Startup Warning: How BlockFi Went from Tech Unicorn to Decline?

It turns out that one or two seemingly insignificant mistakes could be nearly fatal flaws for this highly valued startup.

It turns out that one or two seemingly insignificant mistakes could be nearly fatal flaws for this highly valued startup.Source: Blockworks

Compilation by: Bitpush Mary Liu

"Watching him build high towers, watching him host guests, watching his towers collapse."

Just 12 months ago, BlockFi was thriving in its business operations.

During the crypto bull market and the wave of astonishing company valuations in 2021, this cryptocurrency lending platform became one of the fastest-growing startups in the industry, raising hundreds of millions of dollars from blue-chip venture capitalists like Bain Capital, Tiger Capital, and Peter Thiel's Valar Ventures.

Everything seemed to be going smoothly, and nothing could stop the ambition of BlockFi CEO Zac Prince, but no one anticipated what would come later: a "bargain" acquisition price of $240 million, with FTX's Sam Bankman-Fried (SBF) stepping in at the last moment to "rescue" the company.

Sources told Blockworks that the essence and reasons behind the issues are important lessons not only for BlockFi but for all crypto companies operating amid market cycles.

In Prince's case, the warning signs can be traced back at least a year, when a series of key (and even problematic) management decisions led the lending platform into a spiral of collapse.

What was the first domino? --- BlockFi executives were eager to raise venture capital from some of Wall Street's biggest players, even as the crypto market was in turmoil.

In the days leading up to the deal with FTX, reports indicated that Bankman-Fried was able to acquire BlockFi for as low as $15 million, prompting Prince to arrange a series of executive meetings to seek better options. According to Prince's Google calendar, this included meetings with ConsenSys, Binance, Fortress, JPMorgan, Galaxy Digital, and blockchain giant Barry Silbert, among others.

Blockworks spoke with three sources familiar with the matter, including current and former BlockFi employees. Blockworks obtained some internal company documents, and sources were allowed to discuss sensitive business transactions anonymously.

It turned out that one or two seemingly insignificant mistakes could be the near-fatal flaws for this overvalued startup.

Turning Point of Fate

A problematic fundraising effort (the outcome of which had not been reported before): the Series E funding originally scheduled for June 2021, where Prince set an ambitious goal of raising $500 million at a $4.5 billion valuation.

Prince pitched BlockFi to well-known crypto investors and traditional asset management firms. Some of these options included Third Point Management, led by renowned hedge fund manager Dan Loeb, where BlockFi would directly list or be acquired at a $9 billion valuation under various stringent terms. Other target firms included London-based venture capital firm Hedosophia and other notable venture capitalists.

Sources said that without Third Point's participation, the fundraising ultimately ended with less than half of Prince's target, at $225 million—despite the same valuation.

Sources pointed out that the reasons for the fundraising shortfall included a blunder weeks earlier when BlockFi mistakenly sent Bitcoin promotional rewards, as well as the potential for future regulatory conflicts: a month later, state regulators in New Jersey, Texas, Alabama, and Vermont ordered the startup to stop offering crypto interest products.

In this promotional blunder, BlockFi mistakenly issued Bitcoin as a stablecoin, with some users receiving up to 700 BTC (worth $28 million) instead of the expected $700. Another Reddit user reported receiving an email from BlockFi requesting the return of funds and threatening legal action.

According to two sources, at least one employee was fired over the incident.

Nevertheless, after the startup secured $350 million in Series D funding in March 2021, the Series E funding ended with a significant shortfall, but its valuation jumped from unicorn status to $3 billion (BlockFi's Series C ended in August 2020, valuing the company at $450 million).

Sources described BlockFi's decline as a cautionary tale about tech startups, which experienced exponential growth—but lacked a robust balance sheet to prepare for a bear market.

For BlockFi, the threat of a bear market was quickly replaced by regulatory conflicts. Last November—one week after Bitcoin hit an all-time high of $69,000—media reports detailed the U.S. Securities and Exchange Commission's (SEC) dissatisfaction with BlockFi's interest-bearing crypto accounts, which federal regulators viewed as securities, echoing the concerns of state regulators.

The SEC investigation severely impacted company morale, occurring six months after the promotional blunder incident.

In February 2022, a settlement was reached, with BlockFi agreeing to pay $100 million in fines to federal and state regulators, and the company also agreed to stop offering its yield products to U.S. retail investors (but continued for institutional clients).

BlockFi had intended to register its interest-bearing accounts as securities, which would allow the product to be marketed again to U.S. retail investors.

However, Blockworks learned that this plan was delayed again in late August, pending an audit.

Internally, BlockFi employees indicated that company leadership began to view the SEC's scrutiny as a positive.

One source said, "The story is, 'This is actually great; now we can be one of the first crypto companies registered with the SEC—we're paving the way for that.'"

Despite the potential appeal of SEC support, BlockFi, which once attracted about 70% of customer deposits in the U.S., was watching its customers leave.

A Bigger Crisis?

Sources attributed customer attrition as a major reason for the fundraising failure.

BlockFi closed accounts for U.S. traders between February and March, with new registrations dropping by about half, leading to even greater user outflows. BlockFi's user deposits peaked at over $10 billion last year—briefly hovering around $8 billion before quickly shrinking to between $2 billion and $3 billion.

The crypto bear market further weighed down the company, with the total crypto market cap shrinking by nearly 60%.

Series F Funding to SBF

It was clear that Bankman-Fried's cash injection—directly purchasing BlockFi's options—was a mixed outcome for Prince after an arduous 18 months.

Insiders detailed many issues, such as the obscure programming language Elixir driving a lengthy tech stack, a rough "digitally driven" incentive structure, and deposit-raising tasks, among others.

One source said, "We were building a terrible tech stack, which made our development speed painfully slow—launching products and updates was slower than our competitors, and the company had to hire more developers to catch up."

Sources said BlockFi fired its chief technology officer last year, who had joined in 2018. The company also asked its chief growth officer to leave.

Several other key employees recently left voluntarily, including other growth and development leads and vice president of strategy and finance Mitch Port.

Port, who held a position as a senior associate partner at Bain, declined to comment, only stating that BlockFi was "an incredible company to work with some of the most talented people I've ever worked with."

Other executives also decided to exit, including David Olsson, Shane O'Callaghan, and Samia Bayou. Key figures in BlockFi's institutional business remain, including senior Bank of America executives Giles Colwell and Brian Oliver. Oliver joined in May, having worked for a decade at private equity firm Red Devil Investors.

At its peak, BlockFi had about 1,000 employees, and its growth trajectory in some ways distanced the company's core business from its crypto-native attributes.

For instance, the company's recent chief marketing and growth officer had no professional crypto experience, like many new hires—this shift was viewed internally as a positive: non-crypto professionals should attract other similar talent.

BlockFi Seeks Liquidity—Very Urgently

With support from JPMorgan, Prince and other executives were encouraged when seeking Series F funding at the end of 2021, believing it was a secret ace: BlockFi's interest-bearing accounts would soon become the first and only product registered with the SEC, theoretically attracting a large number of retail investors.

Sources said BlockFi initially sought to raise up to $500 million at a valuation of $6 billion to $7 billion (about 60% higher than the previous round), but given the company's ban on serving new U.S. customers, it proved to be a difficult fundraising process.

Meanwhile, employees were told that the company would soon go public. As negotiations dragged on, the target valuation became unattainable, ultimately settling on a goal of raising $85 million at a $1 billion valuation.

One condition for raising these funds was to cut 20% of the workforce to increase profitability, a plan also executed by industry firms like Coinbase and Gemini.

Sources said BlockFi assured employees it was solvent, claiming it could have handled double the withdrawals during the market crash in May and June. According to company documents, customers withdrew about 30,000 Bitcoin (now worth $568 million), 230,000 Ethereum (now worth $292 million), and $1.5 billion in stablecoins between June and July.

While it remains unclear how close BlockFi was to the brink of collapse, the company never paused withdrawals or other functions during the widespread crypto bear market. Sources described the company as a strong, ethical participant that simply found itself in a difficult situation; otherwise, SBF would not have stepped in to save it.

Competitors Celsius and Voyager struggled under the weight of cascading liquidations, margin calls, and price crashes, with funds fleeing the panicked market leading to the bankruptcy of both companies, resulting in significant losses for tens of thousands of users.

BlockFi took the opposite approach. The company could have—assuming it was in a true crisis—sold off collateral from its institutional clients to facilitate user withdrawals, though such extreme measures would certainly unsettle its institutional clients.

In any case, uncontrolled withdrawals and looming threats only made raising cash more urgent.

BlockFi's "Fire Sale"

On Friday, June 10—three days before BlockFi laid off 20% of its staff—Prince's phone rang at 9:00 AM with an important notification: "Contact major investors," followed by a board meeting two hours later.

Subsequently, a week-long series of meetings was scheduled, starting Sunday at 10:30 AM, including a 30-minute call with Kyle Davies and Su Zhu, co-founders of the now-bankrupt Three Arrows Capital, and other executives like BlockFi's institutional general manager Brian Oliver.

Four days later, BlockFi announced it had liquidated all positions with Three Arrows Capital.

Aside from private sessions, the only scheduled meeting that was absent was a week-long series called the "Batman Plan," involving Prince, Amit Cheela (BlockFi's senior vice president of finance), Matthew Chan (BlockFi's corporate development strategist), and JPMorgan investment bankers focused on fintech.

Here is the internal meeting schedule:

June 15

8:30 AM: Mark Yusko (CEO of Morgan Creek)

9:30 AM: Tony Lauro (CFO of BlockFi); Flori Marquez (co-founder of BlockFi); Jonathan Mayers (general counsel of BlockFi)

6:15 PM: Robby Gutmann (CEO of NYDIG; head of Stone Ridge digital asset strategy); Ross Stevens (CEO of Stone Ridge); Marquez (co-founder of BlockFi)

June 16

9:00 AM: Marquez (co-founder of BlockFi); Lauro (CFO of BlockFi); James Fitzgerald (founding partner of Valar Ventures); Andrew McCormack (founding partner of Valar Ventures)

10:30 AM: Yusko (CEO of Morgan Creek)

June 17

2:45 PM: Richard Chang (head of capital markets at FTX Ventures)

4:00 PM: Barry Silbert (CEO of Digital Currency Group)

June 18

12:00 PM: Gutmann (CEO of NYDIG; head of Stone Ridge digital asset strategy); Stevens (CEO of Stone Ridge); Fitzgerald (founding partner of Valar Ventures); McCormack (founding partner of Valar Ventures); David Heller (investor, former Goldman Sachs executive)

3:30 PM: Chris Ferraro (CIO of Galaxy Digital)

6:00 PM: BlockFi legal team

8:00 PM: Thomas Farley (incoming CEO of Bullish)

June 19

8:30 AM: Bankman-Fried (CEO of FTX); Caroline Ellison (CEO of Alameda Research); Ramnik Arora (head of product at FTX)

9:00 AM: Brian McGrath (general partner at Ribbit Capital)

1:00 PM: Peter Briger (head of Fortress), Mayers (general counsel of BlockFi)

2:00 PM: Cheela (senior vice president of finance at BlockFi); Ellison (CEO of Alameda Research); Arora (head of product at FTX); Bankman-Fried (CEO of FTX); Mayers (general counsel of BlockFi)

5:00 PM: Cheela, Phil Rich (Binance, M&A); Kaiser Ng (Binance senior vice president of finance); Ken Li (Binance, M&A); Michael Chan (Binance head of M&A)

6:00 PM: BlockFi board with three Haynes Boone lawyers (BlockFi's external law firm)

8:00 PM: Cheela, David Merin (head of corporate development at ConsenSys), Matthew Gilmour (assistant in corporate development at ConsenSys)

June 20

8:30 AM: Gavin Michael (CEO of Bakkt)

9:00 AM: Howard Chen (co-head of market infrastructure at JPMorgan); Dan Pombo (head of restructuring at JPMorgan); Jeremy Sipzner (executive director at JPMorgan), Xavier Loriferne (managing director of M&A at JPMorgan); Keith Canton (head of private capital markets at JPMorgan)

9:30 AM: Peter Smith (CEO of Blockchain.com)

4:00 PM: Tom Jessup (president of Fidelity Digital Assets)

5:00 PM: Marshall Beard (chief strategy officer at Gemini)

6:00 PM: FTX executives

June 21

9:30 AM: Marquez (co-founder of BlockFi); Lauro (CFO of BlockFi); Frederik Mijnhardt (CEO of SecFi)

11:00 AM: BlockFi all-hands meeting announcing the FTX rescue plan

11:30 AM: Bloomberg reporters

While it remains unclear whether each of these conference calls ultimately took place, all attendees were present, and Prince arranged meetings with executives from Binance, Ribbit Capital, ConsenSys, Fidelity, Bakkt, and Gemini between multiple calls with Bankman-Fried.

A month later, BlockFi offered voluntary severance packages of 10 weeks' pay to 80% to 90% of remaining employees (about 700 people). According to sources, about 200 accepted, leaving the company with 400 to 500 employees.

Some of the remaining employees received a separate, more complex contract: a 10% raise, with the potential for up to a 20% raise within six months if new, stricter metrics were met.

These metrics included increasing the value of private client deposits in interest-bearing accounts to $3 billion by the end of January and reducing cash burn to below $6 billion by the end of the year.

In fact, like many of its struggling startup peers, BlockFi had almost no net positive cash flow.

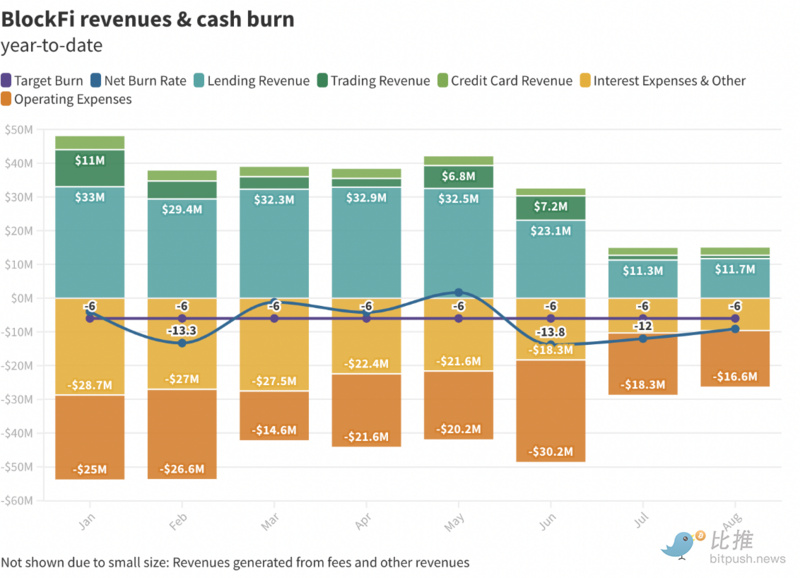

An internal document showed that the company's operating cash flow lost $13.8 million in June, its worst month of the year, with losses of $12 million and $9.1 million in July and August, respectively—averaging a monthly loss of $7 million in 2022.

The document also revealed that BlockFi had only one month of positive operating cash flow this year: May, with a positive gain of $1.7 million, which was a particularly optimistic and hopeful performance.

From the beginning of 2022 to August, BlockFi's cash burn totaled $55.9 million.

What is the Cost of Corporate Integrity?

What BlockFi's next steps are remains uncertain. Some prominent crypto players, while refusing to comment publicly, praised the company's efforts and integrity—especially noting their willingness to dive into alternative revenue sources rather than doubling down on something useless.

One source said, "Do I want to be BlockFi? No, [the executives] made a lot of money. They could have cashed out and closed. They could have exploited their investors, but what they are choosing to do now is much harder."

To make matters worse, the decoupling of stablecoin Terra triggered an implosion, and the collapses of competing crypto lending platforms Celsius and Voyager led to a 70% drop in BlockFi's monthly revenue to $15 million by July and August.

The company earned $48 million in January from its loan ($33 million), trading ($11 million), and credit card ($4 million) revenue streams.

In July and August, BlockFi attracted $15 million in monthly revenue across its three main products, with loans accounting for nearly 80%. Overall, this was less than half of the company's $32.5 million revenue in June.

BlockFi's credit card business has proven to be more resilient than its trading, recently generating about $2.3 million in monthly revenue, down from $4 million in January. August's trading revenue was only $1 million, down from $6.8 million and $7.2 million in May and June, respectively.

According to internal documents and sources, the company now hopes to build global fiat on- and off-ramps, support for Stripe payments, and provide crypto derivatives to its institutional clients, with a Stripe spokesperson declining to comment.

While such integrations do not necessarily mean establishing clear partnerships with payment giants, BlockFi will become a client of companies like FTX and Coinbase.

Incorporating FTX's custody services and launching derivatives for institutions, as well as activities to attract customer deposits, have already begun, with BlockFi still viewing lending and trading revenue as primary growth avenues.

BlockFi's U.S. license appears to be a major reward for Bankman-Fried and his powerful institutional business, although it will take a long time to obtain.

One source said most company employees are still waiting to learn what will happen to their equity. It may convert to FTX stock, but under different and unknown fundamentals.

To retain employees, BlockFi recently increased the weight of its retention incentives from 40% to 80%, thereby reducing the importance of customer deposits and cash burn rates.

This is not a success story; the rapid rise of BlockFi witnessed co-founders Prince and Marquez briefly surpassing digital assets, transcending fintech, and entering the broader tech space, where they were eagerly covered by mainstream television shows and podcasts.

Many lessons can be drawn from the BlockFi saga, whether it's "be vigilant in times of peace," "customer deposits are a dangerous growth metric for crypto lending platforms," or "never mistakenly send Bitcoin as a stablecoin."

But perhaps, simply put in one sentence—"Never mistakenly send Bitcoin as a stablecoin."

Risk warning

Risk warning Risk warning

Risk warning