Messari Crypto Financing Report: Where Did the $30.3 Billion in Investments Go in the First Half of the Year?

The CeFi sector has the highest financing amount at 10.2 billion dollars, followed by infrastructure with 9.7 billion dollars.

The CeFi sector has the highest financing amount at 10.2 billion dollars, followed by infrastructure with 9.7 billion dollars.Author: Messari

Compiled by: Zen, PANews

The cryptocurrency research institution Messari recently released a report on cryptocurrency financing in the first half of 2022, jointly launched with the Dove Metrics team. This report summarizes a total of 1,199 financing events in the first half of the year across Web3, DeFi, CeFi, infrastructure, and NFTs, as well as over 4,300 active cryptocurrency investors, including institutional funds, DAOs, and angel investors.

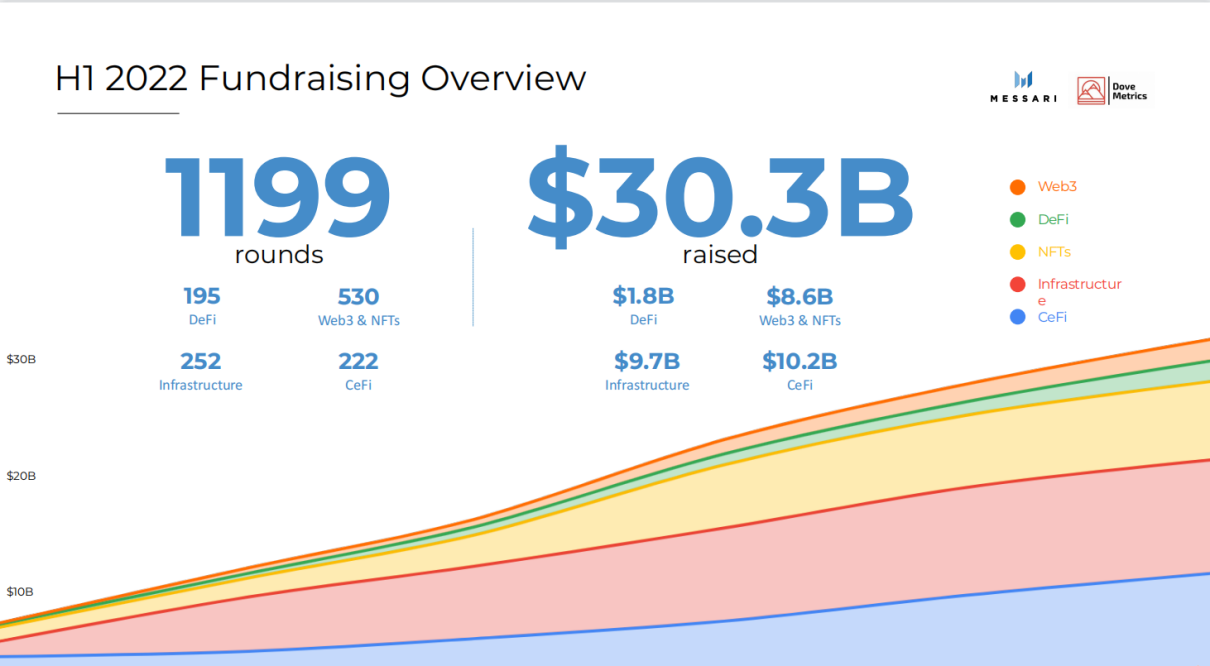

Overview: 1,199 Project Financing Events, Total Fundraising of $30.3 Billion

According to the report, 151 funds related to Web3/cryptocurrency were launched in the first half of 2022, with a total scale of $35.9 billion. Among them, there were 116 cryptocurrency funds with a total amount of $25.9 billion; 35 traditional industry funds entered the market, with a total amount of $10 billion. Correspondingly, the funding landing situation is also quite optimistic—1,199 project financing events were disclosed in the first half of the year, with a total funding scale of $30.3 billion. CeFi, which plays an important role in the industry, raised $10.2 billion through 222 public financing events (just more than DeFi's 195), making it the highest total funding amount across all tracks, with the highest single financing amount.

Compared to the first and second halves of 2021, the total amount of financing and the total number of project financing events in each track in the first half of this year have seen significant growth, mostly above 50%. Among them, the Web3 track has grown the fastest, with a quarter-on-quarter and year-on-year growth rate of 385% and 764%, respectively. It is worth mentioning that the number of DeFi financing events increased by 0.5% compared to the first half of 2021, while the total amount of funds raised in CeFi decreased by 5.6% compared to the second half of 2021.

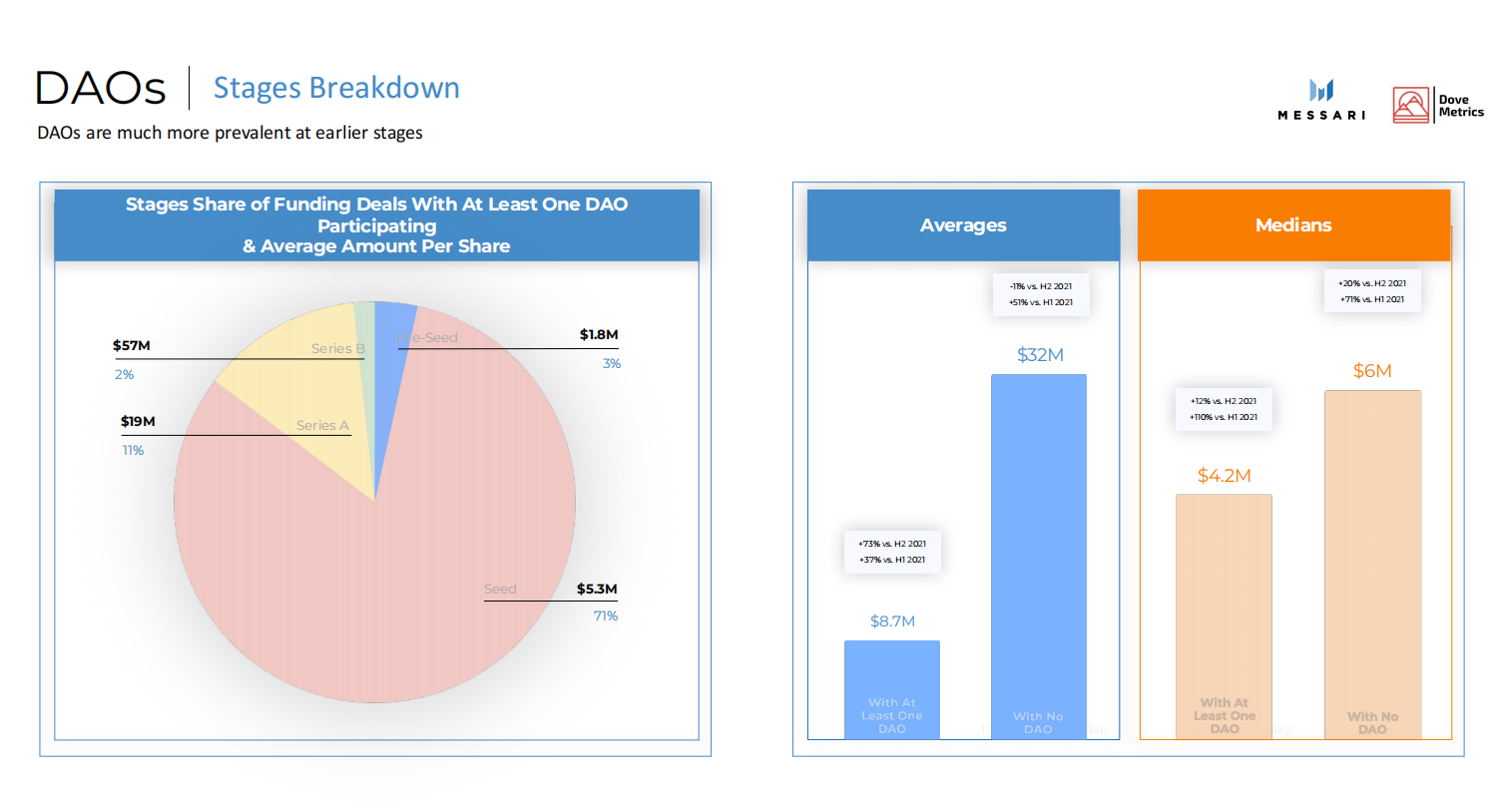

From the overall financing rounds, except for the relatively balanced distribution of financing rounds in CeFi projects, projects in various fields mainly concentrated in the early stages, which is most evident in DeFi and NFTs, where projects receiving early financing accounted for over 80%, dominating the landscape. From the perspective of investment institutions, projects invested by DAOs are concentrated in the early stages, with 71% of all investments in the seed stage.

The following will specifically introduce the financing situation in each track.

DeFi

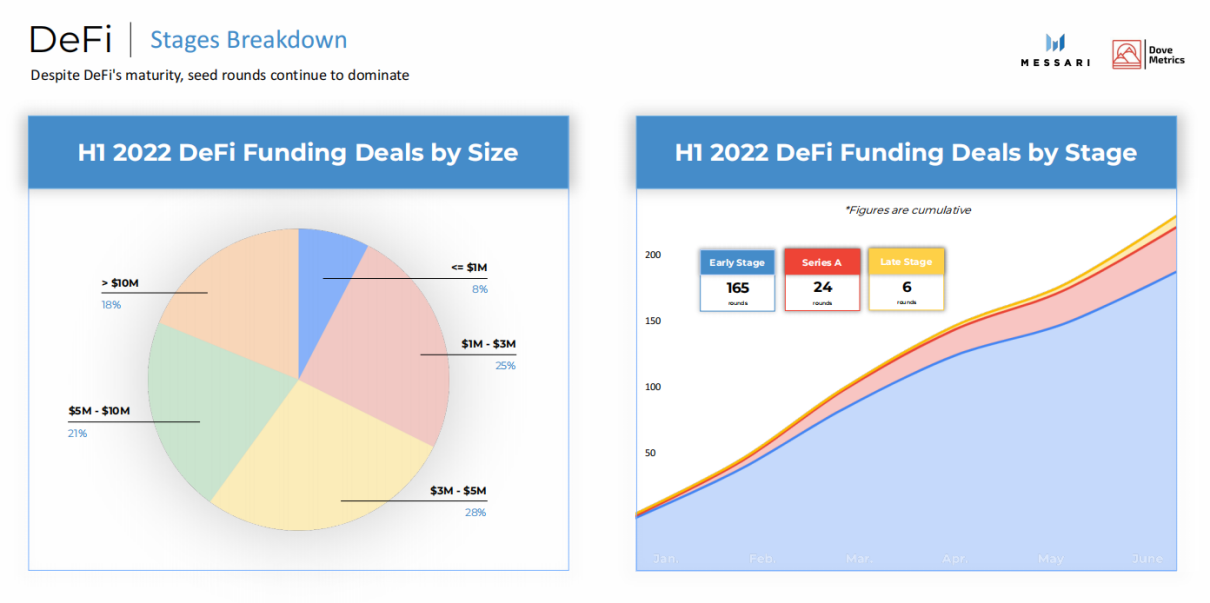

In the DeFi field, there were 195 financing events in the first half of the year, raising a total of $1.8 billion, the smallest financing scale among all tracks. Its total funding increased by 102% quarter-on-quarter and 133% year-on-year, raising $624 million in June, ending the first half of the year with strong momentum, more than double any month in the first half of this year. The projects receiving investment in DeFi are mainly concentrated in the early stages, with 165 cases; the financing scale is most concentrated in the range of $1 million to $5 million, accounting for 53% of the total. The most active verticals in this track are DEX, asset management, yield farming, stablecoins, and lending services. Currently, DeFi projects on Ethereum dominate, while other ecosystems are also continuously developing.

NFT

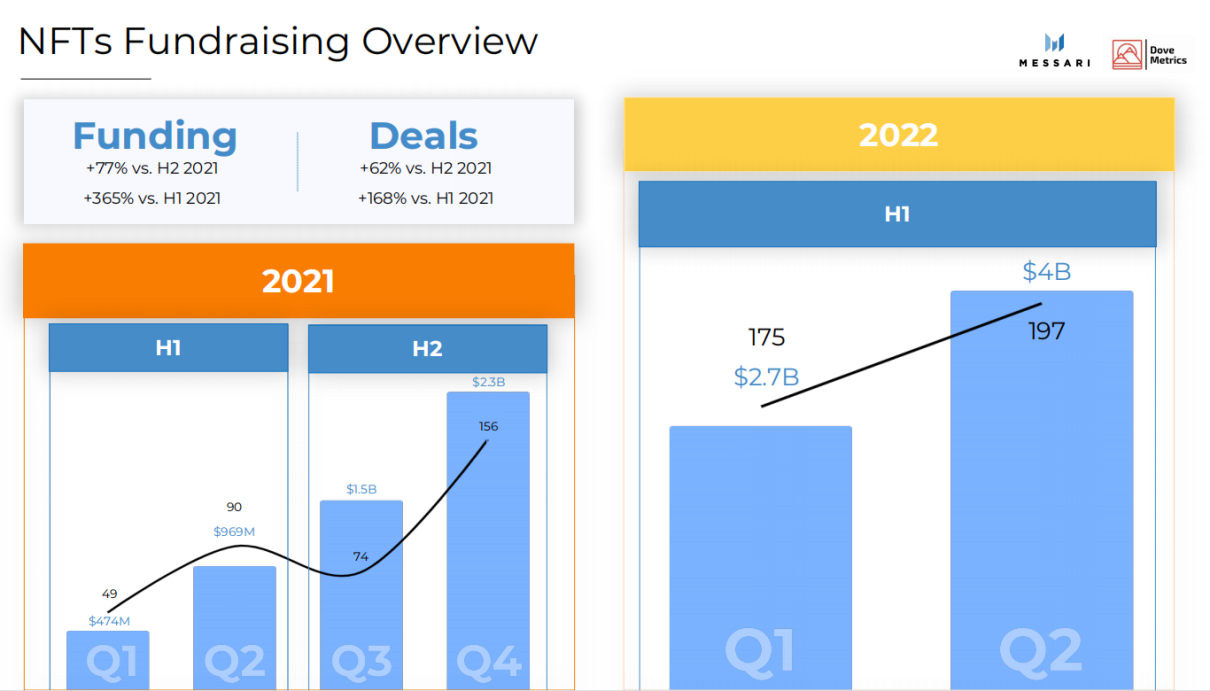

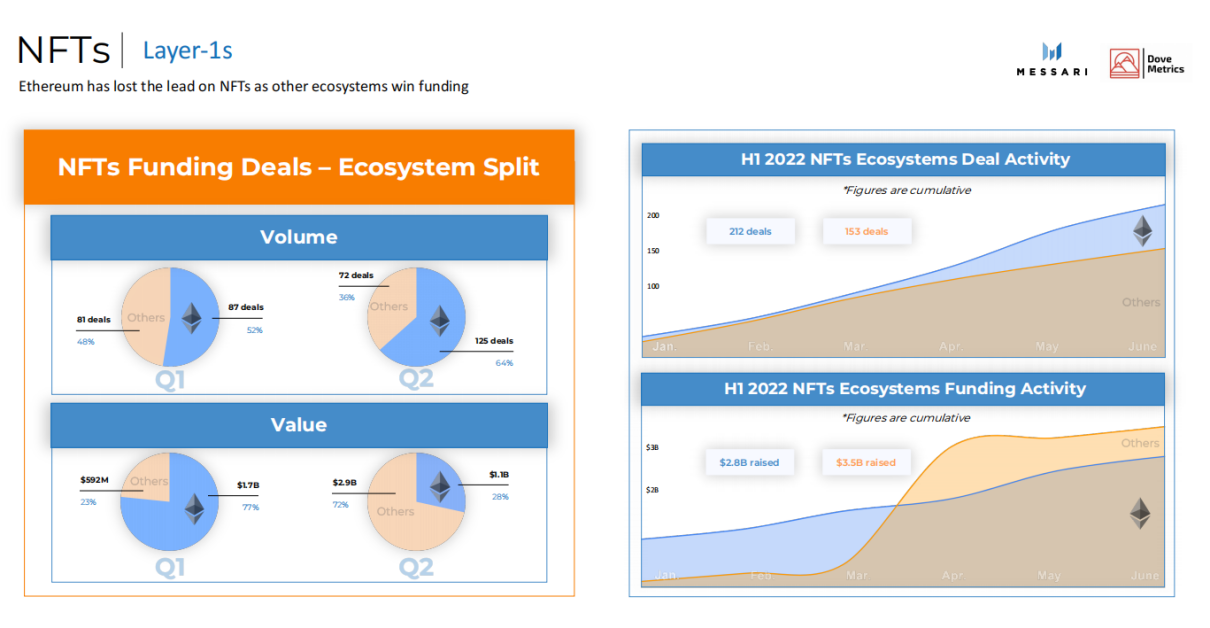

In the NFT field, there were 372 financing events in the first half of the year, the highest among all tracks, raising a total of $6.7 billion. Its total funding increased by 77% quarter-on-quarter and 365% year-on-year, with disclosed financing events increasing by 62% quarter-on-quarter and 168% year-on-year. Since 2021, both the scale of investment and the number of projects have generally maintained an upward trend in each quarter, with both metrics reaching historical highs in the second quarter of 2022, at $4 billion and 197 events, respectively. The projects receiving investment in NFTs are also mainly concentrated in the early stages, with 307 cases, and 70% of the projects have financing scales between $1 million and $10 million, while projects with financing amounts exceeding $10 million account for 22%.

It is noteworthy that game NFTs stand out in their vertical field, with a total financing amount of $4.1 billion, which is more than four times the funding raised in any other NFT vertical. Additionally, non-Ethereum NFT projects achieved a significant lead in financing scale in the second quarter, raising a total of $1.8 billion more than NFT projects in the Ethereum ecosystem.

CeFi

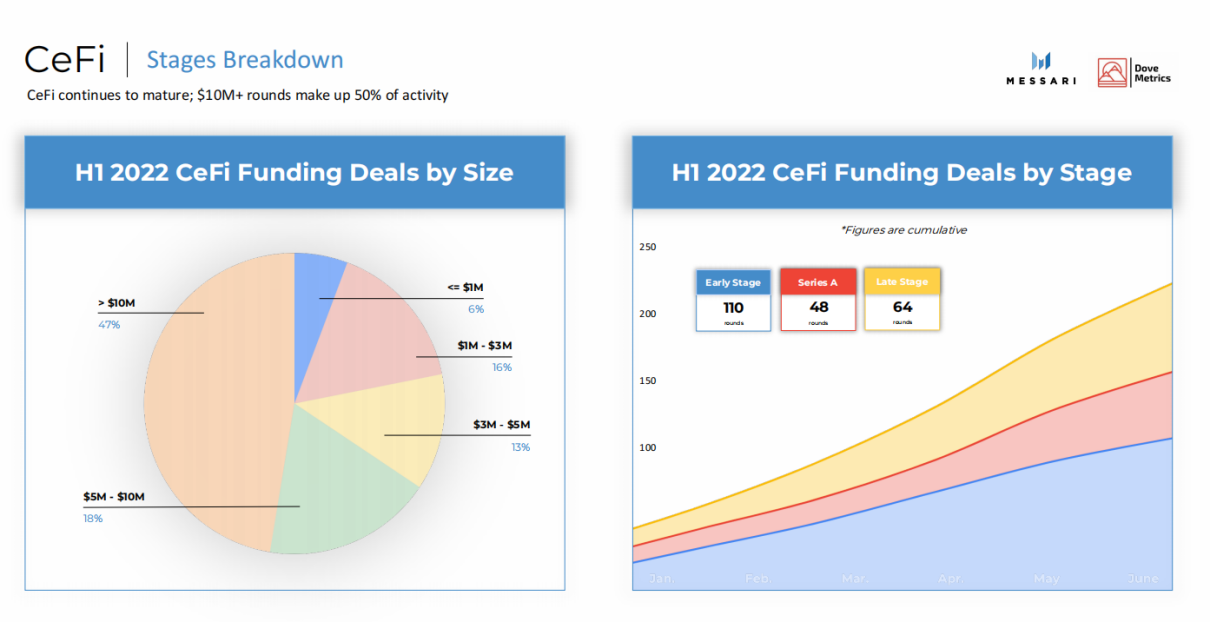

In the CeFi field, there were 222 financing events in the first half of the year, raising a total of $10.2 billion, the highest among all tracks. Its total funding decreased by 5.6% quarter-on-quarter but increased by 108% year-on-year, with disclosed financing events increasing by 40% quarter-on-quarter and 146% year-on-year. The CeFi track has a high maturity level, with a relatively balanced distribution of projects receiving investment: 110 in early stages, 48 in Series A, and 64 in later stages, with Series A+ rounds exceeding half. As the king of capital attraction in the crypto world, 47% of the projects in its financing events have a total amount exceeding $10 million. The most active vertical in the CeFi track is exchanges, with a total funding amount of $3.2 billion, more than double that of any other CeFi vertical, while other popular areas include payments, market making, savings, and asset management.

Web3

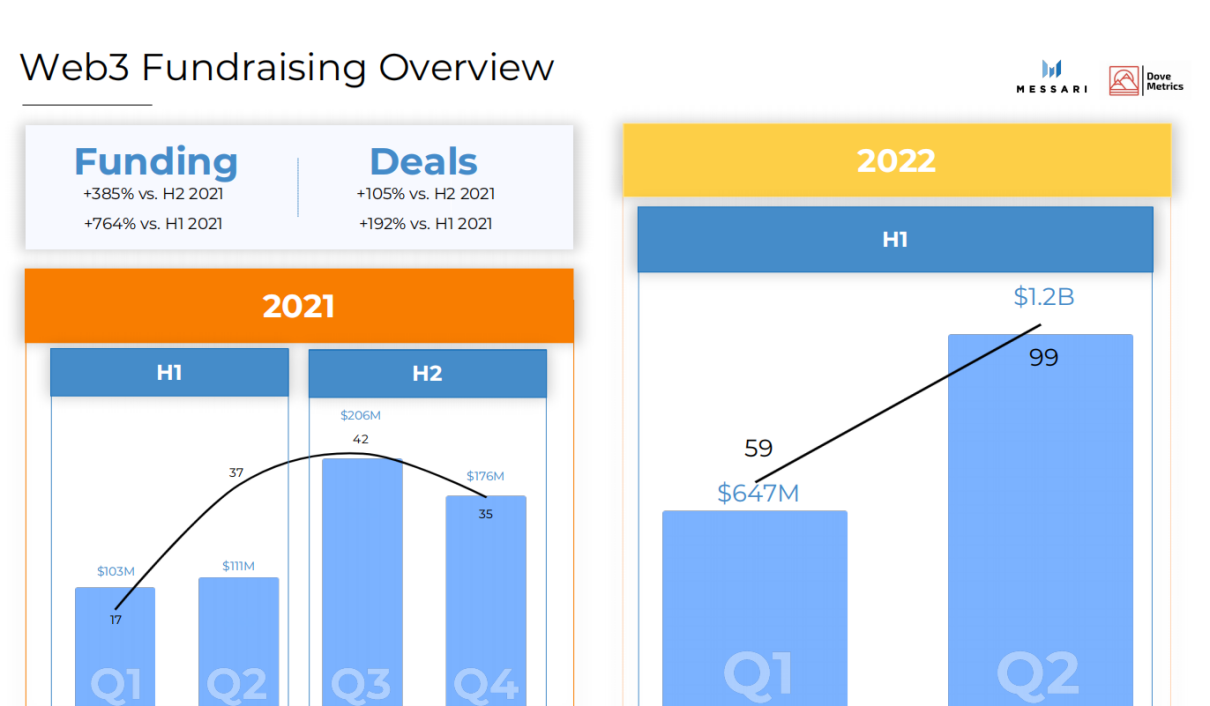

In the Web3 field, there were 158 financing events in the first half of the year, raising a total of $1.847 billion, just above DeFi. Its total funding increased by 385% quarter-on-quarter and 764% year-on-year, with disclosed financing events increasing by 105% quarter-on-quarter and 192% year-on-year, the largest increase among all tracks. Projects receiving investment in Web3 are mainly concentrated in early and Series A stages, with 112 and 32 cases, respectively, and 14 in later stages. In the first half of the year, the financing in Series A+ rounds exceeded 30% of the total, indicating that Web3 has begun to mature. Among the many verticals in Web3, investors showed the highest interest in the media and entertainment industries, which raised $529 million and $395 million, respectively, in the first half of the year, while other areas of interest include DAOs, AR/VR, and the environment.

Infrastructure

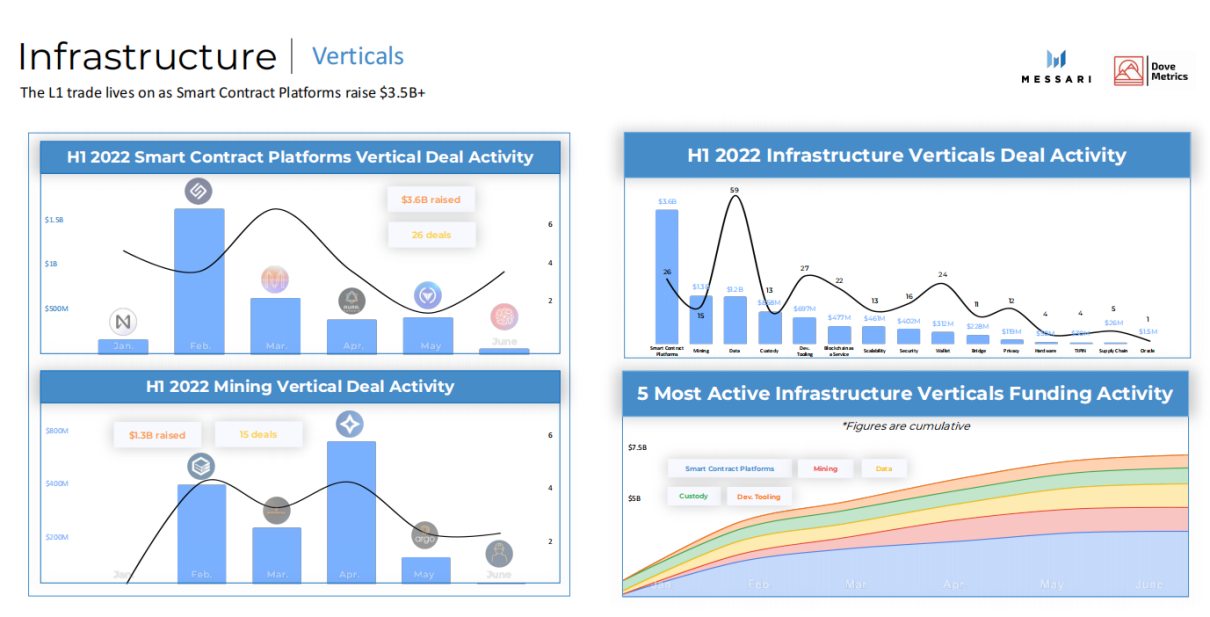

In the infrastructure field, there were 252 financing events in the first half of the year, raising a total of $9.7 billion, second only to CeFi. Its total funding increased by 131% quarter-on-quarter and 246% year-on-year, with disclosed financing events increasing by 129% quarter-on-quarter and 84% year-on-year. The financing rounds of projects in infrastructure are quite similar to those in CeFi, with 148 in early stages, 43 in Series A, and 61 in later stages, and 63% of the projects have a total amount exceeding $5 million, while 43% exceed $10 million. Among them, the total financing amount for smart contract platforms is $3.6 billion, making it the most heavily capitalized project type, ranking first among all verticals in all tracks, while other popular projects include data, custody, and mining.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles