Messari: DEX Market Saturation, How Does Uniswap Achieve Alternative Growth?

Whether to enable the Fee Switch is a major debate in the development of Uniswap.

Whether to enable the Fee Switch is a major debate in the development of Uniswap.Original source: “Expanding Uniswap's Addressable Market”, Ashu Pareek, Kentrell Key

Compiled by: Wendy

Key Insights

To maintain its current growth momentum, Uniswap must find ways to expand its total addressable market.

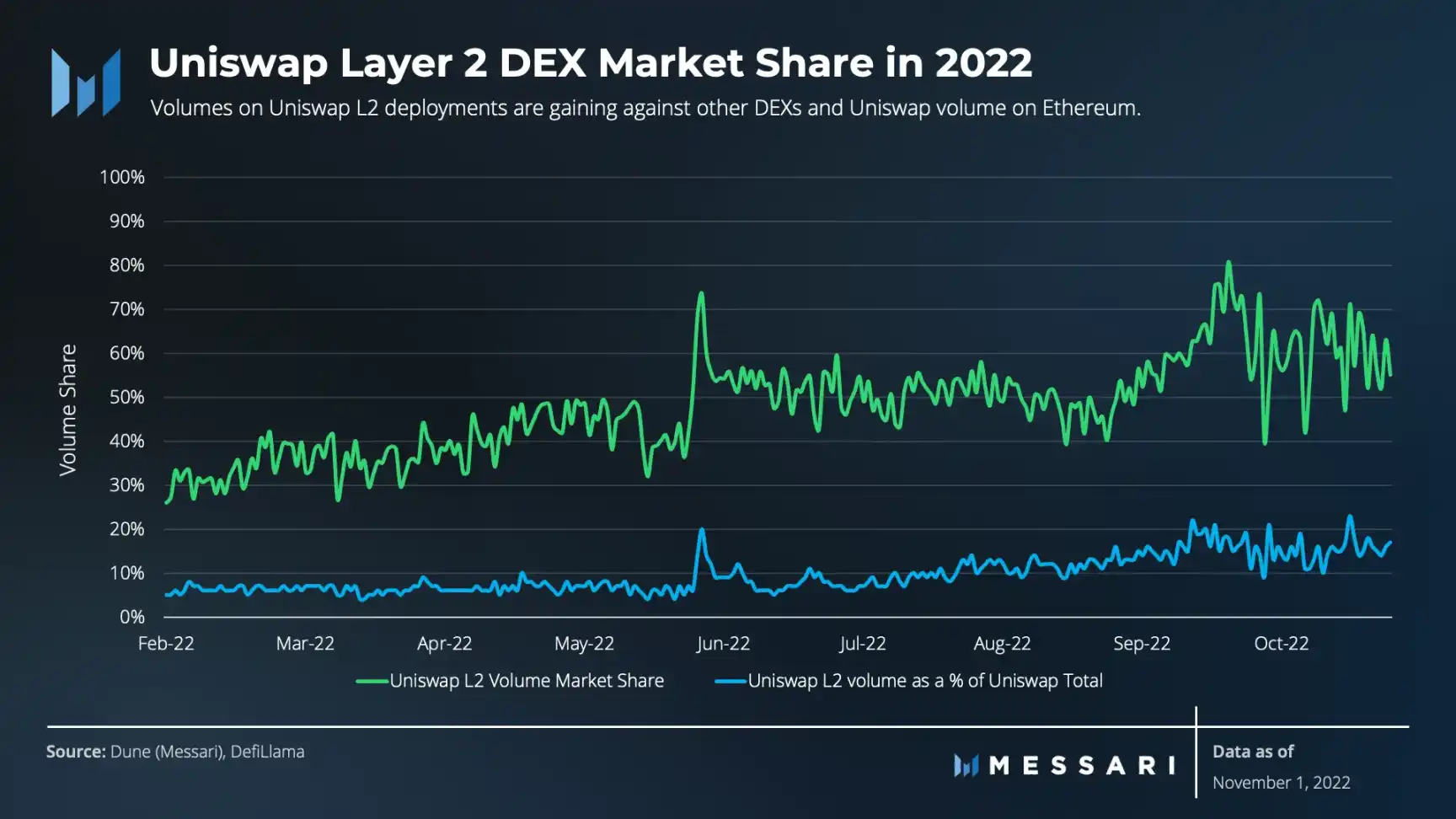

Uniswap has successfully deployed on Layer 2 (L2) scaling solutions, capturing 65% of the trading volume of L2 DEXs (decentralized exchanges) in Q3 2022.

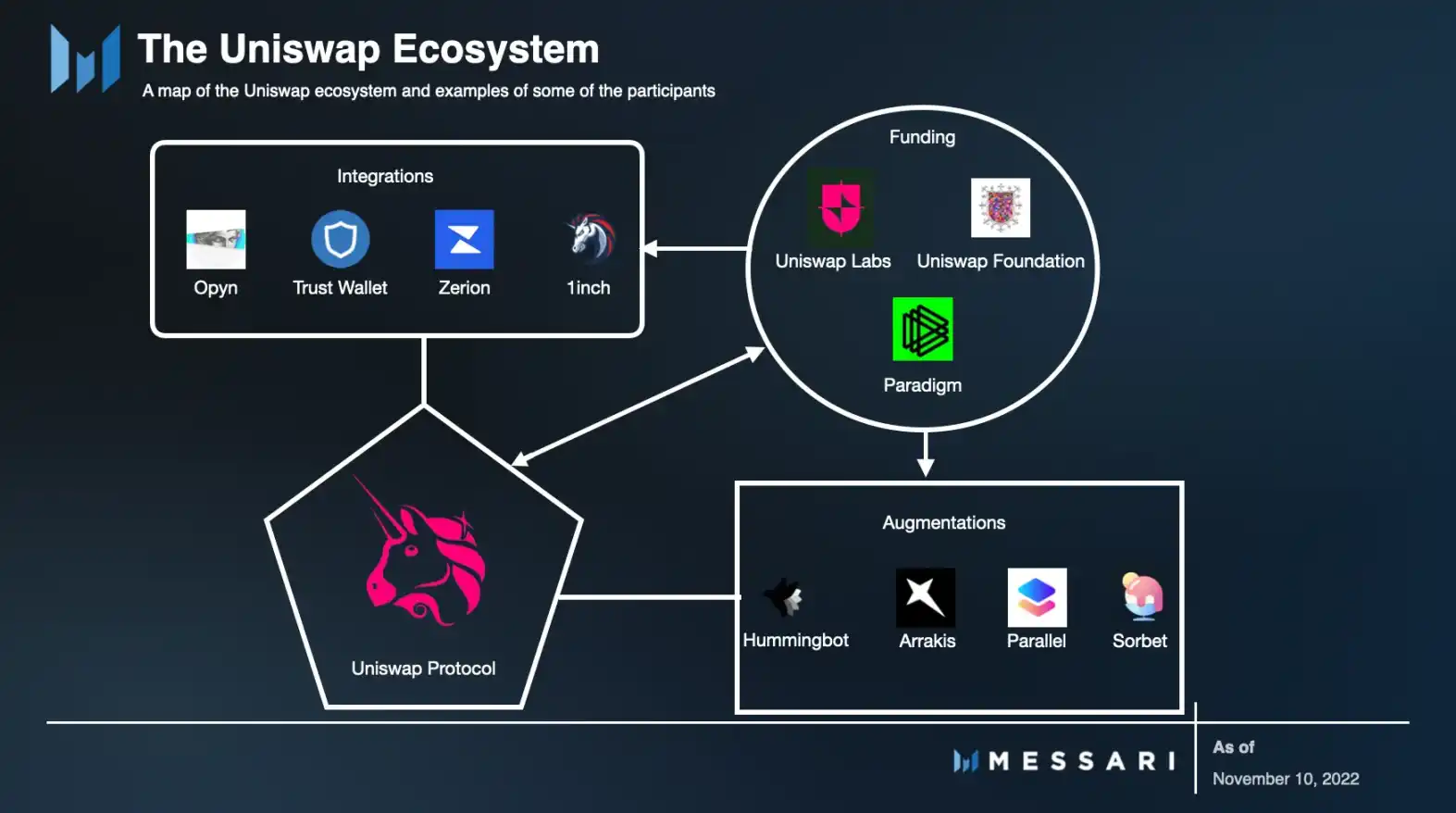

Several projects have utilized Uniswap's software development kit, integrating the Uniswap protocol or enhancing its functionalities.

The question of whether to activate the Fee Switch is a major debate in Uniswap's development. The concern is whether the new funding pool for growth investments will offset the weaker competitive position with liquidity providers.

Uniswap has found a product-market fit. The launch of Uniswap V3 addressed the most apparent flaw of automated market makers—capital inefficiency. On the other hand, Uniswap has successfully saturated its current addressable market: it is the largest DEX, with a cumulative trading volume of $1.3 trillion, accounting for over 70% of Ethereum DEX trading volume.

The dilemma is that this dominance arose precisely because Uniswap successfully capitalized on readily available opportunities. This means that continuing to optimize the DEX and squeezing growth from the existing market will not be sufficient to maintain its current trajectory.

However, Uniswap has consistently adhered to its spirit of innovation and accessibility, and has begun to pull the most challenging growth lever: expanding its addressable market. In other words, it aims to attract a broader audience. In the past, Uniswap has used relatively straightforward methods to expand its market, such as L2 deployment. At the same time, it has adopted more complex strategies, such as developing a robust ecosystem around funding, supplementary projects, and integration. As the core of cryptocurrency value flow, initiatives like NFT integration and the Fee Switch will have widespread implications for the entire industry.

Multi-Chain

Uniswap Labs launched its flagship product V1 AMM on the Ethereum mainnet in November 2018, followed by V2 in 2020. The launch of V3 in 2021 addressed capital efficiency issues and marked the protocol's expansion into a multi-chain future.

In addition to the Ethereum mainnet, Uniswap V3 has since been deployed on EVM-based scaling solutions Optimism, Arbitrum, Polygon, and Celo. These deployments quickly attracted liquidity and trading volume from other DEXs. The liquidity provided by these deployments reached $246 million, and in Q3 2022, over 65% of DEX trading volume on these chains was conducted through Uniswap. The L2 trading volume deployed by Uniswap has accounted for nearly 20% of the protocol's total trading volume.

As more EVM scaling solutions are developed, Uniswap may be deployed on more chains. In October, a proposal to deploy Uniswap V3 on zkSync 2.0 was executed, expected to go live in Q4. Additionally, in a Snapshot "Temperature Check," token holders expressed support for deploying V3 on Aurora. If the proposal passes, Aurora plans to incentivize Uniswap users, with $5 million allocated for liquidity mining activities and long-term protocol development.

The deployment costs for multi-chain and Ethereum L2 are low. In fact, there are often on-chain incentives that distribute their native tokens to Uniswap users. Moreover, the gas fees on these chains are lower than those on Ethereum, effectively lowering the entry barrier for retail investors and expanding Uniswap's user base. Given Uniswap's strong reputation and deep liquidity, newer chains tend to implement incentive strategies, hoping that users and their liquidity can be sustained over the long term.

Funding

Uniswap Labs recently raised $165 million in Series B funding led by Polychain Capital. This funding will be used to expand the development of Uniswap's product line to cover more users.

In addition to the capital injection, Uniswap's vision is supported by a large community treasury, which, as of the time of writing, holds UNI worth over $1.7 billion. Token holders are responsible for deciding how to use these funds, funding internal organizations such as the Uniswap Grants Program (UGP) and the recently established Uniswap Foundation (UF).

Since its inception, UF has absorbed and expanded UGP, which will allocate $60 million in UNI over the next three years. In the nearly two years since the launch of UGP, approximately $9 million in grants have been awarded to a range of ecosystem proposals. These grants aim to strengthen the Uniswap ecosystem and will lead to an increase in projects built on Uniswap.

In addition to donating funds, UF has also supported several community-led projects—most notably, the ongoing liquidity mining (LM) project on Optimism. UF did not directly initiate a liquidity mining program but deployed $800,000 in OP obtained from the Optimism airdrop through community partners, including Arrakis Finance, xToken Terminal, and Gamma Strategies.

These projects provide active liquidity management services for Uniswap V3 pools, thereby supporting the effective allocation of incentives to users providing "in-the-money" liquidity, resulting in deeper pools. Meanwhile, some users are familiar with the process of swapping tokens but may not provide liquidity due to misunderstandings about the flexible mechanisms of Uniswap V3 or the need for active management to maximize returns. When new and existing projects distribute through these initiatives, they will be introduced to LP tools, alleviating their concerns.

Supplementary Projects / Ecosystem

Traders and liquidity providers are two distinct user groups, and there is also a third often-overlooked group: developers. Since Uniswap is open-source, all builders can leverage the Uniswap software development kit (SDK) to apply their ingenuity to Uniswap. In practice, this means projects can integrate Uniswap or enhance existing platforms.

By allowing other projects to integrate its DEX, Uniswap can benefit from many of the latest DeFi innovations and experiments without any additional work. Furthermore, when developers enhance Uniswap's functionalities, they attract more users to the DEX. Most of these projects either simplify the user experience or add more sophisticated ways to interact with the protocol without complicating the core user interface.

Integration

The integration of new projects can be broadly categorized into three types: aggregators, wallets, and other DeFi protocols.

In terms of user growth and acquisition for Uniswap, aggregators may be the least impactful category. Specifically, DEX aggregators like 1inch and ParaSwap exist purely to optimize execution (price, including slippage, fees, and gas costs). While aggregators have contributed 26.8% of Uniswap's trading volume over the past two years, only 48.6% of their trading volume was conducted through Uniswap. Even though aggregators are useful tools, they do not attract additional trading volume because they lack built-in growth flywheels or their own network effects (i.e., for DEXs, trading volume increases liquidity, and vice versa).

Dashboards also fall under the category of aggregators. These non-custodial interfaces, such as Zerion, Zapper, and Instadapp, simplify the use of Uniswap. They streamline the user experience by centrally displaying position data and enabling position management. Users can create new positions (swap tokens) and provide liquidity through position management, both of which can connect to Uniswap.

Another category developing swap functionalities is wallets. Wallets like Trust Wallet and Rainbow Wallet have integrated the Uniswap protocol, meaning users can execute swaps directly within their wallets. Other popular wallets, such as Coinbase Wallet, also offer token swap functionalities through DEX aggregators (0x), which often route through Uniswap.

Other DeFi protocols integrate Uniswap in various ways. Simpler integrations through protocols like Para Space and MakerDAO allow LPs to use their V3 liquidity positions as collateral, thereby enhancing capital efficiency. Projects like Opyn and Ondo Finance integrate Uniswap into their options and structured products, respectively, providing users with more complex strategies.

Enhanced Features

Uniswap's enhancements refer to simultaneously expanding functionalities and making the protocol easier to use.

In terms of liquidity provision, projects like Arrakis Finance have automated liquidity management on Uniswap V3 and reintroduced composable LP tokens. Specifically, Arrakis Finance currently manages approximately $880 million in liquidity on Uniswap V3, accounting for about 31% of its total liquidity. In terms of token swaps, traders can use projects like Sorbet Finance to set limit orders.

Other projects have expanded Uniswap's "non-human" market. As of now, trading bots are estimated to account for 20-40% of Uniswap's trading volume. Open-source software like Hummingbot can help users create high-frequency bots that run market-making and arbitrage strategies alongside Uniswap.

NFTs

While Uniswap has already used NFTs to represent V3 liquidity positions, this is quite different from the NFT integration in its roadmap, which promises to bring NFT swaps to the platform.

In June 2022, Uniswap Labs announced an NFT initiative primarily focused on acquiring the NFT trading aggregator Genie. Since then, Genie’s founder, now the NFT product lead at Uniswap Labs, Scott Gray, has begun to enrich Uniswap's NFT roadmap.

The acquisition of Genie and the announcement of the integration of sudoswap indicate that Uniswap has decided to aggregate and acquire liquidity from multiple NFT trading platforms, rather than "owning" liquidity as it does with ERC-20 tokens. Tactically, this makes sense, as the token market relies more on depth (reducing slippage), while the NFT market relies on breadth (diversity).

In terms of user growth and acquisition, this strategy could have far-reaching implications, as NFTs currently have a larger reachable user base than token trading. Overall, this plan will bring a new and larger user base to this DEX while lowering customer acquisition costs.

Risks

Uniswap's open-source nature allows community developers to create on top of this protocol, fostering user growth and originality. Although these additional layers often strip customers away from this core AMM, they can still introduce risks.

For example, enhanced functionalities that simplify investment strategies require users to interact with smart contracts not developed by the Uniswap Labs team. If this smart contract is attacked, users' funds may be lost, which may not be Uniswap's fault, but it could still negatively impact user confidence and the Uniswap brand. Additionally, the fragmentation of interaction points diminishes the visibility of the Uniswap brand and shifts attention to overlapping projects that cannot guarantee loyalty to the Uniswap ecosystem.

In terms of fragmentation, the increasing number of Uniswap deployments also poses risks. Since current users often extend liquidity supply in new deployments to pursue incentives, existing pools are more likely to lose depth, leading to higher price slippage during trade execution. That said, this dynamic can be offset by new liquidity providers and fee tier centralization. Higher slippage not only prompts traders to look elsewhere but also reduces the chances for DEX aggregators to execute trades through Uniswap pools.

Fee Switch

For a long time, the Fee Switch has been one of the most discussed topics within the Uniswap community. Currently, 100% of trading fees are borne by LPs based on their contribution to the liquidity reserves. This tax-free model has been crucial for Uniswap's development into the giant it is today.

The Fee Switch, controlled by Uniswap governance, refers to shifting a portion of trading fees from liquidity providers to the Uniswap DAO treasury as protocol fees. Although the Fee Switch has not yet been activated, in July, token holders voted in favor of a 120-day pilot test of the Fee Switch on three major stablecoin-ETH pools (DAI-ETH, ETH-USDT, USDC-ETH), charging a 10% protocol fee. The Fee Switch will challenge liquidity providers' bottom lines while increasing the likelihood of liquidity supply being reallocated to other trading platforms.

If the proposal passes on-chain voting, this pilot will be one of the largest experiments in Uniswap's history. It will determine whether LPs redistribute their liquidity supply elsewhere or continue using the DEX with the highest trading volume. Some believe that activating the Fee Switch is a risky short-sighted move, and the focus should be on growth and user acquisition. Others argue that retaining protocol fees provides UNI token holders with a new tool to leverage for the protocol's development.

In October, UF announced funding for Alastor, a team that recently provided the community with qualitative and quantitative research on the impacts of the Fee Switch.

There are also interesting discussions surrounding the Fee Switch and the appreciation of UNI tokens. Dan Elitzer, co-founder of Nascent, described a future where the Uniswap protocol would transition to a specific application chain ("appchain") or an Ethereum-based rollup.

The premise of the appchain argument is that there are three costs traders incur: swap fees, gas fees, and MEV—only swap fees can be controlled by the protocol. In a world of appchains or rollups, gas fees would become cheaper, providing more flexibility for the flow of value for UNI tokens, which could be used to control validators. While such a significant change seems unlikely to occur in the short term, it does reveal the potential for innovation.

Another risk is that the current state of Uniswap may reveal an increasing divide between Uniswap Labs and UNI token holders. Reports indicate that the $165 million funding round values Uniswap Labs at $1.66 billion, which is comparable to the value of UNI held in the community treasury. Most importantly, during the four-year lock-up period, a total of 40% of the genesis UNI supply was allocated to the team, investors, and advisors. Therefore, although there are still two years until this portion of tokens is unlocked, the additional funding may deepen their concerns about token appreciation.

Conclusion

Uniswap has successfully captured the DEX market, so what’s next? This success largely stems from ecosystem funding and open-source development. Both initiatives have paved the way for expanding its potential market through new business ventures. Multi-chain deployments, integrations, enhanced functionalities, and the acquisition of Genie have demonstrated its vertical and horizontal expansion.

In addition to the aforementioned expansions, upcoming operational changes may negatively impact Uniswap's core user base. The Fee Switch experiment, if passed, will be a significant test for UNI holders and protocol builders across the crypto space. Regardless of what ultimately happens, Uniswap Labs has ample funding to continue building. The team that launched Uniswap during the last bear market may continue to innovate during this bear market as well.

Risk warning

Risk warning Risk warning

Risk warning