Five Minutes to Understand GMX: The Leading Derivatives Protocol in the Arbitrum Ecosystem

Overview of GMX features, token model, and new proposals to maintain system perpetual settlement and long-short balance.

Overview of GMX features, token model, and new proposals to maintain system perpetual settlement and long-short balance.Written by: Karen, ForesightNews

In the article "Overview of Hundreds of Ecosystem Projects on Arbitrum: Comprehensive Development in Cross-Chain, DeFi, Infrastructure, and NFTs", we summarize the performance of the Arbitrum network and several projects within its ecosystem, among which GMX, as the project with the second-highest locked value after SushiSwap, is the largest decentralized spot and derivatives protocol in the Arbitrum ecosystem.

What is GMX?

GMX was renamed from Gambit, originally on the BNB Chain, and launched its public version on Arbitrum in the third quarter of last year, integrating the Avalanche network in January this year, allowing up to 30x leverage.

Trading on GMX is supported by a multi-asset pool, which earns liquidity provider fees through market making, exchange fees, and leveraged trading, with prices supported by Chainlink oracles and aggregated prices from major exchanges.

GMX supports using ETH, WETH, BTC, LINK, UNI, USDC, USDT, DAI, FRAX, and MIM as collateral to short or long ETH, BTC, LINK, and UNI on Arbitrum, while offering AVAX, BTC, and ETH contracts on Avalanche. The supported collateral types include AVAX, WAVAX, ETH, BTC, USDC, and MIM. Of course, GMX also provides features such as stop-loss and take-profit.

Currently, the trading fee for opening and closing positions on GMX is 0.1%, which is somewhat higher than mainstream centralized exchanges. Additionally, there is a borrowing fee paid to counterparties, deducted at the start of each hour, with the fee varying based on utilization, calculated as: borrowed assets / total assets in the pool * 0.01%. In terms of liquidation, if the value of the collateral minus losses and loan fees falls below 1% of the position size, it will be automatically liquidated.

According to the official website, since September last year, GMX has generated over $38 million in fees on Arbitrum, with a trading volume exceeding $28.8 billion; in the four months since supporting the Avalanche network, the trading volume reached nearly $9 billion, with total fee revenue exceeding $12 million.

Data on GMX on Arbitrum

Data on GMX on Avalanche

GMX Token Model

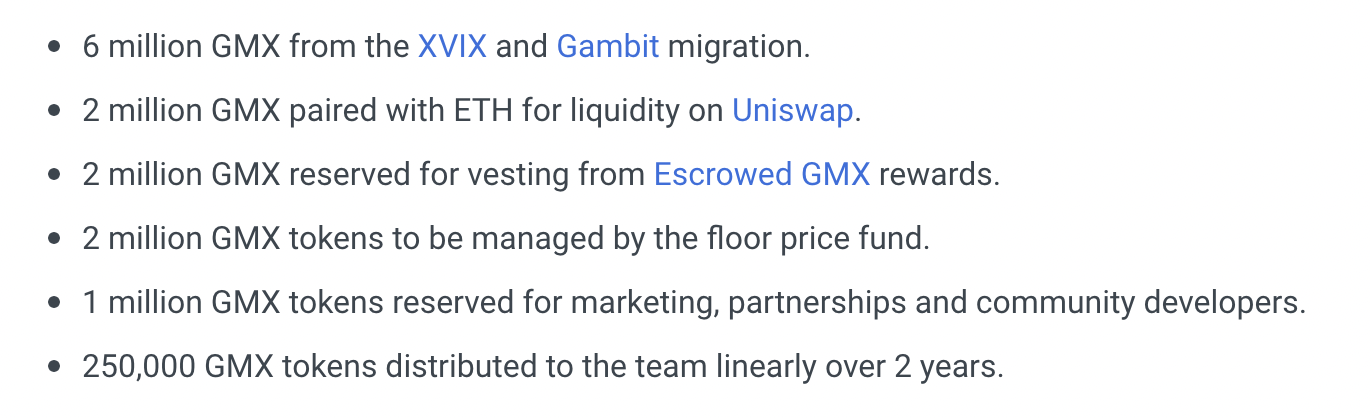

GMX has launched the utility and governance token GMX, with a maximum supply expected to be 13.25 million GMX tokens. Among these, 6 million were migrated from XVIX and Gambit, 2 million are used as Escrowed GMX (esGMX) rewards for GMX staking (released over 365 days after vesting), 2 million are managed by the Floor Price Fund, and 1 million are allocated for marketing, partnerships, and community developers, with 250,000 allocated to the team, which will be released linearly over two years.

GMX Token Distribution Model

GMX stakers can earn 30% of platform fees and esGMX as well as Multiplier Points, where 30% of platform fees generated from swaps and leveraged trading will be converted to ETH (on Arbitrum) or AVAX (on Avalanche) and distributed to stakers.

Additionally, liquidity provider tokens GLP on GMX can also be staked, and GLP stakers can earn esGMX rewards and 70% of platform fees. Similar to GMX stakers, platform fee rewards will also be converted to ETH (on Arbitrum) or AVAX (on Avalanche) rewards.

Moreover, to ensure the liquidity of GLP and provide reliable ETH reward streams for staked GMX, there is a Floor Price Fund in both ETH and GLP. The growth of the Floor Price Fund occurs in two ways: through GMX/ETH liquidity provided and owned by the protocol, where the fees from this trading pair will be converted to GLP and deposited into the Floor Price Fund; additionally, 50% of the funds received through Olympus bonds will be deposited into the Floor Price Fund, with the other 50% allocated for marketing.

According to the documentation, as the size of the Floor Price Fund continues to grow, if the Floor Price Fund / total supply of GMX falls below the market price, GMX will buy back and burn some GMX.

GMX Protocol-Controlled Trading X4 Proposal

Recently, GMX also proposed the Protocol-Controlled Trading X4 proposal, suggesting the construction of an AMM that allows pool creators and projects to have complete control over the pool's functions, meaning pool creators can specify any custom activities. Additionally, there may be dynamic fees, support for all tokens, higher composability, aggregation, GMX Swap, and the proposal to create a PvP AMM that matches traders against each other while allowing liquidity providers to participate.

In general AMMs within derivatives protocols, if the total profit and loss is negative or tending towards zero, the system is solvent, but if the total profit and loss is positive, the protocol becomes unprofitable. Therefore, GMX proposes to introduce an intermediate token GD in the PvP AMM system, which will be minted upon opening a position after depositing collateral, while GD will remain in the pool. When the index asset experiences price changes and users close their positions, the number of GD tokens held by individual users will be proportional to their profit and loss. The real-time price of the GD token depends on the total amount of collateral tokens held by the pool and the total amount of GD tokens, calculated as: total collateral tokens / total GD tokens. Here is an example provided by GMX:

- Alice opens a $10,000 long position on ETH, deposits 1,000 USDC as collateral, mints 1,000 GD tokens, and keeps GD in the pool;

- Bob opens a $20,000 short position on ETH, deposits 2,000 USDC as collateral, mints 2,000 GD tokens, and keeps them in the pool;

- The pool now holds a total of 3,000 USDC and 3,000 GD, with the price of 1 GD currently at 1 USDC;

- If the price of ETH rises by 5%, both Alice and Bob close their positions, Alice now has 1,500 GD, while Bob has 1,000 GD;

- The pool still has 3,000 USDC and 2,500 GD, so the price of 1 GD token is now 1.20 USDC.

- In this case, Alice makes a profit of 800 USDC (instead of 500 USDC), while Bob loses 800 USDC (instead of 1,000 USDC);

- However, if the price of ETH falls by 5%, Alice will have 500 GD; while Bob will have 3,000 GD. In this case, the pool has 3,000 USDC and 3,500 GD, so the price of 1 GD is approximately 0.857. Therefore, Alice's GD tokens are worth 428.50 USDC, resulting in a loss of 571.50 USDC (instead of 500 USDC); while Bob will gain 571.50 USDC (instead of 1,000 USDC) in profit.

Theoretically, the PvP AMM system can indeed maintain permanent solvency, drive long-short balance, and allow unlimited trading liquidity, but whether users are satisfied with this asymmetry in returns and the specific matching method is also an uncertain issue. However, most fees (possibly still 70%) will be allocated to GD token holders, with the remainder continuing to be distributed to GMX stakers. Of course, this proposal is still in the discussion stage.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles