Regulation is gradually weakening Coinbase's competitive advantage - Analysis of Coinbase Q2 financial report

Revenue diversification is the future development trend of exchanges. In addition to trading fees, the importance of subscription and service income will become increasingly significant.

Revenue diversification is the future development trend of exchanges. In addition to trading fees, the importance of subscription and service income will become increasingly significant.Author: BitMart Research, Kevin

On August 9 local time, Coinbase released its Q2 2022 financial report. The data shows that key indicators such as trading volume, revenue, and net profit for Coinbase in the second quarter have significantly declined again, resulting in losses for two consecutive quarters. After the report was released, the $1.1 billion loss clearly exceeded market expectations, causing Coinbase's stock price to plummet, with a single-day decline of over 10%.

1. Financial Report Overview

(1) Trading Volume

Trading volume is one of the most important indicators for measuring a cryptocurrency exchange. Coinbase's total trading volume in the second quarter was $217 billion, a year-on-year decrease of 53.03% and a quarter-on-quarter decrease of 29.77%. Among this, the trading volume from ordinary users (retail) was $46 billion, a year-on-year decrease of 68.28% and a quarter-on-quarter decrease of 37.84%; the trading volume from institutional users was $171 billion, a year-on-year decrease of 46.06% and a quarter-on-quarter decrease of 27.23%. In other words, both retail and institutional users experienced a significant decline in trading volume, with retail users seeing a larger drop.

Figure 1: Changes in Coinbase Trading Volume ($B, Data Source: Coinbase Q2 Financial Report)

From the perspective of trading volume share, Coinbase remains dominated by institutional users, accounting for 78.8%, up 2.75% from the previous quarter (76.05%), marking two consecutive quarters of increase in the share of institutional trading volume. When market conditions are poor, user trading enthusiasm declines, a phenomenon that is more pronounced among retail users.

Figure 2: Trading Volume Share by User Type (Data Source: Coinbase Q2 Financial Report)

The trading volume share of different cryptocurrencies has also changed significantly. Although Coinbase continues to list new cryptocurrencies, the trading volume share of BTC and ETH has increased. This indicates that users' interest in non-mainstream cryptocurrencies has decreased, with a greater preference for mainstream cryptocurrencies that carry relatively lower risks. Additionally, institutional users have stricter requirements for risk control and trading assets, which also contributes to the increase in the trading volume share of BTC and ETH.

Figure 3: Trading Volume Share of Different Cryptocurrencies (Data Source: Coinbase Q2 Financial Report)

(2) Revenue

Coinbase's net revenue in the second quarter was $803 million, a year-on-year decrease of 60.52% and a quarter-on-quarter decrease of 31.1%. Coinbase's revenue is mainly divided into two parts: trading revenue and subscription and service revenue.

Figure 4: Changes in Coinbase Revenue ($M, Data Source: Coinbase Q2 Financial Report)

Trading revenue was $655 million, a year-on-year decrease of 66.1% and a quarter-on-quarter decrease of 35.32%. The significant decline in trading volume directly impacted Coinbase's trading revenue. Among this, the trading revenue contributed by ordinary users was $616 million (accounting for 94%), while institutional users contributed $39 million (accounting for 6%). As mentioned earlier, the trading volume from institutional users is much higher than that of retail users, but the trading fee revenue contributed by institutional users is very low, indicating a significant difference in the calculation of trading fees between the two. The average fee rate for institutional users is far lower than that for retail users, approximately 1.7 times less.

Subscription and service revenue was $147 million, a year-on-year increase of 44% and a quarter-on-quarter decrease of 2.96%. It can be seen that after more than a year of development, Coinbase has made significant progress in revenue diversification. At the same time, under the market downturn, this part of the revenue has been relatively less affected, gradually becoming an important component of Coinbase's platform revenue. The share of subscription and service revenue in the overall revenue structure has also increased from 13% in the previous quarter to 18.37%, showing a significant rise.

Figure 5: Share of Coinbase Subscription and Service Revenue (Data Source: Coinbase Q2 Financial Report)

Details of subscription and service revenue are as follows. Block rewards amounted to $68 million, a quarter-on-quarter decrease of 16%, mainly due to the decline in cryptocurrency prices leading to reduced staking income. Although the number of users participating in custody has increased, custody revenue was $22 million, a quarter-on-quarter decrease of 30%, also caused by the decline in cryptocurrency prices. Revenue from the Earn campaign was $2.5 million, a quarter-on-quarter decrease of 58%. Interest income was $33 million, a quarter-on-quarter increase of 211%, a substantial growth mainly due to activities related to USDC and interest generated from custodial funds. Other subscription and service revenue was approximately $22 million, roughly flat compared to the previous quarter.

(3) Operating Expenses

Coinbase's total operating expenses in the second quarter were $1.853 billion, a year-on-year increase of 36.91% and a quarter-on-quarter increase of 7.66%. While revenue has significantly declined, operating expenses continue to grow, which has directly led to Coinbase's losses for two consecutive quarters.

Figure 6: Coinbase Operating Expenses ($M, Data Source: Coinbase Q2 Financial Report)

Among the operating expenses, trading fees were $167 million, a quarter-on-quarter decrease of 39.81%; marketing expenses were $141 million, a quarter-on-quarter decrease of 29.62%; technology R&D expenses were $609 million, a quarter-on-quarter increase of 6.75%; administrative expenses were $470 million, a quarter-on-quarter increase of 13.68%; restructuring expenses were $43 million, a new expense item in Q2; and other operating expenses were $423 million, a quarter-on-quarter increase of 63.5%.

Figure 7: Share of Various Expenses (Data Source: Coinbase Q2 Financial Report)

From the above data, it can be seen that both trading fees and marketing expenses decreased in the second quarter, while the increase in operating expenses was mainly due to the rise in technology R&D, administrative, restructuring, and other operating expenses. The increases in technology R&D, administrative, and restructuring expenses were due to higher employee costs and severance payments; other operating expenses mainly resulted from impairment of cryptocurrency assets.

(4) Platform Assets

Coinbase's total platform assets were $96 billion, a year-on-year decrease of 46.67% and a quarter-on-quarter decrease of 62.5%. According to CoinMarketCap data, a rough estimate indicates that the total market capitalization of the cryptocurrency market decreased by 60% quarter-on-quarter, roughly in line with the quarter-on-quarter decline in Coinbase's total platform assets, indicating that the decline in cryptocurrency prices is the main reason for the decrease in platform assets, with little change in the amount of cryptocurrency held by Coinbase.

Figure 8: Platform Assets ($B, Data Source: Coinbase Q2 Financial Report)

BTC accounted for 44%, slightly up from the previous quarter (42%), while ETH accounted for 20%, showing a significant decrease compared to the previous quarter (24%). Based on asset scale, asset share, and the asset prices at the time, it can be roughly inferred that the amount of BTC held by Coinbase far exceeds the 600,000 coins reported by recent media.

Figure 9: Share of Coinbase's Platform Assets (Data Source: Coinbase Q2 Financial Report)

2. Coinbase Future Outlook

As a leader in the cryptocurrency industry, Coinbase has achieved remarkable success in recent years, setting a direction for the development of compliant exchanges. However, based on the financial report information disclosed over the past two quarters, Coinbase is facing numerous challenges amid internal and external pressures, and its future development prospects are unclear.

First, Coinbase has consistently emphasized the importance of cycles in its financial reports, a point we strongly agree with. The current macroeconomic environment combined with the cyclical nature of the cryptocurrency industry suggests that the entire market will not see large-scale sustained growth in the short term. In the Q1 2022 financial report, Coinbase listed the decline in cryptocurrency prices and volatility as significant reasons for its performance decline. Although market volatility increased in Q2, Coinbase's trading volume still saw a substantial decline, which is attributed to Coinbase's singular product structure that lacks derivative trading, severely restricting its further development. In a bear market, the trading volume of derivatives will further increase, putting Coinbase, which only offers spot trading, in a more unfavorable position.

Second, Coinbase currently has 103 million users, which is a significant number for a cryptocurrency exchange. However, Coinbase's user market is relatively concentrated, with the vast majority being U.S. users. The total population of the U.S. is about 330 million, with around 100 million people holding stocks or funds. This means that Coinbase's user base in the U.S. has likely reached a bottleneck, and the possibility of large-scale growth in the future is very slim; Coinbase needs to explore other markets.

Third, compliance has always been Coinbase's greatest advantage and highlight, but the cost of compliance is also very high. In addition to product structure, Coinbase has also faced restrictions on listing new cryptocurrencies. Since Coinbase accelerated the frequency of listing new assets, the SEC's scrutiny of Coinbase has increased.

The SEC has requested Coinbase to provide documents and information regarding customer plans, operations, and existing and anticipated future products, including the process for listing assets, classifications, staking plans, as well as stablecoins and yield-generating products. Recently, seven tokens offered by Coinbase were classified as securities by the SEC, and Coinbase is also under investigation for improperly allowing Americans to trade digital assets that should have been registered as securities. To meet these regulatory and compliance requirements, Coinbase has invested a significant amount of funds and effort, which is detrimental to its innovation.

Fourth, Coinbase has made significant efforts in developing institutional users, including a recent partnership with BlackRock that boosted the company's stock price. However, institutional users contribute very little to Coinbase's trading revenue, making the results of this effort not very apparent. Coinbase itself has pointed out that retail users are trading on other exchanges, and the loss of retail users has a significant impact on Coinbase.

Fifth, mainstream investment institutions have shown reduced interest in the cryptocurrency market. Coinbase's stock price has dropped severely, falling over 70% from the beginning of the year, currently well below the opening price of $381 on its first day of listing. At the same time, the correlation between BTC and U.S. stocks and other financial assets has increased, reducing their role in diversified asset allocation, which will also affect the entry of new funds and personnel into this market.

3. Insights for the Industry

Based on July data, Coinbase has made further predictions for Q3. Coinbase believes that due to the further decline in monthly active users (retail users participating in trading and staking, MTUs) in July, Q3 MTUs may be lower than Q2, and the proportion of non-investment users among MTUs will further increase; July's monthly trading volume ($51 billion) was below the average level of Q2, so Q3 trading volume may also be lower than Q2. We disagree with Coinbase's prediction for Q3. We believe the cryptocurrency market will warm up in Q3, with trading volume and trading users exceeding Q2 levels. Coinbase's pessimism about Q3 may be due to the weakness in the U.S. market.

The revenue of exchanges mainly comes from trading fees, and when market conditions are poor, exchange revenues decline rapidly. Based on past experience, trading volume in a bear market can drop by over 90% compared to a bull market. Against the backdrop of a significant decline in revenue, if expenses are not controlled, losses can easily occur. Coinbase laid off 18% of its workforce in Q2, about 1,100 people, but the total number of employees (4,977) remained roughly the same as the previous quarter (4,948). This indicates that Coinbase misjudged the market at the beginning of Q2, failing to adjust its hiring strategy in time, continuing to hire employees, and then quickly laying them off, resulting in greater losses.

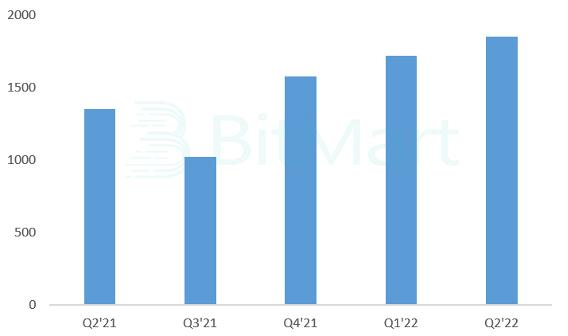

Revenue diversification is the future trend for exchanges, and the importance of subscription and service revenue will continue to grow alongside trading fees. Coinbase's MTUs did not decline significantly in Q2, one key factor being that 67% of users tried non-trading services, such as staking. At the same time, users participating in non-trading services may have a higher retention probability than trading users.

Figure 10: Monthly Trading User Count (M, Data Source: Coinbase Q2 Financial Report)

Coinbase's next five key development directions include: Coinbase Retail Platform (for retail users), Coinbase Prime (for institutional users), Staking, Developer Solutions, and Web3. This aligns with the three strategic pillars Coinbase proposed in its early years: investment platform, financial system, and application platform. Coinbase Retail Platform and Coinbase Prime are investment platforms targeting different groups.

Staking is a product of the financial system, but the sustainability of high returns from staking is questionable, and it will gradually approach mainstream investment products. Developer Solutions correspond to the application platform, and we believe this platform has significant potential, providing assistance to industry developers from various aspects such as cloud services, risk control, and payments. In Q2, Coinbase Cloud has already generated tens of millions of dollars in revenue for Coinbase. Web3 is the future direction of the industry; currently, there are not many scenarios that can be directly monetized, but it greatly aids in attracting traffic, with wallets being a key focus.

Finally, returning to the issue of regulation and compliance. There have been voices suggesting that the cryptocurrency industry needs to embrace regulation to continue to grow, which is certainly true for the entire industry. However, from an internal industry perspective, the imbalance in regulation will clearly reduce Coinbase's competitiveness compared to other leading exchanges. The cryptocurrency industry is still rapidly evolving, and exchanges need to adapt to this development and continue to innovate; being subjected to strict regulation too early is not a good thing.

Risk warning

Risk warning Risk warning

Risk warning