Success and failure are both arbitrage; how did Grayscale's GBTC "trap" institutions like Three Arrows Capital and BlockFi?

Success and failure are both arbitrage; the stars dancing on leverage ultimately fall due to leverage, while BTC remains the same BTC.

Success and failure are both arbitrage; the stars dancing on leverage ultimately fall due to leverage, while BTC remains the same BTC.Written by: Deep Tide TechFlow

The bear market is the rest note of the liquidity symphony.

Famous investor Charlie Munger once said, "There are three ways to go broke: liquor, ladies, and leverage."

For Charlie Munger, who is accustomed to the cycles of the market, he has witnessed the power of leverage. However, newcomers in the crypto market, such as BlockFi and Three Arrows Capital, have gradually met their own end after the chaotic expansion of liquidity during the bull market.

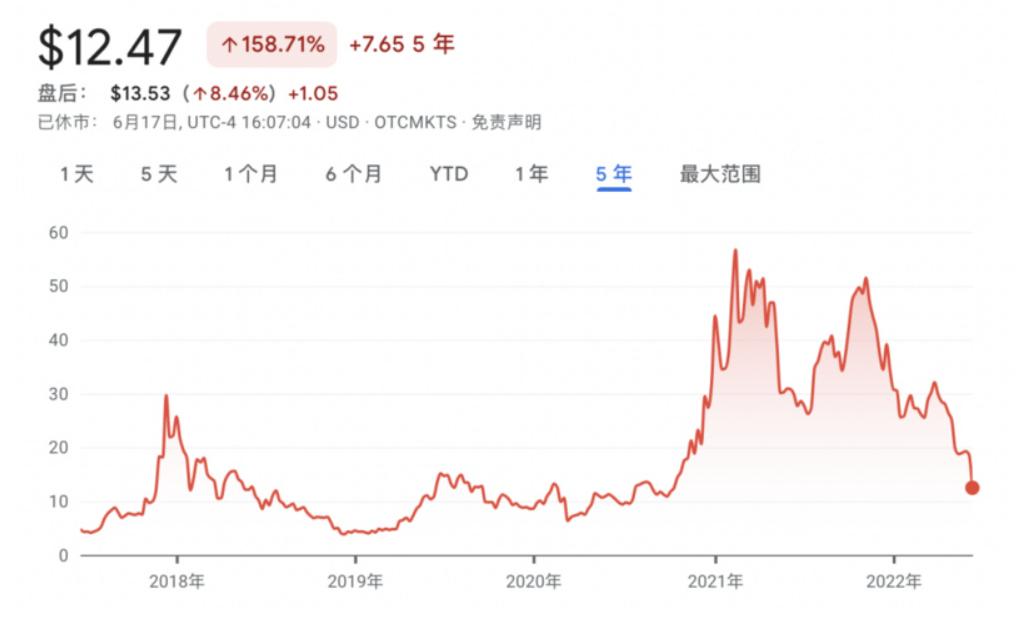

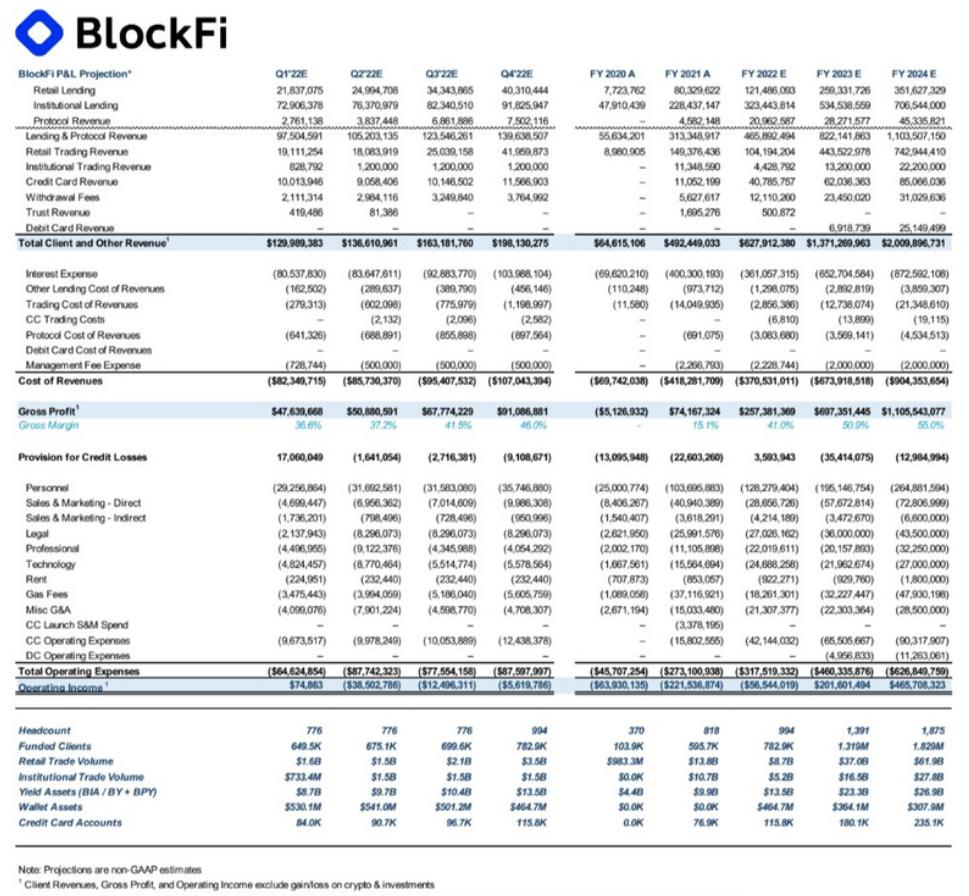

When we look back at the "crypto disaster," whether it was the once top-tier VC Three Arrows Capital or BlockFi, which was once valued at $3 billion, both stumbled over the grayscale Bitcoin Trust fund GBTC issued by Grayscale.

Once the engine of the bull market, it has now become the "barrel of oil" that caused many institutions to explode. How did all this happen?

GBTC, the Bull Market Arbitrage Machine

GBTC, short for Grayscale Bitcoin Trust, was launched by Grayscale. Grayscale is a digital asset management company established by Digital Currency Group in 2013.

The launch of GBTC aimed to help high-net-worth investors in the U.S. invest in Bitcoin within the bounds of local law, much like purchasing a fund, but in reality, Grayscale Bitcoin Trust is more like a "castrated ETF fund."

According to normal logic, investors in the primary issuance market can use their BTC to subscribe for GBTC shares and can redeem BTC through the corresponding GBTC. However, since October 28, 2014, Grayscale Bitcoin Trust has suspended its redemption mechanism.

Additionally, after GBTC is issued in the primary market, it undergoes a 6-month lock-up period before it can be traded in the secondary market.

Against the macro backdrop of massive liquidity during the COVID-19 pandemic, the crypto market became a coveted asset in the eyes of institutions. Due to positive expectations for future Bitcoin price growth, GBTC remained at a premium for a long time during 2020-2021. This meant that if investors wanted to purchase 1 BTC represented by 1,000 shares of GBTC, they would have to pay a higher price than buying 1 BTC directly.

So, why would investors choose to buy GBTC at a premium instead of actually holding BTC?

In the secondary market, the main holders of GBTC are qualified individual and institutional investors. Most retail investors can directly purchase GBTC through their 401(k) accounts (U.S. retirement benefit plans) without paying capital gains tax. Therefore, as long as the GBTC premium remains within an acceptable range for retail investors, they can profit by avoiding tax through the interest rate spread.

Moreover, some traditional institutions, due to regulatory reasons, are unable to buy and hold Bitcoin, and similarly use GBTC for related cryptocurrency investments.

There are also speculations that Grayscale artificially promoted the creation of a premium to attract more investors. Just like the classic scene in the movie "The Wolf of Wall Street," if we want consumers to buy a pen from us, creating demand is the best way, and the premium is the "demand," i.e., the investors' pursuit of profit.

For crypto institutions, the premium represents a stable arbitrage method—buy BTC, deposit it in Grayscale, and sell it at a higher price to retail and institutional investors in the secondary market after the GBTC lock-up period ends.

This was also one of the main drivers of BTC's rise in the second half of 2020. As the available spot BTC for purchase continued to decrease, the price of BTC naturally rose, and American investors were more motivated to invest in GBTC, which is why GBTC maintained a long-term premium.

GBTC and Its Misfortunate Institutions

The GBTC arbitrage was well-known to BlockFi and Three Arrows Capital.

According to previously disclosed SEC Form 13F documents from Grayscale, the holdings of GBTC by just BlockFi and Three Arrows Capital once accounted for 11% (the institutional holding ratio did not exceed 20% of the total circulation).

This was one of the leverage methods for the newcomers—using users' BTC for arbitrage, locking BTC into Grayscale, which is a one-way street.

For example, BlockFi previously attracted BTC from investors at a 5% interest rate. According to normal business models, it needed to lend it out at a higher interest rate, but the actual demand for Bitcoin loans was not high, leading to low capital utilization.

Therefore, BlockFi chose a seemingly safe "arbitrage path," converting BTC into GBTC, sacrificing liquidity for arbitrage opportunities.

With this method, BlockFi once became the largest holder of GBTC, later surpassed by another misfortunate institution, Three Arrows Capital (3AC).

Public information shows that by the end of 2020, 3AC held 6.1% of GBTC shares, maintaining its position as the largest holder. At that time, the trading price of BTC was $27,000, and the $GBTC premium was 20%, with 3AC's holdings exceeding $1 billion.

The news of "the largest holder of GBTC" quickly made 3AC an industry star, but many people wondered how 3AC had so much money and where these BTC came from.

Now all the answers have surfaced—borrowed.

Deep Tide TechFlow learned that 3AC had long been borrowing BTC at ultra-low interest rates without collateral, converting it into GBTC, and then pledging it to Genesis, a lending platform also belonging to DCG, to obtain liquidity.

In the bull market cycle, everything was great; BTC continued to rise, and GBTC had a premium.

However, good times did not last long. After three Bitcoin ETFs were launched in Canada, the demand for GBTC decreased, leading to a rapid disappearance of its premium, and by March 2021, it even showed a negative premium.

Not only did 3AC panic, but Grayscale also panicked. In April 2021, Grayscale announced plans to convert GBTC into an ETF.

The Twitter posts and frequency of the two founders of 3AC essentially served as a barometer for the company. From June to July 2021, they went quiet on Twitter, started discussing TradFi, talked about hedging bets, and even rarely mentioned cryptocurrency for a time.

Until a wave of altcoin trends led by new public chains caused 3AC's asset value to soar, the two founders revived their activity on Twitter.

Moreover, 3AC faced little immediate redemption pressure for institutional lending, while BlockFi raised BTC from the general public and faced more redemption pressure. Therefore, BlockFi had to continuously sell GBTC at a negative premium, selling off its holdings throughout the first quarter of 2021.

Even during the bull markets of 2020 and 2021, BlockFi reported losses of over $63.9 million and $221.5 million, respectively. According to an employee from a crypto lending institution, BlockFi's losses on GBTC were close to $700 million.

3AC had no short-term redemption pressure for BTC, but the pledged GBTC carried liquidation risks, and the risks would also be transmitted to DCG.

On June 18, Bloomberg terminals briefly cleared 3AC's GBTC holdings to zero. Bloomberg stated that since January 4, 2021, 3AC had not submitted a 13G/A filing, and they could not find any confirmation that Three Arrows still held $GBTC, thus deleting it as outdated data.

Less than a day later, the data was restored, and Bloomberg stated, "Until we confirm they no longer hold that position, which may require reviewing the 13G/A filing."

Currently, it can be confirmed that in early June, 3AC still held a large amount of GBTC positions and hoped that GBTC could save 3AC.

According to The Block, starting from June 7, 3AC's over-the-counter trading company TPS Capital began aggressively promoting GBTC arbitrage products, allowing TPS Capital to lock up Bitcoin for 12 months and return it after maturity, receiving a promissory note in exchange for Bitcoin, and charging a 20% management fee.

A certain crypto institution told Deep Tide TechFlow that 3AC contacted them around June 8 to promote arbitrage products, claiming that GBTC arbitrage could yield a 40% profit in 40 days, with a minimum investment amount of $5 million.

Theoretically, severely negative premiums on GBTC still present arbitrage opportunities.

DCG is actively applying to the U.S. SEC to convert GBTC into a Bitcoin ETF.

Once successful, the ETF will more effectively track the price of Bitcoin, eliminating discounts and premiums, meaning that the current negative premium of over 35% will disappear, thus creating arbitrage opportunities.

At the same time, DCG promised to lower GBTC management fees, and the trading venue for GBTC will be upgraded from OTCQX to the more liquid NYSE Arca.

As the largest holder of GBTC, Zhu Su has always hoped for GBTC to be renamed and upgraded from a trust to an ETF, which would rapidly increase the value of its holdings by over 40%.

In October 2021, Grayscale submitted an application to the U.S. SEC to convert GBTC into a Bitcoin spot ETF, with the SEC's deadline for approval or rejection set for July 6. This is why 3AC told many institutions that they could achieve over 40% profit in just 40 days, essentially betting that the SEC would approve the application.

However, regarding this arbitrage product, Bloomberg ETF analyst James Seyffart stated:

"In traditional finance, they call this operation structured notes, but in any case, they will gain ownership of your Bitcoin while also profiting from your BTC. They get your BTC and take returns from investors regardless of whether GBTC converts to an ETF. Even if Three Arrows/TPS is solvent, this is absolutely a bad deal for any investor."

It is reported that 3AC did not rely on this product to obtain much external funding, waiting for either a tragic liquidation.

On June 18, Genesis CEO Michael Moro tweeted that the company had liquidated the collateral of a "large counterparty" because that counterparty failed to meet margin requirements, adding that they would actively seek to recover any potential remaining losses through all possible means, and that their potential losses were limited, as the company had shed the risk.

Although Moro did not directly name 3AC, combined with the current market dynamics and Bloomberg's deliberate clearing of 3AC's GBTC holdings data on that day, the market believes that this large counterparty is most likely Three Arrows Capital.

Success or failure all comes down to arbitrage; the stars dancing on leverage for arbitrage ultimately fall due to leverage.

As Zweig said, perhaps it was because they were still too young at that time, not knowing that all the gifts of fate had already been secretly priced. In the liquidity crisis, no one can remain unscathed; the institutional bull market driven by institutions purchasing BTC ultimately falls silent due to the liquidation of institutional leveraged assets.

Their names will fall into the annals of history, while BTC remains the same BTC.

Risk warning

Risk warning Risk warning

Risk warning