A comprehensive look at the challenger in the Ethereum staking space: Swell Network

Swell plans to build Rails to allow node operators to create their own front ends on top of the protocol, which, if successfully executed, could make Swell the preferred staking market.

Swell plans to build Rails to allow node operators to create their own front ends on top of the protocol, which, if successfully executed, could make Swell the preferred staking market.Original Title: 《Swell Network: Ethereum's First Liquid Staking Marketplace》

Author: Ashu Pareek, Messari

Compiled by: Deep Tide TechFlow

Key Points

- Swell Network is currently in its protected mainnet and is a permissionless, non-custodial Ethereum liquid staking protocol.

- Swell has the first service that integrates atomic deposits: allowing users to directly deposit ETH into their chosen validators—creating a staking market.

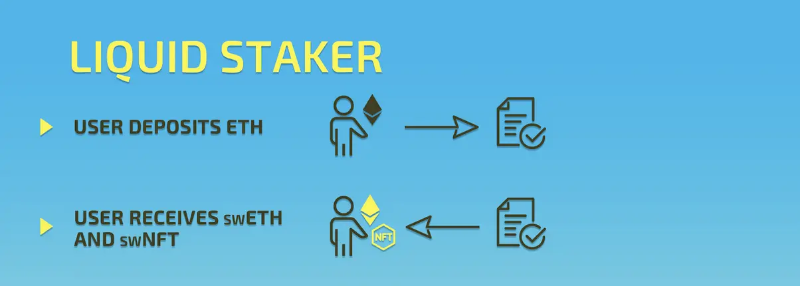

- To make staking liquid, Swell mints and returns NFTs to depositors, known as swNFTs.

- swNFT is a container that holds swETH along with information about rights, rewards, and validators. swETH (non-rebased) is returned at a 1:1 ratio with the ETH deposited (principal).

- Swell has become the first liquid staking service to adopt Distributed Validator Technology (DVT), which will provide high capital efficiency and permissionless access to its validator set.

- There are also plans to provide DeFi vaults and white-label features within the dApp, allowing node operators to create their own front ends on top of the protocol.

Ethereum's transition from Proof of Work (PoW) to Proof of Stake (PoS) has given ETH holders the opportunity to secure Ethereum's new central consensus hub, Beacon 1Chain.

In exchange for locking ("staking") their assets to create new blocks, validators can earn inflationary rewards.

Post-merge, rewards will also include priority fees and maximum extractable value (MEV), providing stakers with an attractive annual interest rate of 7-14%.

However, the minimum capital requirement (32 ETH) is too expensive, along with the technical complexities surrounding the validation process and the extended lock-up period (six months to a year post-merge), which hinder the ability and willingness of ETH holders. To address these user experience issues, an industry called "staking as a service" has emerged.

So far, the most popular solution is non-custodial liquid staking, with Lido being the leader in this sector, while alternatives include Rocket Pool and others.

Although the current set of non-custodial liquid staking protocols has been successful, accumulating over 34% of staked ETH, they leave many untested gaps in design and implementation.

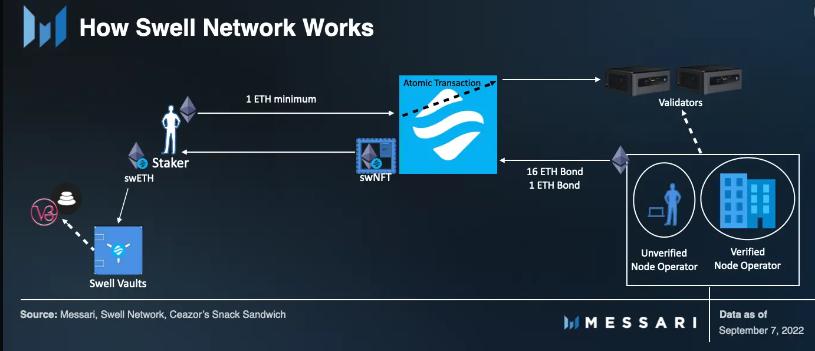

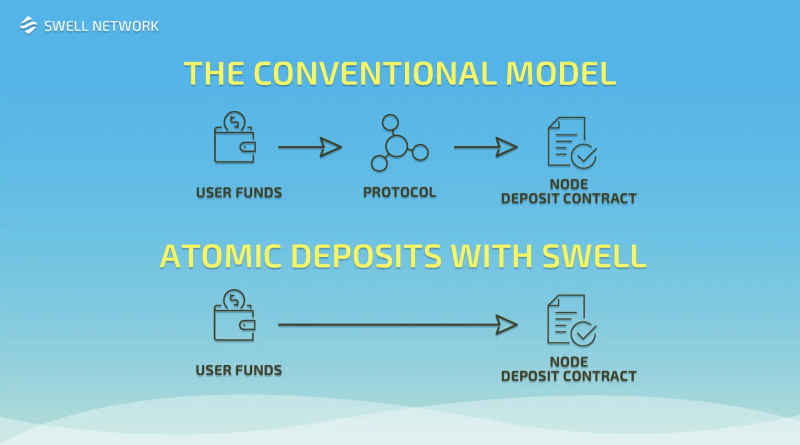

In a competitive, network effect-driven space, newcomers can gain significant advantages, and Swell Network is a prime example. It has learned from the experiences of non-custodial liquid staking pioneers and offers a novel way to stake and earn Ethereum rewards. The most important distinction is its integration of atomic deposits: allowing users to directly deposit ETH into their chosen validators, thus creating the first de facto staking market.

Looking ahead, in addition to providing DeFi vaults within the dApp (similar to Yearn), Swell has taken concrete steps to become the first liquid staking service to adopt Distributed Validator Technology (DVT). DVT will allow Swell to provide independent, permissionless node operators with the same capital efficiency of access to its validator set as commercial, whitelisted operators.

Finally, Swell plans to build Rails to allow node operators to create their own front ends ("white-label") on top of the protocol.

If executed successfully, this could make Swell the preferred staking market: fostering relationships, allowing for customization, and increasing decentralization across the Ethereum network.

Background

Swell's proof of concept (V1) was launched in December 2020, shortly after the Beacon Chain.

In June 2022, Swell launched V2 private testing on Kaleido and soon after opened public testing on Görli.

Around the same time, Swell completed a $3.75 million seed round led by Framework Ventures, with participation from IOSG Ventures, Maven Capital, Apollo Capital, Mark Cuban, Fernando Martinelli (Balancer), and Ryan Sean Adams and David Hoffman (Bankless).

By the end of August 2022, Swell V2 went live on the Ethereum mainnet.

How Does Swell Work?

Swell operates quite differently from other Ethereum liquid staking protocols.

In its final state, Swell V2 will involve:

- Node operators, responsible for managing staking. They can join permissionlessly (independently, with 16 ETH staked per validator) or through whitelisting (verified, with 1 ETH staked per validator).

- Atomic deposits, allowing users to stake directly with their chosen node operators, with a minimum of 1 ETH.

- swNFT/swETH, minted and returned to depositors (stakers). swNFT is a container that can hold swETH along with information about rights, rewards, and validators. swETH (non-rebased) is returned at a 1:1 ratio with the ETH deposited (principal).

- swETH can be withdrawn and used in Swell dApp's built-in DeFi vaults as well as anywhere else that accepts ERC-20 tokens.

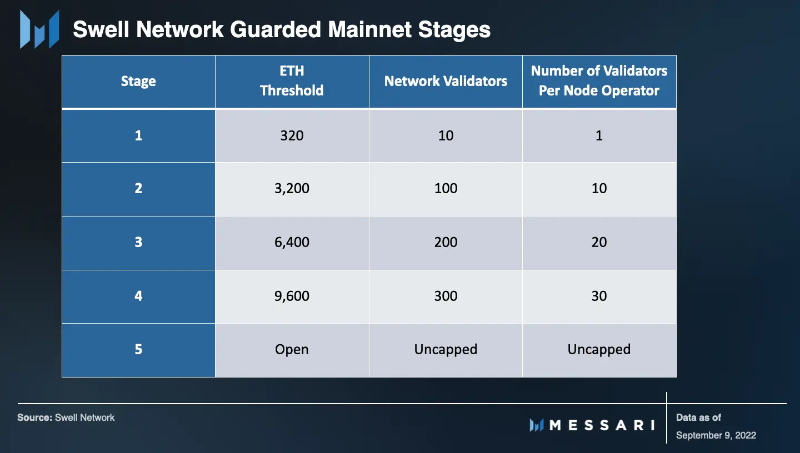

Swell's secure launch occurs in five phases.

The protocol is currently in the first phase, with 242 ETH and 8 whitelisted node operators.

The completion of each phase depends on reaching its ETH threshold, and everything continues to run smoothly.

Node Operations

Swell's node operators are responsible for the actual staking. Swell will have two groups of node operators: verified (permissioned/whitelisted) and independent (permissionless).

During the protected launch, validation is only open to verified node operators. These operators are typically considered experienced and can apply for whitelisting in a single round. The first (and so far only) whitelist was conducted by the Swell core team, which included eight commercial node operators: InfStones, RockX, Smart Node Capital, DSRV, Blockscape, HashQuark, Stakely, and Kiln.

The application process evaluates potential node operators based on their experience, performance, infrastructure (quality, diversity, and security), and potential contributions to the DAO, along with KYC checks and contractual agreements.

Once Swell fully launches, independent node operators will be able to join the Swell platform permissionlessly.

However, they will need to provide 16 ETH as collateral for each validator to do so.

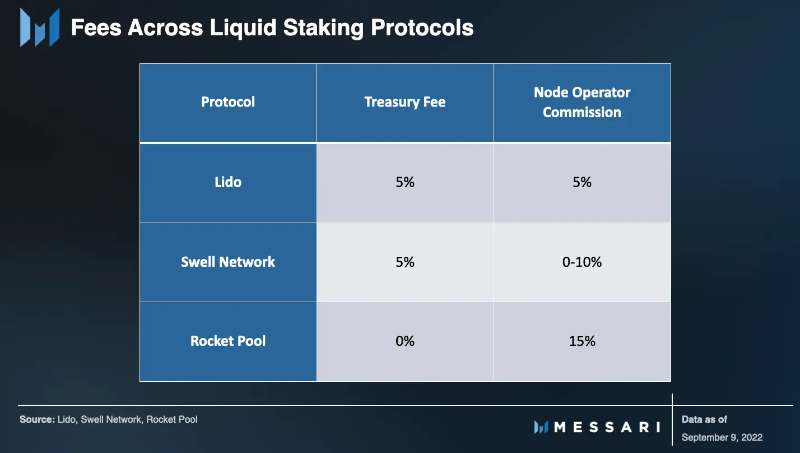

Once onboarded, node operators set their own commission rates, ranging from 0-10%.

Currently, Swell also charges a 5% protocol fee on staking rewards, which goes directly into the DAO treasury and is subject to DAO governance.

Node operators also have flexibility regarding the clients they run. After the merge, node operators will have full control over how they redistribute priority fees and MEV rewards, as clients will not be configured with fee recipient addresses. Swell also plans to eventually release a smoothing pool, similar to Rocket Pool's smoothing pool.

While node operators can adjust their commission rates, the amount of additional earnings sent to their designated Swell fee pool, and how they display their performance (returns), they will compete in an open market. Theoretically, those node operators who maximize transparency and returns while minimizing fees will attract the most staking.

swNFT and swETH

Since Swell uses atomic deposits, users will stake (at least 1 ETH) directly to their chosen Beacon Chain deposit contract. In other words, users can select their node operators (based on profiles, commissions, and/or performance) and continue to track their deposits.

In this model, staking is not naturally fungible (i.e., liquid) because it is tied to specific node operators rather than a general staking pool (composed of many node operators). Today, Swell has found a way to alleviate this to some extent by using swETH derivatives and swNFTs to extract the deposited ETH from staking rewards.

In exchange for the staked deposit, the contract mints and sends users swETH and swNFT.

swETH is a non-rebased ERC-20 liquid staking derivative token that represents the primary stake, with swETH held within the swNFT.

During the protected launch, liquid staking will remain disabled, meaning swETH cannot be withdrawn from the swNFT. Once liquid staking (withdrawals) is live, stakers will be able to choose to use swETH in DeFi. Meanwhile, node operators will receive a soulbound (non-transferable) swNFT representing their collateral.

In addition to serving as a container for swETH, swNFT also holds staking rewards (yield) and specific, non-falsifiable information about the staking. This information includes the delegated node operator, validator address, and the timestamp of the deposit.

swNFT does not actually earn rewards (staking rewards). Instead, the swNFT holding staking-related information will be linked to the yield earned from the ETH initially deposited with the node operator.

In other words, even without holding any swETH, swNFT will continue to accumulate rewards. To actually receive rewards (and principal), users need to burn the swNFT with the amount of swETH initially deposited.

Withdrawals are currently expected to be enabled 6-12 months post-merge. During the merge, the primary source of liquidity for swETH will be the secondary market.

This model has some interesting implications for swETH and swNFT holders.

First, in this model, the only way to earn staking rewards is to obtain swNFT, as swETH obtained without swNFT will not accumulate rewards.

swNFT can also be used in various ways throughout DeFi: as collateral, with interest rate protocols (such as Element Finance and Yield Protocol), for node operators to establish their brand/relationships with stakers, and for access control to certain features by Swell itself.

Roadmap

Improving Capital Efficiency

As mentioned earlier, once permissionless staking is enabled, independent node operators will need to provide 16 ETH as collateral for each validator to join Swell's operations.

However, this poses a bottleneck for independent nodes joining the protocol and raises concerns about the decentralization of the entire Ethereum network.

Swell V3 will lower this requirement by leveraging the technology of secret shared validators (ssv.Network), also known as Distributed Validator Technology (DVT).

Specifically, Swell will collaborate with ssv.Network (DVT infrastructure protocol) to integrate SSV and reduce the collateral requirement for independent operators to 1 ETH (the same as verified ones).

Swell Vaults/DeFi Integration

In addition to delegation, liquid staking also allows users to forgo the opportunity cost of locking funds. Instead, stakers can still retain and use at least part of their staked value. With the launch of Swell Vaults, Swell will take this a step further.

First, the vaults within the dApp will be created by the Swell team, primarily to simplify and automate compounding and create liquidity for swETH. Ultimately, it will allow anyone to build vaults and propose strategies (similar to Yearn).

The second component of DeFi integration will focus on creating liquidity for swETH. Once swETH can be withdrawn, Swell will launch swETH/ETH liquidity pools on Uniswap V3 and Balancer. In addition to running liquidity mining programs, the team also plans to incentivize vlAURA/veBAL holders to increase LP yields (thereby increasing liquidity).

Swell Network Token

Swell has not yet launched its governance token, SWELL. In addition to managing the protocol (parameters and cash flow usage), SWELL will be used to incentivize node operators and swETH/ETH liquidity pools.

Early users will receive airdrops, and seed round investors will have a three-year vesting schedule.

White-Labeled Liquid Staking

Swell will further enhance customization and staker relationships by allowing node operators to create their own interfaces on Swell's backend.

Sector Competition

In the non-custodial liquid staking space, Swell's biggest competitors are Lido and Rocket Pool.

In many ways, Lido and Rocket Pool are at opposite ends of the spectrum in terms of their products and approaches.

Lido is the largest liquid staking provider, accounting for nearly 90% of all liquid staked ETH.

Largely, Lido's aggressive expansion on Ethereum has been achieved through its deposit model. Lido only uses a set of professional, whitelisted node operators, and it does not require them to provide collateral. This model allows node operators to easily absorb large amounts of ETH. Additionally, the staking pool allows users to start earning rewards immediately after depositing into the platform (rather than waiting in line to enter through Ethereum validators), leading to a surge in staking on Lido.

In terms of demand, Lido's stETH integrates with almost all major DeFi blue chips. Yearn, Curve, Aave, MakerDAO, Balancer, and so on. Lido also spends millions of LDO (Lido's governance token) each month to incentivize liquidity (2.5 million LDO in August, approximately $6 million), creating a strong flywheel effect that drives more demand back to the staking service.

However, Lido has also faced criticism from the Ethereum community, with many viewing Lido as a threat to Ethereum's decentralization. Due to Lido's relatively small, closed, institutional node operators, it is effectively overseen by an insider committee (LNOSG). Even though LDO holders have the final say, the insider ownership of LDO is highly concentrated.

Thus, they lean towards Rocket Pool, which takes an almost opposite approach. Launched nearly a year after Lido, Rocket Pool prioritizes decentralization by allowing permissionless access to the validator pool.

The protocol ensures staking rights through economic incentives rather than reputation or past performance. While Rocket Pool's system has led to broader participation in validation, it has also created bottlenecks due to its low capital efficiency. Node operators currently need to stake 16 ETH for each validator, in addition to binding RPL. This setup makes it challenging to scale validators and absorb staking. Consequently, Rocket Pool currently accounts for just over 5% of liquid ETH staking, and less than 2% of total ETH staking.

Swell leverages the advantages of being a latecomer, learning from both of these protocols while introducing its own novel solutions into the "staking as a service" space.

Swell's first major tactical move is to triangulate between the operator setups of Lido and Rocket Pool. By enabling both permissionless and whitelisted node operators, Swell allows for broader participation in the validation process (enhancing decentralization) while maintaining its ability to absorb staking demand. Additionally, Swell will smooth the transition to DVT by implementing permissionless validation from the start.

Swell also adds some novel features—most notably atomic deposits. The first open and transparent staking market will provide a range of benefits for stakers and node operators. Stakers will be able to decide where to stake (based on performance, commissions, infrastructure, jurisdiction, or other publicly listed characteristics) and track their staking on-chain.

Node operators will be able to customize their products (e.g., priority fee/MEV allocation, commissions, clients, etc.), interface with customers (via swNFT), and even eventually build their own front ends ("white-label") on top of Swell. The trade-off of this model is that losses (penalties and cuts) are not shared among all users but distributed between the affected validators and their stakers.

Using NFTs is also a first for liquid staking protocols. This model ultimately excludes the use of yield-accumulating reward tokens (such as Rocket Pool's rETH and Lido's stETH). While this is a necessary trade-off, the lack of fungibility may likely widen the discount of swETH:ETH.

Another strategy for Swell is the minimum staking requirement of 1 ETH, as it does not have a staking pool. Depending on the appreciation of ETH prices, the 1 ETH minimum could lock in a significant number of users in the future, while Rocket Pool has a minimum of 0.01 ETH, and Lido has no minimum requirement.

Swell's other two competitive advantages are Swell Vaults and variable commission rates. The commission rate could become a significant selling point, depending on where the internal market pushes it.

The future staking ecosystem may provide a place for these models and their unique products. These models may begin to converge, especially regarding permissionless node operations/capital efficiency. Rocket Pool is currently considering a formal proposal to reduce the required collateral to 8 ETH and eventually even down to 4 ETH (along with RPL bonds).

Lido's roadmap appears more competitive compared to Swell's, as it is also seeking to implement permissionless DVT. However, Swell seems to be further along in its roadmap, with upcoming (mainnet) permissionless validation and has already publicly disclosed its DVT strategy/collaboration with ssv.network.

Risks

Swell's biggest risk is its late entry into the market. While Ethereum staking is still in its infancy, Lido and, to a lesser extent, Rocket Pool have already established themselves in the DeFi and broader ecosystem. They have a strong flywheel effect, where integration and liquidity drive demand, which in turn drives more integration and liquidity.

Swell has already achieved significant differentiation and is committed to incentivizing swETH liquidity and actively integrating with DeFi. However, the protocol will likely need to execute seamlessly on its features to truly turn the tide. If successful, it could attract a trickle of ETH2 inflows and ignite its own competitive flywheel.

One potential narrative I envision is becoming the first project to successfully implement DVT—reducing the collateral requirements for independent operators to 1 ETH. The unlocked capital efficiency could allow a large number of independent validators to join while enhancing the decentralization of the Ethereum network. In addition to aligning with the core goals of the Ethereum network and community, DVT could also prove its security by enabling trustless validation among four operators.

Another narrative for Swell is establishing a highly attractive market for stakers and operators. This market could benefit from external catalysts that make operators' information more valuable, such as regulatory enforcement in jurisdictions. Another driver could be commission rates that are significantly lower than the current industry standards, which would attract stakeholders, but this shift could also come from the migration of validators. Commercial operators may be drawn to Swell's flexibility, deciding to use Swell's swNFT and eventual white-label features for vertical integration with customers.

The customizable aspect (node operators) is a double-edged sword. Not only could the aforementioned commission rates converge above industry standards, but node operators could also reach a consensus not to send priority fees/MEV to their fee pools. Even though this is a transparent, competitive market, the factors determining market balance are multifaceted and cannot be known in advance.

Although Swell addresses its fungibility issue with swNFT/swETH, this feature introduces additional risk vectors for the protocol. As with stETH, there could be significant divergence in the secondary market for swETH/ETH (from 1:1), even if withdrawal functionality is enabled, as swETH is only a valuable staking derivative for those with positions in Swell (reducing its demand). This uncertainty could also hinder DeFi integration (as it would be viewed as unstable collateral).

Conclusion

While Swell's novelty brings uncertainty, it also brings differentiation.

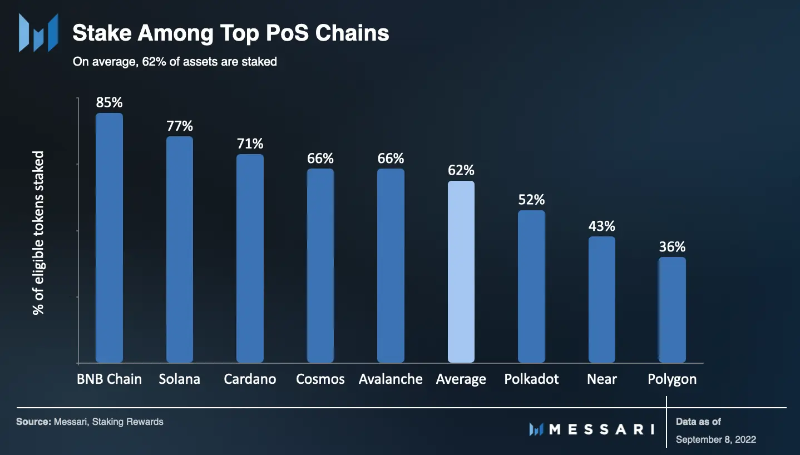

Currently, the amount of ETH staked on Ethereum is about 11% of the circulating supply, and significant growth has yet to come.

Swell launches at the right time, with a significant and unique core product: an open, transparent staking market. It is difficult to know exactly how the liquid staking landscape will evolve over time, but there is no doubt that Swell is an attractive product for both stakers and node operators.

Risk warning

Risk warning Risk warning

Risk warning