Multicoin Capital: The disruptor of Ethereum, the king of the crypto party, and the thesis-driven maniac of hundredfold returns

Multicoin has taken the hippie investment in crypto to a new height of pure rationality.

Multicoin has taken the hippie investment in crypto to a new height of pure rationality.Original Author: Dongfang Ming /Overseas Unicorn Team

In the spring of 2017, the two founders of Multicoin Capital, Kyle and Tushar, recognized the lack of analytical frameworks in crypto investment after experiencing the ICO bubble. They decided to become the Benjamin Graham of the crypto world, attempting to usher in an era of value investing in the crypto space.

Starting with "Understanding the Velocity of Token Circulation," the two established a fearless persona as fund managers unafraid of "anti-consensus" through a series of sharp articles. While people were enthusiastically singing the praises of Ethereum, they made a bold bet on the "Ethereum killer" EOS; however, EOS failed due to issues within the project itself. As the market celebrated Multicoin's "mistake," Multicoin did not "admit error," but instead stuck to their thesis, bearish on Ethereum's scaling speed, ultimately investing in Solana, a project that shone brightly.

Over the past five years, Multicoin's investment style has consistently been thesis-driven: a group of fervent observers of the crypto world, debating the issues of public chains day and night, deducing technological iterations and the "theoretical landscape" of the future of the crypto world, and building their investment portfolio accordingly.

Multicoin believes that once they identify a thesis, they concentrate their firepower on investing. They "look at a ten-year horizon, patiently waiting for the thesis to be validated by time; they fear missing out on an opportunity for infinite compounding growth more than entering the market too early." They work closely with the projects they invest in, playing a crucial role in the construction of the Solana ecosystem, as well as in projects like Helium and The Graph, which have prompted a reevaluation of the Web 3 model.

As of the third quarter of last year, data showed that the Gross MOIC of Multicoin's first VC fund reached an impressive 114.7 times, with a DPI of 47 times. A report from Axios at the end of last year indicated that since its inception, Multicoin's hedge fund had a return rate of approximately 203 times.

Multicoin's LP lineup includes names like Marc Andreessen (a16z), Sam Bankman-Fried (FTX), Fred Wilson (USV), and Su Zhu (Three Arrows), all of whom require little introduction.

Multicoin's culture is passionate and direct. The two founders dare to express unpopular opinions in public, especially in the tribal and intolerant discussion environment of crypto, even if they are later proven right, they still have many resentful detractors. However, this does not affect the extreme admiration from their supporters; this outsider, initially seen as a disruptor in the crypto space with Ethereum, has danced their way to becoming the king of the crypto party.

The following is the table of contents for this article; targeted reading is recommended based on key points.

01 Escape from Wall Street: Seeking New Lands

02 Building Reputation as Observers of the Crypto World, Stroke by Stroke

03 Winners Win Big, Losers Average Losers

04 Thesis-Driven Derivation Maniacs

05 "The Third Entrepreneurial Partner"

06 Investment Themes and the Future of Crypto

- Open Finance: The Grand Ideal of Financial Integration

- Web3: Reimagining the Coordination of Human Economic Activities

- Universal Public Chains: A Future Without Bridges

- Non-Sovereign Currency: Beyond the Trust-Based Economy

01 Escape from Wall Street: Seeking New Lands

Both founders of Multicoin were undergraduate students at New York University in the class of 2008, and both hoped to leave their mark on Wall Street until the financial crisis occurred, which directly influenced their trajectories as Wall Street and Silicon Valley experienced a loss and a gain. Kyle began learning entrepreneurship under his father, a computer scientist, at his electronic medical records company, VersaSuite, while Tushar also wanted to learn entrepreneurship, rejecting offers from several major PB banks and voluntarily taking a significant pay cut to work at Kyle's father's company.

A year later, the two ventured out on their own. Kyle developed a VR display device for surgeons based on Google Glass, which could record the entire interaction with patients during surgery and review past successful surgical guidance. Soon, Google killed this once-famous application, and Kyle was forced to sell his first startup. From a market opportunity perspective, he was at least ten years ahead of his time.

