Starting from the discount of stETH - Pricing, liquidity, and risks of stETH

What exactly is the stETH that Celsius holds in large quantities? Is there a risk of a death spiral for the price of stETH?

What exactly is the stETH that Celsius holds in large quantities? Is there a risk of a death spiral for the price of stETH?Author: Mushroom, IOBC Capital

Recently, rumors about the well-known lending platform Celsius being insolvent have been rampant. The asset sell-off by Celsius and other crisis-hit institutions to raise funds has led to the decoupling of stETH prices. Currently, the exchange rate of stETH to ETH on Curve is approximately 0.937. The decoupling of stETH from ETH has caused panic in the market, with concerns that stETH might follow in the footsteps of UST, falling into a death spiral.

So, what exactly is the stETH that Celsius holds in large quantities? Is there a risk of a death spiral for the price of stETH?

To clarify these issues, let's first understand the mechanism behind the creation of stETH.

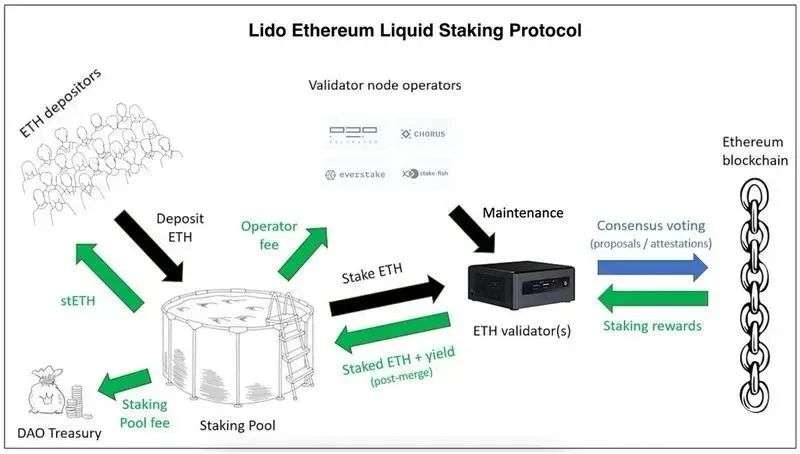

What is stETH? What is Lido?

stETH is a staking certificate generated when users stake ETH through the Lido protocol to participate in the Ethereum network's POS. Lido is a decentralized, non-custodial staking protocol.

Ethereum will complete its upgrade from POW to POS this year, and before that, a portion of staked ETH is needed to ensure the network's security, with on-chain staking earning certain staking rewards. After the network merge, this portion of ETH can be withdrawn.

For ordinary users, directly participating in POS comes with many restrictions, such as the staking quantity threshold (the Ethereum chain requires a minimum of 32 ETH to stake), the technical threshold and hardware costs of becoming a validator node, as well as the opportunity cost and lack of liquidity caused by staking lock-up (users cannot withdraw staked ETH until the Ethereum mainnet completes the merge).

To address these issues, the Lido protocol has launched a staking liquidity solution, providing users with an easy-to-operate staking service that enhances capital efficiency. Users can stake any amount of ETH in Lido to participate in Ethereum's POS process, receiving the certificate stETH and earning staking rewards (distributed in the form of stETH). After Ethereum transitions from POW to POS and completes the merge (Ethereum 2.0), stETH can be exchanged for ETH at a 1:1 ratio.

Lido's Operational Mechanism

The main roles involved in Lido are users (Depositors) and node operators (Validator node operators). Users delegate their staked assets to node operators through Lido's smart contracts.

Node operators are responsible for the actual on-chain staking work within the staking protocol, while users manage the deposit and withdrawal of staked assets and the minting or burning of staked assets through the staking pool contract.

The staking pool contract allocates assets in the pool to node operators for actual on-chain staking by verifying the node operators' addresses and keys, and is responsible for minting staking rewards into staked assets, distributing them proportionally to node operators, the Lido DAO treasury, and stakers.

Reasons for stETH Discount

Having understood the mechanism behind stETH's creation, let's look at why stETH is trading at a discount.

The main reasons for the discount of stETH are:

Compared to ETH, stETH has significantly lower liquidity, and to compensate for this liquidity cost, a discount arises;

Currently, institutions holding large amounts of stETH urgently need to sell their stETH to obtain funds to meet user withdrawals or to supplement collateral to prevent liquidation, leading to significant selling pressure, which inevitably causes further discounts on stETH;

Whether Ethereum can successfully and timely merge determines the timeline for stETH to regain ETH liquidity;

The risks associated with the Lido protocol and smart contracts.

Let's examine these points one by one.

First, the liquidity of stETH.

There are approximately 12.8 million ETH staked on Ethereum, of which about 4.1 million are staked through Lido, accounting for 32% of the total.

From the above introduction, we can see that before Ethereum 2.0 is realized, the staked ETH cannot be redeemed, and users can only pledge their stETH on certain DeFi platforms to obtain liquidity or sell stETH on the secondary market.

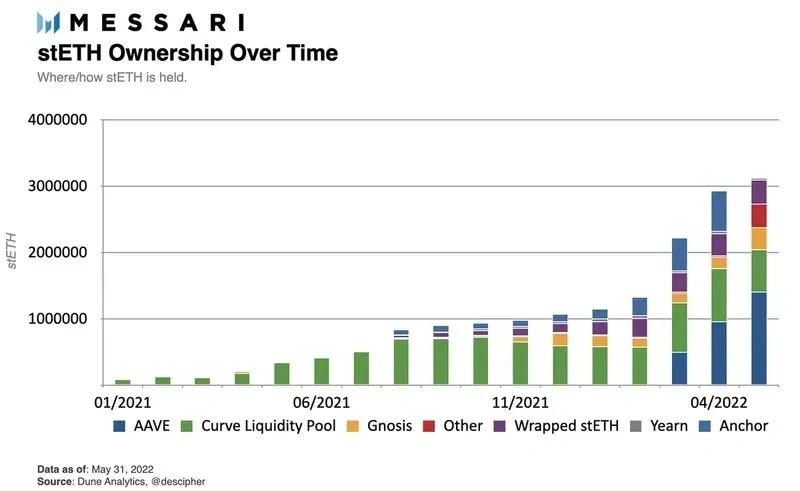

According to Messari data, as of the end of May, the circulating stETH is mainly concentrated in two protocols, Aave and Curve, which together account for two-thirds of the total circulating supply.

For stETH holders looking to sell, the decentralized exchange Curve provides a stETH-ETH liquidity pool where stakers can convert stETH into ETH. Curve's liquidity pool currently has the best depth for stETH among Dex platforms.

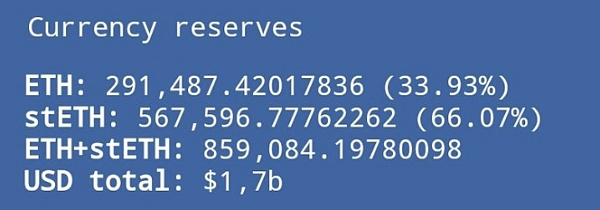

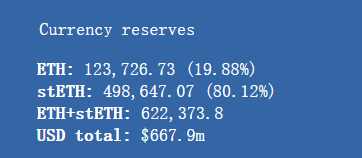

However, entering June, with the sharp decline in ETH prices, a large amount of liquidity has been withdrawn from Curve's liquidity pool, dropping from $1.7 billion on May 18 to $670 million by June 21.

At the same time, more and more stETH has been exchanged for ETH, leading to a severe imbalance in the ratio of the two assets in the pool, even reaching a stETH:ETH ratio of 80%:20%.

As of today, there are only about 120,000 ETH in the pool, meaning it can only accommodate a maximum of 120,000 stETH sell orders (equivalent to $133 million). A month ago, this number was 290,000. However, it is important to note that Celsius alone holds over 450,000 stETH in Aave. It seems unlikely that Curve's pool can absorb the market's selling demand for stETH.

May 18, 2022:

June 21, 2022:

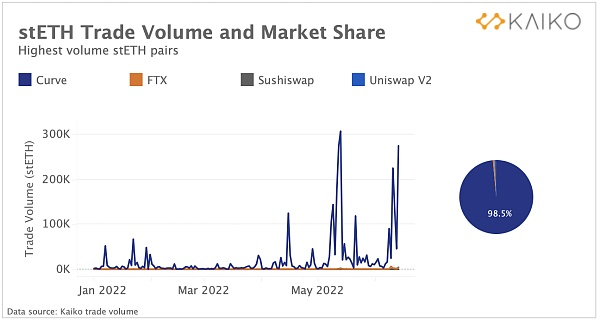

As for centralized exchanges, the trading depth is even more negligible. FTX is currently the only centralized exchange where stETH trading is available. According to data from Kaiko, in 2022, about 98.5% of stETH's trading volume occurred on Curve, with liquidity on other platforms being almost negligible.

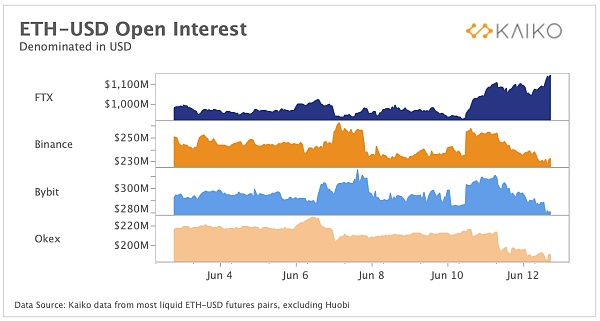

With the public market route proving unfeasible, obtaining funds through pledging has become another option. On-chain data shows that Celsius and Amber have recently sent large amounts of stETH to FTX's address.

At the same time, the number of open contracts on FTX has increased significantly, while the number of open contracts on exchanges like Binance and Okex has decreased due to market crashes leading to liquidations.

Thus, a reasonable speculation is that Celsius and Amber have pledged or sold large amounts of stETH to FTX through over-the-counter transactions, while FTX has hedged the price of this stETH through opening contracts to reduce holding risks.

After reviewing the liquidity situation in the market, let's look at the short-term supply and demand.

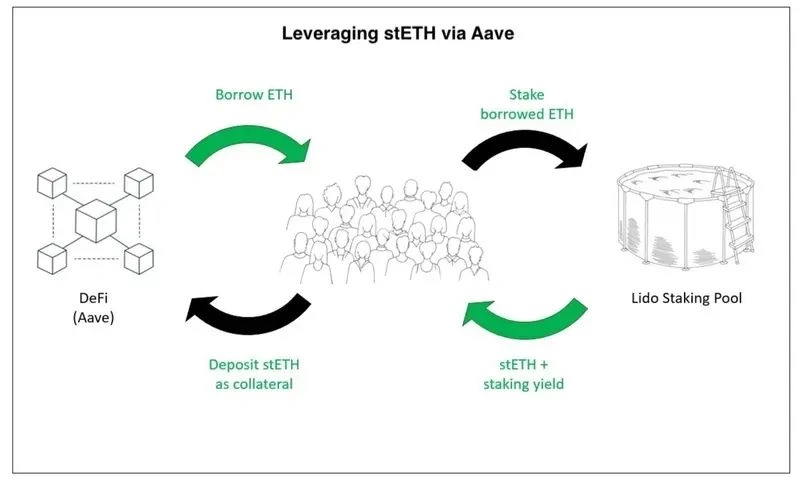

In a bull market, many institutions holding stETH choose to engage in circular staking to leverage and expand asset scale, enhancing capital efficiency. They stake stETH on platforms like Aave to obtain ETH, then stake the borrowed ETH on Lido to earn stETH. When the market is rising, this approach poses no issues, and institutions will continue to hold, keeping the exchange rate of stETH to ETH stable.

However, when a bear market arrives, this model encounters problems. The continuous decline in the value of collateral assets triggers margin calls, forcing institutions to sell their assets for cash.

A sudden influx of selling demand can create a bank run-like effect, where prices fall further with more selling, leading to negative feedback and accelerating the discount, deviating from the original pegged level.

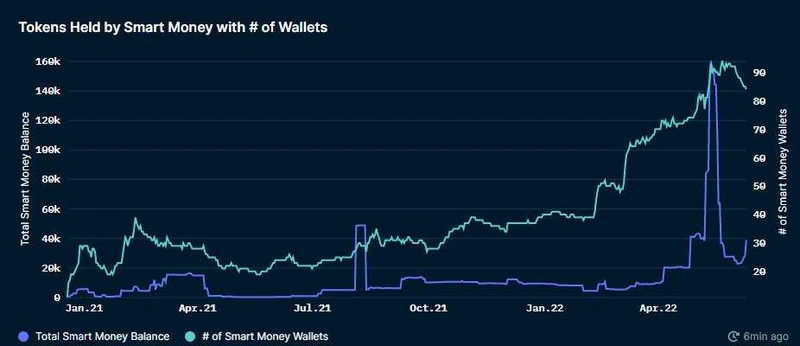

On-chain data indicates that among institutional investors holding stETH, at least Three Arrows, Alameda Research (founded by SBF), Amber, and Celsius have recently engaged in selling. Meanwhile, the amount of stETH held by smart money addresses on-chain has dropped from 160,000 to 27,800 within a month.

The accumulation of a large number of sell orders in a short time, without a corresponding increase in buy orders, has led to insufficient depth, causing the market to be overwhelmed, thus further generating discounts.

Another risk is the delay in Ethereum's merge.

stETH is a derivative of ETH. To some extent, it is similar to ETH futures, as the staked ETH can only be withdrawn at a future point in time, which is after the Ethereum network completes its merge.

If the network merge is delayed, it means that the withdrawal of ETH will also be postponed, further deteriorating liquidity and causing the price of stETH to drop even lower.

The final risk comes from the Lido smart contracts themselves.

The Lido protocol involves several main contracts, including node operator registration contracts, staking pool contracts, and Lido Oracle, which control processes such as node admission, staking asset deposits and withdrawals, and staking pool balance calculations. The security of these contracts undoubtedly affects the safety of users' staked assets. To compensate for this risk, stETH will also incur some discount.

In summary, the combination of poor liquidity, insufficient buying pressure, high and urgent selling demand, along with the uncertainty of the Ethereum network upgrade and the risks associated with Lido protocol smart contracts, makes it unsurprising that stETH is trading at a discount.

So, the final question is, will the price of stETH fall into a death spiral?

The author believes it will not. From the mechanism of stETH, it can be seen that its value source differs from the design of the dual-token system of UST and LUNA, where the decline of Luna drives the decline of UST, creating negative feedback. UST, as a stablecoin, fundamentally lacks sufficient collateral to support its value.

However, stETH has strong value support; after the Ethereum merge, one stETH can be exchanged for one ETH. This fundamentally guarantees the value of stETH, distinguishing it from stablecoins with insufficient collateral.

Although in the short term, due to the lack of liquidity, the prices of stETH and ETH have decoupled, for long-term ETH-based investors who do not urgently need funds, purchasing discounted stETH and holding it until ETH unlocks is quite advantageous.

Therefore, when the discount reaches a certain level, it will inevitably attract arbitrageurs to enter the market, restoring balance between buy and sell orders. Once the deleveraging process is completed and speculative players are eliminated, stETH will return to the hands of long-term investors, and its price is expected to return to the right track.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles