Arthur Hayes: How CBDC Becomes "Pure Evil"?

For the general public, CBDC will launch a comprehensive attack on the right to honest transactions between individuals. For the government, it is the best tool to change people's behavior, as we voluntarily upload our lives to social media platforms like Instagram and TikTok. For banks, CBCD will continue to threaten their existence.

For the general public, CBDC will launch a comprehensive attack on the right to honest transactions between individuals. For the government, it is the best tool to change people's behavior, as we voluntarily upload our lives to social media platforms like Instagram and TikTok. For banks, CBCD will continue to threaten their existence.Original Title: “Pure Evil”

Author: Arthur Hayes

Compiled by: Guo Qianwen, ChainCatcher

Any opinions expressed herein are solely those of the author and do not constitute any investment advice.

Perhaps everything is relative except for the speed of light. Therefore, when I call central bank digital currency (CBDC) "pure evil," the next logical question should be------from whose perspective?

What is evil for some may be a pure good for others.

The three participants in this tragedy are:

- "We (the public)," or those who are governed.

- The government and the political elites manipulating behind the scenes.

- Commercial banks chartered by specific national governments.

For us ordinary people, CBDC will launch a full-scale attack on the right to honest transactions between individuals. For the government, it is the best tool to change people's behavior, as we willingly upload our lives to social media platforms like Instagram and TikTok. For banks, CBDC will continue to threaten their existence.

The indifference of the masses will give the government an opportunity to easily exchange our physical cash for CBDC, and the utopia (or dystopia) of financial regulation is on the horizon. But we have an ally, perhaps not a realistic one, that can hinder the government from implementing the most effective CBDC framework to control the ordinary people------this ally is domestic commercial banks.

Satoshi Nakamoto "brought" blockchain. While his purity and goodness shine like sunlight, his teachings on blockchain may be distorted by some ill-intentioned individuals. This is a very important issue because the inflation of the future will be radically different from the inflation we have become accustomed to over the past 50 years------this crisis will require the government to adopt a similarly novel, blockchain-driven mechanism, namely CBDC, to counter it. I believe CBDC will enable the government to effectively address this new inflation but will bring numerous losses to the people.

Let us pray.

This inflation is not the same as past inflation

Since the early 1970s, when exchange rates began to float, participants in the world's largest economies have largely experienced financial inflation. At that time, people's fiat currencies plummeted, but the cost of living did not rise too much (at least to a large extent).

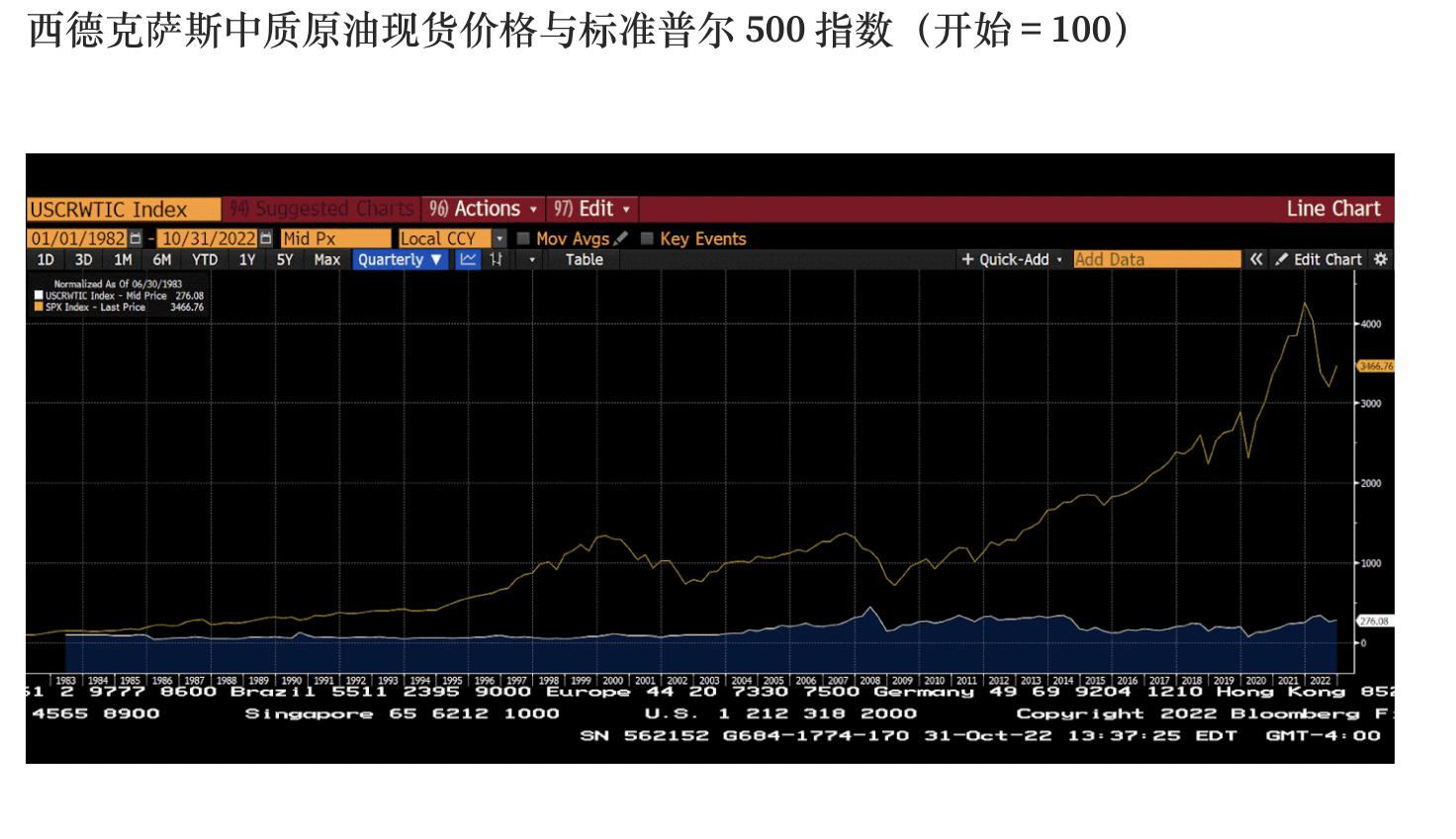

Since 1983, oil prices have risen nearly 180%, with a CAGR (compound annual growth rate) of 2.75%. Since 1983, the S&P 500 index has increased nearly 35 times, with a CAGR of 8.44%. Energy is the primary currency. From this perspective, the Federal Reserve's average inflation target is only 0.75% higher than the 2.00% target. During the same period, the Federal Reserve's balance sheet increased from nearly zero to nearly $9 trillion.

Since 1983, oil prices have risen nearly 180%, with a CAGR (compound annual growth rate) of 2.75%. Since 1983, the S&P 500 index has increased nearly 35 times, with a CAGR of 8.44%. Energy is the primary currency. From this perspective, the Federal Reserve's average inflation target is only 0.75% higher than the 2.00% target. During the same period, the Federal Reserve's balance sheet increased from nearly zero to nearly $9 trillion.

Crazy money printing benefits financial asset prices, which in turn significantly drives global income inequality------but this inflation does not undermine government stability. This inflation has caused a condo across from Central Park on 57th Street to skyrocket to hundreds of millions of dollars; this inflation allows you to earn $25 in any café in an international financial center.

But what we face today is a more terrifying inflation: food and fuel inflation. No one is spared except for the wealthiest------everyone will be forced to become displaced, and its iron grip is tightening around all developed and developing countries. The common people do not care what kind of economic "ism" their government should implement. They are starving and freezing, and if those in power cannot solve the problem immediately, a coup should be launched to oust the authorities.

Thus, the government is in a dilemma. They must print money and distribute it to those who are suffering. But at the same time, the government must ensure that capital does not run out of control. Throughout human history, the world has never endured such low interest rates and such high debt. Overall, savings and capital will suffer significant losses because debt needs to be eliminated through inflation. Under the traditional financial monetary system, its two goals do not conflict------not printing money will cause suffering, but printing money will destroy capital through inflation------the government will need to rely on some technological innovation to achieve these two goals and maintain power.

I believe the innovative answer will be CBDC.

CBDC is the answer!

Open your wallet and take out your cash. Reach into your pocket or purse and pick up your phone. Now, try to stuff your cash into your phone.

If this were a scene from a sci-fi movie, you might succeed------but you have already realized that this physics does not hold in the real world.

CBDC is a digital currency issued by the government (i.e., digital cash) that exists purely in electronic form, making you unable to see the above situation. It is base money, just like physical cash------it is a liability of the central bank. This is different from the electronic money you are familiar with, which operates through traditional commercial banks. These currencies------created by the banking system through loans------are composed of credit money, not direct liabilities of the central bank (a cold hard cash).

Another significant difference between CBDC and current electronic cash is that blockchain technology provides innovation, allowing the government to program CBDC, keeping them 100% in control. This additional control enables them to address the inflation problem that is troubled by dual issues.

In this CBDC dystopia, people will no longer take to the streets to protest high food and fuel prices but will directly receive electronic currency, making staple prices more affordable. Apart from government bonds with yields below inflation rates, those with capital may be prohibited from making any other investments------these restrictions are implemented through the coding of the currency itself, not just by law. All of this can be accomplished through programming, with almost no errors (if any).

This is not pure evil in itself. From the perspective of savers, this is certainly not a good thing, and it is not much different from a forcibly implemented pension plan, where you need to hold a certain amount of government debt below the inflation yield as an "appropriate" investment for retirees. However, CBDC makes these policies easier to enforce than legislative regulation------because their rules are actually coded into the currency------preventing citizens from using their hard-earned money to buy gold, other high-yield foreign government bonds, or Bitcoin.

But what truly makes CBDC potentially hellish is------when the government can push a technology to its limits for their own profit, they will never stop and limit themselves to the initial use case. Instead, they will push forward with all their might. When CBDC is used to its limits, it will be used by the government to directly control who can trade and for what purpose.

Imagine you are the "other." The other in any society are those who are economically exploited due to their race, immigration status, religious beliefs, and/or accent. Most people recognize this ongoing exploitation because they are led to believe that some people are inferior due to certain qualities.

Now imagine you and others decide to change your situation through non-violent means. You march, shout protests, and engage in non-violent civil disobedience activities. You use social media platforms like Facebook, Twitter, and Weibo to organize and influence people to take action. The momentum of the movement grows, and you decide it is time to march in the capital to show the country how unjust its discriminatory policies are.

Before the big march, the movement effectively generates and disseminates heartbreaking and thought-provoking photos of small protest sites across the country, which keeps the movement in the spotlight. The government begins to feel nervous. The police try to counter by using tried-and-true strategies, such as spraying you and your peaceful protest partners with water or attacking you with dogs. As history warns us, the government will not sit idly by.

The police have a new tool------CBDC. Instead of taking public action against the protesters to prevent the upcoming capital march, they ask Facebook, Twitter, Weibo, and other platforms to use their algorithms to identify the data of everyone participating in or sympathizing with the movement. In the days leading up to the march, these individuals are completely frozen out of the financial system.

In the CBDC era, all economic activities between citizens use digital currency, and past currencies (such as physical cash) are no longer accepted or even exist. Therefore, protesters and their supporters cannot fill their cars with gas, cannot buy bus, train, or plane tickets, cannot dine in restaurants, cannot purchase food and water in grocery stores, and ultimately cannot effectively organize------thus the capital march never happens. If you are starving or cannot go to the march from the start, then the march cannot happen.

Under this monetary system, social progress becomes difficult to achieve because the government can completely restrict citizens from engaging in honest business, and citizens cannot effectively organize against the government. If you believe hell exists to some extent, this is a depiction of hell on earth. Society will no longer progress. Using this evil tool, human society will lose its vitality.

Alliance

When it comes to CBDC, the common people and the entities in power are also their potential allies (though unlikely)------domestic commercial banks, which share a common enemy.

The power and profitability of banks directly stem from the privileges granted by the government, allowing them to legally print money through loans. Banks also benefit from the legal system that enforces financial contracts. Therefore, when debtors cannot repay their debts and face violent sanctions from the state, banks have the right to reclaim their collateral. Bankers want to profit, while the government wants power. Power and profit often go hand in hand (though not always), often accompanied by controversy.

The reckless lending of banks always puts the government in a political dilemma. But historically, governments have had no choice but to tolerate their reckless behavior because, before the invention of CBDC, they relied on banks to keep the financial system functioning. In particular, banks are better equipped than the government to assess credit risk because they place profit above politics. Bad credit is bad credit, regardless of which party the debtor belongs to.

Due to their importance to the entire financial system, even when banks mess up and trigger a financial crisis, the government always has to intervene, print money, and save the banking system without being able to impose any actual sanctions for the damage caused by the banks.

But now, the government has a tool that can completely take over the most important functions of commercial banks------namely, accepting, storing, and lending citizens' deposits. All of this can be accomplished with a fraction of the cost and manpower of the commercial banking industry.

The government and its bank, the central bank, have the following options for implementing CBDC. They can execute one of the following:

- Create a network with commercial banks as nodes. End users have an account at the bank, and nodes can move data (i.e., money) across the network. I call this the wholesale model. The central bank supports commercial banks, so there will never be a digital bank run.

- Create a network with only one node, namely the central bank. Each citizen has an account directly at the central bank. I call this the direct model.

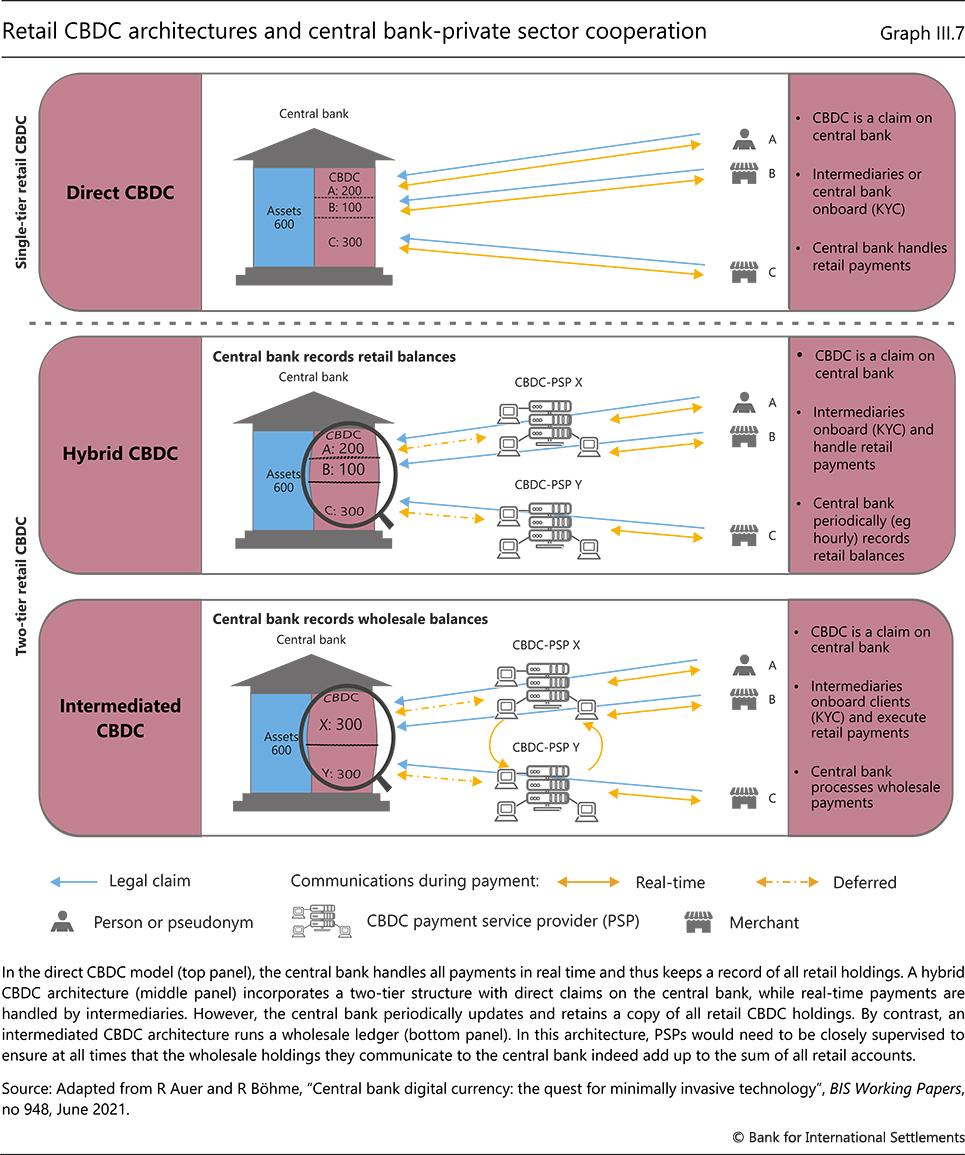

The Bank for International Settlements (BIS) created this beautiful infographic categorizing various types of CBDC:

The wholesale model I described is a fusion of the mixed and intermediary CBDC listed in this chart.

Wholesale Model

JPMorgan Chase (JPM) and the Bank of China (BOC) are the two largest commercial banks in the world. They are both able to clear dollars at the Federal Reserve. Let’s imagine that the Federal Reserve launches its own CBDC, which we will call FedCoin (FED). There are only two FED nodes, operated by JPM and BOC.

As an American citizen (also including citizens of other countries for simplicity), you either download the JPM app or the BOC app. Whichever app you choose, you have a digital wallet to store FED. The internal database in the JPM ecosystem transfers FED between the two JPM accounts. Transferring FED between a JPM account and a Bank of China account requires agreement on the transaction between JPM and BOC. It works like the Bitcoin network, except it is private, and only JPM and BOC can validate transactions.

JPM and BOC compete for FED deposits by offering attractive deposit rates. Then, JPM and BOC fund long-term loans to federal government enterprises in the form of FED using their short-term deposits.

The Federal Reserve is not a profit-making entity, so it does not charge JPM or BOC for operating the nodes. However, the Federal Reserve may occasionally require them to detail who did what on the network, and the banks must comply and provide the requested data. The Federal Reserve may also instruct banks to issue loans to certain demographics at attractive rates and/or send federal government officials to JPM and BOC to instruct them to issue loans to certain customers.

Although JPM and BOC are subject to the Federal Reserve, they are only one step away from escaping government control. This means they have their own priorities, namely profit, and they may not execute the Federal Reserve's orders in a timely manner, prioritizing profitability. In this model, the government's control over the money supply will inevitably be greater than that of an economy with physical cash------but given that the government relies on private organizations to implement policies, the aforementioned policies may not be strictly enforced.

This model does not significantly improve the FedWire dollar clearing system. The banking system is still operated by private banks, which prioritize profit. They may be outraged by policies that affect their profitability. The only major change is that cash is prohibited, and all transactions will be conducted digitally.

The horror story I outlined in the previous section about the government completely controlling citizens' transactions is still possible in this case, but it requires more manpower to achieve. The more people involved, the greater the risk of process execution failure.

Banks clearly prefer this model. As gatekeepers of the financial system, they can still charge fees they deem appropriate and eliminate a key competitor------physical cash.

Direct Model

The Federal Reserve develops its own app that every citizen can download. This app is the only means to store and transfer FED. Commercial banks can still obtain licenses to receive deposits and make loans, but they compete directly with the Federal Reserve. Given that the Federal Reserve only cares about politics, it can set policies that, if banks follow suit, will bankrupt those banks. Specifically, the Federal Reserve can pay the highest deposit rates and offer the lowest loan rates because it is willing to bear the spread as long as it can gain political benefits. The Federal Reserve can do this because it will never go bankrupt, as it is the government. This makes it the safest place for citizens to store federal deposits.

Commercial banks will soon lose their entire deposit base unless they are willing to oppose the Federal Reserve. Here’s an example: imagine the Federal Reserve becomes a social justice warrior, trying to correct the historical advantages its citizens have gained------wealth accumulated due to slavery and other discriminatory practices. Under the new policy, people of color in the U.S. can deposit their money in banks and earn 10% interest, while borrowing at 0% to start businesses. White Americans can deposit money and earn -1% interest while borrowing at 20% to start businesses.

Banks can offer higher savings rates and lower commercial loan rates to white Americans to counter this policy. But they may encounter some problems because there are anti-discrimination laws applicable to federally chartered banks. This puts banks in a dilemma. If the government wants to deprive a certain group of rights, banks can offer them better terms, which would be a profitable business opportunity. But compliance departments say no------this profitable business slips away. While this example is simplistic, it illustrates why commercial banks cannot successfully confront the government in the direct model. The government can and will set rules that banks must follow, but the government is not subject to such restrictions.

Real World

Here is a brief summary of the measures that the five major central banks have already implemented or plan to implement regarding CBDC.

- People's Bank of China (PBOC)------They launched the electronic CNY using the wholesale model.

- Federal Reserve------The Boston Federal Reserve Bank is collaborating with MIT to study the issue. They have not yet decided whether to use the wholesale or direct model.

- European Central Bank (ECB)------They have decided to implement the wholesale model but continue to study the issue.

- Bank of England (BoE)------They are studying the issue and have not fully decided whether to issue CBDC------but if they decide to issue it, they have indicated they will implement the wholesale model.

- Bank of Japan (BoJ)------They are still studying the issue but have already decided to implement CBDC using the wholesale model.

Every country that has at least started "choosing a CBDC model" has chosen the wholesale model, so it is clear that no central bank wants its domestic commercial banks to go bankrupt. Even in China, the largest banks are directly owned by the government. You can see how much political power banks have within the government. For politicians who care more about power than profit, this is their opportunity to completely destroy the "too big to fail" banks------however, they still seem unable to do so politically.

Some Degree of Bankruptcy

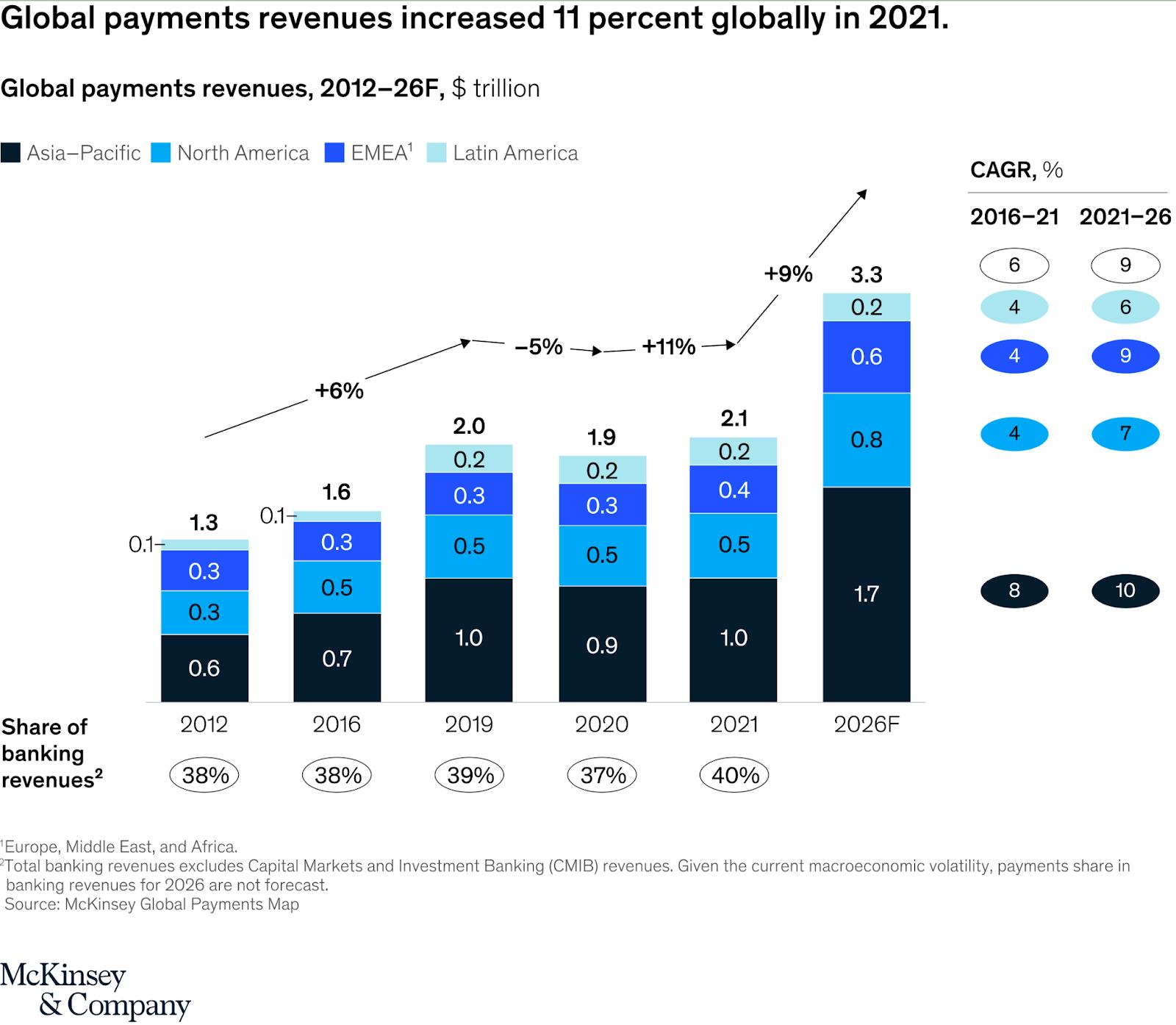

If CBDC is introduced using the direct model, how much business would global commercial banks lose? McKinsey released a detailed chart on the percentage of bank revenue derived from payments.

McKinsey 2022 Global Payments Report

We can assume that if the government directly issues currency to the people, the global payments industry would no longer be needed. As of 2021, the industry's revenue was valued at $2.1 trillion, accounting for 40% of total bank revenue.

Thus, the $2.1 trillion in revenue depends on which model is chosen for CBDC------this is why it is assumed that if CBDC becomes a reality, the banking sector will do everything possible to continue participating in the payment process.

Competition

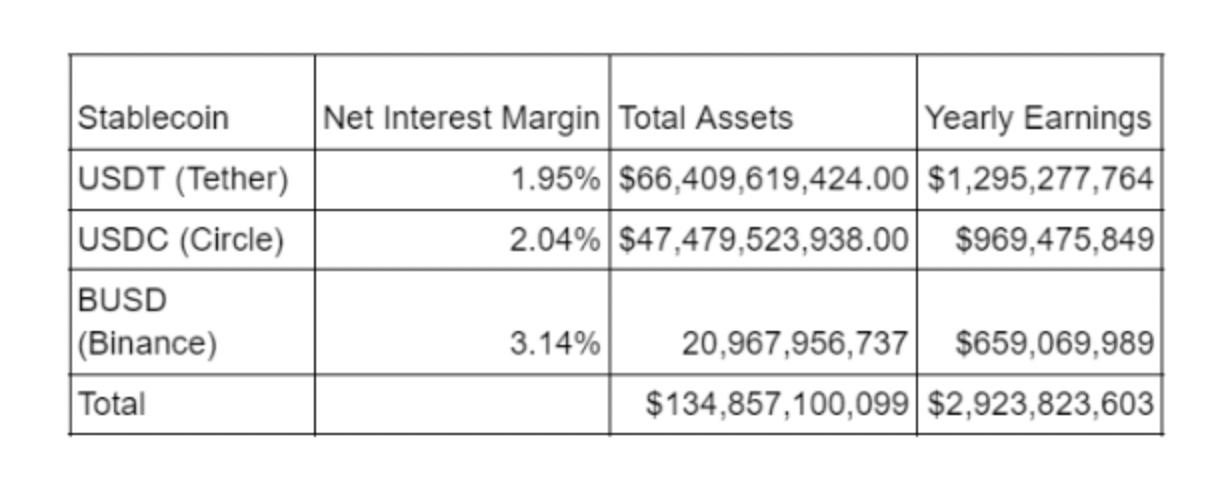

Whenever mainstream financial media collectively expresses fears and anxieties about stablecoins, discussions about CBDC heat up. The most widely issued stablecoins are those tokens pegged 1:1 to the dollar within the banking system.

For every $1 token issued, stablecoin issuers typically hold a combination of cash, short-term government bonds, and short-term corporate bonds. Here are the latest public disclosures for the three largest stablecoins, along with my estimates of each stablecoin's net interest margin (NIM) and annual revenue:

This is indeed a significant amount of revenue. But what about costs?

The advantage of managing these stable bonds is that their costs are a small fraction of the cost of running a bank.

A bank has thousands of branches, with employees demanding salaries and benefits. Stablecoins have no branches and only a few employees doing back-office work, with transactions occurring on public blockchains like Ethereum.

Banks must spend billions to build, secure, and maintain physical infrastructure to safeguard various forms of currency, such as cash, coins, and precious metals. Stablecoins do not incur any security costs. In fact, users pay transaction fees to the network every time they want to send value to cover security costs. For example, on the Ethereum network, a fee is charged every time a transaction is sent on the network.

Banks pay billions to legal and compliance professionals to adhere to regulations. Stablecoins must also pay these individuals, but they need to accept fiat currency from trusted counterparties to purchase fixed-income securities. I believe the total annual expenditure on legal and compliance for the three issuers mentioned above will not exceed $100 million.

Like banks, stablecoin issuers prefer rising interest rates. They do not pay any fees to token holders, so every time JayPow raises short-term rates, they have more cash in their pockets. This week, JayPow raised short-term rates again by 0.75%------which means if their NIM grows proportionately, revenue will increase by $1 billion.

Now you understand why banks hate these monsters, right? Stablecoins perform better in banking than banks do because their profit margins are nearly 100%. Whenever you read anxiety-laden articles about stablecoins, just remember: banks are just jealous.

Additionally, remember that it is those "too big to fail" banks and financial intermediaries (TradFi) that run full-page ads in the Wall Street Journal, Financial Times, and Bloomberg. I haven't seen many ads for USDT, USDC, or BUSD in those publications. TradFi players pay for the existence of these publications, and it is evident that reporting on direct competitors often carries a negative bias.

The reason stablecoins exist and are popular is that there is no competing CBDC. If the Federal Reserve launches FED, there will be no reason to use these solutions because FED will have government backing and will never go bankrupt.

To understand how I estimated the annual revenue of these stablecoin issuers, see this table. Due to inconsistent and incomplete disclosures of the assets held by issuers, I had to make some assumptions. For example, I do not know when certain securities were acquired, nor do I know what certain assets actually are, as they are described in very generic terms. I appreciate Circle and Binance for providing CUSIP for most of the assets they hold. This level of transparency should be emulated by everyone, preventing banks from using mainstream financial media as a mouthpiece for complaints.

Super Antidote

I am pessimistic because I believe that CBDC using the wholesale model will be launched in all major economies. Because they have no way out, they cannot escape the inflation dilemma without using such tools to placate the masses and financially suppress the aristocracy.

I am equally pessimistic that people are busy scrolling through videos, with no time to think about why their physical cash is disappearing and why their financial sovereignty is being openly stripped away.

On the other hand, I am optimistic because at least the most commonly used CBDC model will be the wholesale model, and the most negative aspects of this technology may be offset by profit-driven, too-big-to-fail commercial banks, which often clash with power-hungry politicians.

What also makes me optimistic is that we still have the ability to buy the ultimate antidote: Bitcoin. This opportunity will not last forever. Capital controls are coming, and when all funds are digitized and certain transactions are not allowed, the ability to purchase Bitcoin will soon disappear. If this description of doom resonates with you, and your liquid net worth gains do not come from Bitcoin, then the best day to buy Bitcoin was yesterday.

China's digital currency CNY, supported and primarily operated by the PBoC, is the most widely used CBDC in the world. According to central bank data, "As of August 31, transactions using the digital yuan exceeded 1 trillion yuan (approximately $140 billion), up from about 880 billion yuan in 2021. More than 5.6 million merchants can now accept payments. The People's Bank of China stated that users completed 360 million transactions across 15 pilot areas covering 23 cities. These numbers provide the best comparison to the statistics listed at the end of 2021.

A report from the Atlantic Council noted that since October 2021, the PBoC has not released official data on the adoption and use of electronic CNY. However, earlier this year, some PBoC officials indicated that there are currently 261 million wallets, with a total transaction volume exceeding 87 billion yuan (approximately $13.75 billion).

According to more comprehensive data from October 2021, there are currently 123 million personal wallets and 9.2 million corporate wallets, with a transaction volume of 142 million and a transaction value of 56 billion yuan (approximately $8.8 billion). This means the average balance of personal wallets is 3 yuan (approximately $0.47), and the average balance of corporate wallets is 31 yuan (approximately $4.90). The relatively high number of wallets indicates that many wallets have been opened but are not used for transactions or holding electronic CNY balances.

In China, the private sector is responsible for guiding customers, implementing AML/CFT regulations and due diligence, and conducting retail payments in real-time, with the central bank acting as their backstop.

Digital CNY competes directly with mobile/online payment services like Alipay (Ant Group) and WeChat Pay (Tencent).

Ant Group's data from 2020 showed that its monthly payment volume averaged 10 trillion yuan, and as of June 2020, they had 711 million monthly active users (MAU).

Tencent disclosed in its 2022 interim report that WeChat has 1.3 billion MAU. It did not disclose the total amount of WeChat Pay.

Hamilton Plan in the U.S.

The Boston Federal Reserve Bank and MIT's Digital Currency Initiative (DCI) are collaborating on exploratory research called the Hamilton Project, a multi-year research project aimed at exploring the design space of CBDC and gaining in-depth insights into the technical challenges and opportunities of CBDC. Although the project has not yet released any tests, it boasts impressive statistics, such as TPS exceeding 100,000.

As of the first phase, the project has not decided how to handle intermediaries (i.e., which BIS classification it will target).

"The Bank for International Settlements (BIS) simplifies the choice of intermediaries into three possibilities------the 'direct' model, where the central bank directly issues CBDC to users; the 'two-tier' model, where the central bank issues CBDC to intermediaries, who then manage relationships with users; and a mixed model of both. We do not directly study the role of intermediaries in Phase 1. " ------ Hamilton Project White Paper

European Central Bank (ECB)

Many details regarding the ECB's CBDC are still being formulated. The ECB has stated that they are interested in using supervised intermediaries but have not specified what role these agents will play. Current guidelines are:

- The digital euro should primarily serve as a means of payment rather than becoming a financial investment tool;

- Regulated intermediaries should be involved in the processing of the digital euro.

After completing experimental work with the European Central Bank and the central banks of eurozone countries, the ECB launched the investigation phase of the digital euro project in July 2021. This phase aims to determine the best design for the digital euro and ensure it meets user needs. During this phase, the ECB will also analyze how financial intermediaries can provide front-end services based on the digital euro, with completion expected around October 2023.

Bank of England (BoE)

In the words of the BoE, "We are carefully examining how a central bank digital currency (CBDC) might work in the UK. But we have not yet decided to launch this program." While they have published some discussions and documents regarding potential commercial impacts and technical choices, they have not specified how the central bank will collaborate with the private sector, aside from prioritizing private intermediaries.

The BoE proposed CBDC in 2020 and sought public opinion. The document outlines a descriptive "platform" model for CBDC, in which banks will provide the core technological infrastructure and minimum necessary functions for CBDC payments. This platform allows private sector payment interface providers (PIPs) to connect, providing customer-facing CBDC payment services and any additional value-added services, as part of a competitive and diverse payment landscape.

Public opinion overwhelmingly suggests that banks should provide the minimum level of infrastructure for the system to be reliable, flexible, fast, and efficient. However, the private sector should play a leading role in addressing end-user needs, including providing innovative "overlay" services using the core CBDC infrastructure through competition. The BoE will continue to refine and develop the "platform model" concept in its exploration of CBDC. Interoperability between CBDC and other forms of currency (including innovations like stablecoins)------the ability for users to convert with minimal time or monetary cost------may be a fundamental requirement.

Bank of Japan's Digital Currency

While the Bank of Japan currently has no plans to issue CBDC, it is exploring various design possibilities for eventual implementation.

As the first phase of the Bank of Japan's CBDC research, the bank entered the "Proof of Concept Phase 1" from April 2021 to March 2022. The bank established a publicly available CBDC around a ledger system. The Bank of Japan simultaneously experimented with three designs, collecting data on TPS, latency, and other KPIs. However, as the bank enters the second phase, they have not indicated which design they will implement (if any).

Risk warning

Risk warning Risk warning

Risk warning