

Risk warning

Risk warning Risk warning

Risk warning