Exploring the Microstructure of the NFT Market: What Would an Efficient NFT Market Look Like?

The discussion around the financialization of the NFT market makes some people uneasy, especially those who currently benefit from the inefficiencies of the aforementioned market. One of the core claims is that the NFT market can never be traded through quantification and algorithms.

The discussion around the financialization of the NFT market makes some people uneasy, especially those who currently benefit from the inefficiencies of the aforementioned market. One of the core claims is that the NFT market can never be traded through quantification and algorithms.Original Title: “Building Market Microstructure for NFTs”

Written by: Lao Yapi

Translated by: RR

I have been exploring the evolving market microstructure surrounding NFTs, and recent discussions about the advantages of platforms like Sudoswap have highlighted some inherent contradictions between the current NFT audience and the future of this asset class. A multitude of platforms are set to emerge, trader-oriented, bringing a more robust market structure for NFTs and other niche assets. The evolution of NFT market structure, driven by technological innovation and new financialization models, helps us understand the development trends of all markets over time.

In this article, I will emphasize why market inefficiencies exist, why market microstructure is important, and why NFTs are not immune to arbitrage. Inefficient markets will always be arbitraged by traders who see profit opportunities. Just as we have seen with Bitcoin and later tokens, the inherent digital nature of NFTs accelerates this process. I will also share some brief thoughts from a market perspective on culture as capital and the future of cultural arbitrage, as well as how efficient markets can help eliminate the fraud that is prevalent in emerging asset classes.

Inefficient Markets 101

Market inefficiency results from various factors such as information asymmetry, high transaction costs, psychology and human emotions, as well as collusion and insider trading.

Many "unique" assets like NFTs, real estate, collectibles, fine wines, and artworks are affected by inefficient markets. However, technology can enhance efficiency. With the emergence of new platforms like Zillow, Open Door, and Compass, real estate has begun to become more efficient. These new platforms minimize information asymmetry and transaction costs, developing better workflows to manage these assets at scale. This has led to more companies trading in the real estate sector. Previously highly specialized real estate investors dominated the asset class with their internal systems and processes, but the availability of more generalized tools and market infrastructure has enabled more ordinary investors to establish real estate investment strategies to capitalize on inefficiencies and market arbitrage.

The efficiency of the NFT market is also low, partly because our understanding of NFT assets is largely confined to the subjective world of "art." However, the biggest reason for the inefficiency of the NFT market is the lack of market microstructure that can enhance trading efficiency.

What is Market Microstructure?

While it sounds fancy, market microstructure is simply the nitty-gritty of how exchanges operate in a specific market. The processes, technologies, and platforms used at each stage of the exchange affect order book depth, transaction costs, clearing volumes, trading behavior, and other important market indicators. The study of market microstructure aims to understand how these trading mechanisms influence price formation.

Today, the NFT market lacks a formal, unified market microstructure, making it a challenging asset class for market participants engaged in large-scale trading. However, the tool ecosystem can make NFTs available for quantitative trading strategies such as momentum, arbitrage, and volatility, eliminating the need to pick individual pieces and enabling programmatic buying and selling at scale without needing to "evaluate" NFTs. This potentially unlocks trading volume and liquidity for NFTs.

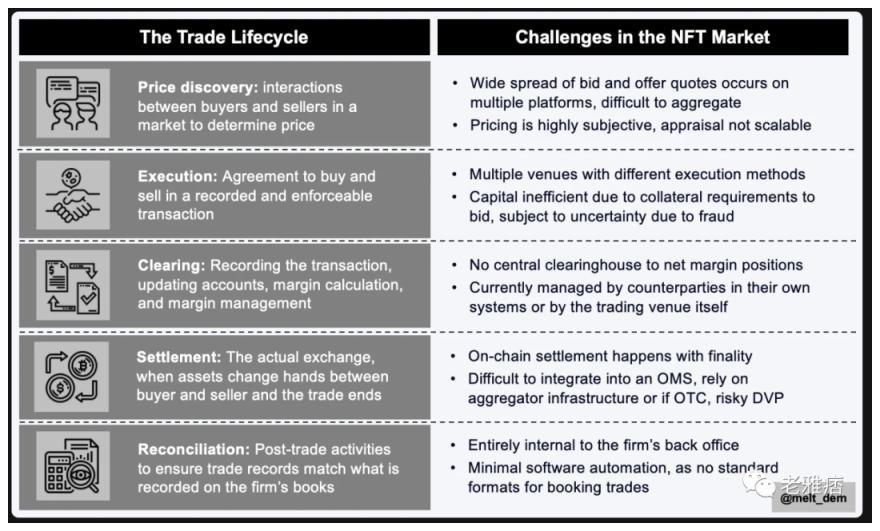

To break down market microstructure, it is helpful to understand the lifecycle of a trade at a high level. Here is a brief introduction to the trade lifecycle and some challenges in the current NFT market:

For the NFT market to grow and scale with the asset class, more protocols and platforms are needed to operate each stage of the trade lifecycle more efficiently. Ideally, these modular components should come together to form an automated, scalable workflow that allows all types of market participants to deploy various trading and investment strategies.

Today's NFT ecosystem caters to the needs of collectors and hobbyists. The future NFT ecosystem will serve a broader range of utilitarian and speculative traders through a complex set of market micro protocols and platforms. This does not mean that collectors or individuals will no longer be market participants; it simply means that the way they interact with the market will change, and as price discovery shifts, so too will the places they find advantages. This could lead to a massive transfer of wealth, benefiting early market participants and collectors, and causing the NFT market to grow exponentially in scale. This process is referred to as financialization, which is part of the evolution of every market and asset class.

NFTs Are Not Immune to Arbitrage

Discussions around the financialization of the NFT market make some people uneasy, especially those currently benefiting from the aforementioned market inefficiencies. One of the core claims is that the NFT market can never be traded quantitatively and algorithmically. I believe that most NFT market participants today are poor traders, driven by profit but inefficient and inconsistent in performance.

Arbitrage is a natural component of all markets. When traders see market inefficiencies, they design a trading strategy to profit from them and execute it repeatedly until it disappears. Early merchants took significant material and financial risks to exploit geographic arbitrage, traveling along the Silk Road with caravans laden with spices, accumulating generational wealth along the way. In 2022, savvy traders of cartoon PFPs will devise strategies to exploit NFT arbitrage, rapidly tossing JPEGs and accumulating generational wealth in the process.

The distinction between ERC-20 tokens and ERC-721 tokens is that ERC-20 tokens are fungible, while ERC-721 tokens are non-fungible. This distinction primarily serves to differentiate the functional economic use of each asset. To some extent, it may also determine the market microstructure of each asset, although over time, I expect most of this will converge, as such convergence will bring more liquidity. We see this trend accelerating as Uniswap integrates NFTs through the acquisition of Genie.

ERC-20 tokens are useful as "currencies" because they can serve as units of account and mediums of exchange, and perhaps also as stores of value. This makes it easier for us to understand and predict the evolution of these assets' market microstructure, as our current understanding of the behavior of currency and monetary assets is built on the belief in market efficiency as a positive attribute. When it comes to these assets, we do not question the arc of progress, as they conform to the psychological patterns we have had since childhood.

Due to the unique nature of each asset, ERC-721 or non-fungible tokens cannot be used as "currencies," but that does not mean they are immune to the same evolutionary curves from a market perspective. Compared to monetary assets, the cultural narratives surrounding NFTs are an effective mechanism for driving broader audience participation in the market, as culture is more interesting and often easier to understand than finance.

However, this medium does not change the information. Like all on-chain markets, NFTs have incredible benefits for efficiency-driven trading strategies.

Envisioning an Efficient NFT Market

In summary, what would an efficient NFT market look like?

