Dialogue Wang Feng: Optimistic about the direction of functional NFTs, the only difference between Element and OpenSea is time

Wang Feng also stated that the biggest mistake he made in the past year was thinking that he would succeed quickly, and he regretted missing the opportunity in the Solana NFT market.

Wang Feng also stated that the biggest mistake he made in the past year was thinking that he would succeed quickly, and he regretted missing the opportunity in the Solana NFT market.Interview: Jessy, Chain Catcher

Interviewee: Wang Feng, Founder of Element

In mid-August, the Element 2.0 version of the NFT aggregation trading platform officially launched. Wang Feng's speech at the Twitter Space launch event, titled "I Want the Whole Team to Hear My Excited Heartbeat," quickly gained widespread attention upon release. This marks another significant moment for Wang Feng, following his "Wang Feng's Ten Questions" series from previous years, as he captures the market's focus with a rare viral article.

Once again stepping into the public eye, this may signify a major turning point and offensive for Wang Feng in the Web3 space. In 2017, Wang Feng resigned as CEO of Blueport Interactive, completely handing over the game company he had been with for a decade to a former entrepreneurial partner. He then founded Mars Finance and Consensus Lab, which initially attracted significant market attention. However, due to domestic policy and other factors, many of these ventures, including Coco Finance, Mars Trading Master, and Mars Cloud Mining, were forced to shut down or pivot.

Less known is that Wang Feng's Twitter ID is "Hidden in the Chain," which carries a sense of seclusion and retreat. Looking back at Wang Feng's growth journey, he rose to fame at Kingsoft, transitioning from starting a business from scratch to listing Blueport Games. He has always been a star figure in the workplace and entrepreneurial community, often a subject of media coverage. Since entering the blockchain industry, although Wang Feng has become well-known in the circle due to "Wang Feng's Ten Questions," he has rarely accepted media interviews about himself.

In April 2021, Wang Feng announced the establishment of Element and completed a $11.5 million financing round led by several capital firms, including Sequoia, SIG, and Dragonfly Capital, within a month. Over the past year, he has focused nearly all his thoughts and energy on this NFT trading platform.

Since the beginning of last year's NFT summer, OpenSea has held an absolute dominant position in the NFT market. Even major cryptocurrency exchanges like Coinbase and FTX, which entered the market with great fanfare, often returned empty-handed. In the fiercely competitive NFT market, Element has remained low-key for a long time, but recently, with the launch of its new version, it has shown a momentum of increasing strength, leading in trading volume and user numbers on the BNB Chain for an extended period, and recently surpassing SudoSwap in data on Ethereum over the past week.

At this crucial juncture, Chain Catcher invited Wang Feng for an exclusive interview to discuss his experiences and insights in entering the NFT industry, as well as the development path of Element. Wang Feng stated that the biggest mistake he made in the past year was believing that success would come quickly, and he regretted missing the opportunity in the Solana NFT market.

However, Wang Feng believes that despite Element lagging behind OpenSea in several data dimensions, the main difference lies in the timing of their respective starts. He plans to surpass OpenSea in usability at the tool level while seeking to capture new opportunities in the changing landscape. For instance, he sees the hype around domain assets like ENS, SpaceID, and .bit as opportunities for functional NFTs. He believes the next wave of GameFi products will eventually rise, and by finding new asset customization tools that cater to user experience, the market will always provide opportunities for diligent players to overtake competitors.

Here is the original dialogue:

1. Chain Catcher: At the beginning of the NFT boom, you were not optimistic about it. When did you start to change your view? What was the specific process of changing your mindset and actions?

Wang Feng: I personally started in software product design and game development, so what I feel most strongly about is creating applications and user experiences. I don't really believe in abstract things that are built on sand. Before 2021, I was more focused on a series of applications in DeFi. In fact, I only started trading digital currencies during the DeFi period.

I bought my first BTC when it was at $3,000 and just held onto it. The same goes for ETH. So I missed out on EOS and didn't buy BNB or FTX, although our Consensus Lab was an early investor in FTX, which yielded good returns.

In the summer of 2019, CZ called me, and Binance invested $1 million in Mars Finance, giving us BNB, which was only a few dollars at that time. I said I only wanted dollars, and CZ said I could exchange the BNB myself, so we almost thoughtlessly converted it to dollars. Initially, I only believed in BTC and ETH. After DeFi gained traction, I developed a real interest in cryptocurrencies and trading, and I began to believe that blockchain technology would go far, with many developers participating to drive applications.

You could say that without DeFi, I might not have waited for the opportunity in NFTs. It was after I became fascinated with DeFi that I started to build a team to work on decentralized applications. I did a lot of internal encouragement, urging everyone to participate in DeFi and NFTs; how could you feel it if you didn't play?

As for my attention to the ERC721 protocol, it actually stems from Blueport Interactive, the game development company I founded, which went public in Hong Kong at the end of 2014. At that time, we had already developed over 15 online games. One day in the fourth quarter of 2017, I saw a blockchain game called CryptoKitties and quickly assembled a team of seven to design a similar product. My technical partner started participating in blockchain at that time, and unexpectedly, he has stuck with it ever since. Our project ran on a public chain designed by a domestic team, and we provided a version in less than ten days. So, I was among the earliest to touch NFTs.

However, at that time, I didn't expect the ERC721 protocol to have the robust wings it has today. What people fear most is that after doing something, they give up, and when others bring it up later, they no longer care. It was precisely because we touched it and then gave up, thinking that the timing for making games on the blockchain was not mature enough. Around the same time, Animoca Brands, which also had a gaming background, got involved. They not only invested in CryptoKitties but also in OpenSea, which sold CryptoKitties, and later in The Sandbox.

During the exploration of DeFi, we considered entering the lending market, looking at major lending protocols like Compound and AAVE. My technical partner researched them in depth for a while, and I also consulted with some entrepreneurial teams working on lending protocols multiple times, so I had some understanding. With a technically prepared team, starting an NFT trading protocol and market was not too daunting. In fact, our development team quickly wrote our first-generation trading protocol.

2. Chain Catcher: In your early vision, what was the positioning and goal of Element? What was the biggest difficulty in this process?

Wang Feng: I will answer this question from four aspects, all of which require a change in mindset.

First, from the perspective of product development. The initial plan was to launch an NFT trading platform based on our own protocol, encapsulating a protocol into a market and then operating the trading data. However, developing a mature NFT trading platform involves a significant amount of work and implementation difficulty. It's not just about resolving Web3 technology stacks like trading protocols and on-chain data cleaning; there's also a substantial workload in practical Web2 functionalities. This process requires continuous refinement from the product development team, and creating a quality product takes time.

Second, most of our team members come from application and game development backgrounds. When benchmarking products like OpenSea, our first reaction was still how to create a better experience. It wasn't until three months after the product launch that we understood that the fundamental value of a trading platform is not just traffic but also solving liquidity effectively.

Third, in the early market entry phase, we did consider creating an OpenSea specifically for the Chinese market, but we quickly realized that Web3 likely does not have so-called national or regional markets; it cannot be compared to the Web2 era's Taobao in China versus eBay in the U.S. Blockchain is a new Mediterranean civilization; you can view each public chain as a Greek city-state. Today's Ethereum might already be the crypto version of the Roman Republic.

OpenSea can succeed on Ethereum, Magic Eden can succeed on Solana, and of course, I can seek a way out on the BNB Chain. So, we quickly launched a version supporting the BNB Chain and then extended it to more EVM chains. In the fourth quarter of last year, many GameFi projects were only focused on the BNB Chain ecosystem, and we received positive cooperation from some GameFi projects, stabilizing our data on the BNB Chain. With some confidence, we then began to allocate time to address the Ethereum market, leading to our final decision to adopt a multi-chain and aggregation product strategy.

Fourth, because each ecosystem has different supporters and operational strategies, we internally considered whether to adopt different brand strategies. Ultimately, we decided to stick with the Element brand for all chain-integrated markets, as we hope users and investors can trust our sincerity. Therefore, our homepage has different entry points for various public chain markets.

3. Chain Catcher: From mid-last year to now, what major changes or new trends do you think have occurred in the NFT industry? What strategic adjustments has Element made in response?

Wang Feng: In fact, many people misjudged the situation at the beginning of last year. Many of the first batch of entrants mainly saw opportunities in purely artistic assets. At that time, I was somewhat skeptical about this. Having focused on online games for ten years, I certainly understand the value of artistic design in products, but I lacked the ability to assess the pure art market. I personally understand the mass market better. At that time, it wasn't just OpenSea dominating; many art platforms were also gaining attention, and Beeple was very popular. Meanwhile, Axie Infinity and Flow's public chains were thriving, and not many people were focusing on PFP (Profile Picture) NFTs.

I believe the largest market in the future will be Ethereum. If OpenSea continues to dominate the NFT market, there will always be opportunities for us to break that dominance. This is a tough nut to crack, and we cannot bypass it. To compete with OpenSea, we must first cooperate with them. Through this process, we realized the fascinating competitive cooperation relationship in the crypto market, which actually stems from composability. We started thinking about doing aggregated orders at the end of 2021. There was a period of detours, and the finalized product planning began in March 2022. During this time, both LooksRare and GEM, based on trading mining, provided me with significant inspiration on how to achieve trading depth in an NFT market; we had to find our own way. No external forces can help you.

I don't believe that simply finding good assets to create a LaunchPad can build a good trading platform. If we don't solve trading depth from a product design perspective, any assets that come in will ultimately flow to the OpenSea market. Many trading platforms entering the market are essentially just acting as quasi-publishers. Even if you find Yuya Mitsushima or Ronaldo, they will ultimately converge into the vast sea of OpenSea's secondary market. It's not that being a publisher is bad; in fact, the teams that made the most money last year were precisely those that focused on NFT publishing. But we are building an NFT trading market, not asset issuance. If we really wanted to be a publisher, we wouldn't need to go through the trouble of creating a user-friendly trading market; we could just build an NFT brand, find IP projects, write bot scripts, and engage with the community.

4. Chain Catcher: Now, Element has become one of the most representative projects among Chinese initiatives and an important competitor in the NFT trading platform space. How would you rate Element's current achievements? Can you share some of the most impressive moments during this process?

Wang Feng: I have never started a business without feeling anxious, fearing that I won't do well. Therefore, I have always been critical of myself. I hold myself to a higher standard than I do others. A friend in Silicon Valley told me this is a psychological disorder. I don't know how to rate it. What I don't want for myself, I won't recommend to others. So, if the product isn't good, I have no face to speak.

Objectively speaking, the Element 2.0 product version is already a highly usable NFT trading platform. Personally, I hardly use OpenSea anymore, and many people around me feel the same way. This state began to emerge gradually three months ago, which is why we started recruiting volunteers in our community. In the past month, people have been saying that once they use Element, they can't go back to OpenSea. This is the most gratifying thing I've heard.

From a purely product and technical perspective, Element's advantages mainly lie in four dimensions: complete on-chain asset coverage, deep order aggregation, tool usability, and real-time data tracking. Because we are rooted in decentralized infrastructure, the NFT trading platform shares many commonalities with DeFi, as both are driven by a foundational protocol. However, the NFT market is increasingly resembling the currently dominant CEX (Centralized Exchange) market, which is a sentiment that has been increasingly echoed by our community and product operations team. For this reason, much of our technical team's workload is also Offchain. Those who have not personally operated an NFT trading platform may underestimate these factors.

5. Chain Catcher: As a Chinese project, one of the biggest challenges is how to expand into the overseas user market. What obstacles have you encountered in this regard? How internationalized is your team currently? What specific strategies have you adopted to expand into overseas markets?

Wang Feng: First, we are looking for people overseas. We have four people stationed in the U.S. market. We need to find trustworthy individuals and then segment the market into multi-chain, multi-language, and regional operations. Each regional market must have local people to cover it, especially experienced individuals who understand NFTs. For the North American market, we have the fourth employee to join OpenSea helping us expand there. They are familiar with resource connections within the ecosystem, such as Coinbase Wallet and Metamask.

Second, we focus on creator relationships. Our director of creator community is a creator himself, and the creator circle is very important. Currently, we have gradually started collaborating with Outland and selected artists from NYC.

In fact, many of our volunteers come from multilingual regions such as Taiwan, Japan, South Korea, Canada, France, and Australia. They are already NFT traders with a deeper understanding of the business than ordinary users. Our relationship with them is steadily built on a commission-based referral system, and Element was one of the first to support a referral commission mechanism.

6. Chain Catcher: From data websites, Element still has a certain distance from the trading volume and user numbers of leading NFT markets like OpenSea. Where do you think the main gaps lie?

Wang Feng: In fact, the only gap is time. Previously, we were 1% of their market; our current goal is to reach 10%. OpenSea's last round was valued at $13 billion, and they entered the market five years before us, so we need some time.

If emerging assets do not rise, and everyone is just competing for the existing PFP market, should investors not invest in new trading markets? The answer is definitely not. Before the next wave of emerging asset categories explodes, we should first refine a user-friendly Web3 product. In R&D, we have grown from fewer than ten people to over twenty now. If we secure more investment, we will also need to invest in personnel for protocols, tools, and data services, ensuring that everyone is convinced and feels the need to use our platform. In today's bear market, having a product team that is not short on funds can allow us to focus on product quality and listen to community user feedback, which could be a blessing in disguise.

We might as well do something that breaks the mold. Because OpenSea holds an absolute dominant position in the Ethereum market, we made the decision at the beginning of the year to aggregate OpenSea and existing leading trading platforms in the Ethereum market. Currently, the aggregation protocol released in Element 2.0 has already gained recognition from many users.

In terms of trading experience, we also plan to first surpass OpenSea in tool usability before seeking new opportunities in the changing landscape. I believe that domain asset opportunities like ENS, SpaceID, and .bit are actually opportunities for functional NFTs. Specifically, the recently very active Space ID, which is an ENS in the BNB Chain ecosystem, allows us to provide customization based on the characteristics of domain NFTs, such as enumerating and categorizing based on numerical and alphabetical combinations, along with our product's advantages in batch processing tools for trading. Element has captured about 75% of the secondary market share. I have already seen daily transaction numbers exceeding 8,000.

Starbucks combining consumer points with NFTs is also a landmark event. I estimate that more offline institutions and Web2 companies will enter the market to issue Pass cards, and rights-based assets are likely to have opportunities to rise. Whether in terms of practical value or cross-border capability, Pass cards may not be a fleeting trend but rather a lasting phenomenon, not just a meme. The next wave of GameFi products will eventually rise, and we are focused on finding new asset customization tools that cater to user experience. The market will always provide opportunities for diligent players to overtake competitors.

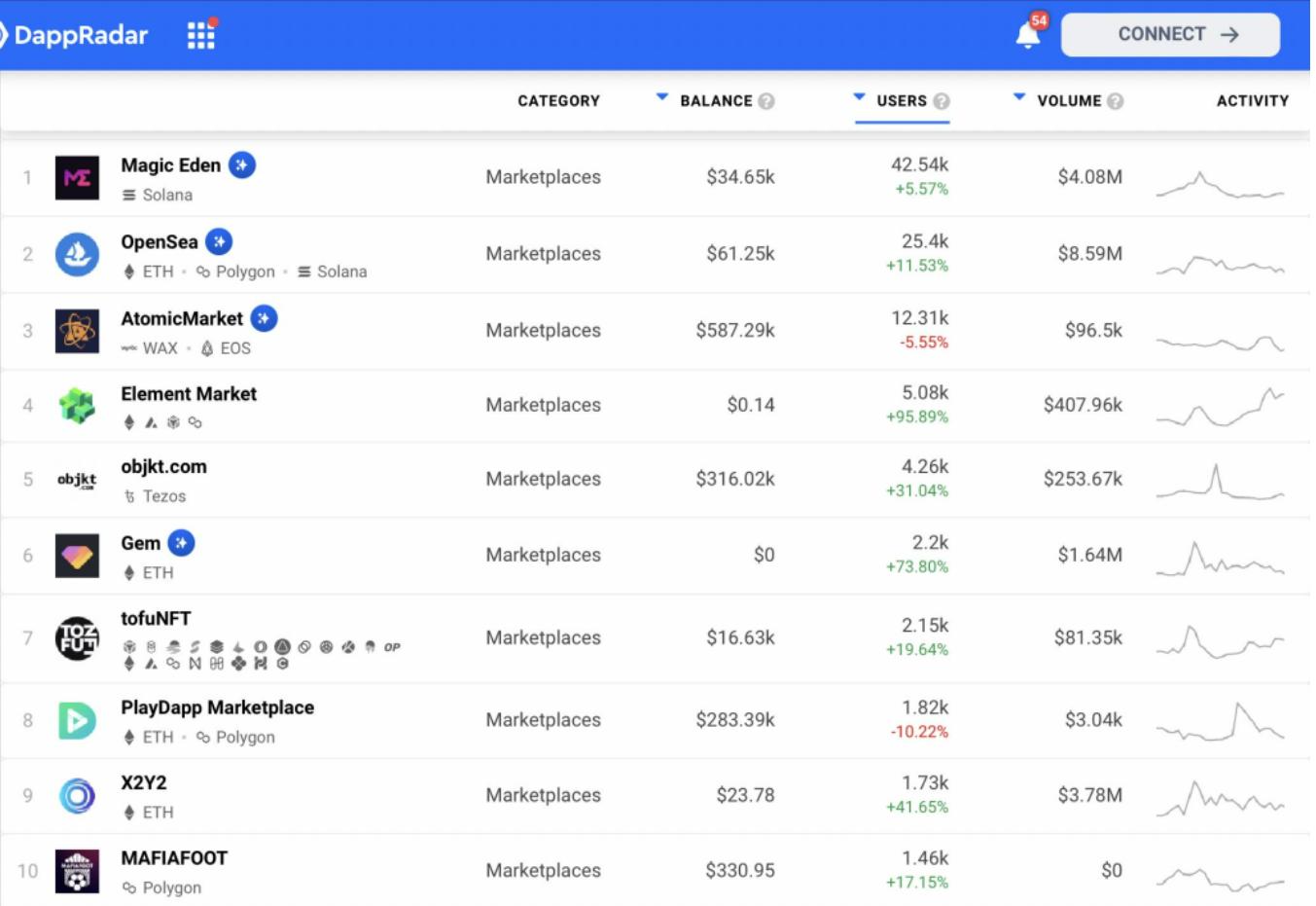

Element's highest ranking has reached fourth

7. Chain Catcher: You once mentioned that OpenSea is moving too slowly in terms of product development. Why do you believe that entering from a tool perspective can compete with OpenSea?

Wang Feng: In terms of product iteration speed, we are definitely moving faster than OpenSea. However, newcomers cannot simply replicate what others have done; there are only two paths: one is product differentiation, such as creating a market focused on aggregation and tools, which requires some competitive spirit, and the market users will validate that. The second is to innovate in operations. We chose the first path, and this perspective was inspired by the transition from the Uniswap AMM model to the 1Inch aggregation trading model in the DEX market. We believe that developing a product focused on aggregated trading is the space left for us by the market, and it is also more suitable for our technical and product design team. If we solve product issues well, operations will have the space for bold exploration.

8. Chain Catcher: Nowadays, multi-chain expansion is the strategic direction for most projects. Element also supports multiple networks like Polygon and BNB Chain, and the official website indicates plans to support Solana, although it has not yet launched. What are the reasons behind this?

Wang Feng: We have invested considerable effort into the BNB Chain. Although there is currently a lack of quality PFP projects on the BNB Chain, we believe that purely relying on PFP NFT trends will soon change. The potential of the BNB Chain in the NFT market is still underestimated. We hope to maintain a leading position in the BNB Chain market, ideally achieving absolute first place. This may take some time.

Additionally, we still plan to enter the Solana market through aggregated trading. In fact, there are always opportunities, such as the new public chain leader Aptos in the Move ecosystem, with whom we are also in contact. Let's wait and see.

9. Chain Catcher: Looking back now, have you made any mistakes during this year of entrepreneurship?

Wang Feng: If I could do it again, we should have gone straight for the Solana public chain market.

Last September, I bought four Crypto Punks with 400 ETH, which caused me to miss out on a Bored Ape that was less than 10 ETH. The former has fluctuated without significant change, while the latter surged 15 times during the same period. If I had researched social sentiment and DC groups more deeply at that time, I might have made a more rational judgment.

However, the biggest mistake we made last year was thinking we would succeed quickly. Worse than the mistake itself is the pain of making mistakes. Specifically, it's the pain of choice; without choices, there is no real pain. This is the biggest difficulty for an entrepreneurial team—not whether someone else has designated a direction for you to charge ahead, but whether you have chosen a path that you can continue on. Especially when you know that differentiation is key, doing as little as possible while finding truly long-term valuable things that match timing, capability, and funding is genuinely difficult. Sometimes we can only look up and hope for luck.

When we were in school, we often confidently chose A, B, C, or D in multiple-choice questions without thinking, but when it came to application questions, we would bite the pencil and feel at a loss. In reality, making choices is often harder than solving application problems.

10. Chain Catcher: Currently, horizontal and vertical integration and mergers in the overseas NFT market are very evident. Does this put pressure on you? If OpenSea integrates GEM in the future and Uniswap integrates Genie on the front end, what impact do you think this will have on the NFT market?

Wang Feng: In fact, I am very pleased to see these two mergers, as they signal positive developments in the market.

Currently, among aggregation trading platforms, we are the only ones that have not been sold, and we also support multiple chains, while GEM only operates on Ethereum.

11. Chain Catcher: At present, several independent NFT trading aggregators still have relatively low trading shares in the overall market. Why is it that even with the best liquidity, trading aggregators still struggle to win over the majority of users? What do you think are the main factors and issues users focus on when purchasing NFTs?

Wang Feng: I actually believe that aggregated trading will increasingly capture a larger market share.

Our users are traders. In the art market, there is a term called collectors, but today's market is still dominated by typical traders. No profit means no motivation, but different types of traders focus on different aspects. Their preferences and investment time horizons all influence their trading decisions.

12. Chain Catcher: In terms of enhancing liquidity, X2Y2 and LooksRare have adopted trading mining. Although there are obvious signs of volume manipulation, it has greatly helped increase trading volume and influence. How do you view the sustainability and practical effects of this model?

Wang Feng: LooksRare and X2Y2 entered the market earlier this year with trading rewards, quickly gaining market influence. We rely on our product, so our actions in the market are much clumsier than theirs. At that time, we were preparing to move towards providing aggregation protocols. I was initially very skeptical of them, but I noticed that both companies continuously iterated their operational strategies, including alternating between invitation rewards and trading rewards. I admire their operational capabilities.

However, fundamentally, I have never believed that trading platforms should make trading mining a core operational strategy. While it is an effective cold-start solution, a user's interest in choosing from multiple asset values shifts to selecting based on the inequality formed between direct trading costs and mining rewards. Therefore, their primary demand from the platform is to "farm" rewards. This is somewhat akin to sprinters or swimmers using performance-enhancing drugs; you can't overdo it. Have you ever seen marathon runners using performance enhancers?

We will not make trading mining a core part of our product. However, we do not reject conducting some time-limited promotional reward activities. But I don't think it's wise for a trading platform to include trading mining in its economic model. I wonder if such teams have long-term aspirations to continue. If you have worked hard to develop a trading platform but have not allocated token assets to genuine trading users or your supportive investors, only to have it monopolized by a few miners, leading you to have to mine your own tokens, that is truly a case of drinking poison to quench thirst.

Long-term solutions for enhancing liquidity in a trading market should still focus on the product's professional service capabilities in trading, such as improving trading efficiency and developing aggregation pricing systems. It should also involve asset collaboration capabilities, branding, and reputation. As I said, marathon runners do not use performance enhancers.

13. Chain Catcher: From a medium to long-term perspective, what are Element's market goals? What specific plans can you share moving forward?

Wang Feng: Element has two directions: one is to become a very mature NFT trading market, and the other is to move towards complete community governance by launching ELE DAO to operate more businesses.

From an operational efficiency perspective, these two paths conflict with each other. Therefore, we are still in a product-centered process, focusing on rapid iteration in R&D and valuing community feedback.

14. Chain Catcher: Element will also issue tokens and establish a DAO. What role will the ELE token play in enhancing platform liquidity and attracting new users? Many DAOs today are actually pseudo-decentralized; to what extent do you hope to achieve decentralization?

Wang Feng: If we officially launch the ELE token, we hope to provide incentive tokens for users and the market. However, we will not use token financing. Our investors are all equity capital. Last year, we secured $11.5 million in investment from Sequoia, SIG, and DragonFly, and our future tokens will be for users, shareholders, and the team.

As for the complete ELE DAO plan, we still need some time to prepare, seeking input from investors and the community. We are opening a community forum.

15. Chain Catcher: OpenSea was previously reported to be planning an IPO, and its management is very centralized, which has drawn criticism for being contrary to the spirit of crypto. How do you view this controversy? As a very centralized project, yet the largest NFT market, how important is decentralization for the long-term development of a project?

Wang Feng: A platform's market position is determined by its users; whether users like it or can tolerate it is a decision made by their votes. We will not attract attention by criticizing OpenSea, nor do we have any reason to criticize them. I have never seen Binance publicly criticize Coinbase.

Conversely, I increasingly believe in a prediction that the NFT trading market will coexist in a state of semi-centralized and decentralized market operations. This is largely similar to the current ecosystem of the digital currency trading market. After we started operating in the NFT trading space, we better understood Binance's strengths. In trading, many things are interconnected.

16. Chain Catcher: Since the launch of the Coinbase NFT market, it has faced criticism for low trading volumes, which do not meet market expectations. Why do you think this product has been met with cold reception? What issues exist in Coinbase's NFT development strategy?

Wang Feng: The problems Coinbase faces in the NFT market are almost identical to those encountered by most cryptocurrency exchanges entering the NFT space: an overreliance on traffic and capital advantages as key competitive capabilities. In fact, the core competitive capabilities of any market are focus, differentiated choices, and cost leadership, which is Michael Porter's three elements of competition. I have not seen Coinbase do the right things. The only difference in their product compared to OpenSea might be a more elegant interface; in terms of technical solutions, they merely integrated the V4 version of the 0x protocol released in March this year. It seems that the NFT team they assembled has not done much.

Moreover, centralized trading markets and decentralized trading markets represent two distinct eras in the crypto world. It's somewhat like when Yahoo saw Google emerge and thought that simply adding a search box to their content portal would allow them to crush the competition. Little did they know that true competitive advantage comes from technological pathways and operational concepts, not just traffic advantages, capital, and existing brand definitions.

17. Chain Catcher: Currently, speculation in the NFT field is very serious, and Vitalik has also expressed concerns about the excessive financialization of the crypto industry. What do you think are the non-financial scenarios for NFTs? How do you view the recent popularity of soulbound tokens (SBT)?

Wang Feng: I completely understand Vitalik's concerns. Blockchain was born from a monetary hypothesis experiment, which then sparked a revolution in more financial scenarios. However, blockchain is not just about finance. This issue has been reiterated many times. There was a time when people fell into the trap of blockchain anti-counterfeiting. I believe that since the inception of Bitcoin's block creation and accounting, blockchain's inherent advantage lies in its decentralized mechanism, allowing for a one-to-one record that can be written and read but not altered. SBT is such a product.

In fact, our current Web3 identities are trapped in the historical scenarios of Web2 that they aim to break free from, often being humorously referred to as Web2.5/Web2.8. For example, most NFT artists rely on centralized platforms like OpenSea and Twitter to promise the initial provenance of their identities. In the crypto universe, there is no native identity beacon; various credential proofs rely entirely on the discerning eyes of Web2's big brother. If we were to revisit digital existence today, it would be ironically evident that global users still live in the Orwellian 1984 and Animal Farm, only with the big brother replaced by global social giants. Even our token voting DAOs today often rely on Web2 infrastructure, such as having to use social media accounts to fend off witch hunts.

I believe that more attention should be paid to the underlying DID (Decentralized Identifier), which is the so-called native crypto identity marker. The latter is like a decentralized passport, while the former represents various stamps and visas on the passport. A single passport can have many visas. Personally, I am more interested in DID as the foundational application for the new digital society.

18. Chain Catcher: Public data shows that the current market trading volume of NFTs is less than one-tenth of its peak. Many believe the NFT market has entered a bear market. What do you think the upcoming stimulus factors or incremental markets for the NFT market might come from?

Wang Feng: Pass cards, functional NFTs, and GameFi, which integrate with traditional economies, may all present new opportunities.

After a bear market comes a bull market. If we can increase our user base by ten times during a bear market, we won't have to worry about when the bull market will return.

Risk warning

Risk warning Risk warning

Risk warning