Messari Q2 Web3 Infrastructure Revenue Report: Revenue Down Only 10%, Demand Remains Strong

The revenue generated by Web3 protocols pales in comparison to that of Web2 companies, but the potential market is enormous.

The revenue generated by Web3 protocols pales in comparison to that of Web2 companies, but the potential market is enormous.Written by: Sami Kassab, Messari Researcher

Compiled by: iambabywhale.eth

Key Points:

Many Web3 infrastructure protocols generate stable revenue by providing services both within and outside the Web3 ecosystem. Services range from storage to computing to wireless data transmission;

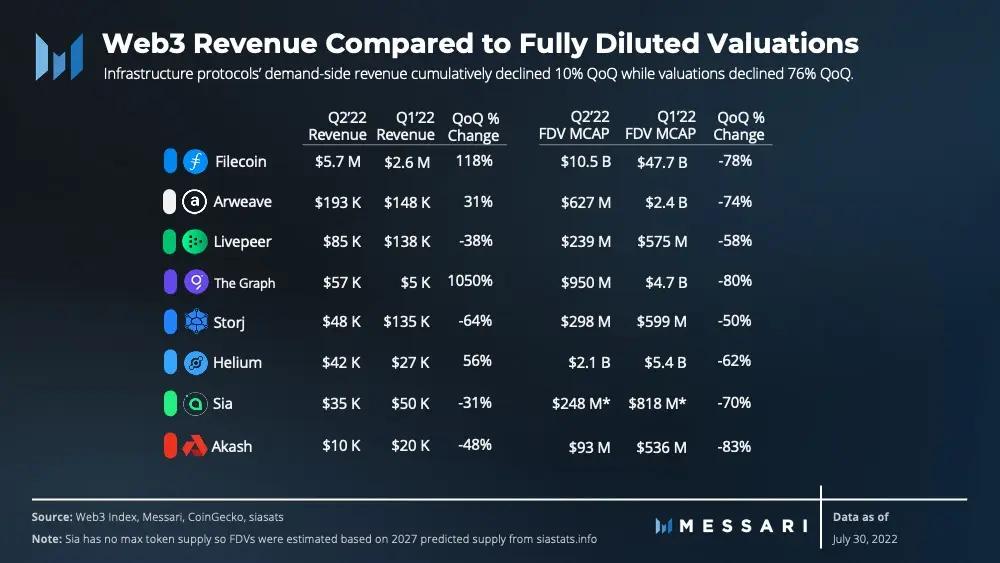

As the bear market deepens, Web3 infrastructure revenue has only declined by 10%, indicating that despite a 76% drop in overall protocol valuations, demand for these protocol services remains strong;

Although Web3 protocols may appear overvalued on a revenue basis, given the total potential market for each industry, current valuations are more attractive than in Q1 2022.

The Web3 industry is often criticized for lacking any practical use cases beyond the circular economy, but this is not the case; some Web3 infrastructure protocols provide services both within and outside the Web3 ecosystem. They offer services including decentralized storage, computing, and wireless data transmission to Web3 users and non-crypto-native participants. End users are required to pay fees when using these services, thus generating revenue for the protocols.

In the last quarter, the total market capitalization of cryptocurrencies fell by 59%, from $2.1 trillion to $860 billion. In the Web3 infrastructure space, fully diluted valuations decreased by 76%, from $63 billion to $15 billion. Despite the harsh environment, Web3 infrastructure protocols continue to operate and generate revenue without interruption.

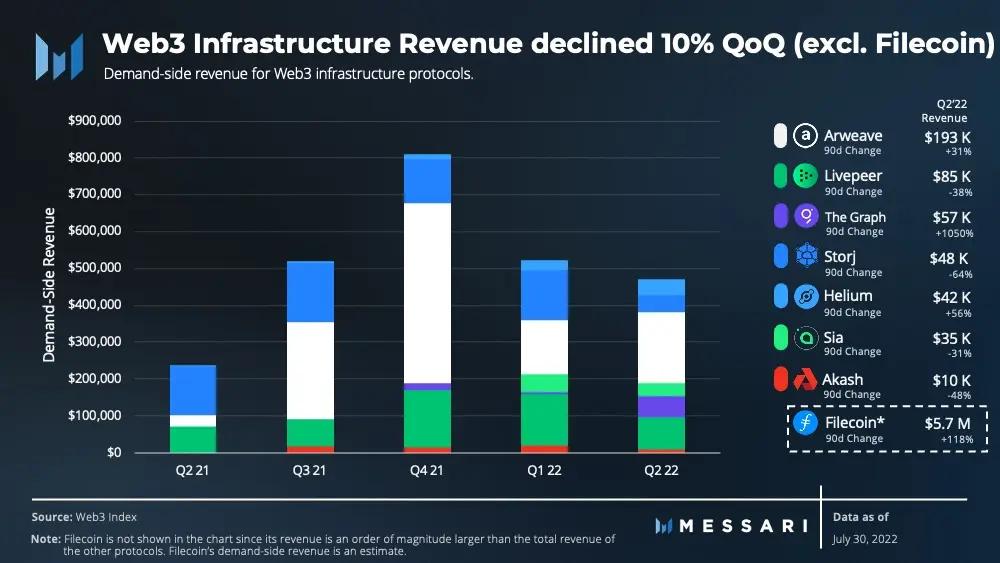

In Q2 2022, Web3 infrastructure protocols generated $5.7 million in revenue. Excluding the dominant Filecoin, the remaining Web3 infrastructure protocols collectively generated $470,000 in revenue last quarter, a 10% decline compared to Q1 2022.

Revenue Calculation Method

Data comes from the Web3 Index, which tracks demand-side revenue for infrastructure protocols, primarily including fees paid by end users for using the network and its services. This metric measures actual network usage, while total revenue and similar metrics can include income from supply-side participants and inflationary token rewards, which do not reflect network usage.

Filecoin is the only protocol not included in the Web3 Index in this report because it has a unique revenue framework. Demand-side participants pay for retrieval data services provided by storage providers for updating storage transactions. Unlike storage transactions, data is retrieved off-chain by storage providers, making the retrieval fee data unknown. Since storage fees are subsidized by the protocol, users only need to pay a base fee and any additional fees that may arise when transacting on the network. Revenue generated by demand-side participants for Filecoin can be estimated by assuming that 45% of network transaction fees come from demand-side participants (assuming half of network transactions come from supply-side participants).

Revenue Breakdown by Sector

Storage

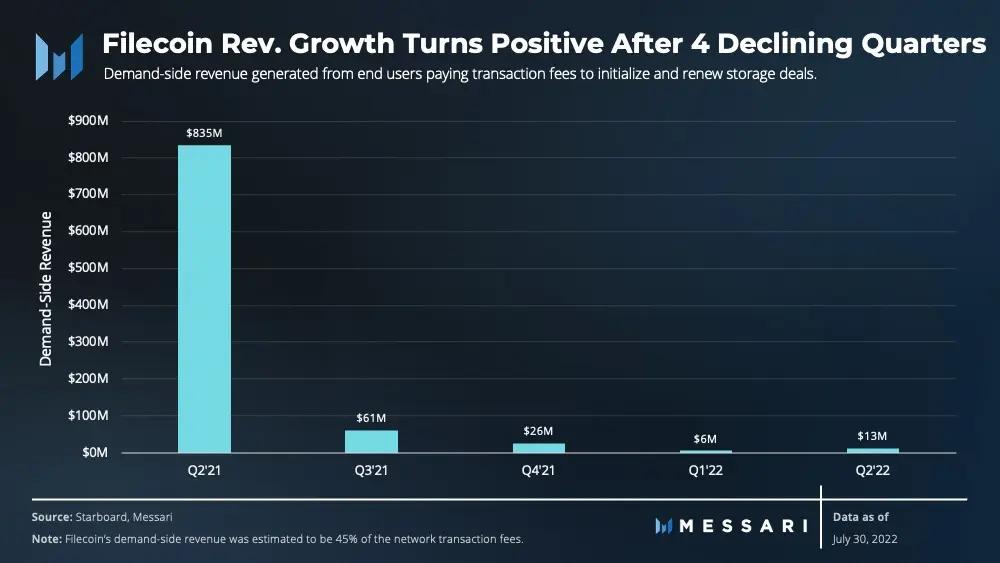

Based on the storage used and network capacity, Filecoin holds the largest market share. Its revenue corresponds to the demand for block space (higher demand means users will pay higher transaction fees), rather than the amount of data stored on the network. Therefore, to increase revenue, the transaction volume generated by storage demand needs to exceed the network's capacity.

Although Filecoin's storage capacity and utilization have been increasing over the past year, revenue has been declining until the most recent quarter. Filecoin's revenue sharply declined after Q2 2021 due to the HyperDrive upgrade, which increased the network's throughput by 10-25 times, thereby reducing transaction fees. Therefore, revenue figures are not expected to recover to Q2 2021 levels anytime soon.

After experiencing four quarters of declining revenue, Filecoin generated $5.7 million in revenue in Q2, a 118% quarter-over-quarter increase. This is attributed to a significant increase in active transactions (i.e., the amount of data currently stored on the network): an 80% increase from the previous quarter. Filecoin stands out as its revenue is several times that of other storage protocols.

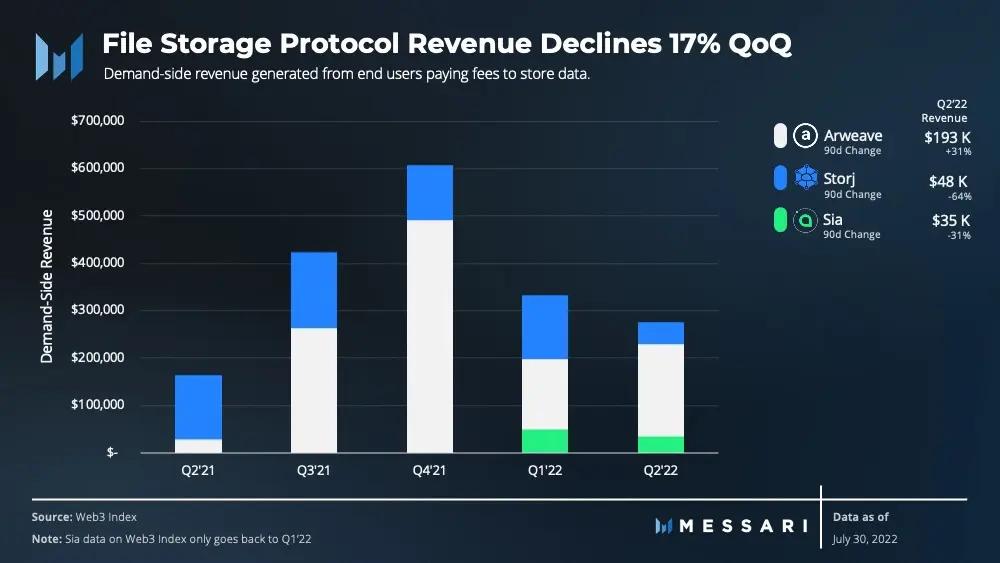

Arweave is a protocol focused on permanent storage, generating the second-highest revenue among storage protocols this quarter, at $193,430, a 31% quarter-over-quarter increase. Its storage volume increased by 33% quarter-over-quarter. Meanwhile, Storj and Sia experienced negative revenue growth of -64% and -31%, respectively. However, the storage volumes for Storj and Sia increased by 9% and 36% quarter-over-quarter, respectively.

Despite an increase in Sia's storage volume, the average storage price set by the market fell by 63%, leading to a revenue decline. On the other hand, Storj charges a fixed fee of $4 per TB while providing users with 150 GB of free storage. The free storage plan has led to an increase in storage volume, but Storj's revenue decreased this quarter.

Computing

A range of applications and services, including rendering, hosting, and transcoding, require computing resources. Web3 computing protocols allow supply-side participants to earn rewards by renting out their GPU and CPU resources to end users in need.

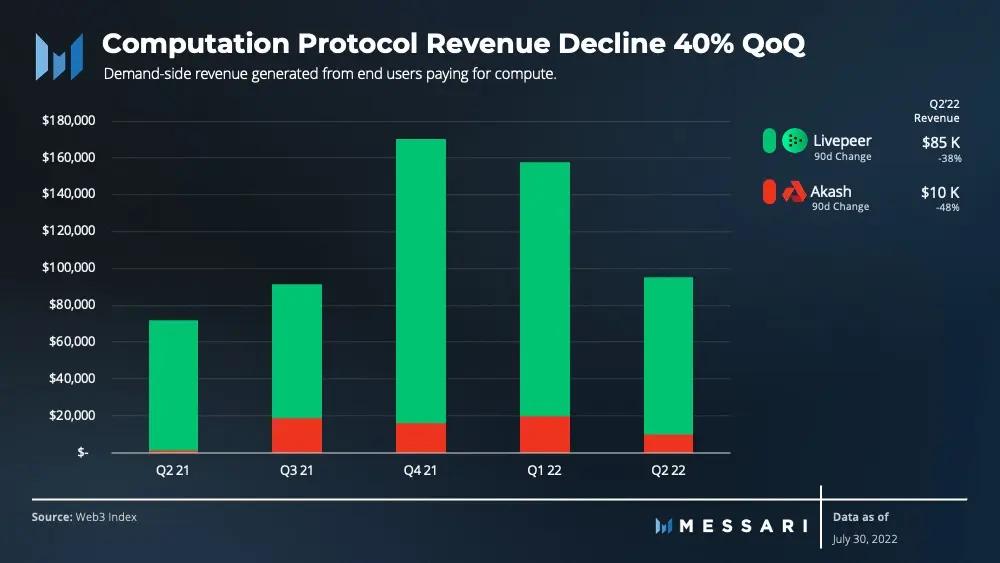

Livepeer is a decentralized marketplace for streaming applications that require video processing services. The network relies on miners using GPUs to provide video processing services to the network. Livepeer's revenue in Q2 2022 decreased by 39% quarter-over-quarter, but the number of videos processed by Livepeer remained the same as in Q1 2022. Given that Livepeer is an open market where fees are set by nodes, competition among node operators, combined with stagnant demand, has led to lower fees.

Akash is a decentralized cloud marketplace that connects users seeking computing resources with suppliers who have spare computing capacity. Akash's revenue decreased by 50% in Q2 2022, but the number of active leases on the network (i.e., the number of protocols renting computing resources) increased by 11%.

To rent resources on Akash, suppliers and end users agree on a monthly price denominated in AKT, which does not automatically adjust due to fluctuations in AKT prices. Since AKT fell by 83% in Q2, this naturally led to a decrease in dollar revenue. To address the issue of price stability, Overclock Labs is developing a stable settlement mechanism to stabilize the network's revenue through a non-tradable token pegged to the dollar.

Wireless Networks

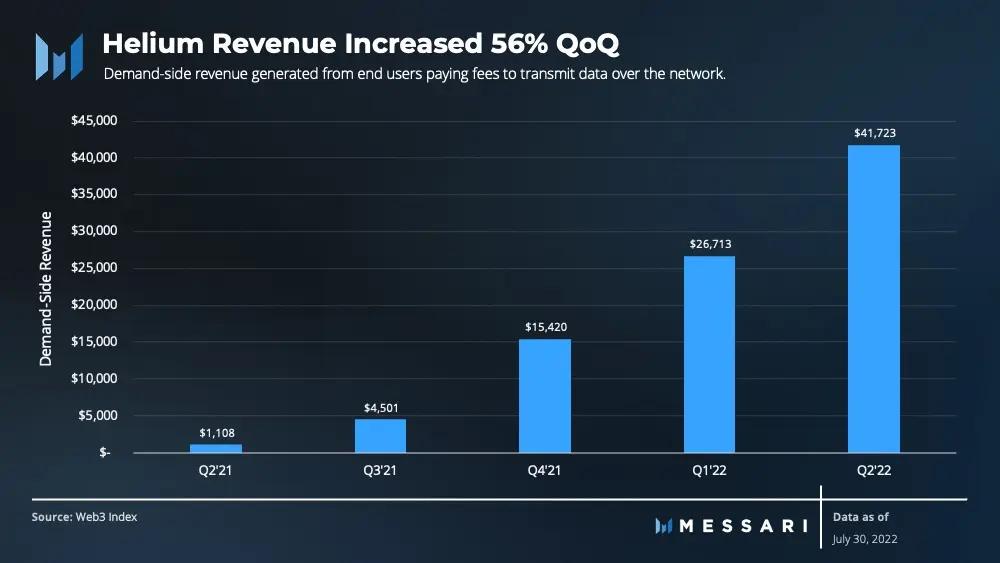

Helium is an economic system and platform for building distributed wireless networks. The protocol started with IoT networks and is currently developing 5G networks. The Helium network incentivizes supply-side participants to deploy hotspots, through which end users can transmit data.

The cost of transmitting data on Helium's IoT network is $0.0001 per 24 bytes. Last quarter, end users spent $42,000 transmitting data over the network, a 56% increase compared to the previous quarter. Although the revenue generated from end users transmitting data is relatively low compared to Helium's fully diluted valuation, the launch of 5G is expected to significantly increase the amount of data transmitted over the network. Additionally, the Helium community plans to launch many other networks, including WiFi, VPN, and CDN. If these networks prove successful, the total data transmitted through Helium should continue to increase.

Data Indexing

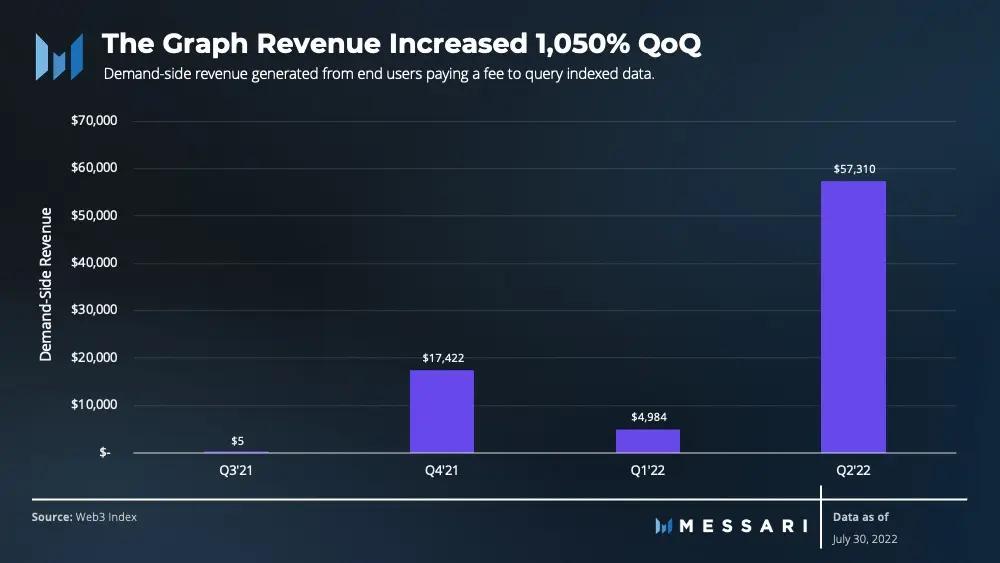

The Graph is a decentralized protocol for indexing and querying data from blockchains. Its end users are typically application developers who pay fees for each query from subgraphs (data indexes) to network indexers. Initially, The Graph provided indexing and querying services through a centralized hosting service, where queries were fully subsidized. However, since the migration of subgraphs to a decentralized network began in March 2022, the number of migrated subgraphs has increased by 40%, leading to a 1050% quarter-over-quarter increase in revenue from query fees. As more subgraphs migrate away from hosting services, revenue generated from end user fees for The Graph should continue to increase.

Thoughts on Fundamentals

Evaluating Web3 infrastructure protocols requires examining the actual usage of the network. Demand-side revenue shows the total fees paid by end users for using the network and its services. This metric excludes inflationary token rewards and income from supply-side participants, which do not reflect network usage. After assigning a reasonable multiple to these revenues, the current protocol valuations may seem overvalued. However, considering that the fully diluted valuations of Web3 infrastructure protocols have decreased by 76%, the current valuations are more attractive than they were three months ago.

Despite a 76% decline in valuations, revenue excluding Filecoin has only decreased by 10%. Including Filecoin, total revenue generated from the demand side has increased by 97%. Given the significant drop in valuations, this indicates that demand for Web3 infrastructure protocols remains stable during the bear market.

While the revenue generated by these protocols pales in comparison to that of Web2 companies, it should be noted that these protocols are still in their infancy. Each protocol is expanding its service offerings, developing new monetization methods, and integrating both within and outside the Web3 ecosystem. Ultimately, the total potential market for each sector is enormous. With a long-term view on current valuations, it is likely that the major players in each category are currently undervalued.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles