Detailed Explanation of NFT Lending Pool Liquidation Mechanism: How to Avoid BendDAO-style Liquidity Crisis?

In the depths of the bear market, can we expect NFT-Fi to improve the liquidity of NFTs? Currently, the answer is not so optimistic. In a cooling market environment, these protocols that initially aimed to "improve NFT liquidity" are facing severe challenges.

In the depths of the bear market, can we expect NFT-Fi to improve the liquidity of NFTs? Currently, the answer is not so optimistic. In a cooling market environment, these protocols that initially aimed to "improve NFT liquidity" are facing severe challenges.Author: Nianqing, Chain Catcher

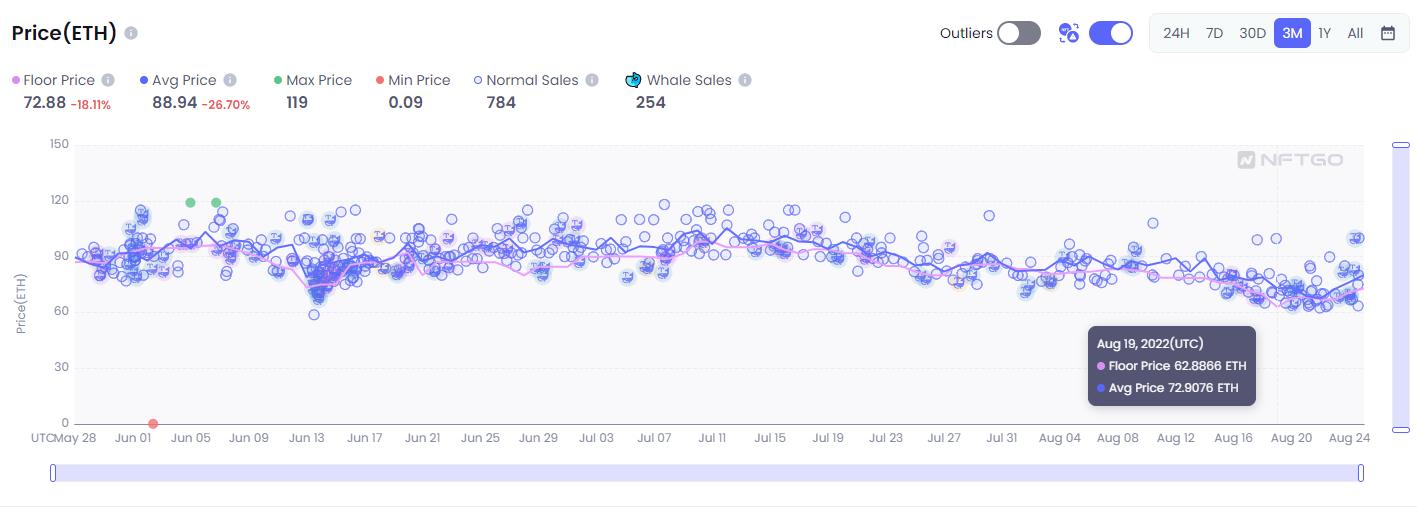

Recently, with the NFT market cooling down, even blue-chip NFTs like Bored Apes have struggled under pressure, with the floor price continuously declining since August. On August 19, the floor price dropped to 62.8 ETH, triggering a liquidation on BendDAO, the NFT collateral lending protocol with the highest number of listed Bored Apes.

*Chart of BAYC floor price and average price changes over the past three months, data source: * NFTgo

In just three days, 28 BAYC and 28 MAYC were liquidated, while dozens of Bored Ape NFTs had health factors less than or equal to 1.1, trembling on the edge of liquidation. Even the Bored Ape NFT of BendDAO co-founder @CodeInCoffee was on the verge of liquidation.

The "liquidation crisis" caused considerable panic, with depositors quickly withdrawing their assets from the liquidity pool, even triggering a bank run. In just a few days, the balance in BendDAO's ETH lending pool dropped from over 16,000 ETH to nearly depleted. This also triggered a series of chain reactions, as BendDAO collateralized nearly 3% of the entire Bored Ape collection, forcing both the BAYC and MAYC floor series to face downward pressure, leading to further declines in floor prices.

The market began to worry whether this would further trigger a "death spiral" effect in the NFT lending sector. How did this "liquidity crisis" arise? For a detailed account of the events, refer to 《From a 300-fold surge to triggering chain liquidations of blue-chip NFTs, what has BendDAO experienced?》.

Although the liquidity crisis at BendDAO has been temporarily overcome, we must question whether surviving this small storm means that the NFT lending pool model is safe and sound. Do other NFT lending pools' liquidation mechanisms still harbor potential risks, and can they withstand the test of extreme market conditions?

In this article, we will systematically outline the liquidation mechanisms of several major protocols in the NFT lending pool model, including BendDAO, JPEG'd, Pine Loan, and Drops DAO, as well as how users can assess and control risks from their perspective.

1. Peer to Peer Lending Model (P2P) VS Pool Model (P2Pool)

First, we must clarify a concept: NFT lending currently includes both Peer to Peer (P2P) and Peer to Pool (P2Pool) models. BendDAO, which triggered the liquidity crisis, belongs to the pool model, and following the incident, several similar P2P lending projects like NFT-Fi began to "promote" their P2P model as superior to the pool model.

In the P2P model, NFT holders need to negotiate acceptable prices with lenders, and then the lending platform facilitates the transaction. For example, the process is similar to listing on Xianyu, where holders pledge their NFTs to the lending platform, specify the amount they wish to borrow, the term, and the interest to be paid. Lenders can browse various NFT lending information on the platform and submit the loan amount and interest they are willing to provide. Representative projects include NFTfi and Arcade.

Lenders only need to repay on time to avoid liquidation risks. However, if the loan is not repaid by the due date, the pledged NFT will be transferred to the lender from the smart contract. Since the transaction is limited to the two parties involved, even if a default occurs, the risk will not further escalate.

In the pool model, holders can immediately borrow funds after over-collateralizing their NFT assets into a liquidity pool, and the entire process is similar to using platforms like Aave or Compound. NFT pricing is determined by the average floor price over a recent period. The interest amount paid by NFT owners depends on the amount borrowed and the remaining funds in the pool. If NFT owners fail to repay or if the NFT price falls to the liquidation line, the NFT will be publicly auctioned, and the funds will be returned to the lender. The market for NFT lending protocols using the pool mechanism is more crowded compared to P2P, with BendDAO, DropsDAO, JPEG'd, XCarnival, Pine, Pilgrim, etc., all belonging to this model.

However, just like DeFi protocols such as Aave and Compound, liquidation is a routine operation in lending. In extreme market conditions, liquidation, selling pressure, and bad debts are inevitable paths for new projects.

2. How Should the Liquidation Mechanism of NFT Pool Models Be Set Up?

This article mainly outlines the liquidation mechanisms and current development status of four leading protocols in the NFT pool model (BendDAO, DropsDAO, JPEG'd, and Pine).

1. BendDAO

What was BendDAO's liquidation mechanism before this crisis?

BendDAO uses a straightforward metric, the "health factor," to assess the current lending situation. The health factor is a numerical representation of the safety of the collateralized NFT relative to the borrowed ETH and its underlying value; the higher the value, the safer the funds are, and the better they can withstand liquidation risks. Its calculation formula is:

Health Factor = (Floor Price * Liquidation Threshold) / Debt with Interest

Additionally, another key value is the Loan-to-Value (LTV) ratio (Loan Amount or Debt Value / Collateral Market Value), with BendDAO's maximum LTV set at 40%. Currently, BAYC and CRYPTOPUNKS have the highest collateralization rates, close to 40%. Users can set the amount they wish to borrow, with lower borrowing prices resulting in higher health factors.

Assuming you pledged a BAYC priced at 150 ETH (usually the floor price) and borrowed 60 ETH, according to BendDAO's previous liquidation threshold of 90% (similar to LTV, Debt Value / Collateral Value), if the floor price drops to 66.67 ETH, it would trigger a 48-hour liquidation protection and auction of the NFT collateral, as your NFT loan's health factor falls below 1.

For example, this time, when the BAYC floor price fell below 65 ETH, it triggered the liquidation of some pledged NFTs. The health factor depends on the collateral's liquidation threshold and the loan amount; the lower the loan amount (debt with interest), the higher the floor price, and the lower the liquidation threshold, the higher the health factor.

BendDAO's NFT calculation data comes from OpenSea and LooksRare, with collateral values denominated in ETH rather than USDT. The initial 48-hour liquidation protection was mainly set up to protect the pledger, allowing borrowers (users with pledged NFTs) to repay the loan within 48 hours to redeem their collateral.

Moreover, to protect pledgers, the auction conditions are relatively strict: 1. The bid must exceed 95% of the floor price; 2. It must be greater than the total accumulated debt; 3. It must be higher than the previous bid plus 1% of the debt.

BendDAO co-founder @CodeInCoffee acknowledged in a community proposal, "When setting the initial parameters, we underestimated the illiquidity of NFTs in a bear market."

After the proposal, BendDAO modified its liquidation mechanism: the liquidation threshold was gradually adjusted from 90% to 70% to reduce bad debts; the auction period was changed from 48 hours to 4 hours to prevent excessive price fluctuations over time, stimulating asset liquidity; the ETH benchmark interest rate was adjusted to 20%, and the 95% floor price and first bid restrictions were removed, while the storage interest rate was adjusted to 20% to encourage ETH depositors to provide liquidity.

In fact, in the early design of BendDAO's mechanism, there was consideration for extreme situations where the floor price drops but no liquidators participate in the auction. However, the team believed that short-term fluctuations in NFT floor prices were normal, and blue-chip NFT consensus is not built in a day, nor will it collapse in a short time. Therefore, the platform only faced temporary floating losses without actual losses. Either the borrower would repay the debt at some point in the future, or some liquidators would appear to participate in the auction of the debt after the market price rebounded.

However, the biggest problem BendDAO faces is that the liquidation price is lower than the debt price, leading to an inability to liquidate, while being stuck in the predicament where no one is willing to buy back the NFT when the liquidation price exceeds the debt price. Thus, the NFT category ultimately can only include blue-chip projects.

Why did BendDAO first show a yellow light this time?

Cobo Ventures researcher Walon Lin believes that the key issue in BendDAO's liquidity crisis is not the setting of LTV and liquidation thresholds, but the later requirement that liquidators' bids must exceed 95% of the floor price and be greater than the total accumulated debt, which lacks incentives for liquidators, resulting in the failure of liquidated NFTs to be auctioned. Additionally, BendDAO uses a direct liquidation model, unlike JPEG'd, which has a priority liquidation mechanism set up for the DAO treasury, where the DAO treasury first buys the liquidated NFTs and then disposes of them.

However, this model relies on the DAO being confident in the market prospects of that NFT series, believing that this batch of assets can be absorbed by the market to ensure the stability of the treasury's funds. Therefore, this model requires strong risk control capabilities and a sufficiently strong consensus on the NFT.

The awkward situation faced by BendDAO's liquidation model is that many large NFT holders have poor liquidity with their Bored Apes, and since they cannot sell them, they simply seek a suitable exit mechanism within the lending protocol, effectively passing the liquidity risk onto the liquidators.

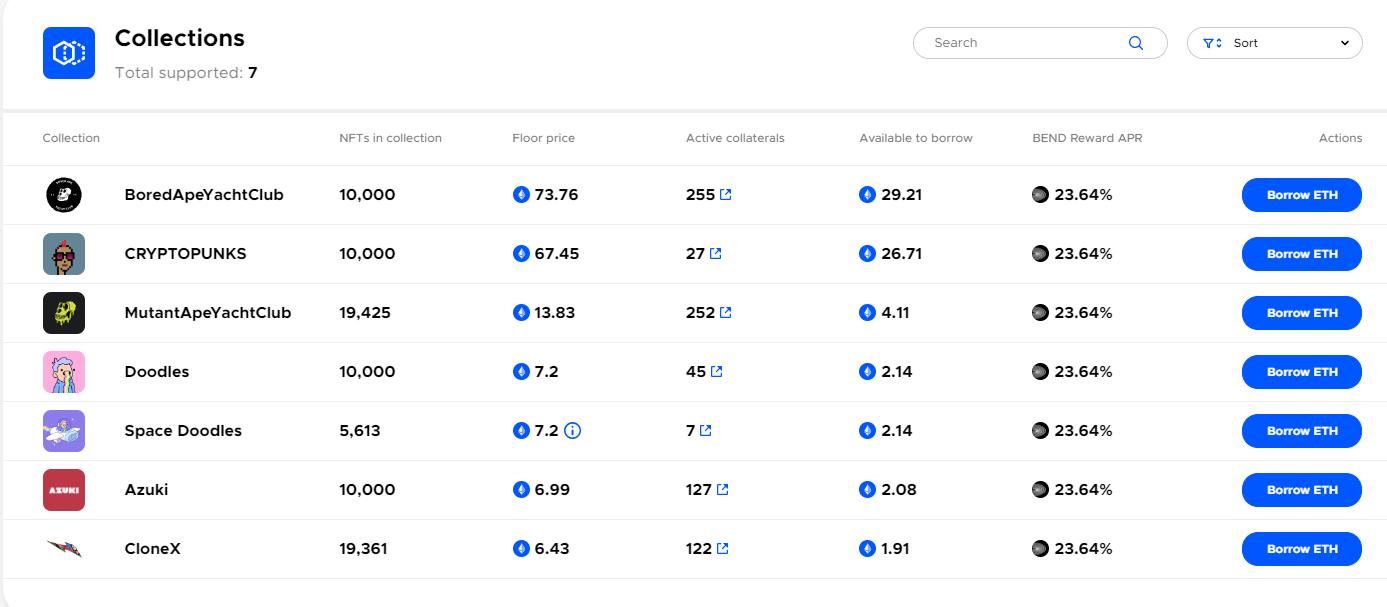

Current collateral and quantity on the BendDAO platform.

2. JPEG'd

JPEG'd is also a pool-type NFT lending platform, but it adopts the MakerDAO CDP (Collateralized Debt Position) model in its lending mechanism. Protocol users pledge NFTs into the protocol and borrow stablecoins PUSd generated from the NFT collateral, with a maximum borrowing limit of 32% of the PUSd floor price. JPEG'd offers a 2% loan interest rate for pledgers, while the stored APY ranges from 10% to 20%.

Currently, the main NFT collateral pools on the JPEG'd platform include CryptoPunks (69), BAYC (9), MAYC (12), and Doodles (5).

JPEG'd also uses a "health index" to assess the current lending situation, with higher values indicating safer fund status. Its calculation formula is:

Health Index = (1 - (LTV / Liquidation Index)) X 100

However, the platform's liquidation mechanism is triggered by the liquidation index. Previously, JPEG'd set the liquidation index (debt value / collateral value ratio) at 33%. If the value of the NFT collateral declines slightly or if users withdraw more debt, causing the debt/collateral ratio to equal or exceed 33%, liquidation will occur (locking NFTs with JPEG'd Cigarette attributes can increase credit limits and liquidation ratios; some pledged NFTs can have LTVs of up to 40%. Additionally, JPEG'd recently launched the JPEG'd Traits Boost feature, allowing for higher credit limits for rare NFTs).

The health index is presented as a percentage, aiming to provide users with a more intuitive understanding of whether their orders are at risk of liquidation, allowing for timely loan repayments. This differs from BendDAO's health factor, which is directly linked to liquidation.

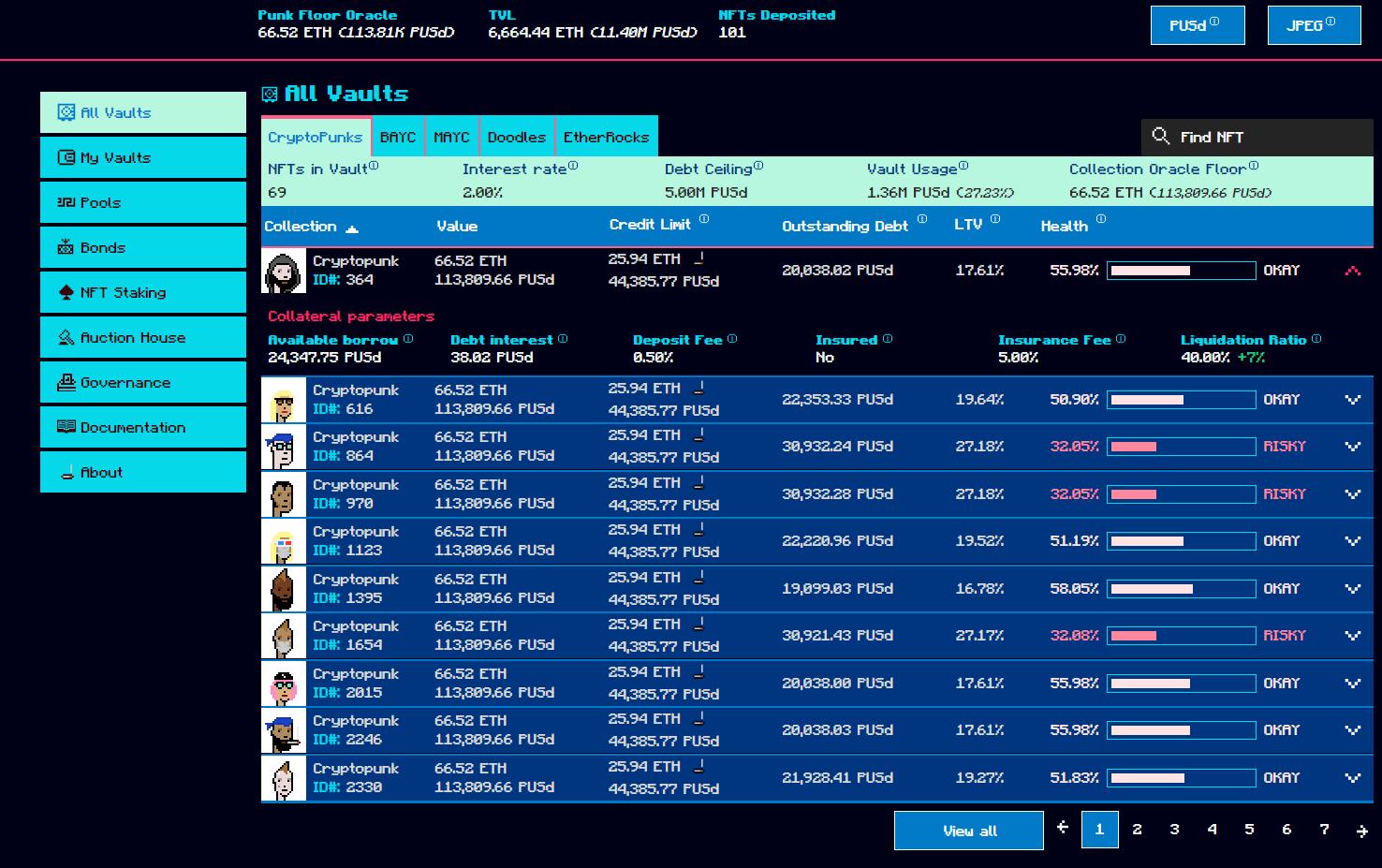

As shown in the image, if the floor price of your pledged CryptoPunks is 66.52 ETH, the maximum amount you can borrow is 25.94 ETH. When the CryptoPunks floor price drops below 64.94 ETH (25.94 ETH / 40%), your NFT will enter the liquidation protection and auction process, which lasts for 24 hours. If a new bid is placed less than 5 minutes before the countdown ends, the auction will be extended by 10 minutes. This process repeats until there are no other bidders.

Compared to BendDAO's liquidation mechanism, JPEG'd's mechanism can be said to be extremely strict, forcing pledgers to borrow less to ensure their orders remain healthy. However, the benefits are also evident; as long as the floor price drops slightly, it will compel pledgers to redeem their NFTs or enter liquidation, thereby reducing the risk of bad debts. But from the pledger's perspective, this means having less buffer space and an increased risk of liquidation, thus being forced to shorten the lending period. Of course, this also means that the collateral on the JPEG'd platform flows more quickly.

Additionally, as mentioned earlier, unlike BendDAO, after the liquidation begins, the JPEG'd treasury will buy back the NFTs at the loan amount price, which are then disposed of by the DAO treasury, thus somewhat alleviating panic and liquidity crises in the NFT market under poor market conditions.

Considering the risks faced by pledgers, JPEG'd has designed a new insurance module, which is not available in other similar protocols. The cost of purchasing insurance is 5% of the initial debt. If a pledger is liquidated, they can repay the debt and 25% of the liquidation fee within 48 hours after liquidation to buy back their NFT from the DAO. The 25% liquidation fee is based on the user's outstanding debt, which includes the principal plus any accrued interest.

It is worth mentioning that recently, in response to the BendDAO incident, JPEG'd DAO passed a new proposal to provide free insurance for eligible NFTs that migrate from BendDAO to JPEG'd within two weeks (from August 17, 2022, to August 31, 2022). The proposal has already been approved.

3. Drops DAO

Drops DAO officially launched its mainnet in May this year. Currently, the largest pool on the Drops platform is the Yuga Labs lending pool, where users holding BAYC, MAYC, and PUNKS NFTs can engage in liquidity mining. Unlike the previous three protocols, Drops generally has a higher LTV, with the official statement indicating a maximum borrowing limit of up to 60% of the NFT floor price. However, the high LTV is supported by Drops' unique pricing mechanism.

Drops employs oracles, time-weighted pricing, and extreme value removal while utilizing fragmentation for pricing. Specifically, it uses the floor price as a baseline for preliminary transaction verification: 25 block confirmations, 1 NFT sale, and the same Token ID not being sold again within 24 hours; extreme values are removed by calculating the floor price from 100 transaction data points and excluding transactions below the 5th percentile and above the 950th percentile; potential extreme values are removed by excluding transactions that deviate by N standard deviations; prices are fed every 4 hours, etc.

This relatively strict pricing method, which takes liquidity into account, ensures the basic quality of NFTs pledged on the Drops platform, allowing for higher valuations while controlling risk exposure, but it is not friendly to non-blue-chip NFT series.

Additionally, Drops encourages the simultaneous pledging of multiple NFT assets.

For example, based on Drops' maximum LTV of 60%, the minimum collateralization rate (100% divided by the LTV percentage) is 166.6%.

Assuming you borrowed 50 ETH when the value of your BAYC was 100 ETH, the minimum collateralization rate is 166.6%, so 50 ETH * 166.6% = 83.3 ETH. As long as the BAYC price does not fall below 83.3 ETH and no additional funds are borrowed, the loan will remain solvent. Once the borrowing limit is exceeded, the borrower's loan can be liquidated by anyone.

When only 1 NFT is provided as collateral, an LTV of 90% or higher will trigger liquidation. For example, if the provided NFT is valued at 100 ETH and the user borrows 50 ETH, the NFT value must be greater than 55.5 ETH to avoid liquidation.

When providing 2 or more NFTs as collateral, the first liquidation threshold is 60%, while the second and subsequent liquidation thresholds are 90%.

For example, if a user provides 2 BAYCs, each valued at 100 ETH (totaling 200 ETH), with an LTV of 60%, the borrowing limit is 120 ETH, and the user borrows 100 ETH. If the price of BAYC drops to 80 ETH, the total value of the collateral is now 160 ETH, and the new borrowing limit is 96 ETH. The first NFT of the pledger will be liquidated at a price of 80 ETH * 90% = 72 ETH, effectively using one of the NFTs to repay the debt, reducing the pledger's debt from 100 ETH to 28 ETH, allowing the user to keep 1 of the 2 NFTs. The borrower no longer exceeds their borrowing limit and has a collateralization rate of 285% (NFT value of 80 ETH / debt amount of 28 ETH).

This liquidation mechanism allows borrowers to borrow more funds and alleviates the financial pressure on borrowers through the collateralization of multiple NFTs. However, similar to the risks faced by JPEG'd, the DAO assumes the role of initial liquidator, and the treasury funds face certain stability risks.

4. Pine

Compared to the previous protocols, Pine is still in a relatively early beta stage, having completed a $1.5 million financing round led by Sino Global Capital and Amber Group in May this year. Pine has currently created 31 NFT pools, with a total locked value of $855,765.

Pine's liquidation mechanism is relatively simple; an LTV greater than 40% will trigger liquidation. Pine's LTV will vary based on the terms set by the lender. For safety reasons, Pine's LTV ratio is set in the range of 30-50%. If the borrower fails to fulfill their loan obligations before the loan due date, i.e., repaying the loan and accrued interest, manual liquidation will occur.

According to its white paper, pledgers will receive a final repayment deadline notice 24 hours in advance. After the loan due date, borrowers have a 12-hour grace period to repurchase their liquidated assets from the lender or liquidator. During the repurchase period, liquidators will not sell the assets before the end of this period. Additionally, borrowers have a 3-day adjustment period during which the Pine team will attempt to help borrowers negotiate with liquidators for repurchase. There is no guarantee that a transaction can be arranged (for example, if the liquidator sells the asset on OpenSea, repurchase may not be possible).

Overall, Pine's liquidation mechanism is relatively simple, and the platform's awareness of risk management is relatively weak, so users should pay attention to controlling risks. Moreover, the NFT projects included on this platform are not typically blue-chip NFTs, making prices prone to fluctuations and risks relatively high.

3. What Problems Exist in the Current P2Pool Model?

Cobo Ventures researcher Walon Lin believes that, ultimately, the biggest challenge for NFT-Fi is still the issue of liquidity. If this problem is not resolved, the leverage ratio of pool protocols will remain low.

The infrastructure for the P2Pool model has not yet been fully established. For instance, the current pricing models and oracles have not achieved proper incentives. For example, using floor price pricing is not friendly to rare NFT holders, while oracle pricing does not allow for timely liquidation of floor price NFTs. Secondly, this sector has yet to see more platforms with AMM mechanisms like Sudoswap or liquidation-like platforms. In the future, perhaps involving NFT project parties as liquidators could help solve the liquidation crisis.

How each pool protocol sets LTV and pricing is essentially a trade-off issue that needs to balance the interests of both pledgers and liquidity providers, but these issues cannot be resolved at the moment. Until the infrastructure is fully established, C2C will be a better choice.

Additionally, according to the current operational logic, the pool model has a fundamental flaw: it cannot achieve permissionless entry, only allowing blue-chip projects to participate, thus limiting its audience. However, the original intention of NFT-Fi is to "enhance NFT liquidity," and allowing non-blue-chip NFTs into the pool is the true meaning of large-scale adoption.

Finally, I would like to ask everyone to consider a question: In the depths of a bear market, can we rely on NFT-Fi to enhance NFT liquidity? Currently, the answer is not so optimistic; NFT-Fi essentially adds leverage to NFTs, akin to icing on the cake. In a cooling market environment, these protocols, which embrace the original intention of "enhancing NFT liquidity," face severe tests. What are your thoughts on this? Feel free to add WeChat ID jiayifan510 to discuss with the author of Chain Catcher.

Reference: 《Cobo Ventures: In-depth Analysis of NFTFi---Looking at the Future Development of NFTFi from the Current Market》

Risk warning

Risk warning Risk warning

Risk warning