DeFi On-chain Fund

Overall, DeFi on-chain funds are still an untapped potential sector, with a relatively small total AUM.

Overall, DeFi on-chain funds are still an untapped potential sector, with a relatively small total AUM.Abstract

Compared to the opacity of CeFi, DeFi on-chain funds bring a more efficient and transparent asset management model.

With the continuous maturation of on-chain exchanges, lending, and various derivatives platforms, DeFi on-chain funds have sufficient investment space and feasibility for practical development. By customizing smart contracts to set operational scopes, combining multi-signature with permission control, and layering automated algorithms and other technical means, DeFi on-chain funds can effectively integrate the advantages of security, transparency, and high efficiency. Although the overall scale of DeFi on-chain funds is still small, especially for actively managed strategy funds, there is significant growth potential in the future.

The variety of on-chain assets is constantly enriching, providing DeFi on-chain funds with more diversified investment portfolio targets.

The emergence of new on-chain assets and derivatives such as LP liquidity provider tokens, perpetual leveraged contracts, and perpetual leverage pools brings more combinability to DeFi on-chain funds, enabling diversified hedging to mitigate risks and providing users with safe, transparent, and balanced risk-return financial products.

Lowering user entry costs and the trend of packaging complex financial products is evident.

During our research, we clearly observed a trend where platform-based projects began to build or collaborate through ecosystems to create clearly packaged, easy-to-understand financial products that do not require frequent user operations, such as the Vault constructed by Umami Finance and Opyn's Crab Strategy.

After verifying the security of on-chain funds, wallets will be an ideal traffic entry point.

Similar to the logic of Web2 financial brokerage software, pushing fund products on wallet pages is a reasonable trend. For funds, it represents a channel for traffic and capital, while for wallets, it can generate revenue rather than relying solely on transaction fees from sending trades. However, for wallet users, the security of funds is crucial. Trading scenarios are one-time events; as long as the trading process is problem-free, wallets bear no responsibility. However, if an on-chain fund product encounters an incident, the consequences can be severe. Currently, the entire sector is still in its early stages, so more time is needed to verify product security.

Intro

The cryptocurrency market is always fraught with risks and opportunities we cannot imagine. In May, the top ten cryptocurrency project Luna saw its market cap of hundreds of billions drop to zero in a week, triggering a wave of collapses among institutions such as Celusis, 3AC Capital, Babel Finance, and BlockFi, affecting millions of people and hundreds of billions of dollars in assets.

The fundamental reason lies in the lack of regulation in the cryptocurrency investment field, where the asset conditions of various companies are opaque, and mutual borrowing continues in an optimistic market. Leverage accumulates outside the regulatory framework, and risks accumulate in the shadows. Luna ultimately became the match that ignited a series of explosions, even threatening centralized exchanges that have experienced two rounds of bull and bear markets. The subprime mortgage crisis in 2008, while affecting a broader scope, had fundamentally similar reasons.

This article will explore and analyze a track in the DeFi field that has yet to explode: on-chain funds/asset management, starting from the traditional financial fund management industry.

We collected nearly 60 projects from the market, filtered, categorized, and organized them, and selected 22 projects that meet the definition for analysis, with in-depth analysis of three representative projects: Ribbon Finance, Umami Finance, and iZUMi Finance.

Fund Introduction

Anyone on the street can name a few well-known fund names, and the operation of "funds," which pools small, public investors into large funds, actually emerged two hundred years ago.

The emergence and vigorous development of new things often require the demand of the times. The essence of finance is to enhance the efficiency of capital utilization, and funds, as a socialized financial tool, can achieve more efficient resource allocation, originating from the capital needs brought about by the development of the real economy.

In the nineteenth century, Britain had just experienced the first industrial revolution, with significant productivity growth, colonies and trade spread across the globe, and rapid wealth accumulation. However, the general public heard similar myths but struggled with a lack of relevant knowledge and understanding of the overseas investment environment, leading to the idea of entrusting funds to relevant professionals for management. Meanwhile, some merchants and sailors had sufficient relevant experience but lacked financial support. Subsequently, the British government supported this idea, establishing investment companies to entrust specialized financial experts to invest on behalf of small and medium investors, allowing them to share in the returns from international investments and diversify risks. In 1868, Britain established the "Overseas and Colonial Government Trust" organization, publishing a prospectus in The Times to publicly sell stock certificates to society.

Funds originated in Britain but saw the most rapid development in the United States. After World War I, the U.S. economy grew rapidly, transforming from a capital-importing country to a major capital-exporting country. In 1926, the Massachusetts Financial Services Company in Boston established the "Massachusetts Investment Trust," becoming the first modern mutual fund in the United States. However, the rapid development of the U.S. fund industry in the 1920s saw total assets grow at over 20% annually, even exceeding 100% growth in 1927, followed by the Great Crash of 1929.

After experiencing the crash and the impact of World War II, the U.S. government enacted comprehensive laws such as the Securities Act, Securities Exchange Act, Investment Company Act, and Investment Advisers Act, laying a solid foundation for the development of the U.S. financial industry.

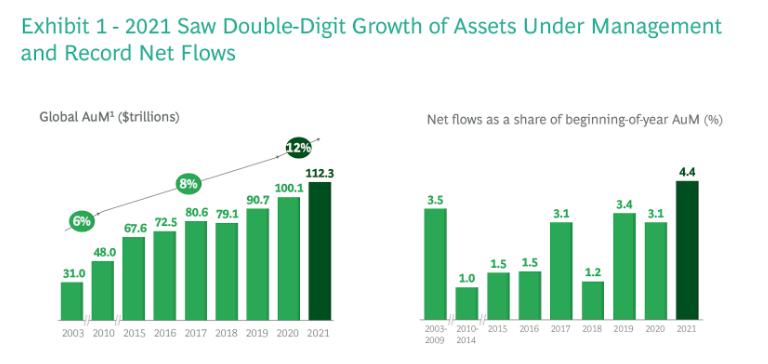

With the continuous development and improvement of the financial system, the fund or asset management industry has also flourished. By 2021, asset management (capital) had become a trillion-dollar market, growing rapidly at an annual rate of up to 12% in recent years. Additionally, the share of passive investment has rapidly increased, reaching one-third in 2020, indicating a growing preference among investors for passive financial management and investment strategies that diversify risks through portfolio strategies.

Data source: https://www.bcg.com/publications/2021/global-asset-management-industry-report

Funds raise capital by issuing fund shares, pooling investor funds to form independent property, which is managed and utilized by fund managers through a portfolio approach for securities investment, sharing benefits and risks in a collective investment manner.

Why Are Funds So Popular?

Funds broaden investment channels for small and medium investors, operating through experts to help many small and medium investors with portfolio investments. By converting savings and idle funds into investments, funds release social capital, providing momentum for industrial development and economic growth. In this process, investors earn returns, society releases idle funds, and fund managers receive income related to performance.

Moreover, the development of funds managed by professional investors also contributes to the stability and development of financial markets. Generally, funds tend to focus more on long-term strategies, with less frequent trading, thus reducing volatility in the securities market. Similarly, a stable financial market creates a more stable and predictable financing environment for enterprises.

As a new type of asset, cryptocurrencies have reached a market value of trillions of dollars in just over a decade. The management of crypto assets has also seen the emergence of completely different methods from traditional finance. Currently, most crypto assets are still managed using traditional fund operation methods, governed by the current legal system, regulatory organizations, and assessment institutions. However, based on decentralized, permissionless blockchain networks and smart contract technology, a more efficient and transparent fund operation method has been continuously explored and developed in recent years. These methods treat code as law, eliminate intermediaries, and combine emerging on-chain assets to provide higher efficiency, lower risk, and more diversified financial products.

DeFi On-Chain Funds

DeFi applications have rapidly mimicked traditional finance in just five years, introducing tiered funds, futures, options, and various derivatives, mixed with various innovations such as perpetual options and liquidity provider tokens (LP), covering a very broad scope. Here, we will limit the discussion to "DeFi on-chain funds" for ease of research and discussion, defined as follows:

Project parties/fund managers invest user funds (mainstream tokens such as BTC/ETH/mainstream stablecoins) based on pre-agreed strategies, using fully on-chain operations to invest in one or several types of decentralized financial products to achieve asset appreciation for users.

Expanding this definition, the following standards must be met:

Regarding users:

Based on the anonymous and open characteristics of DeFi, any user can participate in investing in the fund, although some on-chain funds may have whitelist features.

Returns and investments:

The product's goal is for it to appreciate in mainstream coin terms, either on its own or in conjunction with other products. Here, returns are in mainstream coins, not in more volatile altcoins obtained through staking or other activities (some platform tokens may be included as incentives, but the primary income is from mainstream tokens). Thus, fund products can capture long-term returns through strategies rather than short-term gains from economic model inflation.

Regarding operational permissions and scope:

Permissions are controlled by smart contracts, with all operations conducted on-chain, interacting with a set of other contracts specified by the agreement or operating a combination of assets defined by the contract. Operations on-chain ensure transparency of funds, rather than being invested in CeFi or CEX for opaque operations. Permissions are controlled by the contract, defining the scope of operations to ensure the safety of funds.

What is the Market Space for DeFi On-Chain Funds?

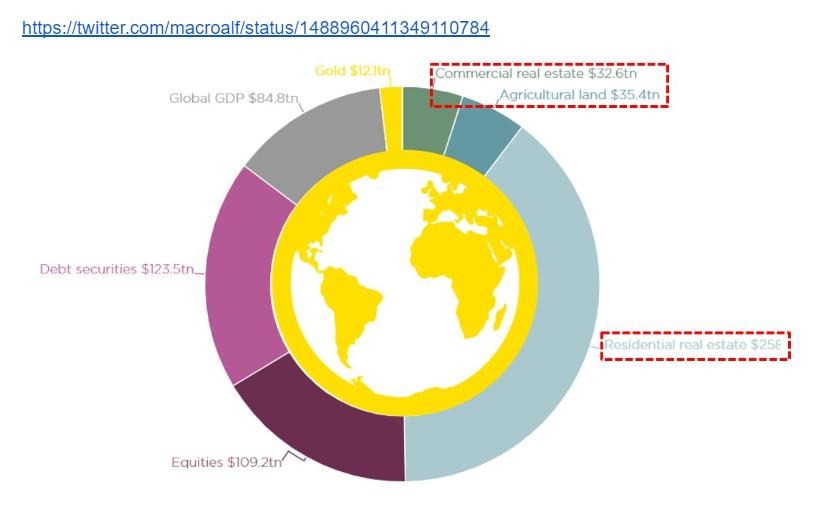

Currently, global funds manage a total of $112 trillion in assets. According to data from Twitter KOL Alf, the global stock market is $109 trillion, the bond market is $124 trillion, gold is $12 trillion, and digital assets are less than $2 trillion. According to Investopedia, the derivatives market has a scale of about $600 trillion. If we assume that 10% of assets are managed by various funds, with 30% managed in the form of on-chain funds, then based on the current $1.2 trillion market cap of the cryptocurrency market, $36 billion in assets would enter on-chain funds, while the current scale of on-chain funds is far below this amount.

https://twitter.com/macroalf/status/1488960411349110784

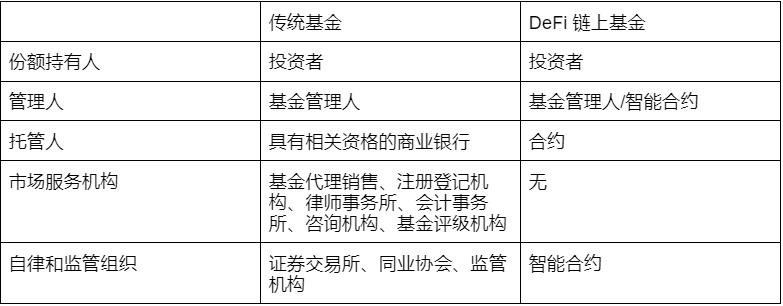

Comparison of Ecological Roles Between Traditional Funds and DeFi On-Chain Funds

The traditional fund industry has developed a complete ecological industrial chain, including front-end services, back-end rating and certification, as well as relevant legal and regulatory systems. In contrast, DeFi on-chain funds currently lack standards, certifications, and related upstream and downstream services, and at present, they only have certain advantages in asset transparency and efficiency brought about by the elimination of intermediaries due to technological advantages.

Classification of DeFi On-Chain Funds

Traditional funds are classified based on fundraising methods (public, private), operational methods (closed-end, open-end), investment philosophies (active, passive), legal forms (contractual, corporate), trading methods (on-exchange, off-exchange), investment targets (stocks, bonds, currencies), and many other criteria. However, whether in DeFi or traditional finance, regardless of the underlying asset or framework, strategies are the most fascinating part. Therefore, we will classify based on strategies and analyze 15 projects collected from the market across multiple dimensions.

The classification is as follows:

First, the products will meet our definition of "DeFi on-chain funds," and then be categorized into three types based on the specific execution of strategies: algorithmic strategy funds, active strategy funds, and passive strategy funds, defined as follows:

Active strategy funds: Fund managers/teams use their expertise to conduct on-chain operations within the scope defined by the contract to pursue returns that exceed market averages. Examples include DeFiEdge Protocol, Arrakis Finance, etc.

Algorithmic strategy funds: Users invest funds, and the contract automatically executes based on defined algorithms and strategies to help users build structured asset portfolios or execute repetitive operations. Typical products include Yearn.Finance and Ribbon Finance products.

Passive strategy funds: Primarily index funds, diversifying investments in a certain type of asset or tracking the performance of certain/multiple assets, providing users with broad market exposure, low operating costs, and low portfolio turnover rates. Typical products include DeFi Pulse Index (DPI), Metaverse Index, ETH 2x Flexible Leverage Index, etc.

Risk from high to low: Active strategy funds > Algorithmic strategy funds > Passive strategy funds

Returns: Active strategy funds > Algorithmic strategy funds > Passive strategy funds

Active Strategy Funds: Contracts as Law, Crafting Diamonds with Precision

Active strategy funds are relatively simple, with mechanisms basically defined by contracts that specify the investment scope. During the deployment of the fund pool, the operational range is set, and fund managers can only operate within the pre-defined scope, such as lending on large platforms like Aave or Compound, or providing liquidity for a specific trading pair on Uniswap V3.

These funds are closer to traditional fund models, charging certain management fees and commissions. Currently, these funds are relatively small in scale but have significant growth potential.

Algorithmic Strategy Funds: Combining Newborn Assets, Algorithms Shine

Algorithmic strategy funds are more diversified compared to the other two types. Yearn Finance and Beefy Finance belong to the algorithmic strategy fund category (this type is referred to as "yield farms," and there are relatively many projects, so they are not listed here). Algorithmic strategy funds tend to be more innovative, combining more new DeFi assets, such as liquidity provider tokens (LP), perpetual contracts, etc., and hedging with other long/short leveraged products, becoming fund products that approach neutral strategies. These products generally offer higher returns and lower risks.

Shares of algorithmic strategy funds are generally not tradable, but they can be deposited or withdrawn at any time or after periodic settlements.

Passive Strategy Funds: Constructing Synthetic Assets, Automatically Anchoring Targets

Passive strategy funds typically issue ERC20 tokens to represent fund shares, with invested funds buying and selling corresponding assets according to rules during adjustments. Platforms attract users to purchase index funds through staking rewards in the form of platform governance tokens or incentivizing liquidity for the ERC20 trading pairs on DEX. Platforms allow users to trade fund shares in the market, making them closer to ETFs, and can achieve arbitrage through minting and redeeming shares.

Typical Project Examples

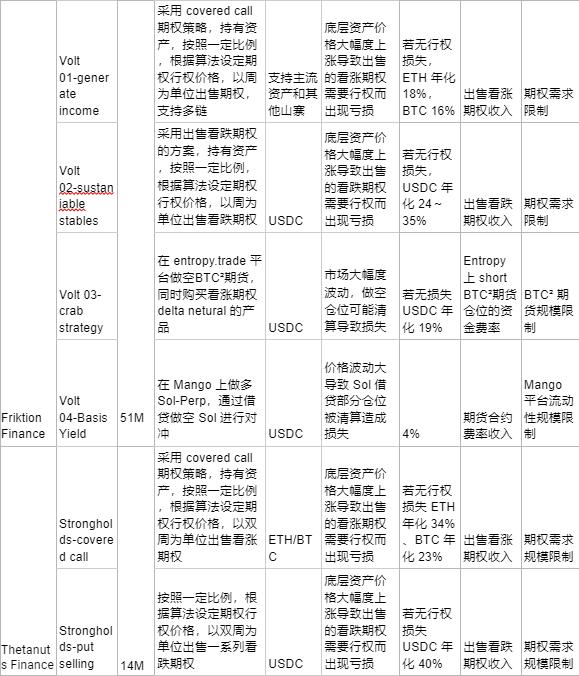

Ribbon Finance - On-Chain Automated Strategies Based on Options

https://docs.google.com/document/d/1yxfUIG5sc_tr9eFma_aZfeaAvxogNlBC6Guoz4Idlpk/edit

Ribbon Finance is a DeFi structured product based on Opyn's early options products, with the entire process of minting, selling, and exercising options occurring on the Ethereum chain. Currently, the structured products launched include Covered Call (holding stock protection strategy) and Put Selling strategy (unprotected bearish), with contracts deployed on Avalanche, Solana, and Ethereum. As of early August 2020, it had over $70 million in AUM on Ethereum, making it the largest in its category.

After investors deposit funds, Ribbon Finance sets the option strike price through algorithms on the Opyn platform and mints option oTokens, selling options on multiple platforms every Friday. If the options are not exercised, they can earn premium income, providing returns to investors. In the future, Ribbon's main trading products will cover options, futures, fixed income, etc. (currently mainly options products), helping users improve the risk-return of their funds.

Core Products & Design Principles

Ribbon Finance's current core product is called Theta Vault, which includes Covered Call and Put Selling strategies, totaling 12 products.

Ribbon Finance's Covered Call involves holding the corresponding cryptocurrency and selling call options on that cryptocurrency every Friday to earn premium income. Put Selling is the opposite strategy, where investors deposit USDC and sell a certain number of put options every Friday to earn returns.

The algorithmic strategy sets a fixed Delta value, incorporating current market volatility factors into the calculation. In Ribbon Finance V1, the team manually calculated the option strike price based on delta=0.1. In V2, the contract reads the current spot price from Chainlink and automatically calculates market volatility, combining the pre-set delta value to automatically compute the strike price. All options have a validity period of one week.

Additionally, in the latest version, Theta Vault combines with Yearn Finance, investing idle funds into Yearn Finance to add a small portion of risk-free returns. All operations on Ribbon are executed through smart contracts, making it a typical algorithmic strategy fund.

Risks and Returns

Whether selling call or put options, the way to earn returns is to hope that the options are not exercised (and thus expire) at settlement. From Ribbon's historical performance, since January 2020, less than 5% of the time have options been exercised (resulting in losses). Due to the high volatility of the altcoin market, options are often exercised, with funds primarily being covered call strategies on altcoins.

Overall, in the absence of extreme market conditions, Ribbon Finance can indeed provide users with appreciation in coin terms. If not exercised, Ribbon Finance can offer users annualized returns of 34% for ETH, 27% for BTC, and 50% for USDC. However, considering the volatility of the crypto market, overall returns are not ideal, with the BTC fund currently yielding 6.05% in coin terms over the year, Ethereum at 3.38%, and USDC at -28%.

Considering the design of Ribbon's product mechanism, the Covered Call strategy is more suitable for bear markets, avoiding the risk of call options being exercised due to rapid price increases, thus earning some coin-based returns. In bull markets, the Put Selling strategy using USDC is more appropriate to avoid the risk of put options being exercised due to rapid price declines.

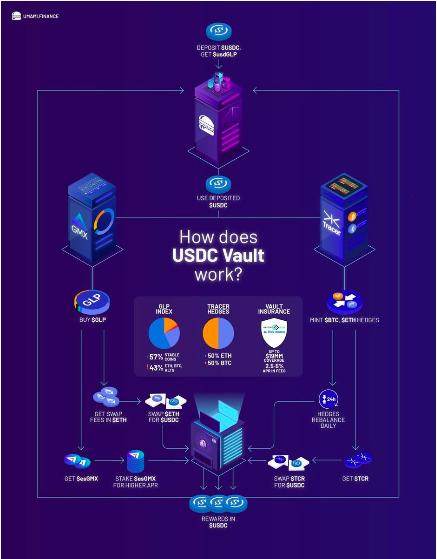

Umami Finance - High-Yield Hedge Fund Based on DeFi Innovative Assets

https://docs.google.com/document/d/1xFyKV04C_ShZC85D-h-hFfIH1BYqiPPx6l_SGfq_Xh8/edit

Introduction: Umami Finance closed this fund project on August 19 and is currently researching a second version. The closure was due to deviations caused by the Mycelium leveraged token algorithm during significant market fluctuations, where the performance of short tokens did not meet expectations when hedging against downside risks. Ultimately, the team chose to close this project and compensate affected users with team funds.

Umami Finance initially operated as a decentralized financial reserve platform similar to Olympus DAO on Arbitrum, launching the GLP and Mycelium (formerly Tracer DAO) Perpetual Pool USDC fund - GLP/TCR USDC POOL last month. By combining GLP and the Perpetual Pool for risk hedging, it achieved approximately 20% annualized returns in USDC.

Source: Umami Finance Documentation

Underlying DeFi Lego Modules: GMX's GLP and Mycelium's Perpetual Pool

GMX is a decentralized perpetual contract exchange currently deployed on the Arbitrum and Avalanche networks, which are not interoperable. GLP serves as a liquidity provider within the GMX ecosystem, acting as a counterparty for contract and spot trading, providing liquidity for various trading scenarios on the GMX platform. In GMX, trading occurs without slippage, directly exchanging based on Chainlink's quotes, with the counterparty's funds coming from GLP and subject to limits based on the size of the GLP pool.

Here, Max ETH in and Max USDC out refer to the limits set when exchanging ETH for USDC (or during contract trading).

Additionally, as trading amounts increase, fees will also rise, ranging from 0.3% (for small trades) to 0.8% (for large trades).

GLP is provided by users and includes a basket of asset combinations, with proportions set by the platform. Users can mint GLP using any asset from the basket. To maintain proportion stability, minting GLP incurs fees, incentivizing users to mint with the missing assets to keep the GLP pool balanced. For example, if the amount of WBTC in the GLP pool is significantly below the set proportion while ETH is above, minting GLP with ETH incurs additional fees, while minting with WBTC reduces fees.

70% of the revenue from activities such as trading, minting, and burning GLP, leveraged trading, and liquidation (collectively referred to as Platform fees) will be distributed to GLP in ETH. The remaining distribution goes to the governance token GMX. GLP can also participate in staking to earn GMX rewards.

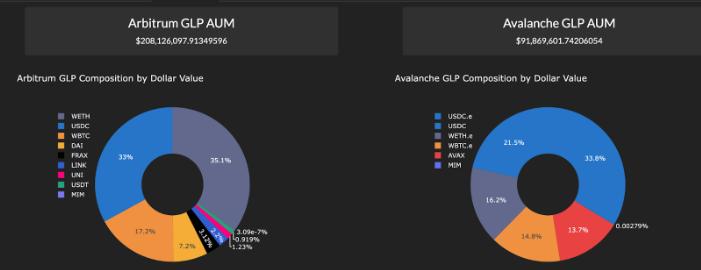

Since GLP is a basket of assets at a certain ratio, its unit net value will fluctuate with token price changes. The following chart shows the composition of GLP.

Composition of GLP (August 7, 2022)

GLP Net Value Change Curve (August 7, 2022)

GLP Net Value Change Curve (August 7, 2022)

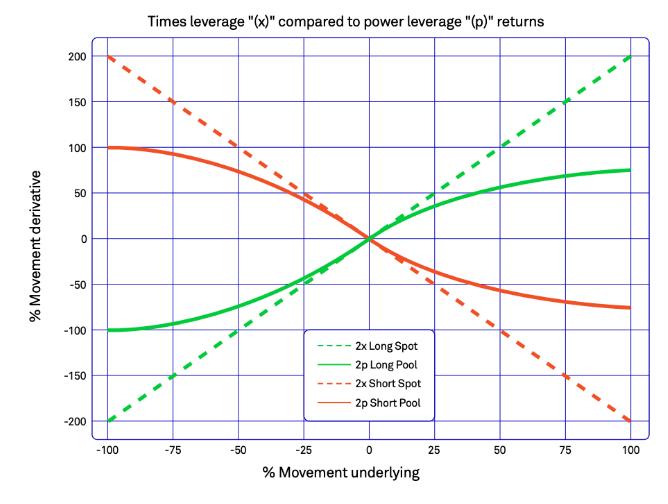

Mycelium's Perpetual Pool (formerly Tracer DAO)

Taking the 3x leveraged token as an example, Mycelium has built 3x long and 3x short tokens, allowing users to mint long or short tokens directly using USDC. Long/short tokens represent shares of the long/short pools. Mycelium periodically adjusts the ratio of the two pools based on Ethereum's price. If the asset price rises by 1%, the threefold leveraged pool will automatically transfer 3% of funds from the short pool to the long pool during adjustments, thus creating a non-liquidatable leveraged product.

The pool's adjustments follow the curve shown below (the chart uses 2x leverage as an example), with the horizontal axis representing changes in the underlying asset's price and the vertical axis representing the amount of funds transferred between pools. It can be seen that the larger the price change, the more difficult it is to adjust the leverage accurately.

Additionally, an arbitrage model is employed to maintain balance between the two pools, and a portion of the fee is extracted to trigger the contract for stable operation of the product.

Umami's Strategy:

As seen above, GLP contains approximately 40% volatile assets (mainly BTC and ETH, along with other tokens like Uni) and over 50% stable assets (primarily USDC). Therefore, purchasing GLP is equivalent to holding this basket of asset combinations, while also having future GMX platform fees as cash flow income. Thus, Umami's Vault uses Mycelium's threefold leveraged tokens to hedge the volatile asset portion proportionally (Mycelium only supports ETH and BTC but has hedged most of the risk), aiming for stable returns. The contract adjusts once daily to ensure the accuracy of the hedge quantity.

Additionally, a small amount of funds is used to purchase GLP insurance from the insurance platform Insurace to avoid unexpected losses due to hacker attacks and other incidents.

Risks and Returns:

Umami's product takes various risks into account, including purchasing insurance on Insurace and Riskhabor to avoid sudden security incidents with GLP, as well as using Mycelium to hedge GLP's risks. However, due to underlying product mechanism issues, risks still exist:

Risks from Mycelium: Mycelium periodically rebalances the allocation of long/short pools to maintain leverage, but the curve used by Mycelium is an approximation. If large-scale price fluctuations occur, Mycelium cannot guarantee that the pool allocations are completely even.

Additionally, there are other contract-related risks associated with Mycelium. Currently, Umami's insurance does not cover the Mycelium portion.

If large-scale withdrawals or deposits of GLP cause an imbalance in proportions, Umami's rebalancing every 9 hours incurs additional costs.

Based on on-chain data, at the current scale, each 9-hour rebalancing incurs about 1% of the fund, and the fees paid to GMX and Mycelium during the rebalancing process could significantly reduce the final user returns. If the GLP proportion becomes uneven, purchasing costs will increase, leading to higher expenses.

Professionally Managed Closed-End Active Fund - iZUMi Finance

https://docs.google.com/document/d/1bsaxgztJtk8ciXW8BfBlkz55RyhWEKsTEkC_zesUR0E/edit#

iZUMi Finance is a multi-chain one-stop liquidity service platform that offers various products centered around liquidity services, including liquidity incentive tools like the liquidity box and efficient decentralized exchanges like iZiswap. iZUMi Finance is about to launch three products: fixed-income bonds, dual-currency wealth management, and impermanent loss insurance.

Both fixed-income bonds and dual-currency wealth management fall under DeFi on-chain funds and belong to the active strategy fund category. Compared to the previously mentioned fund products, iZUMi Finance offers closed-end funds that cannot be traded after purchase and can be redeemed with principal and interest upon maturity.

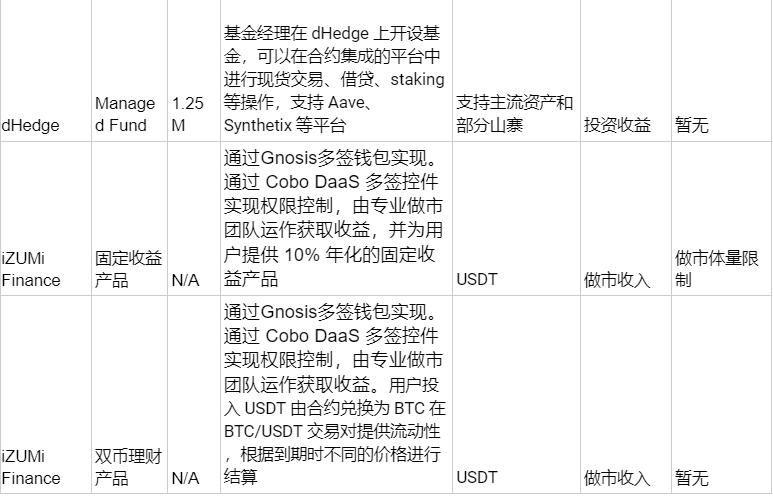

iZUMi Finance Fixed-Income Products

iZUMi Finance's fixed-income bonds are implemented through a Gnosis multi-signature wallet. Permission control is achieved through the Cobo DaaS multi-signature widget, allowing a party to perform operations within a pre-defined range, such as trading on Uniswap and adjusting price ranges on V3.

The bond products offered by iZUMi Finance have a term of 30 days, providing an annualized return of 10% when invested in USDT, with principal and interest paid at maturity. The funds raised from the bonds are used to provide liquidity in decentralized exchanges, with strategies provided by a professional trading team.

The multi-signature wallet is jointly managed by iZUMi Finance and LPs, with liquidity provision and price adjustment permissions only granted to the Market Maker (MM) team. At the end, funds are extracted with signatures from all three parties. The bond yield is fixed at 10% APR, with any additional returns going to the Market Maker. If LP returns are insufficient, the Market Maker will cover the shortfall with margin.

iZUMi Finance Dual-Currency Wealth Management Products

Another wealth management product from iZUMi Finance is dual-currency wealth management, which carries slightly higher risks and returns compared to bond products. The product invests USDT, allowing users to choose a lock-in period of 1/7/30 days, with funds used to provide liquidity for the BTC/USDT trading pair on DEX.

The final assets returned depend on market prices. When purchasing the product, a price range is set, and during investment, the contract automatically trades a% of USDT for BTC at market prices to provide liquidity within that price range.

If the price remains within the set range at redemption, users can withdraw liquidity corresponding to the principal and earn annualized returns of 50% to 150%. If the price exceeds the upper limit, users can receive USDT corresponding to the liquidity tokens above the price range. If the price falls below the lower limit, users can receive BTC corresponding to the liquidity tokens below the price range.

Compared to other active strategy funds, in addition to maintaining the security and transparency of on-chain funds, iZUMi Finance's products are more flexible due to professional team operations and can provide stable returns that are largely independent of market bull and bear cycles, making them relatively competitive.

iZUMi Finance Impermanent Loss Insurance Products

After users provide liquidity on Uniswap V3 and receive liquidity proof NFTs, they can deposit these NFTs into the iZUMi Finance impermanent loss insurance product's smart contract. The contract automatically calculates the amount to hedge and related fees, with the insurance market lasting for 30 days. The contract will automatically allocate a portion of LP fee income as the cost of purchasing insurance. iZUMi Finance will provide impermanent loss insurance for users through a combination of hedging strategies on CEX. Settlements occur when the insurance expires or liquidity exits the set price range, paying users their premiums. By purchasing impermanent loss insurance, users can avoid impermanent loss while providing liquidity, thus earning stable market-making fee income.

All three products from iZUMi Finance are innovative attempts, with the first two classified as DeFi active strategy on-chain funds, while the insurance product combines CEX strategies, with all calculations and payments for impermanent loss being transparent and verifiable on-chain. Currently, iZUMi Finance's incubated project Glass Finance has joined the first phase of the Cronos Accelerator, and we look forward to the upcoming product launch.

Advantages of DeFi On-Chain Funds

Asset transparency and security: Asset operations are fully traceable on-chain, reducing opaque operations. Whether active, passive, or algorithmic strategy funds, the holdings and adjustments of the funds are real-time verifiable. Moreover, most funds allow for withdrawal at any time, providing good protection for user funds.

New asset combinability: On-chain funds like Thetanuts Finance, Index Coop, and Cook Finance have issued corresponding ERC20 tokens as certificates representing fund shares, allowing participation in other staking activities and potentially serving as certificates for lending activities in the future.

Diversity of investment targets: Traditional funds consider risk control and only allow investments in permitted asset categories, such as money market, equity, and bond funds. DeFi on-chain funds can invest in a more diverse range of targets, including interest-bearing tokens, perpetual contracts, leveraged tokens, liquidity provider tokens, etc. By combining and hedging different new products, they can form low-risk, high-return (stablecoin returns exceeding 20%) products that carry a certain amount of risk. However, compared to Luna's Anchor Protocol, which provided around 20% stable returns, these products have stable sources of income and controllable risks.

Deficiencies of DeFi On-Chain Funds

Excessive transparency: This can make them vulnerable to attacks from malicious counterparties, such as artificially inflating option prices, leading to losses for some algorithmic strategy funds. The layering of assets can accumulate risks.

High operational costs: Some automatically running strategy fund products require frequent on-chain operations, resulting in high transaction fee expenditures.

Imprecise calculations: DEXs using AMMs find it challenging to make precise estimates during trading. Additionally, designs like Mycelium's simulated leverage curves can also experience significant deviations during volatile market conditions, leading to additional losses and expenditures for funds.

Contract risks: On-chain fund products are often combinations of multiple assets, linked to several smart contracts, with funds held in smart contracts. If any contract encounters issues, it can impact the entire product. However, most fund products currently allow users to purchase insurance policies from platforms like Insurace or Riskhabor to hedge certain risks. Umami Finance's USDC Vault product even directly includes an Insurace policy.

Product complexity: Compared to centralized financial products, DeFi fund products still have a high entry threshold. This includes not only a smaller user base and complex, difficult-to-use DeFi products but also various sources of fund returns and operational principles. For example, understanding the composition and risks of Opyn's Crab Strategy requires knowledge of perpetual contracts and Opyn's Squeeth products.

Innovative products have yet to stabilize and require time for validation: Umami Finance used Mycelium's leveraged tokens for hedging, hoping to hedge the volatile asset positions in GLP without liquidation risks. However, Mycelium's mechanism is designed to adjust every 8 hours, which can lead to deviations during significant market fluctuations, resulting in substantial losses for Umami's USDC Vault between August 18 and 19. Ultimately, Umami decided to close this Vault and compensate the gap with team funds. Such innovative products using on-chain algorithms still carry significant, unverified risks that require time for validation.

Trends and Opportunities:

Platform-developed fund products: During our research, we found that DeFi trading platforms are developing financial products based on their platforms, packaging them so that users only need to understand the existing risks and returns without needing to manipulate the funds themselves. A typical example is Opyn's Crab Strategy built on its Squeeth.

Combining DID will be the future direction for active strategy funds: In an anonymous environment, even with smart contracts ensuring fund security, users find it difficult to trust active strategy fund products. Most fund projects, such as DeFiEdge, are relatively early, and the platforms themselves cannot provide sufficient credit endorsement for fund managers. Some projects use Twitter account associations, but the effect is relatively limited. If DID can be combined to provide actual performance records of fund managers on-chain and confirm that they indeed operate the funds, it could enhance the credibility of the products and potentially lead to the emergence of fund ratings in anonymous environments.

The demand for stable liquidity from DEXs: DEXs like GMX and Uniswap hope to have sufficient and stable liquidity. Funds launched by Umami Finance, DeFiEdge, etc., can help DEXs provide long-term, stable liquidity support. Additionally, for Umami Finance's products, combining liquidity and leveraged tokens for hedging provides users with high-yield financial products, effectively benefiting all four parties (Umami Finance, GMX, Mycelium, and investors).

Opportunities for fund marketing channels: Using wallets as entry points or aggregating entry points similar to traditional brokerage software and financial pages can horizontally compare various on-chain fund returns and risks, helping users reduce decision-making costs and directing traffic to reliable DeFi on-chain fund products.

Conclusion

Overall, DeFi on-chain funds remain an underexplored track with significant potential, with a relatively small overall AUM. However, innovative products like Umami's USDC Vault and Opyn's Crab Strategy still face supply shortages, indicating that market demand indeed exists. The market's high volatility and speculative activities are typical of early-stage markets, and many on-chain fund products face challenges due to market conditions and inadequate infrastructure.

Compared to traditional fund models, the standards, operational processes, models, and ecological roles of on-chain funds are still in very early stages, with many ecological roles even missing. We look forward to seeing more builders emerge with more explorations and ideas to construct a more robust DeFi ecosystem in the future.

Risk warning

Risk warning Risk warning

Risk warning