Price Discovery

How do you collect data about NFTs? How do you know what the price of an NFT should be? How do you find the best pricing for your trades?

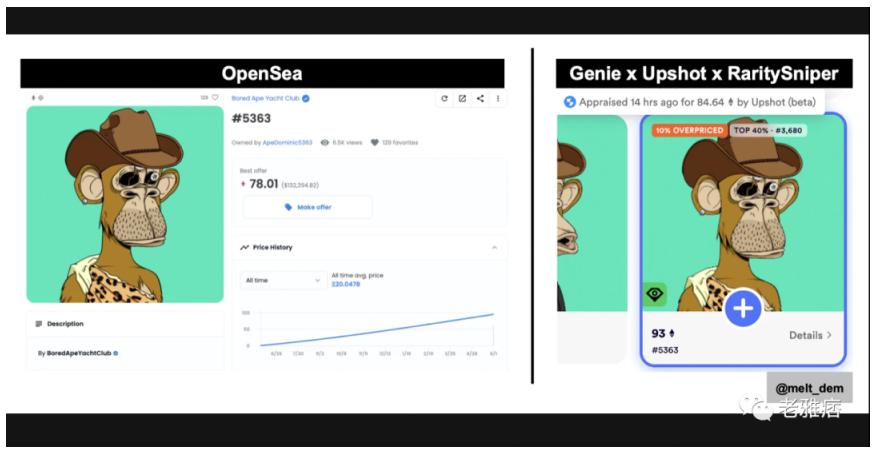

The most commonly used discovery platform today is OpenSea; however, the data provided by the OpenSea interface is quite limited, offering little insight beyond what can be collected on-chain. OpenSea also restricts your view of listings on their platform, which does not always represent the entirety of the order book.

Genie is a market aggregator that can obtain price data from multiple different markets like OpenSea and LooksRare. It not only consolidates price data from the market but also incorporates valuation data from Upshot. Additionally, there is rarity data from RaritySniper for users who still value rarity data. Note that I personally agree with the views of my two favorite NFT thinkers—if it’s not the Holy Grail, it’s the floor.

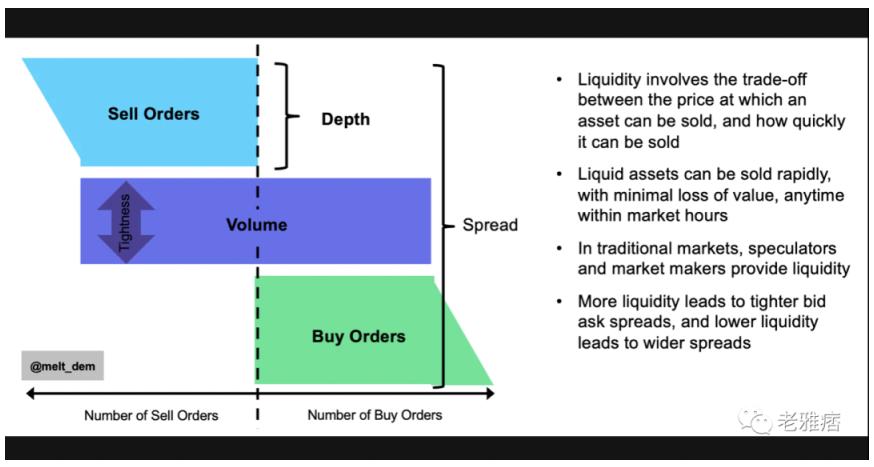

However, all data services, aggregators, and markets today focus solely on summarizing listings or sales prices. We have yet to see the development of structured data feeds or aggregators that include bids or buy offers, as well as the settlement prices of these bids, which would show market depth. Therefore, it is difficult to determine market depth. As shown in the figure below, market liquidity is determined by the depth of the order book, while prices are determined by the range of order clearances. Without understanding the price differentials across various trading venues and over-the-counter trades, price discovery is very incomplete.

Currently, there are numerous price discovery platforms under construction, each varying in usefulness to traders. Many platforms cater more to collectors, focusing on features, scarcity, and other data points lacking in actionable insights. The emergence of price discovery platforms that focus on market insights and combine asset-specific data is where miracles happen; Upshot is currently leading in implementing arbitrage trading strategies, although we have yet to see any funds or products integrating these data sets to establish a purely arbitrage-driven strategy. Perhaps someone will build such a product soon…

I also expect the OTC market to become more efficient. Just as Paradigm has provided large-scale OTC quotes for Bitcoin and other cryptocurrencies, we need a bulk RFQ platform for OTC NFT trading. I hope to be able to bid on hundreds of NFTs at once with specific search parameters by clicking a button, rather than placing hundreds of bids individually across different platforms. Perhaps on-chain messaging solutions will help make this easier; savvy snipers are already using wallet-level messaging to place bids, achieve optimal pricing, and avoid market fees.

Trade Execution

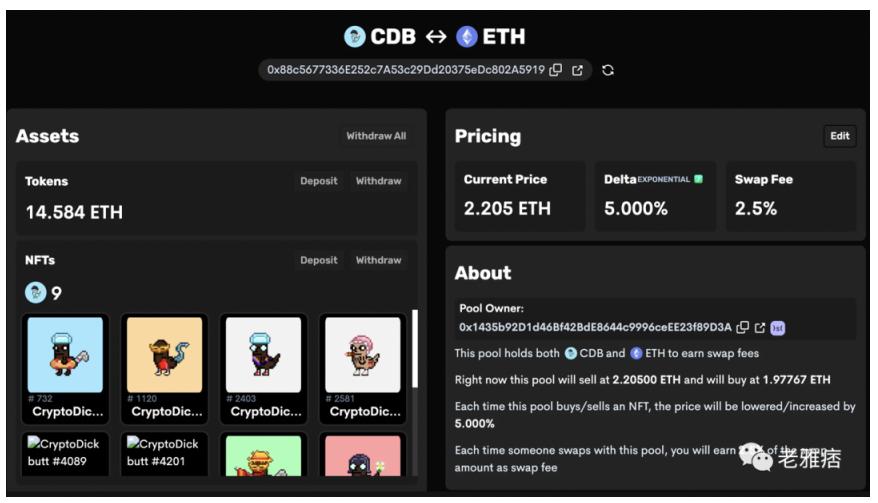

Once I have identified the asset I want to trade and am confident in price discovery, I will want to execute the trade. Many markets and aggregators today bind trade execution, price discovery, and settlement to a single interface; some NFT collections even build their own protocols or programs for trade execution. For example, LarvaLabs has directly embedded its own Cryptopunk market on its website, while EtherRocks can only be traded on the EtherRock website, as these early NFTs did not have a market when they emerged. Today, efficiency needs aggregation. Sudoswap is such a building block that simplifies aggregation and execution at scale by developing liquidity pools that allow market-making across the entire collection through responsive market dynamics.

In the example above, users can buy or sell dickbutts at an exponential bonding curve in ETH. Sudoswap also allows you to bid across all liquidity pools in a collection, meaning you can bid on multiple liquid dickbutts with a single click.

Uniswap has also added NFTs to their protocol, which is an exciting step towards the fusion of token and NFT markets, allowing more applications to leverage Uniswap liquidity. The key is to make execution simple, programmatic, and scalable, regardless of the order type.

Currently, the best solution for large-scale purchases is: (a) using OpenSea, Genie, or the soon-to-be Uniswap's Gem to scan floor prices, or (b) seeking large holders, negotiating bulk bids, and conducting DVP (delivery versus payment) settlements.

Today, there are very few OTC brokers trading NFTs, and most large trades often occur between specific collectibles and collectors. Sourcing at scale is a challenge, but I expect we will see more specialized OTC brokers and market makers emerge who will conduct large-scale trades in off-chain and on-chain NFT markets, clearing or accumulating substantial positions without impacting market prices. As always, the main challenge of OTC trading lies in the opacity of such transactions and how to integrate market data into pricing models, especially when trades are completed off-chain.

Margin and Clearing

One of the biggest limitations to NFT liquidity is the clearing and settlement process, as well as the requirement for trading venues to submit collateral when you place a bid. Suppose I want to place a bid on 100 CryptoDickbutts in a bulk bid. OpenSea would require me to wrap ETH into wETH and then post 100 bids, locking my wETH for several days. While I can post the minimum wETH to minimize capital drag, this also means I may have multiple ambiguous bids matched. This is severe capital inefficiency and could lead to suboptimal execution. To make NFTs more liquid, we need the ability to bid at scale with any other asset and reduce collateral requirements.

Perhaps integrating on-chain clearinghouses like Credora that can facilitate credit management could help drive better capital efficiency. We may see the emergence of high-quality brokers that provide short-term credit for such bids. But structurally, this issue may be one of the biggest challenges to solve, especially for on-chain trading. If NFT clearing shifts to a daily settlement model rather than an instantaneous settlement hub-and-spoke model, this process may become easier but also more centralized. Efficiency and decentralization are difficult to achieve simultaneously.

In terms of margin, platforms like NFTFi allow NFT holders to use their existing NFTs as collateral to gain more trading liquidity. The upcoming Astaria promises to provide instant liquidity for NFTs by incorporating lenders into a yield payment pool, rather than splitting it by collection. OTC trading firms and major brokers are also accepting NFTs as loan collateral; notably, Genesis accepted NFTs as collateral for loans in January 2022, lending $6 million to the NFT fund Meta4, which subsequently used those funds to purchase more NFTs. This is known as leveraging, and leverage is the lifeblood of modern financial markets.

Today, the cost of obtaining leverage is high and often occurs outside existing order processes. You must access a separate platform, transfer your NFTs to a third-party custody account, and carefully manage margin. Integrating margin directly into the trading process can help traders acquire leverage more steadily and at scale, but lenders will need better pricing oracles, which brings us back to why Step 1, price discovery, is important not just for traders.

The enormous opportunity for NFTs lies in improving capital efficiency. Systematic trading requires capital efficiency because arbitrage profit margins often decrease over time, and your profits must exceed your capital costs. For example, if you can continuously exploit 10-15% short-term price arbitrage, the cost of capital borrowing for doing so must be below 10-15%, ideally with a significant margin, so you can account for profits and make this practice worthwhile. Additionally, an important metric for portfolio managers is ROIC or "Return on Invested Capital." If I have 100 ETH but can only trade at 1x without leverage to achieve a 6% ARB, my ROIC will be far lower than if I have 100 ETH but can amplify my returns per dollar with 4-5x leverage, as the 6% ARB is now magnified several times.

Settlement and Post-Trade Reconciliation

The final step in this cycle is settling the trade, which means the exchange of assets and then ensuring that the settlement occurs as agreed, known as reconciliation. The biggest advantage of on-chain markets is instant settlement; NFTs are a significant proof point for unique markets where collectibles, artworks, and other non-standardized, high-cost, or specialized custody assets are involved. Today's NFT settlements leverage smart contracts to enable atomic swaps without the need for a trusted third party to coordinate delivery versus payment (DVP), which is a significant advantage over other types of assets. The provenance of NFTs is easily traceable, and authenticity can be verified on-chain.

Given the informal and non-standardized nature of the above steps and the lack of standardized data formats and APIs, the least structured part of the NFT trade lifecycle is reconciliation. Collecting data and integrating it into risk management or back-office systems is often a manual and labor-intensive process that requires data aggregation, cleaning, and standardization. Perhaps tools like Cryptio, which more broadly support back-office functions for crypto assets, will develop NFT reporting modules, and subsequently, real-time monitoring of positions and assigning value to them will require better pricing data—this again brings us back to Step 1, price discovery. Tracking public bids and offers, as well as any margin requirements, will require aggregating all positions into a company-wide view that can achieve real-time programmatic execution if risk parameters or thresholds are crossed.

Over time, I am optimistic that more standardized data APIs will make managing reconciliation easier without too much manual work and will facilitate the application of tax and accounting overlays, making real-time profit and loss tracking possible. For example, the widely used FIX (Financial Information Exchange) standard was developed in 1992 by the trading community to serve it, an independent electronic communication protocol. FIX has become the messaging standard for order workflow communication and regulatory reporting, and a FIX API will ensure your data is compatible with every trading, accounting, and risk management system built for modern capital markets. As a public data layer, the inherent structure of blockchain makes data extraction easier, but it is challenging to determine how best to aggregate and coordinate data between protocols, platforms, and applications before defining more formal workflows for NFT trading.

While reconciliation may seem like a fundamentally unappealing business, it is very tricky because all companies need it and build their processes around it; moreover, it can become a significant recurring revenue/cash cow business.

Conclusion

In the long run, traders may not only engage in basic trading of NFTs but also see the emergence of new synthetic derivatives or prediction markets that allow traders to make directional bets rather than trade the underlying assets. However, in the short term, the opportunities are quite apparent.

These details are not yet in place, but any trader can see what is about to happen. The microstructure of the NFT market is slowly becoming clearer and more orderly, creating opportunities for new types of market participants and operators and investors with underlying infrastructure. It remains to be seen which parts of this trade lifecycle will be established and commercialized as independent platforms or protocols, and whether any players will attempt to build or acquire the components needed to construct vertically integrated NFT trading workflows.

Many people argue that the entry of arbitrage-driven traders into the NFT space is a bad thing. The infusion of cultural capital into financial capital has been a significant trend over the past 20 years, and while this has been indirectly achieved through the rise of social media and influencers, this trend will continue to gain momentum and become more directly visible as cryptocurrency encroaches on culture.

The era of institutions is over, the era of influencers is fading, and next comes the era of degens. The Kardashians are wealthier than most hedge fund managers. Coinbase's deposits rank in the top ten among U.S. banks. Anonymous traders have built profit and loss accounts that rival those of Wall Street's most famous traditional trading firms. Soon, anonymous cartoon avatars will dominate the NFT market, flipping exquisite jpeg images of original sources.

Whether you are selling a few ETH or billions of dollars, on-chain markets have begun to create a level playing field by enabling anyone to become a market maker or liquidity provider.

As information asymmetry decreases and market structures improve, all inefficient markets become more efficient. The view that cultural capital is somehow immune to this model is at best willfully ignorant. Algorithms have determined how you consume culture. Don’t delude yourself into thinking you have taste; just look at NFTs. First, how did you discover NFTs? How many times did you buy because an NFT influencer promoted it on your homepage? Testing the cultural purity of your market participation is a good way to embrace poverty and sadness.

The consensus reached around culture creates value. With tools like Upshot, Context, and Flip, the consensus emerging in the NFT market is a pattern that can be discovered and presented through quantitative and qualitative information. Today's cultural capital has been arbitraged; it is merely being constructed by a small group of insiders behind closed doors. Why not democratize this process by providing transparency and tools to benefit more market participants?

Some may say this is dystopian, but I disagree. The market is becoming efficient, and technology is merely driving this in new ways. It could be argued that the real issue is that efficient markets do not benefit insiders—there are many frauds in inefficient, opaque markets like wine, art, and collectibles. We see this in capital markets as well—every wave of technological innovation brings some fraudsters selling access channels and insider information—we have seen this in tokens, cannabis stocks, and now NFTs. Fraud and financial bubbles will always exist; it is human nature and an inevitable part of the market, and no technology can change that (for now). Therefore, when people protest the pace of progress, it is often because they fear the structural power shifts that such change brings.

You can resist progress, or you can embrace it. History will not erect statues for critics. Investing in progress is for profit; make your choice accordingly.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles