How to build a cryptocurrency banking system?

Building a robust cryptocurrency financial system requires three components: tokenized real-world credit (bonds), a strong cryptocurrency market for trading and lending (providing deep liquidity and price discovery), and the maturity conversion of crypto banks.

Building a robust cryptocurrency financial system requires three components: tokenized real-world credit (bonds), a strong cryptocurrency market for trading and lending (providing deep liquidity and price discovery), and the maturity conversion of crypto banks.Source: CryptoBanking

Original Title: 《The Crypto Banking System》

Compiled by: Guo Qianwen, Chain Catcher

This article explores the foundations needed to build a financial system on DeFi. Despite numerous innovations in the DeFi space, most of them are merely repeating speculation. Today, we discuss the necessary components required to construct an effective financial system that can provide funding for the real economy.

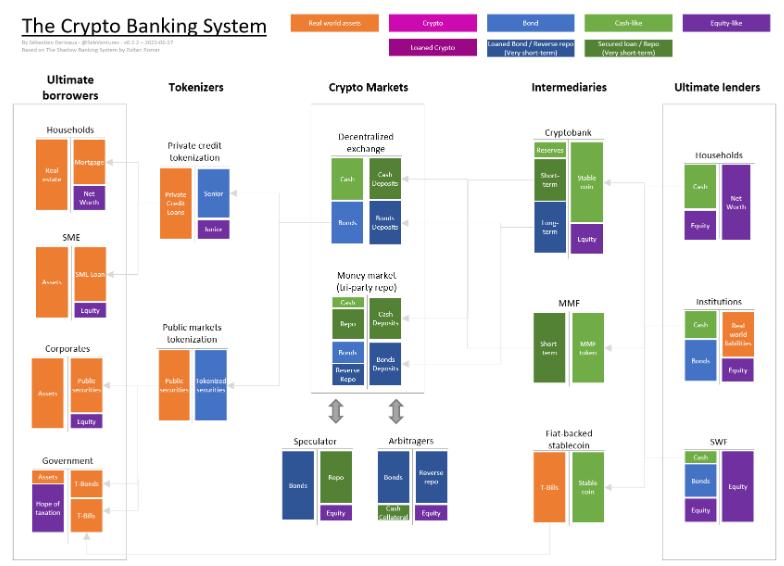

The following diagram, based on Zoltan's interpretation of the shadow banking system, provides a high-level overview of the cryptocurrency banking system. It also extends the content of "Crypto Banking System 101" and "Comparison of Cryptocurrency Banking System and Shadow Banking".

On the right side are the ultimate funders (households with substantial savings, financial institutions, independent wealth funds, etc.) who have excess cash (under the condition of charging fees/interest) available to fund the ultimate lenders on the left side (households with mortgages, small and medium-sized enterprises, large corporations, governments).

As shown in the chart, despite many stories about native cryptocurrency assets (such as ETH, BTC, etc.), they do not appear in this table. The chart is not exhaustive, and further analysis will be conducted on the position of cryptocurrency assets. You can also consider cash as a form of cryptocurrency, assuming that real-world assets use the same accounting unit, as the mechanism works similarly.

Key Elements of the Cryptocurrency Banking System:

- Deeply liquid tokenized bonds representing real-world credit (including private credit and public markets).

- Cryptocurrency markets, which are the core infrastructure of a market-based economy, including decentralized exchanges and repo markets.

- Cryptocurrency banks acting as intermediaries for savers and borrowers to facilitate maturity transformation.

Demand for New Components

DeFi is built on a foundation that does not require credit, with most borrowing relying on collateral. The key element of good collateral is deep liquidity—ability to quickly liquidate at scale without significantly impacting prices.

The most commonly used primary collateral in the DeFi world is ETH and WBTC. Both are highly volatile (thus experiencing significant valuation loss), have limited supply, and are speculative. They may serve as collateral in the future, but currently, they are not convenient enough.

Therefore, we need to introduce a new form of collateral. For example, gold, which has been tokenized (PAXG), has not received much attention.

If we look at TradFi, we find that the collateral chosen by people has shifted from commercial paper to government bonds.

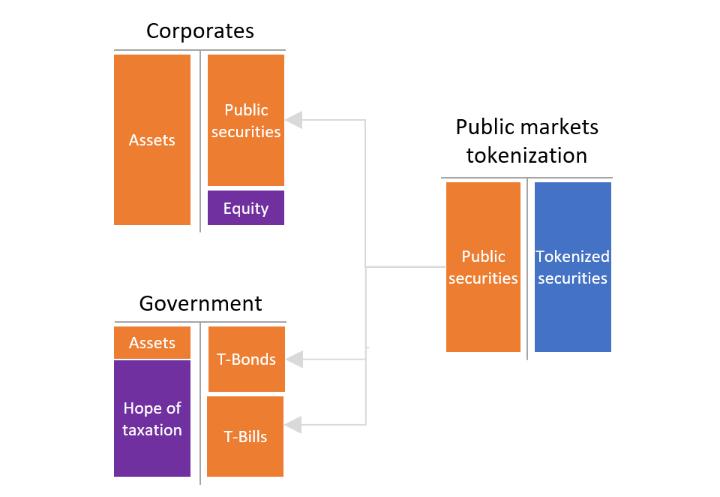

Public Credit Tokenization

The first area to obtain liquid collateral is on-chain public markets. Companies issue tradable bonds rated by credit rating agencies. Governments issue securities with high liquidity and high ratings, which, unlike cryptocurrency assets, are more stable and can effectively serve as collateral. In TradFi, these financial instruments are considered safe and sufficiently liquid, qualifying as high-quality liquid assets.

Public market tokenization would allow some public securities to be issued on the asset side while simultaneously issuing tokens (possibly on a 1:1 basis). To achieve better liquidity, similar types of bonds can be pooled together, or ETFs can be directly introduced (with the underlying assets also on-chain, allowing for centralized pooling).

One example is Backed Finance, which is collaborating with MakerDAO to tokenize the iShares U.S. Treasury Bond 1-3 Year UCITS ETF.

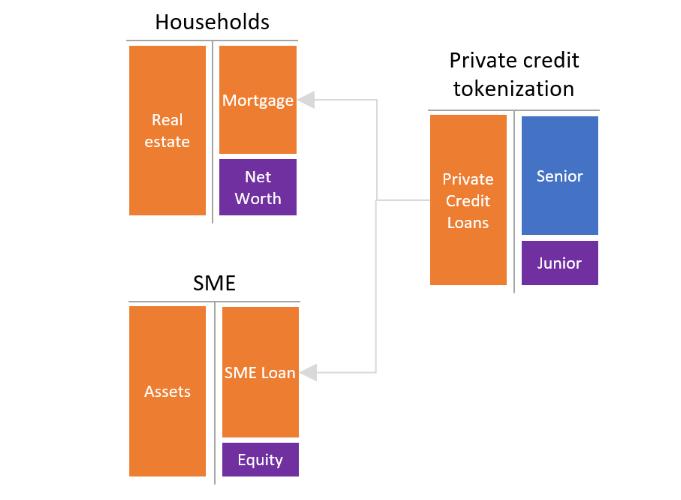

Private Credit Tokenization

If we limit ourselves to the public credit phase, many forms of collateral can still be used in the coming years, but such a system would exclude households and small to medium enterprises from financing.

The solution is securitization, utilizing a pool of illiquid assets (loans or non-tradable assets) while issuing two types of tokens, divided into senior and junior tranches. The increased credit of the junior tranche can provide safety and convenient price discovery for the senior tranche while forcing intermediaries to "play the game." Ideally, the price of the senior tranche needs to be assessed by credit rating agencies. The scale must be large enough, and the pool must be transparent enough to encourage the emergence of a strong liquid market in the senior tranche.

Examples of such tokenization include New Silver, which engages in "fix-and-flip" lending (currently not aimed at households), and FortunaFi, which collects loans from asset owners in the income-based finance sector.

Scale and Liquidity Over Everything

A key point is that both public and private sectors need to form liquid markets at a certain scale to avoid fragmented liquidity.

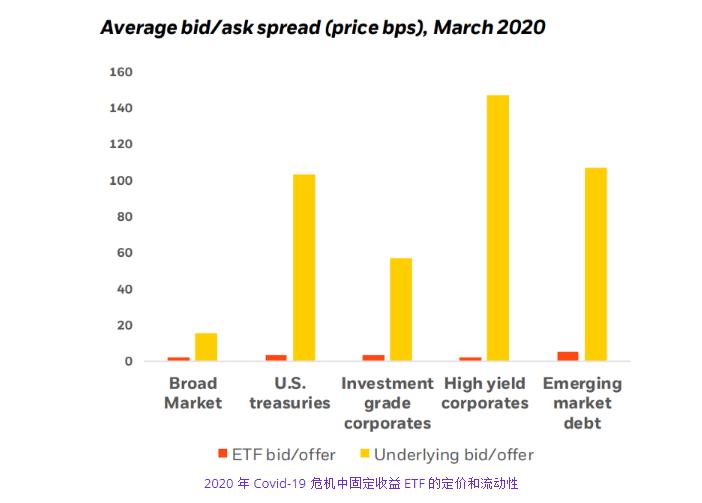

From the first data, it can be seen that in March 2022, ETF bonds had more liquidity than their underlying assets. Some studies also indicate that this aggregation of investments reduces the impact from asset sell-offs.

One major issue during the 2008 financial crisis was that illiquid securitized assets were used as collateral, sometimes with a haircut of zero. However, during severe crises, higher haircuts were adopted, leading to such collateral being excluded from the repo market.

Therefore, it is crucial to have very liquid and transparent tools to support the cryptocurrency banking system, rather than relying on a series of low liquidity and hard-to-understand tools.

What is not shown in the cryptocurrency banking system are funds issued by on-chain protocols and DAOs, which may or may not be backed by cryptocurrency collateral. Aggregating these assets requires the creation of other liquid and transparent fund tools.

With these deep and liquid components, we can build a robust cryptocurrency market.

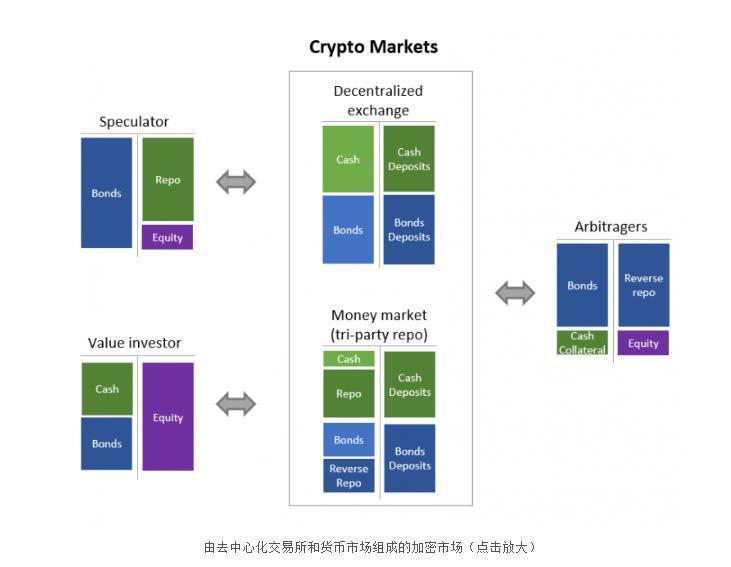

Cryptocurrency Market

The core of the cryptocurrency banking system is the cryptocurrency market, which provides deep liquidity pools for trading and short-term funding. The cryptocurrency market consists of two main sub-markets: decentralized exchanges (for trading) and money markets (for short-term funding). Both markets should minimize management and maximize the immutability of contracts. It should be credit-free, permissionless, and custodial-free.

There are three types of operators in the cryptocurrency market: value investors, speculators, and arbitrageurs.

The stability of the entire system is provided by value investors. These can be individuals, DeFi institutions (such as cryptocurrency banks or insurance protocols), or TradFi investors. In short, assuming they allocate their assets in a predetermined manner (e.g., 50% cash, 50% bonds), they will deposit a portion of these assets into decentralized exchanges, passively allowing the market to arbitrage their positions to maintain constant risk exposure. They will also earn trading fees (unlike TradFi, maintaining a constant allocation charges clients). They can also deposit unused liquidity and bonds into the money market for other users to borrow for a fee (again increasing the returns for value investors, while in TradFi, custodial services incur fees).

Arbitrageurs provide more liquidity for smaller spreads to create an efficient market. If the prices of investment-grade bonds fluctuate significantly, they can borrow in the money market, exchanging for government bonds with similar maturities (to hedge interest rate risk) and high credit risk bonds (to hedge credit risk). These bonds will be used as collateral in the money market, providing funding for the borrowed bonds. Arbitrageurs can also provide liquidity on options protocols, creating orderly markets for on-chain ETFs (by arbitraging ETF prices alongside the underlying assets).

Speculators are those willing to take on more risk than arbitrageurs—they go long or short on different assets to seize speculative opportunities. For example, going long on government bonds when speculators believe the yield curve is too steep (or vice versa), and then re-entering positions in the money market to gain leverage. Through speculation, they provide a price discovery mechanism, attempting to achieve an efficient market.

By concentrating liquidity in the cryptocurrency market rather than leaving it idle in wallets, the cryptocurrency banking system can achieve higher liquidity at lower costs and complexity compared to traditional markets.

Bond components are designed as a collection of low liquidity tools (i.e., corporate bonds and mortgages) to achieve high liquidity. The cryptocurrency market provides methods to use a significant portion of the market value of these components for liquidity trading or funding facilitation (nothing prevents decentralized exchanges from using liquidity from the money market in the background).

To be more effective, we need a new participant: the cryptocurrency bank.

Cryptocurrency Banks Moving Towards a Fractional Reserve System

According to the current definition, the cryptocurrency banking system consists of bond instruments and cash instruments. We have learned that bonds are composed of tokenized private collective credit and public market tools. So what is cash?

Defining Cash in the Cryptocurrency Banking System

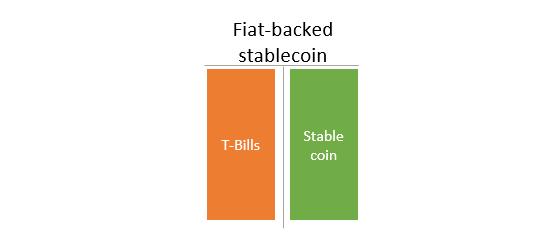

In a simplified version, fiat-backed stablecoins are on-demand liabilities backed by government bonds (or bank deposits) at a rate of 1 dollar. This backing allows stablecoins to be redeemed at any time (on demand) without liquidity issues. Currently, the interest rate spread between the two (i.e., Treasury bill rates) flows entirely to stablecoin issuers (or distributors), rather than stablecoin holders. This situation may change, but structurally, the interest rates received by stablecoin holders will be limited by Treasury bill rates.

At scale, such a system may be detrimental to credit intermediaries. In fact, if stablecoins become the new bank savings, it would shrink the scale of the latter and reduce credit creation by traditional banks. This is where cryptocurrency banks come into play.

Addressing Liquidity Preferences and Expanding Money Supply

There is a fundamental mismatch between ultimate lenders needing long-term loans and ultimate funders with liquidity preferences. As shown below, most ultimate funders hold cash, possibly large amounts of cash. While the likelihood of national deficit shortages is low, providing substantial funding for economic activity is not permitted, which may lead to economic limitations.

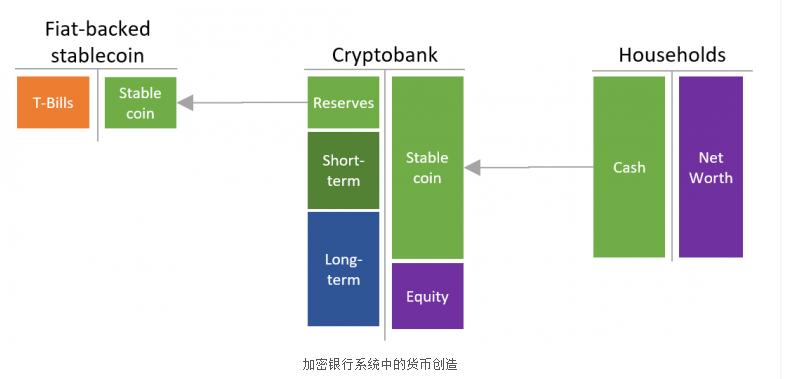

To address this issue, a fractional reserve system is introduced to expand the cash supply based on long-term loans.

As illustrated below, through intermediaries, namely cryptocurrency banks, a small amount of fiat-backed stablecoins can be expanded through a fractional reserve system. Cryptocurrency banks issue stablecoins, which creditors consider similar to money because they can be redeemed for fiat-backed stablecoins (reserves). But herein lies the problem: there are not enough reserves to redeem all stablecoins at once. History shows that a decline in credit can lead to bank runs, but the banking system can operate for years without experiencing a run, even during economic downturns.

Money Creation in the Cryptocurrency Banking System

The cryptocurrency banking system is neither a traditional banking system (where banks hold illiquid loans), nor a market-based banking system (without maturity transformation), nor shadow banking (which is an illusion of market-based maturity transformation).

Cryptocurrency banks hold highly liquid assets, serving as a means to prevent bank runs.

Conclusion

As we have seen, building a robust cryptocurrency financial system requires three components: tokenized real-world credit (bonds), a strong cryptocurrency market for trading and lending (providing deep liquidity and price discovery), and maturity transformation by cryptocurrency banks.

At the time of writing this article, the cryptocurrency market, while not perfect, is still operational (Uniswap for lending, Aave as a money market). However, there is a significant lack of bonds. The system exists, but is primarily used for speculation.

Cryptocurrency banks like MakerDAO are already integrating with money markets using tools like D3M. MakerDAO is also helping to create bond components, including collaborations with Centrifuge in private credit and with Backed in public markets, and is proposing to issue up to $1 billion in short-term bonds.

We have never been closer to a powerful cryptocurrency banking system.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles