Exploring the OMM market-making mechanism under the ILM model and its practitioner Fort Protocol

The OMM of Fort Protocol links traders directly to smart contracts, continuously providing trading liquidity through the burning and minting of DCU.

The OMM of Fort Protocol links traders directly to smart contracts, continuously providing trading liquidity through the burning and minting of DCU.Traditional CEX exchanges usually introduce some market makers to provide liquidity for assets. They quickly place and cancel orders on the buy and sell boards according to strategies to match the trading needs of some users. These market makers are typically teams that hold substantial assets and generate profits while avoiding losses based on their own strategies.

In contrast, DEXs have been led by AMM, which has become the preferred liquidity model for many DEXs. With the development of DeFi, AMMs have gradually exposed many issues, such as inefficient capital liquidity provision and significant price deviations. Therefore, they are not suitable for some derivatives protocols, and this model also has relatively low compatibility with other ecosystems.

ILM is a liquidity mechanism known as "infinite liquidity," and the model built on this basis, which corresponds to AMM, is called "OMM," or "infinite market making" model. This model can better match decentralized derivatives protocols, providing liquidity through a reasonable mechanism and having good composability with various ecosystems. Fort Protocol is currently the first DeFi protocol to use the OMM model. This article will briefly compare the AMM model with the ILM model and provide a brief introduction to Fort Protocol.

Automated Market Maker (AMM)

The AMM model also introduces the concept of market making, which we usually call LP (Liquidity Provider). In the AMM model, there is typically also an asset pool or liquidity pool (smart contract that holds assets). LPs usually deposit their own assets into the pool in proportion to provide liquidity for trading (constant asset pool). For example, if 1 ETH = 1000 USDT, when you provide liquidity, you need to inject 1 ETH and 1000 USDT into the liquidity pool simultaneously. Of course, there are also mixed asset pools and weighted asset pools that support multiple assets for liquidity provision, but the constant asset pool model is currently the most widely used.

The benefits of being an LP include earning a certain amount of interest and sharing transaction fees. Additionally, some DeFi protocols that support liquidity mining will reward you with governance tokens, i.e., liquidity mining. Therefore, the incentives attract many users with idle assets to voluntarily provide liquidity, resulting in a continuous flow of liquidity.

Traders typically trade with the liquidity pool, and the trading price is automatically generated by the AMM model based on parameters.

The constant product model is the most common in AMM (there are also constant sum, constant mean, etc.). For example, Uniswap is an AMM DEX that combines product market making with a constant asset ratio pool. Typically, the product of the two corresponding assets in the liquidity pool is a constant, i.e., XY = K. When the quantity of assets in the pool changes, it usually leads to a price deviation from the market price on the DEX. At this point, speculators will come in to arbitrage and stabilize the quantities of the two assets in the pool to further achieve balance.

Although it can provide considerable liquidity for DEXs, AMMs have certain shortcomings. When the amount of funds traded by traders accounts for a large proportion of the funds in the pool, it can lead to excessive price deviation, i.e., high slippage.

For example, in an ETH/DAI trading pool where 1 ETH = 100 DAI, the constant product K is 10000, and the initial pool contains 1000 DAI and 10 ETH. When you inject 250 DAI into the trading pool to trade Ethereum, you will find that the remaining number of Ethereum in the pool is 10000/(1000+2500)=8, and the 2 ETH reduced from the pool will be what you obtained from the trade. This means that you exchanged 250 DAI for only 2 ETH, with a unit price of 125 DAI.

Although this may not be so exaggerated in reality, this problem is still quite common. Therefore, for the AMM model, the existence of slippage has a significant impact on traders.

From the perspective of LPs, AMMs typically incur some impermanent loss. This loss is termed "impermanent" because it can be recovered. For example, when the off-market price and the price of the corresponding tokens in the liquidity pool deviate in any direction, it leads to LPs incurring losses in terms of the currency. Of course, arbitrageurs will restore the situation in the pool, and the impermanent loss will disappear (which is almost difficult to achieve). Additionally, the assets injected by LPs into the liquidity pool may face losses in terms of currency due to asset price declines, which may also lead LPs to withdraw funds during market fluctuations. This is also common in some lending protocols, where changes in interest rates, such as in AAVE, can further reduce the enthusiasm of one party in borrowing/lending.

Moreover, the size of the DEX, i.e., TVL, will also affect trading prices. The smaller the TVL, the larger the price deviation. For example, Uniswap's price accuracy is better than that of KyberSwap because small-sized liquidity pools find it difficult to attract traders.

Furthermore, the capital efficiency of the AMM model is relatively low. When trading is active, the liquidity near the current price will quickly deplete, accompanied by increased slippage, leading to significant price deviations and causing trading to stop. This results in low utilization rates of funds in the liquidity pool, and DeFi protocols cannot share TVL, which is the current state of most AMM DEXs.

Of course, in the derivatives sector, even with the introduction of oracles, the liquidity pools of AMMs may still be insufficient to cover the assets due to the high profits of large traders, as extreme situations may occur more frequently in derivatives compared to spot trading.

ILM Model

The roles in the AMM model typically exhibit a certain asymmetry, such as between liquidity providers and traders. It usually sacrifices the flexibility of liquidity providers to further create liquidity for traders. Additionally, it continuously generates deviations due to the algorithms in the pool. In this model, the smart contract merely acts as an intermediary, rather than being the endpoint for traders' transactions, as it often needs to connect the traders on one end with LPs.

The idea of ILM is to directly use the smart contract as the trading endpoint or counterparty. It continuously provides liquidity for traders' transactions through a certain system of encrypted assets, using smart contracts to mint and burn tokens, and this system token is elastically supplied according to market prices, bound to other assets through oracle price feeds.

Compared to the AMM model, the ILM model is more straightforward. It does not generate trading settlement deviations due to factors such as trading volume, TVL, and price changes, as it does not have the constants found in AMM. The smart contract can mint or burn system tokens at any time based on trading demand, meaning that trading is always instantaneous. This is particularly advantageous in the derivatives sector.

Fort Protocol's OMM Infinite Market Making Mechanism

Based on the ILM infinite liquidity model, Fort Protocol has launched the OMM, which currently has considerable application prospects in the derivatives field.

In the OMM system, it issues the DCU token as the driving asset for liquidity within the ecosystem. For example, when a user purchases a call option in Fort Protocol's options product, they first need to pay for the option using DCU to the smart contract. These DCUs will be immediately burned, and when the system reaches the delivery time and generates profits, the contract will mint an equivalent amount of DCU tokens based on the profit according to the oracle price (currently using the NEST oracle), which many AMM model liquidity pools will be unable to deliver when funds are insufficient.

The DCU itself is long-term deflationary and is a balanced token. Various financial products in OMM are uniformly priced in DCU, enabling infinite liquidity and settlement within the system, and not requiring external liquidity in various derivatives scenarios. This also facilitates trading across different financial products, as long as the liquidity of DUC is ensured.

Fort Protocol's OMM mechanism possesses composability and supports the construction of pluggable applications. Projects (on-chain or off-chain) can quickly build and deploy applications using the contracts provided by Fort, offering user-friendly decentralized products. Through the functional combinations provided by Fort Protocol, the costs and revenues of any application can be settled using the system token DCU according to algorithmic functions, without the need to issue excessive tokens. By utilizing complex contracts and algorithms, along with the DCU token, it provides infinite liquidity compatible with various financial products, reducing user costs.

In addition to the options scenarios mentioned above, perpetual contracts, leveraged trading, and leveraged tokens are also derivatives scenarios. For example, constructing a dynamic settlement model based on fundamental yield functions, which changes the balance of its tokens dynamically according to price, has already been practiced in current algorithmic stablecoins. Furthermore, in insurance, lending, interest rate derivatives, and indexed tokens, similar models can also be realized through Fort Protocol.

Moreover, Fort Protocol can further expand into the NFT and GameFi fields. For instance, DCU can be economically bound to on-chain games or NFTs, and all game assets can be designed with some probability tokens or derivatives scenarios. Corresponding to the NFT game assets, regardless of whether they possess liquidity in the game, they can be monetized in FORT, and this is expected to extend into the metaverse in the future.

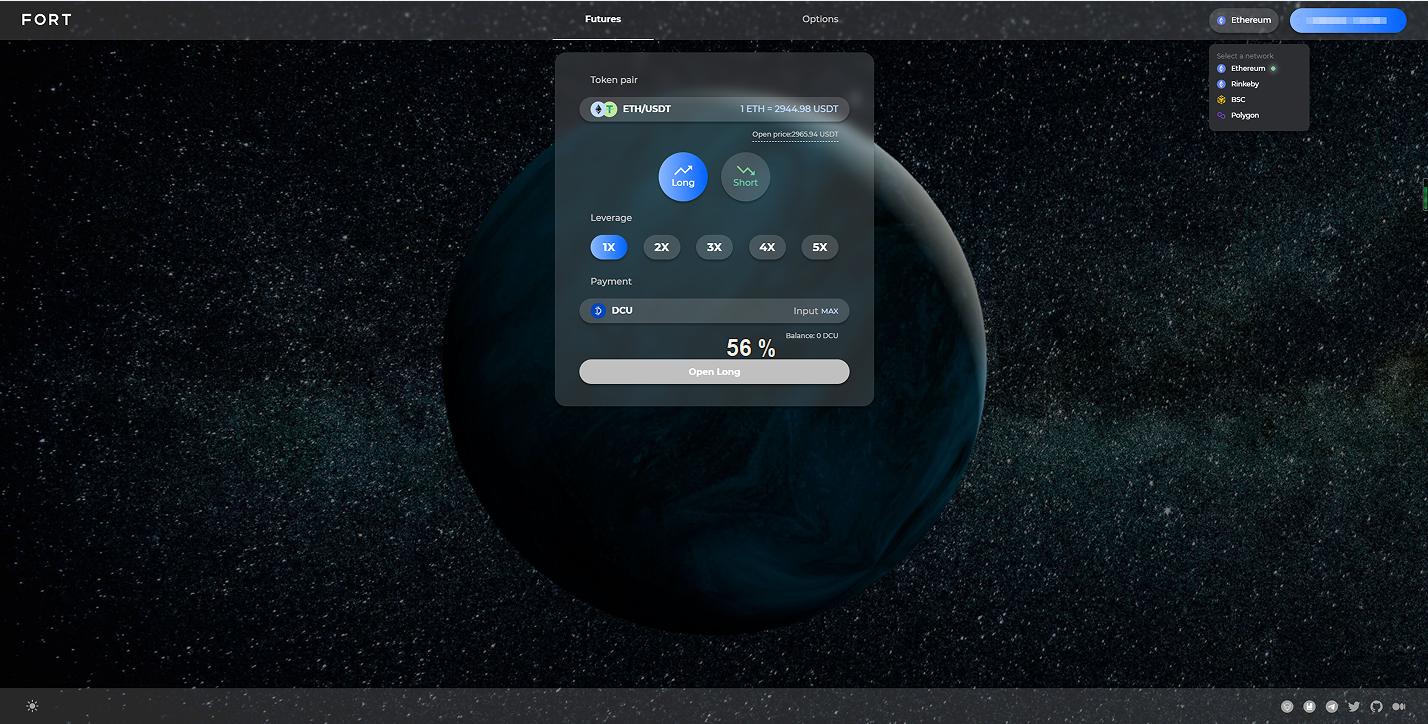

Currently, Fort Protocol has launched two derivatives sectors: one is a leveraged futures play, and the other is short-term options. The product interface is simple and the functions are clear. Fort Protocol supports users on Ethereum, BSC, Rinkeby, and Polygon, which also means that Fort Protocol will build a multi-chain ecosystem.

Although AMM became one of the effective ways to solve liquidity for DEXs in the early days, the algorithm-driven nature will always cause losses to the interests of traders and LPs. Additionally, the effectiveness of liquidity and capital utilization is severely affected by the pool's APY, and it has considerable shortcomings in the derivatives field.

Fort Protocol's OMM links traders directly to smart contracts, continuously providing liquidity for trades through the minting and burning of DCU. The liquidity factor solely depends on the liquidity of DCU, and it can be combined with all decentralized derivatives models. The innovation of ILM over AMM may be a result driven by deep market demand. We look forward to further extending into the fields of NFT, GameFi, SocialFi, and even the metaverse in the future.

Risk warning Risk warning

Risk warning Risk warning

Popular articles