Dialogue Orbiter Finance: May issue native tokens, will open Maker system beta at the end of October

Orbiter likens the current Ethereum to a large city, and it will build fast and efficient bridges for the skyscrapers (Layer2) in the city.

Orbiter likens the current Ethereum to a large city, and it will build fast and efficient bridges for the skyscrapers (Layer2) in the city.Interview: Biscuit, ChainCatcher

Interviewee: Russell, Partner at Orbiter Finance

Ethereum is the origin and central hub of DeFi, but with the explosive growth of DeFi protocols, Ethereum is becoming increasingly congested. The development of emerging protocols in the future is likely to occur on Ethereum's Layer 2 scaling networks. Therefore, the demand for users to transfer funds between different L2 platforms is growing. In less than a year since its launch, Orbiter Finance has become one of the most mainstream cross-chain bridges by focusing on cross-chain asset transfers across Rollup networks.

Currently, Orbiter Finance supports over 10 Rollup networks, almost meeting all cross-chain needs for Optimistic Rollups and Zk Rollups, and enabling high-freedom cross-chain transfers such as from Loopring to Immutable X. At the same time, Orbiter is targeting the Layer 2 data track, launching a product in August this year that provides Layer 2 network and application data. Users can view daily active address counts, cumulative address counts, locked amounts, and more on this platform, and can also discover emerging quality projects based on data trends.

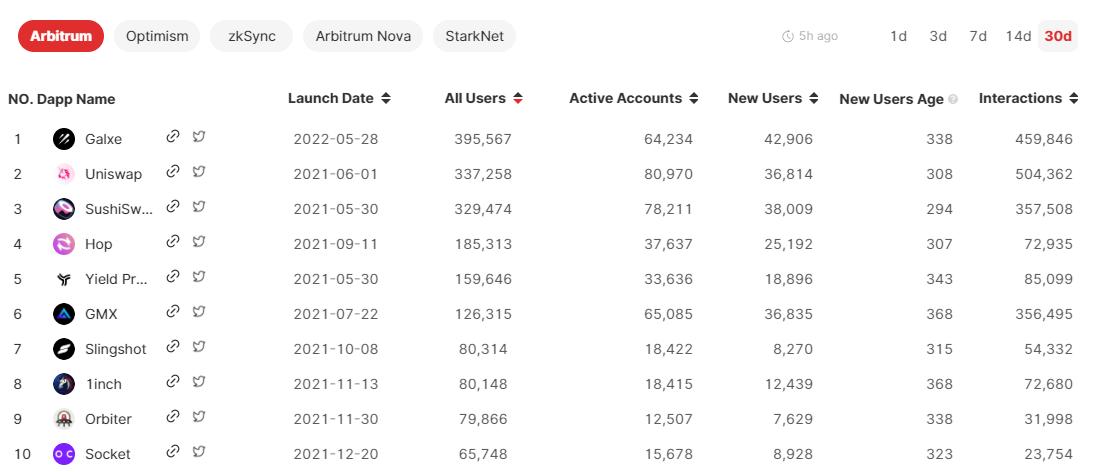

According to the product data, Orbiter Finance currently has accumulated transaction addresses reaching 79,000 on the Arbitrum network, with nearly 13,000 active addresses in the last 30 days. On the Optimism network, the accumulated transaction addresses have reached 40,000, with about 6,000 active addresses in the last 30 days, ranking around 10th among all DApps on both networks.

Compared to other cross-chain bridges, Orbiter Finance's main differentiating feature is the Maker mechanism, which acts as a smart contract-based intermediary with its client deployed across multiple networks. Users transfer crypto assets to the Maker and inform it of the target network where they want to receive the funds. After receiving the instruction, the Maker will transfer the crypto assets to the user's specified address on the target network. Currently, all liquidity for Orbiter Finance is provided by the team itself, but in the future, it will open up liquidity provision to all users, with a testnet expected to launch by the end of October.

Recently, ChainCatcher spoke with Russell, a partner at Orbiter Finance, about cross-chain bridges, including why Orbiter chose to focus on Layer 2 cross-chain, and discussed Orbiter Finance's business logic, future token plans, and more.

1. ChainCatcher: Please briefly introduce the development history of Orbiter Finance.

Orbiter Finance: Orbiter Finance is a project that started in April 2021. We launched the alpha version of our product on November 29 last year, with all features fully developed. In mid-July this year, we released the official version of Orbiter, redesigning the UI and UX, and adding features like viewing transaction history. Now, Orbiter is the cross-chain bridge supporting the most L2 environments.

2. ChainCatcher: What was the initial intention behind Orbiter Finance's focus on Layer 2 cross-chain compared to most other cross-chain bridges?

Orbiter Finance: First of all, we strongly recognize the development prospects of Layer 2. Vitalik once posted on the Ethereum Research forum about the design concept of Rollup Bridges in the post “Cross-Rollup DEX with Smart Contracts Only on the Destination Side,” which Orbiter has implemented while adding some optimized features.

Layer 2 cross-chain bridges are built on the infrastructure within the Ethereum network, with many aspects centered around Ethereum or Rollups, including security mechanisms and solutions.

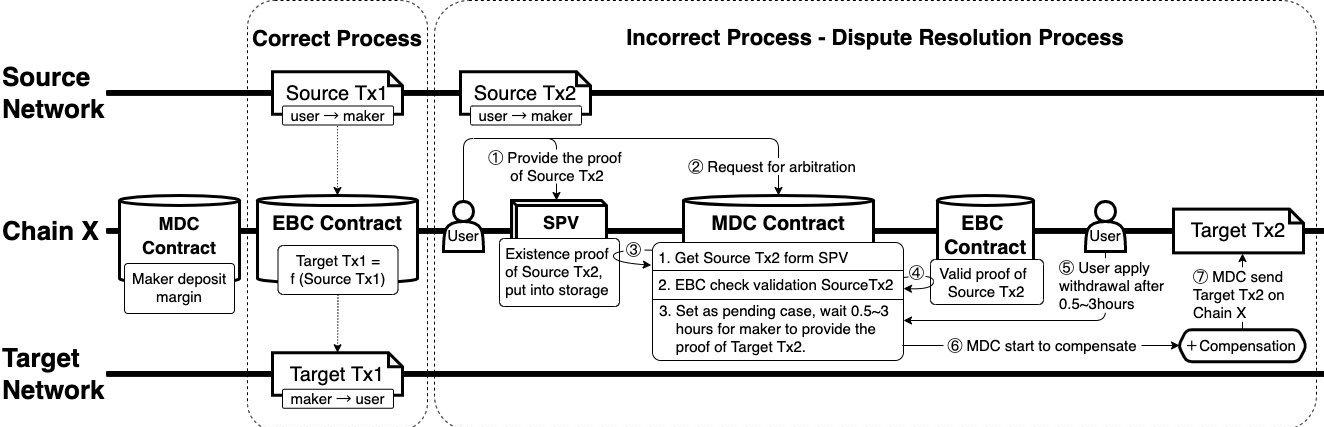

3. ChainCatcher: Can you elaborate on the overall operational logic of Orbiter Finance, such as how you utilize MDC, EBC, SPV, and other smart contracts to achieve secure and cost-effective asset cross-chain transfers? Additionally, could you explain the specific mechanisms of the core components Sender and Maker?

Orbiter Finance: Let me first explain the process for users to use Orbiter Finance for cross-chain transfers. For example, if a user (the Sender) wants to transfer ETH from zkSync to Arbitrum, after operating on the Orbiter web front end, the ETH will be transferred from the Sender's EOA address on zkSync to the Maker's EOA address on the same network. Once the Maker receives the ETH, it will send the tokens to the Sender's address on the target network (Arbitrum).

Orbiter Finance's Cross-Chain Mechanism

Orbiter provides a client for the Maker, or the Maker can deploy a client to automate this process, such as identifying the amount, currency, network status, etc., for the user's cross-chain transfer. This is the "correct" cross-chain process, meaning the user receives the crypto assets they are entitled to on the target network.

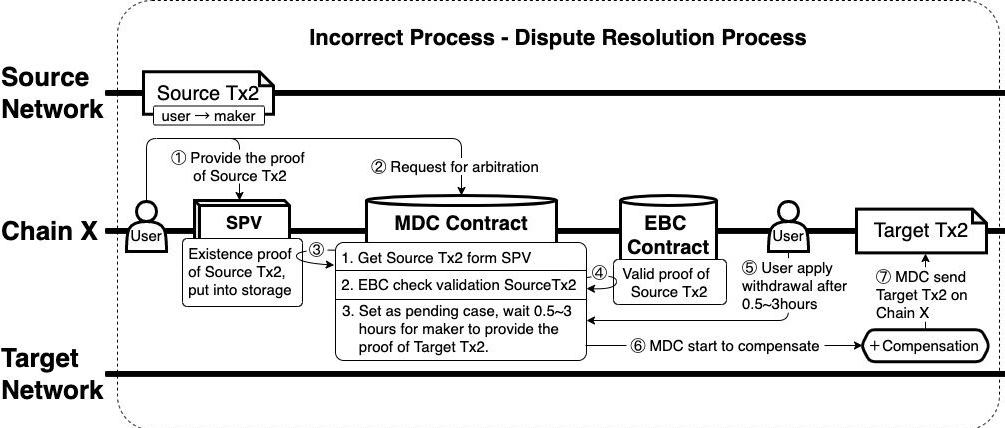

However, during this process, the Maker has the potential to act maliciously, possibly withholding the user's assets and not sending them on the target network. Therefore, Orbiter Finance employs a decentralized mechanism to prevent Maker malfeasance, ensuring cross-chain security, which is reflected in three types of smart contracts: MDC is the Maker deposit contract, holding the Maker's collateral for arbitration on behalf of the Sender. EBC is the event binding contract, used to establish collateral rules and some fee standards. SPV is the simple payment verification contract, used to prove the number of cross-chain transactions the user has on networks supported by Orbiter.

Additionally, to prevent Maker malfeasance, Orbiter Finance adopts an over-collateralization scheme. The Maker needs to provide two parts of funding: one for liquidity and the other as over-collateral. If the Maker acts dishonestly and the Sender does not receive the token on time on the target network, all losses incurred by the Sender will be covered by the over-collateral. Furthermore, the Sender will receive compensation, which also comes from the Maker's over-collateral.

Orbiter Finance's Arbitration Mechanism

All of this is achieved through Orbiter's arbitration mechanism. When the Sender believes there is a dispute with the transaction, they can apply for arbitration on the Orbiter platform. Once in the arbitration process, all subsequent steps will be executed by smart contracts, which is also why Orbiter is a decentralized cross-chain bridge.

4. ChainCatcher: It seems that the Maker mechanism is indeed innovative, and many community members are looking forward to experiencing Maker's functionality, as they can earn returns after providing liquidity. Can you disclose when Maker is expected to be opened?

Orbiter Finance: The team is currently refining the smart contracts, and we expect the Maker system to launch on the testnet by the end of October, followed by code audits before the official version goes live. The time taken for this process is uncertain.

5. ChainCatcher: Please discuss the current operational data of the Orbiter Finance protocol. Is the team satisfied with these achievements? What core data do you observe to evaluate business performance?

Orbiter Finance: In the DeFi world, people are accustomed to using Total Value Locked (TVL) to evaluate whether a protocol is of high quality. However, we believe that TVL may not be very applicable to cross-chain bridges. Our team internally focuses more on the number of transactions (tx) as a metric, while the cross-chain transaction volume is also quite important.

For cross-chain bridges, liquidity providers lock assets to earn returns. If they can use a small amount of assets to earn a larger return, it certainly aligns better with the expectations of liquidity providers. For example, if a user deposits the same amount of funds into different cross-chain bridge protocols, the protocol that generates more returns is more capital efficient. If a user locks a large amount of funds in a cross-chain bridge but cannot achieve the target return, then those funds are of no value to the cross-chain bridge and may even attract hacker attacks. Therefore, TVL is not an accurate metric for cross-chain bridges.

In contrast, the number of transactions (tx) can reflect the active user situation of the cross-chain bridge. Active users frequently use the protocol and generate returns for liquidity providers.

6. ChainCatcher: From a technical and operational perspective, what challenges is Orbiter Finance currently facing?

Orbiter Finance: First of all, there is security. Every cross-chain bridge protocol is committed to providing users with the safest cross-chain experience, which may be a long-term challenge. On the other hand, due to the evolution of the Ethereum ecosystem, such as the Ethereum merge and the development of Rollup technology, Orbiter also needs to keep pace with the times in terms of technology and solutions, maintaining its advanced nature. Especially in the development of Rollups, this technology is still in its infancy and has a lot of uncertainties. For example, StarkNet is not yet a mature blockchain and has many peculiarities, with its technology being updated and iterated daily. Therefore, Orbiter Finance also needs to adjust its solutions accordingly. Additionally, if Ethereum adopts account abstraction, we will need to reassess our solutions to ensure cross-chain security.

From an operational perspective, although there are not many cross-chain bridge protocols focusing on Layer 2 in the market, many traditional Layer 1 cross-chain bridge protocols are also starting to venture into this area. Currently, the cross-chain demand for Layer 2 itself is not very high. We need to consider how to expand our market share in the existing Layer 2 market while helping the Layer 2 ecosystem attract more users, thinking about how to facilitate Layer 1 users' transition to Layer 2. This is also something we are currently working on.

7. ChainCatcher: The vast majority of cross-chain bridges have their own tokens. Will Orbiter Finance issue a token? What kind of token economics scheme does the team lean towards?

Orbiter Finance: The native tokens of cross-chain bridges can indeed provide some use cases and additional functionalities. We may issue a token in the future, but we have not yet discussed specific plans, and there will be no native token launched in the short term.

Regarding token economics, since our team is relatively conservative, we prefer to reference the token schemes of mature DeFi protocols or other cross-chain bridges. In fact, we would rather focus our energy on refining the product.

8. ChainCatcher: What considerations led the team to launch Orbiter L2 Data? What can users with different identities do with this feature?

Orbiter Finance: We believe there is a need for products focused on Layer 2 data. Users need a place to discover new DApps and protocols to support their roles, and currently, there are not many data products targeting Layer 2 in the market, so there is some space for growth.

Moreover, measuring whether a protocol on Layer 2 is excellent may require some new data dimensions that could be more effective. It resembles traditional internet products, like DAU, which we don't discuss much in the DeFi world, but we believe it's very important on Layer 2. If we can bring these new dimensions to users, it will be a win-win situation.

9. ChainCatcher: DeFi is known as financial Legos, and composability is the most fundamental characteristic of DeFi. With the development of Layer 2, more and more DeFi projects are adopting Layer 2 solutions. How will the composability of DeFi change? How can protocols achieve interoperability if they adopt different Layer 2 solutions?

Orbiter Finance: The composability of DeFi will become more effective and interesting on Layer 2. TPS is the foundation of this Lego, and Ethereum 2.0 and Layer 2 can ensure this. However, the parallelism of multiple Rollups will indeed make interoperability between protocols more challenging, and Orbiter is very interested in solving this problem. In fact, cross-rollup bridges themselves are also an attempt to address interoperability, which is something Orbiter is already working on.

10. ChainCatcher: Orbiter Finance received donations from nearly 10,000 supporters during the Gitcoin Grants event, and the Orbiter Discord community is very active, with members engaging in meaningful discussions and proposals. Do you have any secrets in your operations?

Orbiter Finance: Haha, to be honest, we don't have any special tricks. Orbiter is a technology-driven team, with most members being engineers. Operations are actually our shortcoming. At this stage, we are product-centric, collecting and meeting more user needs. Especially for crypto users, Layer 2 cross-chain bridges are a necessity, and if we can make the product good, it will naturally attract more users. Our community and Twitter are our main promotional platforms. In short, our belief is to create a good product, meet user needs, and follow the development and trends of the ecosystem.

11. ChainCatcher: Can you talk about the story of Vitalik gifting ETH to the Orbiter team?

Orbiter Finance: Last December, Vitalik posted a bounty on Gitcoin for designing a cross-L2 bridge. We participated in this bounty and won, and Vitalik awarded us 16 ETH as a reward. We also had direct communication with Vitalik through this bounty, and he asked many questions about Orbiter. We are very grateful for his recognition of Orbiter, which is a great encouragement for us.

12. ChainCatcher: As the crypto market enters a bear market, many companies are starting to lay off employees and cut expenses. How does Orbiter Finance plan to respond to the bear market? Will the bear market affect users' cross-chain demand and thus impact business development?

Orbiter Finance: The bear market does have an impact on all crypto protocols, such as a decline in business volume for cross-chain bridges. However, for the Orbiter team, there hasn't been much impact, and all product plans are progressing as scheduled.

Additionally, Orbiter's revenue is sufficient to cover all team expenses, so there will be no layoffs. We will continue to develop according to our product roadmap. There may be adjustments due to changes in Layer 2 and Ethereum, but the reasons for adjustments will never be the bear market; rather, they will be to choose better technical solutions or meet user needs.

13. ChainCatcher: In the first quarter of 2022 alone, cross-chain bridges suffered losses exceeding $1 billion due to hacker attacks, making cross-chain bridges seem like a cash cow for hackers. Why are cross-chain bridges so vulnerable? What special considerations do you have regarding security?

Orbiter Finance: Most of the reasons for attacks on cross-chain bridges stem from hackers noticing that large amounts of user assets are locked in cross-chain bridge contracts. They then attack by creating fake signatures or false redemption vouchers. However, the Orbiter protocol does not involve locking assets or performing minting or mapping operations; the cross-chain process is essentially a transfer between two addresses on the same network. On the other hand, since Orbiter Finance focuses on Layer 2, it also benefits from the security of Rollups.

14. ChainCatcher: At this stage, more and more cross-chain protocols are not limited to providing asset cross-chain services but are also beginning to explore cross-chain messaging functions. What are Orbiter Finance's views and plans regarding the expansion of cross-chain functionalities?

Orbiter Finance: Messaging is indeed a direction that cross-chain bridges will expand into, and Orbiter will consider it, but it mainly depends on market demand and the development of Ethereum. We are still conducting internal discussions, such as the messaging functionality between multiple Layer 2 networks.

15. ChainCatcher: According to data from L2beat, the total locked value in Layer 2 has increased more than fourfold this year, and Layer 2 projects are experiencing an explosion. To what extent do you think Layer 2 will capture the Ethereum market in the future?

Orbiter Finance: This is certain. After the Ethereum merge, its positioning and ecological structure will change. I tend to compare the current Ethereum to a large city where residents live in Layer 1. As more residents move in, everyone feels resource scarcity and poor experiences. Residents can perform some basic operations on Layer 2, while Layer 1 retains only important structural data (such as data storage, verification, etc.). Layer 1 becomes like the foundation supporting the entire super city, while daily affairs are handled on Layer 2. In my view, this is something that will inevitably happen in the future.

Risk warning

Risk warning Risk warning

Risk warning