Tushar's first attempt was also in the healthcare field, establishing a platform called ePatientFinder for matching patient data and clinical trials. At that time, the acceptance of SaaS was not as high as it is today, and the entire sales chain, clinical trial feedback, and product cycle were too lengthy, leading Tushar to ultimately sell it to a competitor.

The first four years after graduation were not considered successful in the conventional sense; many would even think they were somewhat slow. The Bitcoin white paper by Satoshi Nakamoto, published in 2008, was not picked up by Tushar until 2013. Then Kyle "discovered" Ethereum, and the two fully immersed themselves in the crypto world, participating in numerous offline discussions about cryptocurrencies within a year, where they met a future Multicoin LP, Adam Mastrelli.

It wasn't until the spring of 2017 that they decided to establish a crypto fund together. From that point on, everything accelerated dramatically, achieving unattainable returns over five years.

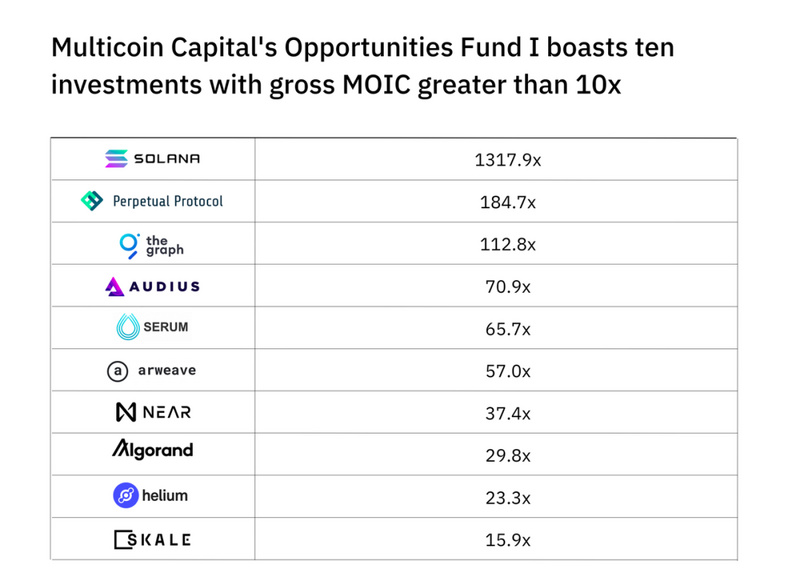

The two major projects that Multicoin heavily invested in, Helium and Solana, represent their two core beliefs: the power of decentralized organization in the physical world through Web3, and a future of universal public chains. By the second half of last year, when raising their third fund, Multicoin allocated about 11% of the two previous VC funds to Helium and 7% to Solana, both achieving returns of over ten times, with Solana's MOIC reaching an astonishing 1318 times.

As of the third quarter of 2021, an LP shared that their returns from Multicoin's first VC fund had a Gross MOIC of 114.7 times, with a DPI of 47 times. Multicoin's official figures show that the first and second VC funds achieved return rates of 33.1x and 3.6x, respectively.

Founder Kyle often mentions in interviews that 'Timing is a bitch,' believing that timing investments in the crypto field is nearly impossible, and thus he had to detach himself from the obsession with timing, "winning ten years later."

Multicoin's first VC fund was only $17 million, and after achieving impressive results, the second and third funds were still very restrained, raising only $100 million and $250 million, respectively. Now, with approximately $4.5 billion AUM including the hedge fund, Multicoin, with a team of just over a dozen people, continues to focus on finding the top 1% of entrepreneurs, always maintaining the mindset of "we are still at the forefront of this wave." If you carefully observe their public appearances, you may notice that when answering tricky questions about the future of crypto, they often seem a bit spaced out, gazing into the distance, as if that is where all great things happen.

02 Building Reputation as Observers of the Crypto World, Stroke by Stroke

2017 is regarded by many as the inaugural year of the crypto field, with the ICO bubble being unparalleled at the time. Tushar cited examples where even absurd concepts like Dentacoin could gather a following in the market—Dentacoin aimed to provide token rewards for those with high dental hygiene to disrupt the dental industry, sparking a wave of public discourse, claiming these tokens could serve as "general equivalents" for purchasing goods.

The phenomenon of short-term quick bursts and rapid listings deprived long-term investments of survival space. At that time, very few institutional investors paid attention to the crypto field, and capital movements were very discreet. Influential players like Polychain and MetaStable never shared any market insights in public, let alone advocate for a more rational value investment approach.

The crypto world of 2017 needed a Benjamin Graham [Note: "Father of Value Investing," author of "The Intelligent Investor"]. Kyle and Tushar found a vacuum and began to speak out.

Neither of them had impressive resumes related to crypto, and their greatest weapon for attracting attention and building their brand was writing. At the outset, Kyle's article "Understanding the Velocity of Token Circulation" was wildly shared within the crypto community. To this day, Multicoin can be considered one of the loudest investment teams in the crypto world.

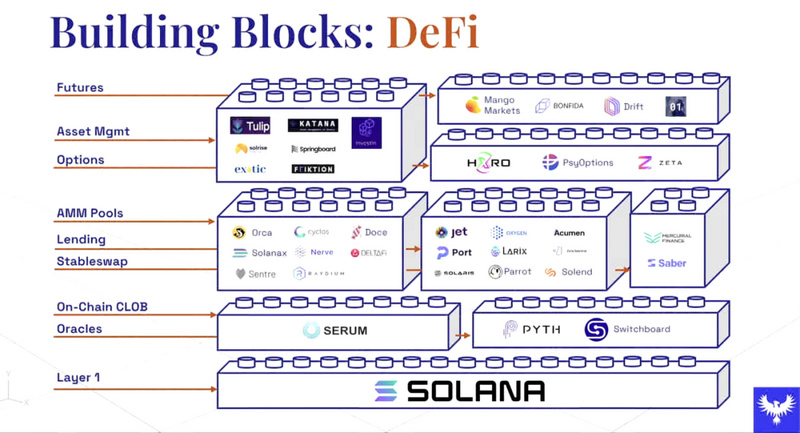

For instance, one of the concepts Multicoin has written about the most recently is composability, which refers to the ability to continuously build new modules on a platform and program them into higher-level applications. Multicoin believes the time to build a "crypto version of Lego" has matured, allowing users to combine foundational protocols in various ways. While arguing for composability, Kyle has repeatedly supported the argument that the answer to public chain scaling cannot be "sharding."

Take DeFi as an example: based on the same "Lego base" (underlying order book), decentralized spot trading Serum and futures exchange Mango Markets can simultaneously go long on spot and short on contracts based on an "incremental neutral" strategy, creating a stablecoin UXD through fully collateralized methods; on a high-performance universal public chain, lending protocols, digital asset custody, options trading, and even hedging tools can be integrated, which would be impossible in a fragmented multi-chain state: delays in information loading between systems, technical complexities of development, and coordination costs, as well as the fragility of cross-chain applications, would all disrupt the operation of this Lego world.

The two founders are keen to share how they view the potential application processes and technological paths in the crypto world, often referencing previous assertions in articles announcing an investment, as if conducting a social experiment with timestamps. Tushar mentioned in an interview with Capital Allocators:

We are accustomed to putting our insights on paper and publishing them online because people in the crypto world, especially on Twitter, love to poke holes in your arguments, forcing you to debate repeatedly, thus constantly refining and validating your position.

Initially, Multicoin's fundraising did not go smoothly; many institutional investors were skeptical about crypto, and some large LP managers were reluctant to take on risks, preferring to invest in established funds like Sequoia or even Paradigm, which had established social connections. However, as Kyle and Tushar's writing became more prolific and their influence grew, many investors began to take notice of them.

Throughout 2018, Multicoin secured a number of heavyweight LPs: Marc Andreessen, Chris Dixon, and David Sacks (the first two being key figures at a16z, and David being the former COO of PayPal and founder of Craft Ventures). Fred Wilson of Union Square Ventures even stated that his reason for investing was that the two founders "aren't afraid to make mistakes in public."

Of course, Multicoin's frankness also attracted a lot of fire. They initially held a firm bearish view on Ethereum, which led them to invest in EOS, the once-famous "Ethereum killer," a blockchain attempting to provide a high-speed alternative. This was seen by many Ethereum supporters as a direct challenge to Ethereum.

Multicoin is unafraid to publicly criticize projects they believe are overvalued (such as Ripple) and express their views on projects like Ethereum and Litecoin, which have substantial community support. This critical thinking and willingness to voice anti-consensus opinions have become a distinctive banner for Multicoin.

03 Winners Win Big, Losers Average Losers

Due to the rapid listing of projects in the cryptocurrency market, Multicoin initially only had a hedge fund chasing good ICO projects. Starting in 2018, people no longer viewed cryptocurrencies as a fleeting trend; they began to pursue lasting influence and opened up private token issuances early on.

Multicoin quickly established a specialized venture capital fund. This crossover fund model provided Multicoin with significant discretion: early investments in good projects, close collaboration with entrepreneurs, and if they had strong convictions about a project, they could hold it longer through secondary tools.

The assumption behind Multicoin's investment decisions is to invest in projects they believe they can hold for ten years. This is the so-called ability for continuous long-term, compound growth, akin to Tiger's long-standing strategy of "Long the internet" from ten years ago.

Multicoin hopes that the thesis derived from repeated debates will fully play out, capturing the strongest returns at the end of the cycle, which requires firm belief and ample patience. This is why during the crypto winter of 2018 and the Black Thursday of March 2020, Multicoin steadfastly held large positions in Solana and Helium (at that time, these teams were actually struggling to keep up).

When the crypto market was retreating, Multicoin even doubled down on several large positions, including Solana, and made a "counter-cyclical" investment in decentralized music streaming service Audius, along with later investments in Livepeer and Braintrust, becoming important cases under the theme of "web3 digital sovereignty and application logic." (We will elaborate on investment themes in the latter part of this article.)

At the lowest point, Multicoin made the decision to stop trading, holding firm to their bets, and in 2018, despite EOS's disastrous failure, they still outperformed Bitcoin and Bitwise 10 (a significant index fund in the crypto circle) by a large margin. This was a decisive turning point for Multicoin: from then on, they no longer obsessed over so-called "market timing," focusing more on the size of the opportunity and value capture—as Tushar said, "We realized you can never predict black swan events; standing in January 2020, you cannot accurately predict what will happen in March. We decided to stick to our strengths: thesis-driven asset selection."

Before introducing their thesis-driven strategy in the next chapter, let's take an example: after Multicoin's bold bet on EOS fell through, those "Ethereum centrists" were gloating. However, the two founders did not retract their previous thoughts on Ethereum's issues: Ethereum's scaling route was constantly changing, yet it lacked sufficient speed in delivery, and many elder genius developers in the community had left. Co-founder Gavin Wood had already shifted to a new project, Polkadot, while Vitalik's slow pace made Ethereum's congestion and low throughput obscure any promising future.

They recognized that EOS's failure was due to its resource allocation model and other factors, not because their thesis was wrong. They quickly figured out why they bet on the wrong horse and maintained their original thesis, eventually investing in Solana, a project that yielded thousandfold returns in their search for an "Ethereum challenger."

Multicoin does not wish to cast a wide net but aims to catch the biggest fish, investing their entire fortune to capture it. When asked about Layer 2 and the recently favored zero-knowledge proof rollups, Kyle candidly stated, "It's not something we do; we don't pile into this trade," admitting that their bet on Starkware had an element of luck. Starkware was a joint investment they made with top funds like Paradigm and Sequoia, and Multicoin did not repeatedly elaborate on the investment logic or continue to systematically layout Layer 2. These actions honestly reflect their level of belief and endorsement in this field. This focused investment philosophy is also why Multicoin has a few star projects driving significant excess profits.

The two founders unanimously believe that Multicoin is more risk-tolerant than its peers, being one of the few crypto funds that "abandon" managing volatility while managing risk qualitatively. Paul Tudor Jones's "Losers Average Losers" is their creed; interestingly, this big shot entered the Bitcoin market early and publicly stated on CNBC that it is a more inflation-resistant asset than gold, marking a significant figure in traditional finance's gradual acceptance of crypto.

04 Thesis-Driven Derivation Maniacs

Thesis-driven sounds easy but is hard to execute. Opportunists reactively and acceptingly evaluate the new things emerging in the world; Tushar bluntly stated that it's no different from swiping on Tinder. True thesis-driven investors first form predictive viewpoints, much like the public roadmaps many Web 3 projects now share, revealing their entire "brainwave."

To put it extremely, Multicoin's primary mission is not to invest in good projects but to form good investment theories. They recalibrate the "ought" of the Web 3 world using pure first principles; once they identify an element that will occupy a significant strategic position in the future, they go all in to "bet." Although the two founders like to use the term "bet," the theoretical construction behind it is as precise as a surgical operation.

Tushar published "Trade-offs in the Decentralized FTX Space," proposing the concept of "decentralized FTX," and only four months later did they find their desired project, Perpetual Protocol, valuing its deep liquidity and high leverage; Kyle's repeated assertions about "regaining our digital sovereignty stored with tech giants" led to investments in projects like Audius and Project Galaxy, which directly hand over their "IP" to end users.

In their investment decision meetings, they spend 80% to 90% of their time discussing the market, debating existing problems, possible models, flaws in existing models, and future technological innovations using first principles, "ensuring that what can be distinguished is distinguished, so they know what they are underwriting and what value they can create."

Just as they intentionally provoke discussions by continuously expressing opinions in public, investment decision meetings serve as a venue to expose any ill-considered or unsound logical deductions. This "habitual, constructive opposition" has become Multicoin's most relied-upon communication method, efficient and in-depth. "After leaving the meeting, we either solidify our previous ideas or can overturn them and start building an entirely new theory."

Interestingly, in the first ten minutes of their IC meetings, they silently comment on memos on their computers to make discussions more flat, allowing everyone to think independently without any preconceptions before gathering to discuss.

Multicoin has a fairly balanced team. Kyle is passionate (his writing reflects his personality), while Tushar is calm; their roles are thesis establishment and portfolio management, respectively. Kyle speaks rapidly, exhibiting a typical debate personality. Although he offended some insiders by publicly criticizing certain projects early on, it is evident that he has thought deeply about "our sovereignty in the digital world." Tushar, on the other hand, is relatively mild, speaking logically while often gazing into the distance, frequently stating, "We're missionaries, not mercenaries," believing that crypto technology can broaden the horizons of human technology to achieve greater freedom.

Interestingly, the two founders who escaped Wall Street managed to recruit two important founding members from there: one is Brian Smith, a former analyst at Tiger Management and former VP of finance at a listed e-commerce software provider, who serves as COO and CFO. Matt Shapiro also has a banking background and quickly rose to become a partner.

Here, we must mention the addition of Mable Jiang. The opportunity arose when many criticized Binance for not being decentralized enough, and Multicoin took on the role of anti-consensus. At that time, Kyle recognized his insufficient understanding of the Asian crypto market and specifically moved to China for over a month to find an investor responsible for the Chinese market. During a meeting, he met Mable and ultimately invited her to join (Mable recently left Multicoin to become the Chief Revenue Officer at the recently popular move-to-earn project StepN). It was also due to their shared enthusiasm for Binance that FTX's Sam Bankman-Fried and the two founders hit it off. Later, Multicoin purchased FTT at $5 in the fourth quarter of 2019, which is now priced at $60.

When discussing the future profile of crypto investors, the two founders half-jokingly said, "There are lots of things to be unlearned." Indeed, traditional investors always think about setting gates and charging tolls, but this approach is entirely unsuitable in the crypto world; one must adapt to an open-source, no-gate commercial model to truly understand Web3 entrepreneurs and generate productive dialogue.

05 "The Third Entrepreneurial Partner"

Multicoin firmly believes that investors also have the ability to create alpha alongside entrepreneurial teams. From token design, on-chain governance, protocol iterations, network participation, to insights into the cryptocurrency market, and even BD and brand media relations, the Multicoin team can provide substantial assistance to the companies they invest in. Let's take their two major investments, Solana and Helium, as examples.

The founder of Solana attracted Multicoin's attention due to his "almost obsessive pursuit of blockchain performance." After their first investment in Solana in early summer 2018, Multicoin continuously acquired shares from some "faint-hearted" investors. It is worth noting that when investing in Solana, Multicoin faced similar market fears as with EOS, but that did not deter Kyle and Tushar from actively participating and promoting it.

One significant stroke of genius may have been their collaboration with Sam Bankman-Fried: establishing a decentralized exchange Serum on Solana, leveraging Solana's performance to integrate it into Serum's on-chain order book, allowing developers to more easily build scalable DeFi applications on Solana. This became an important step for Solana in establishing an increasingly broad ecosystem. Multicoin also openly mocked Uniswap across from Serum: between the order book on a high-performance chain and the AMM on a low-performance chain, Multicoin unhesitatingly supported the former, precisely because they are believers in unified chains and do not allow for low-performance compromises.

The founder of Solana views Multicoin as his "third entrepreneurial partner," becoming "the first person to think of when encountering problems," a level many VC investors aspire to reach.

Similarly, after encountering the Helium project, Tushar had countless phone discussions with founder Amir about Helium's token economics. Multicoin's initial thesis was: data is the largest commodity in the world that has not been fully financialized, and we need a more economical way to transmit data. Based on this belief, Multicoin actively participated in governance and heavily concentrated its bets on Helium, deploying over 11% of its funds, while also operating SPVs for LPs to increase their HNT holdings.

In return, the Helium team granted Multicoin preferred shares and proportionally distributed Founder's Rewards as the network expanded, almost providing Multicoin with a perpetual annuity-like income.

The Graph (aiming to become the unified search engine for Web3) founder commented that Tushar's ten-minute conversation with him at the Solana developer ecosystem conference completely changed their direction for the next three months. A fellow crypto investor described Kyle as, "He will pick fights for whoever. No fight is too big for Kyle Samani."

06 Investment Themes and the Future of Crypto

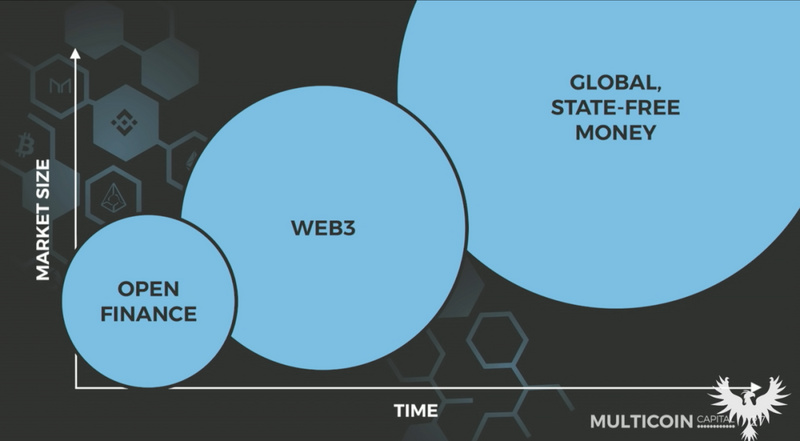

Multicoin's three major investment themes are: Open Finance, Web3, and Non-Sovereign Currency.

Open Finance: The Grand Ideal of Financial Integration

Open finance represents the grand ideal of the two founders: enabling transactions in global capital markets to occur in a mode of full trust without collateral. No intermediaries are needed, and there is no need to worry about counterparty risk; your assets can be transferred between platforms in seconds.

In a conversation with Micky Malka, founder of Ribbit Capital (an excellent fund focused on fintech), Tushar discussed where DeFi's competitive advantage lies, attributing it to consumer relationships: It's all about who owns the customer relationship. The true moat that determines DeFi's value is how many relevant parties (developers, consumers) they can attract to accumulate value.

Bitcoin itself firmly grasps consumers in the form of a social contract or value storage/appreciation, but for DeFi, people do not naturally form a sense of attachment and belonging to a specific protocol; they only want the best rates, liquidity, and experience. This is why some aggregators now disperse consumer orders across various DeFi venues to obtain the best configurations, resulting in better relationships with consumers.

Micky used a vivid analogy: in his hometown in Venezuela, there might only be one barbershop and one hotel, but there are always two or three banks, competing based on interest rates and various minor service differences. Financial services have always been a highly commoditized industry; nothing is uncopyable, but how to win? It relies on branding. To have consumer relationships, perhaps DeFi needs to follow the old path of traditional finance to pursue brand effects, exploring the core characteristics of brands that can ultimately gain consumer trust. Until then, situations like Sushiswap's replication (fork) or tweaks of Uniswap will not change.

Looking ahead, Kyle provided a corresponding analogy to traditional finance: there will be a "DeFi-native" "prime brokerage" to support blockchain versions of perpetual swap contracts—where you can freely exchange between cryptocurrencies and fiat currencies and purchase financial products from around the world. In the future, traditional finance and DeFi will coexist, but DeFi's clearly lower transaction costs will undoubtedly attract more people to shift.

Of course, the future of DeFi will not be a smooth path. The EU Commission has issued regulations imposing extremely high capital requirements on asset-backed stablecoins and has prohibited interest-bearing tokens. This is also a bear case that Multicoin has considered: if deemed a threat to their sovereignty by the government, they could only trade in the gray market afterward. Additionally, the "next investors" in the crypto world will have even less understanding of financial concepts, so trading in more complex ways (adding derivatives, digital asset management, etc.) will face some resistance.

Web3: Reimagining the Coordination of Human Economic Activities

Multicoin's Web 3 theme can be summarized in one sentence: a network that allows people to coordinate economic activities more freely and efficiently without trust, essentially extending the logic of DeFi to all aspects beyond finance.

Specifically, many activities in modern society rely on a centralized entity to allocate resources: AWS for storage, AT&T for communication, Google for queries. Behind this are high transaction costs and severe centralization risks (data privacy, single points of failure, etc.).

Some projects attempt to decentralize these, deconstructing the infrastructure we once took for granted into the smallest units of value, allowing each Web3.0 resident to monetize resources that were previously impossible to monetize: social networks (SocialFi), hard drives (Arweave), network bandwidth (Helium), and even attention (Brave).

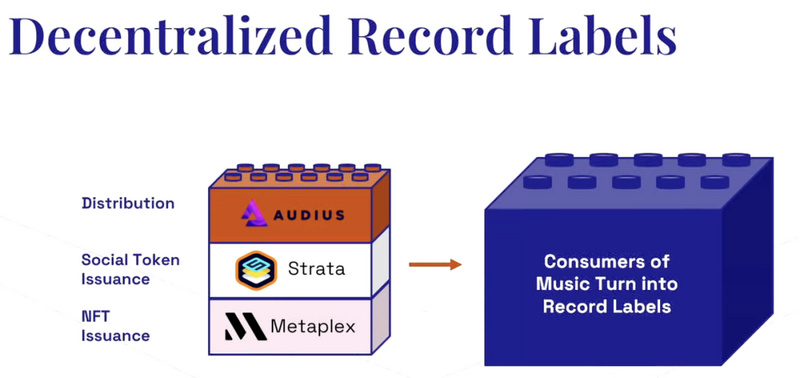

Among these is a very interesting subtopic: the Web3 sharing economy, under which Multicoin has invested in projects like Helium, The Graph, Arweave, RNDR, and Audius.

Helium's background is that with the proliferation of IoT and 5G, the demand for network speed and layout is increasing, making the traditional communication model, which is centralized and capital-intensive, unsustainable. Therefore, Helium established a decentralized communication network using shared bandwidth.

The Graph aims to become the unified search engine for Web 3, making blockchain data universally accessible and usable, allowing Dapps to operate without relying on centralized service providers.

Arweave not only disrupts AWS but also solves the problem of not being able to store all data on-chain due to Ethereum's scalability limitations, utilizing a distributed permanent storage network of shared idle hard drives.

RNDR emerged from the enormous and complex graphic rendering demands brought about by the metaverse, creating a distributed GPU computing rendering network.

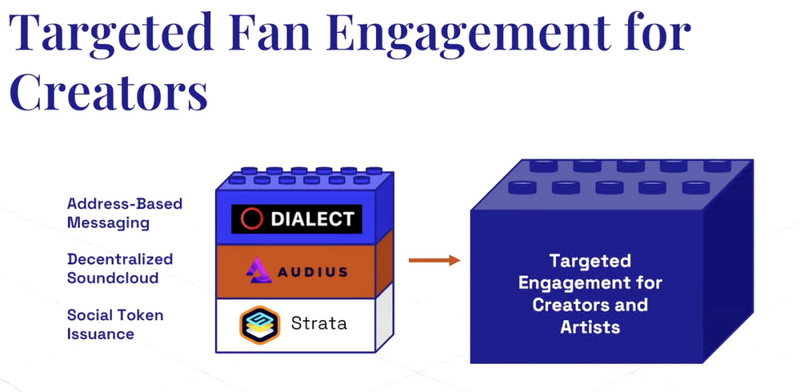

Audius returns control, copyright, and revenue rights of music to musicians, removing intermediaries between musicians and fans, which could redefine IP and fan economies:

In this way, without centralized entities mediating, network participants contribute their digital resources (including computing power, bandwidth, etc.) to complete tasks for a specific mission-driven Web3 economy (Arweave storage economy, Helium communication economy) and receive token rewards corresponding to their resources, sharing in the value while co-constructing the vision of that economy.

Universal Public Chains: A Future Without Bridges

This section represents Multicoin's predictions for the future of crypto, which inevitably includes elements of reinforcing previously made bets and passionately promoting them, but the arguments of the two founders are indeed worth sharing.

From a feasibility perspective, Tushar used an analogy to describe the historical role of cross-chain bridges: in the 1990s, technicians focused on how to connect everyone's intranets with bridges to weave a network until the concept of the internet emerged, leading people to realize they could use a single global network. Similarly, cross-chain bridges are a transitional form; once a complex application layer is added, friction between systems becomes difficult to manage, and in the long run, cross-chain bridges are expected to gradually phase out.

Kyle added a point from the perspective of efficiency: cross-chain bridges increase latency, create barriers to value and data migration, and gas consumption, and the application layer's requirements for system consistency and interoperability may be very high. Currently, we do not know what should be placed on the same layer, but generally speaking, having only one shard is the best. This is why he believes there won't be niche public chains, such as gaming public chains or DeFi public chains, as the demand for cross-chain bridges would be too great.

Thus, Multicoin does not believe in the co-prosperity of multiple chains, asserting that in the next year or two, there may be a multi-chain world, but over a longer time frame, it should shrink to 2-3 universal public chains. Public chains will gradually be filtered, and a turning point may occur when internet giants choose one chain to build applications on. A dual oligopoly is their base case for public chains, just as mobile OSs are dual oligopolies due to inherent economies of scale and agglomeration effects.

Non-Sovereign Digital Currency: Beyond the Trust-Based Economy

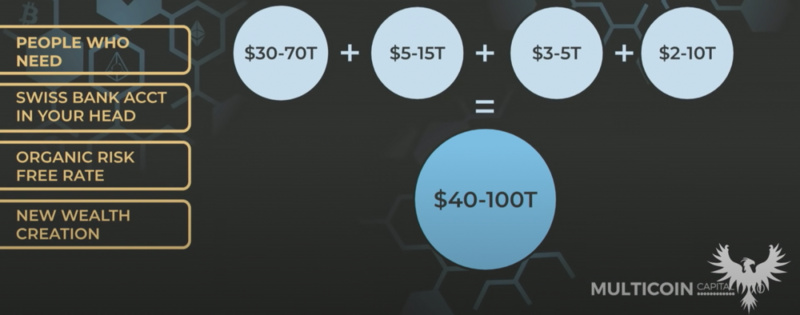

At Multicoin's 2019 summit, Kyle mentioned that the stability of fiat currency relies on a powerful national government, but there are 500 million people living in societies with inflation rates exceeding 10%. For these individuals, if they do not find a way to preserve their assets, their net worth will decrease by at least 10% each year. Digital currencies could serve as digital gold, helping them preserve their assets.

He also believes that from the perspective of asset appreciation, digital currencies are a highly market-expansive way of capitalizing (people can seek returns through staking, etc.); finally, a significant portion of the wealth created in the crypto world still needs to be digested within that world (for example, purchasing NFTs, social tokens, etc.).

Multicoin believes that these four points together represent a market size of $40-100 trillion USD. These are the futures they see for crypto.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles