StepN: The Temptation of Struggling Against the Death Spiral

In Web2 games, many have perished for a few to succeed, and only a handful of games possess long-term viability. This pattern in Web3 may manifest directly through the rise and fall of major projects.

In Web2 games, many have perished for a few to succeed, and only a handful of games possess long-term viability. This pattern in Web3 may manifest directly through the rise and fall of major projects.Author: Coral, Liuyi Capital

A couple of days ago, an article compared StepN to a beautiful woman from Sicily, whom everyone desires, everyone wants to take advantage of, yet everyone also envies and seeks to stigmatize, making her a target of public humiliation. Objectively speaking, this metaphor is very apt for describing the GameFi ecosystem: everyone wants to reap huge profits, yet everyone harshly criticizes the games that naturally possess a Ponzi model after they collapse. When the game model is in an upward cycle, most voices praise it as an innovative mechanism; after the collapse, a group of people insists it was a Ponzi scheme from the start, trampling it down in public opinion along with players who did not escape.

But let’s not forget that this is a product created by two founders who are no strangers to operating mechanism-based games. They are very clear game operators. At the moment the model collapses, the project team extracts profits, selling at the peak of the BNB rebound, recovering hundreds of millions of dollars in profits, which changed the previous practice of repurchasing and destroying GMT.

This is an immature game. Compared to the beautiful economic models of the Web2 masterpieces we often discuss, and the "unbeatable" classic game "Fantasy Westward Journey," which has existed for 20 years without collapsing, its operation is too inexperienced, its rise too rapid, and its collapse too swift.

However, this is a very typical case of game operation, just like the previously failed stablecoin and public chain, providing a good project sample: the participants in the ecosystem can basically be divided into three categories: the project team, shoe manufacturers, and small to medium players, aside from the true runners who continue to enter the market even after the collapse. None of these three parties are innocent; they all belong to the "know the game and play the game" category, where the competition creates prosperity. This is actually the essence of mechanism-based games and also the root of their easy demise.

In Web2, a few games thrive while many others fail. This pattern may manifest directly in Web3 through the rise and fall of large projects.

For games that rely on "game mechanisms" and economic models to achieve explosive growth (which I believe is the most promising type of game in the current GameFi landscape), the death spiral hangs over them like a sword of Damocles, always looming. Many actions are taken with great confidence to prevent it from falling, but for most projects, that sword ultimately falls; the difference lies in how long they manage to hold it off.

However, the real process and interesting aspect of project operation lie in the constant struggle, wrestling, and dancing with the gravitational pull of the death spiral.

Product

When we see the StepN product, we have to say it is stunning. It is something that combines the characteristics of a sports app with GameFi, SocialFi, and Web3 Keep.

Any product that combines these elements in a slightly unexpected yet effective way has a high probability of becoming popular.

StepN initially claimed to be a sports app, and indeed, many players have reported losing several pounds over the past few months, validating this attribute in the market.

As for SocialFi, this attribute includes not only showcasing high-level shoes, similar to monkeys and luxury cars, but also the "offline running meetups" operated by the project team in various cities around the world, long-term social platform planning, and various community imaginations. This also stands up, as any mobile game can form offline groups for gaming, not to mention shoes that require physical running.

But the most important attribute is actually its GameFi aspect, which combines a Ponzi model with a casino model (blind box opening). This point was greatly underestimated in the initial discussions; the project team claimed to have hired economists from EVE (Eve Online) and there were rumors of former team members from "Fantasy Westward Journey," which the market overlooked. Of course, there were also unverified claims that "the team has former executives from FunStep."

In summary, relying on the first two validated attributes of sports app + SocialFi as a solid foundation and effective narrative, combined with the Ponzi and blind box elements that truly allow it to "thrive," is the comprehensive model of StepN.

The community has a very clever metaphor, saying that StepN is a casino located in a sports arena, filled with spectators—this really summarizes the three attributes well.

A casino located in a sports arena, filled with spectators

Sports provide a huge base and stickiness, the casino provides a way to consume in-game currency and the explosive growth of the Ponzi model, and SocialFi attributes provide a natural power of dissemination: mutual recommendations and contagion, leading to collective shoe purchases and box openings for show.

Explosion, Struggle, and Surprises

In June, the shoe prices were like the aftermath of a nuclear explosion, with various voices questioning: Did it explode too quickly?

The rapid growth in user numbers, the team making money too quickly, and the swift changes in circumstances led the project team to lose control of the project, even leading to a situation where they no longer wanted to work hard on the project after achieving financial freedom, resulting in the project collapsing… In fact, it’s not that way. If a project can become popular, there must be an explosive period, which is characterized by a simultaneous rise in volume and price, a rapid pace, and a situation where everything rises together, with potential for sudden disasters… Surprises and uncertainty about what will happen tomorrow characterize such periods.

However, if a project never experiences an explosive period, it is essentially a dud.

Even for a large project with a highly anticipated massive financing and a luxurious team, you can have high expectations, and a wave of PR can create a suspected hype upon launch, but the real data for game entry peaks immediately upon launch; the market never pays for a glamorous lineup.

In short, a game that does not explode will die; no matter how well you configure it, it’s useless. If the market does not buy in, everything is in vain. This cruel law of Web2 games still holds true in Web3.

A good GameFi project must experience explosive growth; the explosive period is a life-and-death test. Surviving the explosion is a necessary experience for a sufficiently impressive project and project team (due to the Ponzi model underlying the game project, it is not appropriate to use the term "great project" here, but it can be downgraded to "impressive").

Spending so many words on "explosive growth" is indeed due to the deep-rooted perception that projects like DeFi and public chains excel at explosive volume, while GameFi is closer to "if it rises to an unaffordable level, it becomes visually appealing," and "if it doesn't rise, no matter how good it looks, it's useless." Explosive growth and popularity are the principles; to some extent, they are more important than "good" or "bad"—for NFTs, before the explosive growth of blue-chip projects like monkeys and MoonBirds, everyone thought they were quite ugly, but after the surge, everyone’s aesthetic "caught up," believing that monkeys have a high aesthetic standard and style, while MoonBirds appear cute and valuable everywhere. The same applies to games; when a game becomes popular, you can analyze why it exploded, but if it doesn’t, there’s no need to analyze how good it is.

StepN has experienced at least two rounds of real explosive periods.

The first round was the explosion on Solana, from early March to late April, where the growth curve went from flat to steep. In just 50 days, the number of player accounts grew from 10,000 to over 10,000 daily increases, totaling from 10,000 to 300,000, achieving an explosion within the circle and initial breakout. This round was basically under control, with only a few anomalies appearing in the last few days.

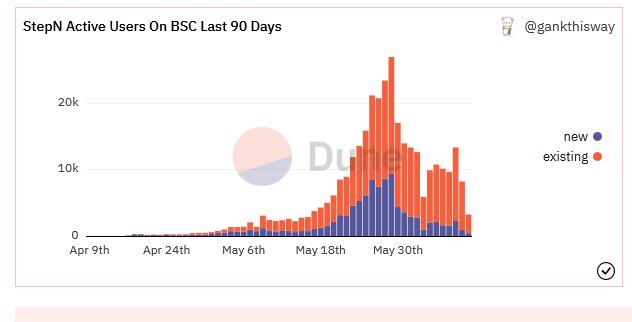

The second round was the nearly insane and highly controversial explosion on BSC, which occurred throughout May.

During this period, the most important aspect was that it actually experienced stable and controllable growth, as well as four uncontrollable explosions and an unsurprising collapse.

Most people remember that the shoe prices on the Solana chain remained stable and controlled, just like when I entered in mid-April, until the collapse of shoe prices on BSC led to a decline in June. However, that was not the case.

Although the subsequent surges on BSC left many astonished, this market force, referred to externally as "Shenzhen brothers," first revealed its sharpness on Solana and engaged with the project team. However, this brief history has been completely forgotten by most shoe enthusiasts.

At the end of April, BSC shoes had just experienced a lottery sale on BA, where the price of a co-branded shoe at 10 BNB was daunting, and most people were eagerly waiting for the price of BSC shoes to drop. At this time, the GST and shoe prices on Solana suddenly began to rise regularly.

Within three days, GST surged from below 4 to 9, and the price of a floor gray shoe, which had stabilized around 11 SOL for nearly a month, was crazily driven up to 18, accompanied by a small wave of excitement: my companions either gritted their teeth and went all in at high positions or exchanged their gray shoes for green shoes starting at 7000 USD. Then everyone kept refreshing the GST price in astonishment—each refresh saw another increase.

The project team quickly responded, announcing a triple twin event—minting once would yield two shoe boxes with a probability three times higher than usual: shoe enthusiasts said if they wanted shoes, they should get more shoes.

Soon, facing the soaring GST, they announced the listing of GST on FTX—both spot and futures, clearly using a short-selling mechanism to suppress the obviously controlled GST price, which was a clever tactic.

More importantly, they announced an airdrop of 10,000 pairs of shoes to the holders of the Genesis shoes on Solana.

After this wave of operations, the GST and shoe prices on Solana fell in response, and after a few days, they never looked back, with GST plummeting to today’s 0.6 USD.

Meanwhile, the shoes on BSC began their first wave of decline after the explosive rise, with the initial 2000 pairs of shoes crashing from a price of 38 BNB to 5 BNB, attracting the attention of most people.

No one knew that this wave of controlling GST and shoe prices had quietly shifted to BSC, quickly taking control of this nascent market.

(Note: The term "Shenzhen brothers" here refers to a group whose real existence has not been 100% verified; it is a general term representing a clearly existing market force.)

The mutual game between the Shenzhen brothers, other small shoe enthusiasts, and the project team staged several rounds of encounters between capital forces and macro control, creating several waves of explosive growth and decline in the BSC shoe market, ultimately leading to chaos.

Genesis shoe owners recall that the early Solana shoe market ecosystem was also like a live volcano, with shoe prices and GST erupting to 20, then being controlled down by the project team. After that, it remained stable, being precisely controlled below 1100 USD daily, with SOL priced around 100 USD, stabilizing around 11 SOL. Walking and minting profits were quite certain, and most people followed a regular routine to recoup their investment cycle, with profits as certain as working for gold, Work To Earn.

This was likely the reason the project team did not pay enough attention when the second round of shoe prices and GST began to rise on BSC.

Before the airdrop of 10,000 pairs on BSC, everyone expected the airdrop to bring a crash, with even big players advising in large groups of 500 people: sell now, tomorrow’s airdrop will bring cheaper and better shoes.

However, the result was that the day before the airdrop, shoe prices hit bottom and rebounded, and that mysterious market manipulator began to operate quietly. Accompanied by the airdrop and the subsequent synchronized upgrading of shoes in batches every two days, the demand for GST significantly exceeded supply, leading to a rapid increase from an already eye-catching 11 USD to 45 USD. At this point, the highest earners could reach 5000 USD a day with a set of shoes, "walking over 30,000 a day, it feels a bit embarrassing."

It is important to note that the GST on Solana and the GST on BSC are not cross-chain interoperable; they are actually two tokens with no relation in terms of supply, demand, or value.

At the same time, the floor price of gray shoes soared from the bottom of 5 BNB to 45 BNB, a ninefold increase, while players from Solana were astonished by the profits of 2000 to 3000 USD a day, wanting to exchange a Sol green shoe for a BSC gray shoe, but unfortunately, they could not.

------At this point, a premium gray Jogger could demand over 50 BNB, "100,000 RMB for a pair of shoes, are you crazy?" Sol players were very angry.

It is said that during this round, the Shenzhen brothers had already started selling, and the shoes were soaring wildly, with early entrants into BSC reaping significant profits.

At the same time, the strange feeling of selling shoes clearly indicated the presence of market manipulators: if you listed shoes at a similar floor price, several pairs slightly below your price would instantly appear in front of you; if you lowered your price, even more lower-priced shoes would emerge… until you listed your shoes at a significantly lower price than the market, and they would be sold out instantly. A shoe listed at around 60 BNB might only sell for 40 BNB. The market liquidity was weak, comparable to the stable period of the NFT image market.

When GST surged 40% to 45, the project team took action again, announcing a change in the GST and GMT ratio required for minting, changing from 200 GST to 100 GST + 100 GMT (later further modified to a dynamic ratio, such as 40 GST + 160 GMT, currently 360 GST + GMT), causing GST to plummet, and shoe prices followed suit. At their lowest, they reached 12 BNB, a clear knee-jerk reaction.

At this point, a logic truly emerged: shoe prices actually fluctuate around GST prices, and the real support for shoe prices comes from GST prices, as this is the true output and actual cost of shoes as production materials------minting and upgrading shoes require GST as the main cost, and the output of shoes is also GST . If shoes are shovels, then GST is the gold they can dig up.

This special moment was also accompanied by the major market crash in May: BNB plummeted from around 300 to a low of 210, then quickly rebounded; while SOL directly dropped from 100 over several days, then halved to 50, and continued to probe down to 30.

The dual blow of shoe prices and the local currency nearly led to a market silence.

However, one piece of data foreshadowed the later most frenzied and largest surge of shoes on BSC, as well as the reason it failed to surge again after the third round of decline, and the reason for the downward trend of shoes on SOL: the number of new entrants.

The number of new entrants on SOL rose from a few hundred to a thousand daily from January to March, to several thousand daily in April, and during the explosive wave at the end of April, it peaked at over 10,000 daily. It achieved a three-level jump in new entrants, with the last wave, driven by the Shenzhen brothers' market control and the market sentiment of small players, pushing the project across the threshold of 10,000 daily increases.

This process, which lasted half a year on SOL, was shortened to two months on BSC.

During the aforementioned two rounds, the shoes on BSC surged from 10 BNB to 38 BNB, then plummeted back to 5 BNB, surged again to 45 BNB, and then dropped to 12 BNB, with daily new entrants never exceeding 1000, hovering between 500 and 800 daily. I even speculated at one point, how much longer would it take to hatch?

I didn’t expect the explosion to come so quickly.

It took about 20 days for the daily new entrants to break 1000, but once it did, it surged at a speed of 1000+ on the first day, 2000+ on the second day, 3000+ on the third day… and 7000+ on the seventh day. Previous articles analyzed that the total new entrants were 2% daily, controlled by the project team through invitation codes, with only 2% of invitation codes issued daily, and no more than that. However, the new entrants on BSC were largely the migration of existing accounts from SOL, which required no invitation codes at all; it was entirely possible for tens of thousands of existing users to migrate over 10,000 in a day.

Accompanied by the explosive migration of new entrants and the stabilization of the overall market, shoe prices began another round of reckless surges, once again rising from 12 BNB to 35 BNB, then quickly retracing to 25 BNB, and surprisingly achieving several days of price stability at this level.

At this time, a simple screenshot of arithmetic circulated wildly online: the minting cost of a pair of shoes was about 3 BNB, while the floor price was 25 BNB, meaning a profit of about 22 BNB per pair, minting a pair every 48 hours—essentially buying two pairs of shoes, recouping the cost in 4 days, doubling in 8 days, and exponentially multiplying in a month…

In the last week of May, the entire circle was filled with such statements, but the selling pressure had already reached irretrievable data: nearly 10,000 new entrants daily, and the shoes these people purchased would return several tens of thousands of shoes to the market in just a few days, not to mention the tens of thousands of shoes already held by existing players… along with the selling pressure on GST… unless the number of new entrants reached tens of thousands daily, it simply could not withstand such selling pressure.

At this precarious moment, when players in the market were "earning tens of thousands daily with their hearts in their mouths," NFT players and DeFi players in the circle began to privately message to enter the market… some were blocked, while others disregarded the 25 BNB shoe price and jumped in to take over.

The peak of this round of frenzy was Zhu Xiaohu, a traditional capital tycoon, who posted on social media that he bought a gray Runner on BSC and stated that StepN "is not entirely a Ponzi scheme."

The shoe prices on BSC unprecedentedly remained at the enormous bubble high of 25 BNB for nearly a week.

Just as everyone was immersed in brutal joy, singing and dancing, rumors began to circulate in the market. The project team's clarifications and AMAs could not stop the shoe prices from continuously plummeting amidst rumors of "the technical team being arrested." Finally, less than three hours after a favorable AMA from the project team, at 12:30 AM, the announcement to withdraw Chinese users came.

In the following days, shoe prices plummeted below 1 BNB, dropping 98% from the peak.

The StepN project team continuously transferred tens of thousands of BNB and hundreds of thousands of SOL to various centralized exchanges for sale.

The community continued to fantasize that the project team would use the funds obtained from selling tokens to pump GST or raise shoe prices, even though days later, due to severe updates, the fact that "the technical team had issues and was in disarray" was basically accepted. The community still held expectations.

But in reality, even though the changes in the domestic technical team were shocking—this was somewhat absurd, like the core developers of Ethereum dying in a car accident, causing a halt in development—the real reason for the shoe prices diving from high levels and never recovering was still due to the mechanism: the higher the price and the more players in the market, the more new entrants and funds are needed for support.

If it could maintain a shoe price of around 1100 USD (or other prices) as it once did on Solana, along with a GST price of around 4 USD (or other prices), such stable output, stable entry, and stable consumption might allow this Ponzi-based economic model to be sustained.

But there are no "ifs." The entry of the Shenzhen brothers and the passive involvement of retail investors in the brutal joy significantly overdrawn the development speed of the game model. The project team made efforts, but when they realized they could not control the situation, they also joined in the "daily revenue of 100 million USD with 6 million USD profit" frenzy. After all, a giant like Tencent, with a market of 1.4 billion people, peaked at no more than this.

Currently, StepN has fallen into a death spiral similar to Axie: shoe prices are fluctuating downwards, GST is fluctuating downwards, and although it can be calculated that any entry point will yield a return in about 35 days (if GST prices do not continue to fall), it has become very difficult to recoup the investment at this point. It has truly transformed into a Web3 fitness annual pass: there is always an enticing return, but it is merely an incentive for health. Recouping? You can only give up on that idea from the very beginning.

Recouping incentives and loss aversion: "Always walk for 35 days to recoup"

There is no doubt that the project team originally hoped to use limited skins, burning gems, burning shoes, scroll minting, opening new Realms, and other methods (regardless of what they are, they are all means of in-game consumption and survival) to repeatedly engage in a tug-of-war with the death spiral, maintaining a basic balance, giving StepN a chance to become a game that does not collapse for 20 years like "Fantasy Westward Journey." After all, if you have worked hard to create a money printer, you certainly hope it lasts for 20 years… or at least 2 years?

It is hard to say whether the final outcome was due to a specific issue with the technical team that led to a substantial halt in updates, or whether the game data became uncontrollable due to poor management or the project team’s failure against the Shenzhen brothers. It is even harder to discern which reason led to the collapse—however, I believe entering a stage where it cannot provide stable recoup expectations for an extended period can already be considered a collapse. At the same time, the number of new entrants is showing a clear decline; during the peak, the number of new entrants on Solana reached over 15,000, while on BSC it was close to 10,000. Now, the number of new entrants on Solana has dropped to over 6,000, and on BSC it is below 1,000.

For a game that is indeed based on a Ponzi model, this has entered a very unhealthy stage, with visible growth shrinking, temporarily stepping into a spiral similar to Axie.

The number of new entrants on Solana dropped to over 6,000 on June 9

Source: https://dune.com/nguyentoan/STEPN-(GMT-GST)-Core-Metrics

On June 9, the number of new entrants on BSC fell below 1,000, only over 900

Source: https://dune.com/waterstone/fork-Stepn-Analysis-(BSC)

Undoubtedly, if they want to create a long-lasting project, they have at least temporarily failed, although there are still over 5,000 new entrants daily.

In the future, we will continue to observe the development of this still capable team. After all, no matter how angry we blame the teams of Axie and StepN, they are the only ones who created the first and second generations of popular GameFi projects.

The standards of other imitation projects are even less worth mentioning compared to these two.

Perhaps StepN will continue to slide at a low level for a while, giving Jerry and Yawn, who indeed possess theoretical and operational standards, a time window to bring their project back onto a track that could potentially achieve millions of users.

In recent days, the project team has announced that they recognize "the stability of the economic model and price is their responsibility" (in essence).

Gains and Losses

From the entire process, the project team has gone through several stages: "steady slow growth ------ controllable explosion ------ uncontrollable explosion ------ downward spiral." The data explosion can be said to be expected; if there are no surprises, the current data and development are absolutely in line with the current situation.

The unexpected factors are mainly two: first, the "Shenzhen brothers," a strong market force competing with the project team for control over the quantity and price of shoes and GST in the game; second, the sudden appearance of major issues with the technical team or updates after the announcement of the limited "Panda Skin" at the end of April and the beginning of May.

The former led to accelerated data explosion and shortened game life, while the latter meant that the project team could not deploy a large amount of "weapons" to compete for control and respond quickly to project development, only able to adjust mint parameters and hold AMAs to manage market expectations and control the game.

If we were to maintain the health of this model fundamentally, a more practical suggestion would be to use a portion of the transaction fees from selling shoes directly to burn tokens, meaning that buying shoes would also be a form of consumption, making the buying and selling itself, mainly for new players/new accounts entering the market, akin to a point card activity.

However, in the previous period, a more important operation was to find a way to bring shoe prices back to a slow rising channel, or to launch new Realms at the right pace. The goal of the former effort was to return the model to a state of fatigue before the explosive decline in new entrants, but looking at the data, it seems unlikely that the Realms on BSC and Solana will return; the most likely scenario is to open new Realms. However, from the perspective of maintaining confidence, it is crucial to maintain the basic balance of the previous two Realms and not let prices drop too quickly, because if a project loses confidence among players, its growth potential may be lost.

In terms of the technical team, which is a vital part, there is a strong need to adopt a decentralized work structure in Web3 as soon as possible. After all, Web3 does not necessarily have to operate within a company framework, and it is not suitable to do so.

As a team with strong operational ideas and a rapidly popular game project, the challenges faced by the StepN team should be considered normal market tests, whether from the Shenzhen brothers or issues with the technical team—if the game is made and truly becomes a long-lasting project, such levels of issues will arise from time to time, and only continuous improvement by the team can address them one by one.

Therefore, rather than providing them with more suggestions, it is better to encourage the team to recognize that there are still many areas needing improvement. The rapid success in April and May made it too easy for a young team to become complacent. Moving forward, whether they plan to continue adjusting and expanding the StepN project or launch another project, the most important factors are actually the team's integrity and the confidence of the outside world.

Perhaps this is what is often referred to as the moment that tests one's vision in the Chinese blockchain world.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles