Detailed Explanation of DeFi Options Vaults (DOV) and Its Ecosystem: The Path to Financial Democratization

Although options trading is a tool for seasoned investors in traditional finance, DOV is available for all types of investors, representing an important step towards democratizing finance for the masses.

Although options trading is a tool for seasoned investors in traditional finance, DOV is available for all types of investors, representing an important step towards democratizing finance for the masses.Authors: @j_mokwh, @Web3Geee, Treehouse

Compiled by: Beichen, Chain Teahouse

Introduction to DOV

DeFi users are familiar with yield farming. After all, in the early days of DeFi Summer, most mining had no lock-up period, so yields started directly from double digits and even soared to astronomical numbers reminiscent of Ponzi schemes.

However, the initial high yields quickly disappeared, as DeFi protocols primarily offered subsidies to attract users. When DeFi protocols began to imitate each other in the name of "user adoption," we saw many projects unable to sustain themselves gradually exit the market.

In this process, while many users gained short-term benefits, when the entire market's capital dried up, it was inevitably the last wave of users who would bear the cost.

This unsustainable return leads people to exploit volatility to earn profits on options.

Options have always been an indispensable part of the TradFi market, allowing investors to express directional views and profit from volatility, thus forming numerous structured products like Lego blocks. If implemented correctly, these tools can provide exceptional risk-adjusted capital returns, surpassing simple buy-and-hold strategies.

Moreover, options have become an important source of income in TradFi, especially in the stock/forex domain, where spot holders hedge their assets by purchasing options.

For cryptocurrencies and DeFi to further develop, a liquid options market is crucial, as it opens up another dimension beyond spot price movements.

That said, options strategies are very complex, and not everyone has the time or knowledge to execute these strategies in a timely manner, which is why we need DeFi Options Vaults (DOV).

DOV provides users with a way to easily deposit funds into predefined options strategies to earn returns.

Before the creation of DOV, only qualified investors could trade through over-the-counter (OTC) transactions or execute options strategies on exchanges like Opyn. DOV allows investors to simply deposit assets into the vault, which then executes yield-generating strategies on behalf of the investors.

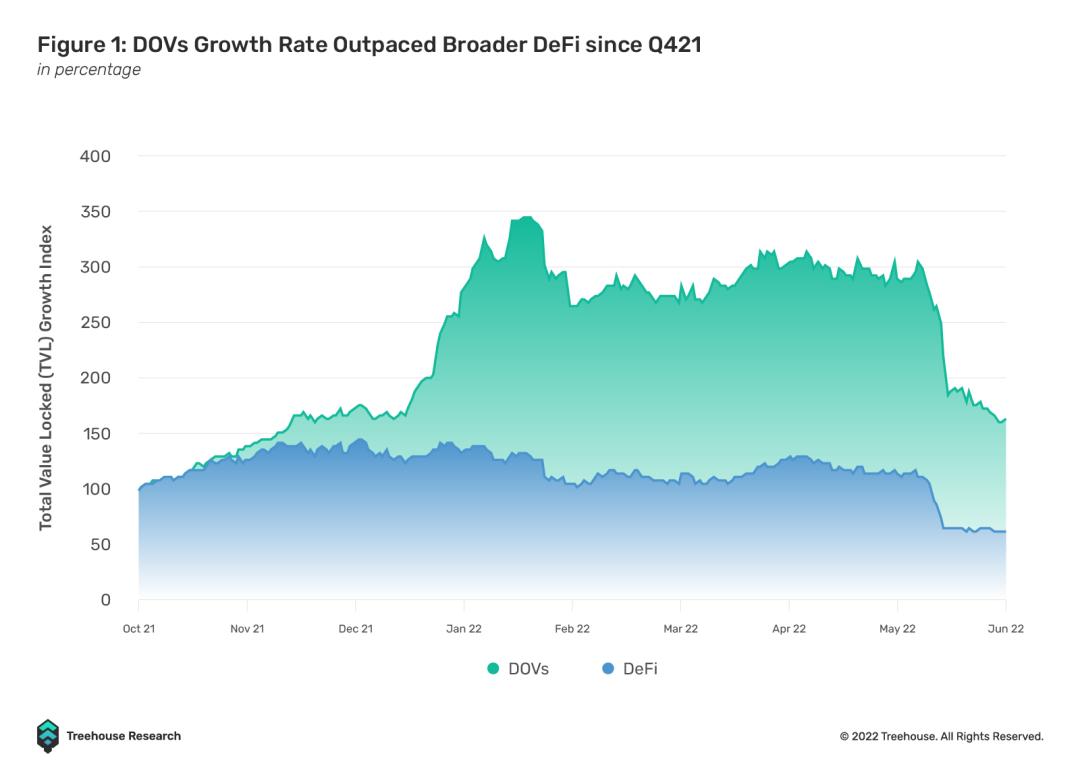

Growth rates of DOV and the DeFi market since Q4 2021

In Q1 2021, DOV's growth rate was similar to that of the entire DeFi market, but by December 2021, DOV began to explode, with TVL tripling in three months. Despite entering a bear market in early 2022, it still showed resilience.

There are several reasons why DOV has recently gained popularity and will continue to appear in the DeFi space.

First, DOV can generate returns by monetizing the volatility of underlying assets. Crypto options are an important source of income, with implied volatility often exceeding actual volatility, also known as variance risk premium.

Second, DOV allows for scalable trading of nonlinear tools on DeFi.

Options provided by centralized exchanges follow a limit order book model, meaning liquidity is dispersed across different price levels. In contrast, DOV concentrates options liquidity on specific or a series of strike prices with predetermined expiration dates, greatly enhancing liquidity. The improvement in liquidity will inevitably spread to CeFi.

In this article, we will explore the complexities of DOV, evaluate different types of DOVs, and provide our outlook on the future.

How DOV Works Internally

The most common strategies implemented by DOV products are covered call options and cash-secured put options.

The covered call strategy involves selling call options at a strike price higher than the current market price and returning the earned option premiums to the vault, which constitutes the earnings for depositors.

Cash-secured put options are similar, just in the opposite direction.

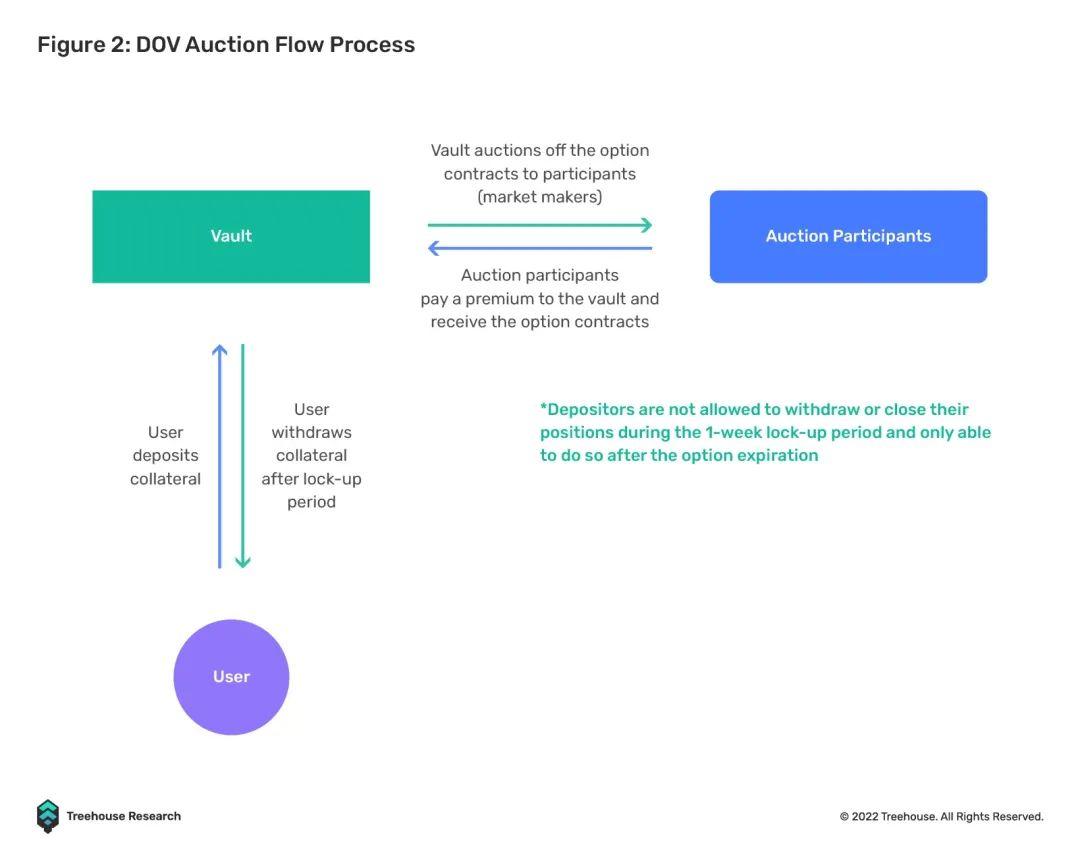

The vault is open to traders, who can deposit assets into the corresponding strategies they wish to participate in. Typically, volatile assets are deposited for the call-selling vault, while stablecoins are deposited for the put-selling vault. The vault then opens options weekly and auctions them to market participants at predetermined dates and times.

Different DOV products have their own mechanisms for minting and selling options to authorized participants, but overall, they determine option parameters, such as strike price and expiration, based on backtesting results to provide depositors with the highest risk-adjusted capital returns.

After the auction is completed, the vault receives the option premiums. Upon expiration, depositors can withdraw their deposits or continue to keep them in the vault for the next auction.

Due to varying performance of strategies, the balance in the vault may be higher or lower than the previous week.

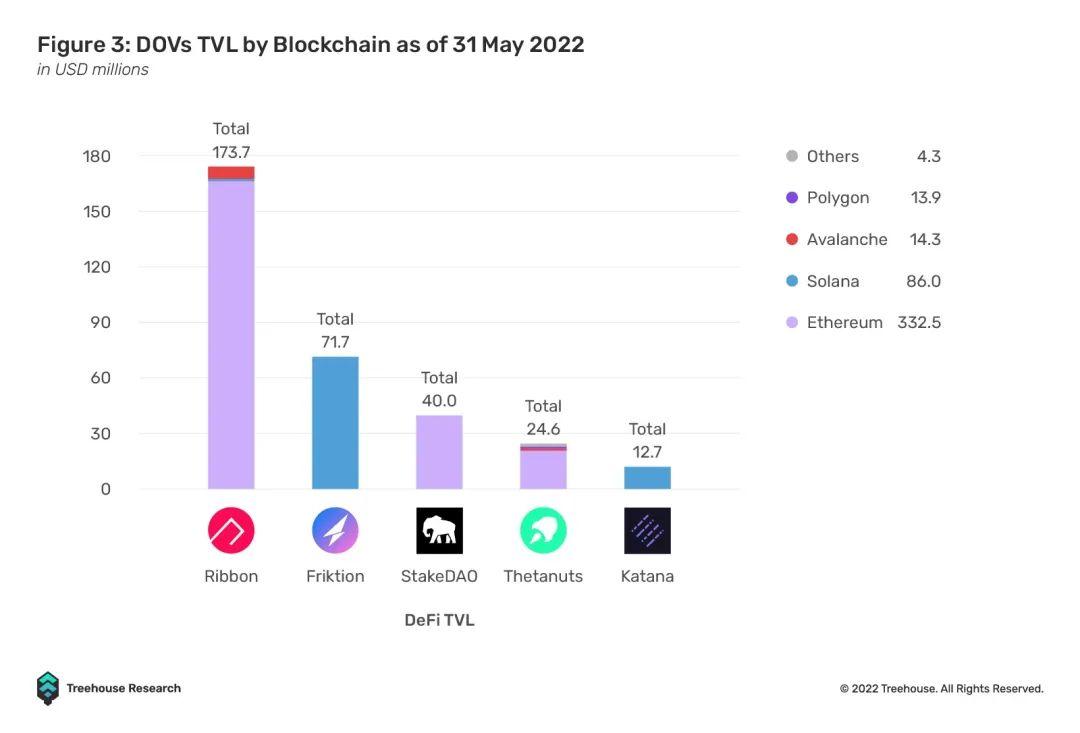

Existing DOV Protocols

Many existing DOV protocols are deployed on various blockchains with the same goal: to generate returns for investors.

Although most of them have similar strategies (covered call options or cash-secured put options), the capabilities across DOV protocols can vary due to different execution mechanisms, micro-strategies, and additional yield coverage.

Ribbon Finance

Ribbon Finance is a pioneer in the DOV space, allowing users access to crypto structured products for DeFi.

Ribbon Finance's flagship product, Theta Vault, enables users to deposit assets and earn returns through various options strategies. Currently, it offers 11 different vaults covering 5 different tokens for put options and covered call strategies.

Since its launch in April 2021, Ribbon Finance's vaults have generated over $38 million in revenue, with a peak TVL exceeding $300 million. Institutions like Dragonfly Capital, Nascent, and Coinbase Ventures participated in the seed round financing.

StakeDAO

StakeDAO initially started as a yield aggregator similar to Yearn Finance but later expanded to other yield products, such as arbitrage vaults, staking-as-a-service, and DOV.

It launched its first options vault on August 19, 2021, featuring three main vaults centered around BTC and ETH, operating similarly to Ribbon by using Opyn as the options market to underwrite their options.

What sets StakeDAO apart is that assets deposited into the StakeDAO options vault are immediately transferred to the platform's passive yield vault, generating additional returns on top of the earned option premiums. StakeDAO also allows users to stake LP tokens received from the options vault to earn SDT tokens, thereby enhancing yields.

While Ribbon has shifted to an active fund management fee model, StakeDAO charges zero platform fees on assets or profits but imposes a 0.50% withdrawal fee.

StakeDAO has been actively building within the Curve ecosystem, supporting various Curve-based assets and strategies.

Thetanuts

Thetanuts is a cross-chain structured product protocol designed for everyday investors, fundamentally simplifying the yield earning process and providing options exposure.

Launched in December 2021, Thetanuts is now available on chains like Ethereum, Avalanche, BNBChain, Polygon, Fantom, Aurora, and Boba. It has gained over $24 million in TVL through active deployment on new chains.

Thetanuts does not charge fees for its vaults and utilizes off-chain auctions to auction options to trading firms like QCP Capital and Paradigm, allowing them to offer differentiated options as they are not constrained by on-chain collateral availability.

Thetanuts recently completed an $18 million seed round led by Three Arrows Capital, Deribit, QCP Capital, and Jump Crypto.

Thetanuts stands out from other DOV protocols through its Stronghold strategy.

Stronghold aggregates multiple Thetanuts base vaults to create an index token representing the proportional fair value of the vault's composition. By exchanging tokens for the Stronghold index token, investors are essentially investing in a strategy pool optimized based on backtesting and periodically adjusted parameters, similar to volatility risk premium harvesting hedge funds, but it is on-chain and fee-free.

Friktion

Friktion is currently a DeFi portfolio management product protocol on the Solana network, providing risk-adjusted yield generation strategies for DAOs, individuals, and traditional institutions.

Friktion's native portfolio strategy, "Volts," is a play on the term "Vaults," allowing investors to earn returns through derivatives arbitrage and volatility strategies.

Launched in December 2021, Friktion has a trading volume of $2.2 billion and offers the largest options market in DeFi, covering 35 assets.

Friktion uses Inertia (Euro cash-settled options) and Entropy (a unique derivatives DEX) for their on-chain settlements. Additionally, Friktion has built an institutional analytics platform for all users to analyze the performance of each vault and their respective strategies.

Last December, Friktion raised $5.5 million from companies like Jump Crypto and DeFiance Capital, and it has grown to become the largest structured product protocol on Solana.

Friktion's product range extends from yield-generating vaults to comprehensive portfolio management services, focusing on risk management products: for example, Volt#05, which helps liquidity providers hedge against impermanent loss while benefiting from high-yield opportunities. Friktion also offers delta-neutral strategies that automatically delta-hedge through their system, as well as directional strategies like covered calls and puts with delta.

Katana

After winning the 2021 Solana IGNITION hackathon, Katana officially launched in December 2021. It has successfully built 14 different vaults, supporting assets similar to Friktion.

Katana's vault minting factory tokenizes out-of-the-money options on Zeta and sells them to market makers through a competitive request for quote (RFQ) auction process. Katana's current TVL is $11 million.

Recently, Katana announced a $5 million seed round led by Framework, which will be used to help the protocol scale and become the de facto yield generation layer in DeFi.

Potential Issues Surrounding DOV

While DOV has the potential to revolutionize yield farming and democratize structured products, they also have potential downsides. DOVs in the TradFi stock space and systematic volatility selling strategies may be similar to each other. The latter has witnessed several explosions among option sellers, particularly after prolonged periods of low volatility from 2016 to 2018, when volatility eventually mean-reverted significantly, during which participants crowded into the same volatility selling strategies. As the DOV space expands, it may face similar issues. Additionally, capital inefficiency and front-running issues may be the next obstacles DOV needs to address before attracting more TVL.

Capital Inefficiency

Since the heyday of modern finance, volatility selling has come a long way, but it has also experienced quite a few collapses. Fortunately, most decentralized options vaults today require full collateralization.

For example, a call vault for ETH would require investors to deposit the underlying ETH into the vault and sell options at a nominal amount below the collateral deposited to prevent naked shorting and protect investors from losing more than they own when the strategy is not leveraged. However, the cost of increased security is lower returns.

Unlike directly selling options, DOVs do not allow holders to close positions before expiration, meaning if investors wish to take profits before expiration, they must engage in offsetting trades.

For retail investors who do not mind delta exposure, locked ETH represents an opportunity cost, as it could generate returns elsewhere to compound their yields.

Improvements are being made to address the capital inefficiency of DOVs, and a good balance must ultimately be struck between capital efficiency and investor protection.

For instance, Ribbon Finance is considering reducing the collateral required for options vaults. Additionally, Ribbon Finance has integrated with Lido Finance's Liquid Staking feature, allowing vault depositors to simultaneously earn ETH staking rewards and option premiums.

Front-Running in DOVs

Like any other asset, option prices are determined by supply and demand, and a key component of option pricing is implied volatility. Options are volatility products that represent a specific return distribution of the underlying asset. Simply put, if implied volatility is high, option prices will be higher, and vice versa.

This is a problem currently faced by most DOVs—what happens if over $100 million worth of options are sold weekly on the same expiration time and target delta platform? The result is that implied volatility gets compressed, leading to suppressed yields, and opportunistic frontrunners further drive down yields.

Currently, most DOV auctions are held on Fridays, as market makers can transfer risk over the weekend. Given that weekly options managed by Deribit also expire on Fridays, market makers can easily handle DOV liquidity. However, this allows savvy volatility traders to front-run trades before DOV auctions, reducing the yields for vault holders.

For the benefit of vault depositors, some protocols are attempting to change the timing. For example, the Friktion protocol has adjusted its execution time to occur throughout the day to leverage volatility market dynamics and provide users with higher risk-adjusted returns. Additionally, Ribbon Finance is the first to decentralize and open bidding to non-market makers.

However, current efforts have not effectively addressed the supply-demand imbalance, as buyers cannot unwind their options before expiration, meaning they must provide additional collateral on another centralized exchange to close their positions.

Crowding and Underperformance

As more investors flock to options selling strategies, two things happen.

Option sellers exceed buyers during specific intervals before and after DOV auctions, resulting in lower premiums earned from selling options. This is evident in the TradFi space, and DOV is no exception.

First, most DOV participants are inexperienced retail investors who are price insensitive and primarily seek yield.

Second, protocol designers are attempting to create a one-size-fits-all approach for DOVs, allowing vault holders to enjoy a hands-free options selling method. These dynamics may further depress yields, as vault holders may indiscriminately and systematically sell volatility, even when market conditions indicate that risk-adjusted returns from volatility selling are poor.

Returning to the TradFi space, given the influx of options selling strategies leading to a decline in variance risk premium, option sellers either increase their selling volume through leverage or choose more aggressive strike prices to meet their return benchmarks. This accumulates negative Gamma and Vega risk. Therefore, if the market moves sharply in either direction, option sellers' performance will suffer.

Volatility selling may also have secondary effects on the entire spot market. The crypto options market currently accounts for less than 1% of the entire crypto market, and if this proportion increases, the market structure may change, giving the options market greater influence.

As options trading becomes increasingly popular in cryptocurrencies, the traders creating these markets will more frequently hedge, as they take on more Gamma risk, whether long or short.

Investors should recognize the risks they take when investing using options vaults. For covered call options, overall collateral is limited, as if the options are exercised in the money, their dollar value will still increase. However, selling put options is a risky endeavor, as if the options expire in the money, their value will decrease.

The Future of DOV

Despite the cautionary tales mentioned in the previous section, we believe DOV will fundamentally change the DeFi landscape by providing yields to the masses and democratizing options. Here are our views on how DOV should progress from here.

Innovation, Innovation, and More Innovation

The fact that DOV is still in its infancy is perhaps the most exciting aspect.

Currently, DOV only offers covered call options and put options, but the potential uses of options are so broad that they allow investors to express specific views. Therefore, in the future, new strategies with enticing returns may be offered to investors, such as butterfly spreads. DOV could also research physical settlement for vault holders (if options are exercised, they do not have to buy or sell the underlying asset on another exchange).

In addition to expanding their products in the field, protocol developers can also consider improving their execution methods. Execution can occur on any day of the week rather than focusing on one day.

For example, Ribbon Finance recently announced its planned V3 upgrade, allowing auctions to be executed at random times and sizes.

Paradigm, an institutional crypto liquidity network, has also recently collaborated with several DOV protocols to improve on-demand liquidity for traders and investors to adjust their options exposure in terms of expiration dates, risk profiles, and settlement preferences. This collaboration will significantly enhance liquidity throughout the DOV auction process, benefiting all parties involved.

Finally, DOV could consider tokenizing vault positions to address capital inefficiency issues. For example, Thetanuts will soon convert its vaults into tokenized positions, allowing users to swap in and out early. The token value will reflect the options prices of the vault.

Self-Regulation and Retail Education

In addition to the usual smart contract and protocol risks, there are some risks that may not be familiar to first-time options investors.

There are many avenues for learning, such as Deribit and GenesisVolatility, which publish useful options content for both beginners and experts. Recently, Katana announced they will launch Katana Dojo, an educational program aimed at providing investors with basic options knowledge.

Investors should not focus solely on yield but should consider strike prices, expiration dates, and whether they are willing to be exercised if options expire in the money. Investors must also understand the management and performance fees of these vaults.

Investors should not simply engage in systematic selling but should understand the current volatility environment. For example, in a risk-off environment, actual volatility may exceed implied volatility, and investors should remain cautious before implementing volatility selling strategies.

It is strongly recommended that investors adopt a mixed approach to selling volatility. If they believe the risks they are taking are not adequately compensated, they can choose not to participate that week.

Again, Ribbon Finance V3 will offer a "pause" feature, allowing investors to improve user experience without needing to withdraw funds from the vault. Education and self-regulation are key to protecting investors.

Conclusion

While options trading is reserved for more mature investors in traditional finance, DOV is accessible to all types of investors, representing a significant step toward the democratization of finance for the masses.

DOV has a bright future ahead.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles