Grayscale (GBTC) Effect: The Originator of Institutional Bubble and Collapse

Regardless of the current bill, it heralds the end of the current cycle.

Regardless of the current bill, it heralds the end of the current cycle.Original Title: 《The Grayscale (GBTC) Effect》

Written by: Ben Lilly

Compiled by: Deep Tide TechFlow

We have reorganized a story from two years ago, starting in 2020, which we call the "Grayscale Effect."

As we look back at these images, we find that 2020-2021 marked the beginning of a bull market, but at the same time, it also sowed the seeds for the bear market that emerged in 2022.

Today, the bear market continues.

Perhaps, cryptocurrency bystanders on Twitter and the media are currently helplessly waiting for the final doomsday to arrive, hoping it comes sooner rather than later. Because that Digital Currency Group (DCG) empire is collapsing in on itself… an empire that now notoriously holds the Grayscale Bitcoin Trust…

And these early clues show us that we are entering a complete cycle, where various catalysts from the past are now disintegrating, and we are seeing the other side of the double-edged sword.

So today, let’s delve into some recent scandals to make sense of what is happening today.

The Beginning of the Bubble

Before we begin, I want to address one thing.

I mentioned that we are treading water, and before anyone suggests that all the progress made two and a half years ago has now vanished, I want to quickly dispel that malignant thought.

This is not two and a half years ago; what has happened this year will not set the industry back three to four years.

Thinking in such a malignant way may hint at the origin of a person's beliefs ------ rooted in speculation. I believe this mindset is detrimental to society as a whole. We will soon see many of the downsides brought about by this behavior.

Therefore, while the current atmosphere is somber and reflective, let us not overlook the technological breakthroughs that are occurring at an astonishing pace every week… this innovation is a fact. It is the intrinsic power of the industry that will not be pushed back a few years due to speculative behavior.

If anything, the rising energy among GitHub, forums, and eager teams is like a volcano ready to erupt. Nothing in its path can slow its progress. And once this energy is released into the world, it will create the most fertile ground, making the future brighter.

The innovation and development of this industry is the freest force in any industry; it is a power that is highlighted in freedom, truth, and self-sovereignty. These are truths that will not simply lose faith… and they are truths that today’s failed headlines do not reflect or mention.

Therefore, if "the purpose of conquest is to avoid doing the same things as the conquered"…… let us look back at the past in hopes of helping us move forward, not letting past mistakes haunt us tomorrow. We have not regressed; we have merely understood the distance to our goals.

Act One ------ The Beginning

It all started in the summer of 2020 with DeFi. Every crypto user caught in the on-chain trading dilemma began to learn about yield farming, vaults, liquidity aggregation, synthetic tokens, yield tokens, and more.

Amidst the clamor of these tokens and short-term yield products exceeding 1,000%, our internal trading and alert AI systems conducted an in-depth study of the abnormal demand occurring in the Bitcoin spot market.

This was a significant alert for us, as spot demand pushed prices into new ranges. Derivatives pushed us to the highs and lows of the range. For anyone recalling 2020, the fear of the March 2020 lows is etched in traders' minds.

Looking back, we find it somewhat ironic that a new species in the form of yield tokens emerged, allowing the largest whales in the ecosystem to roam unnoticed…

These whales were the reason for the 18-month bull market.

And today, as prices pull back to near the market positions of 18 months ago, we realize that all the leverage that started it all is exiting the stage. This is the double-edged sword we mentioned earlier.

The person who initiated this cycle is the same person who made headlines.

So, who am I referring to here, and what am I pointing to?

Let’s pull out a tweet that caught our interest in the summer of 2020. At the time, it attracted us more than any other simply because this bullish attitude was likely related to what AI had picked.

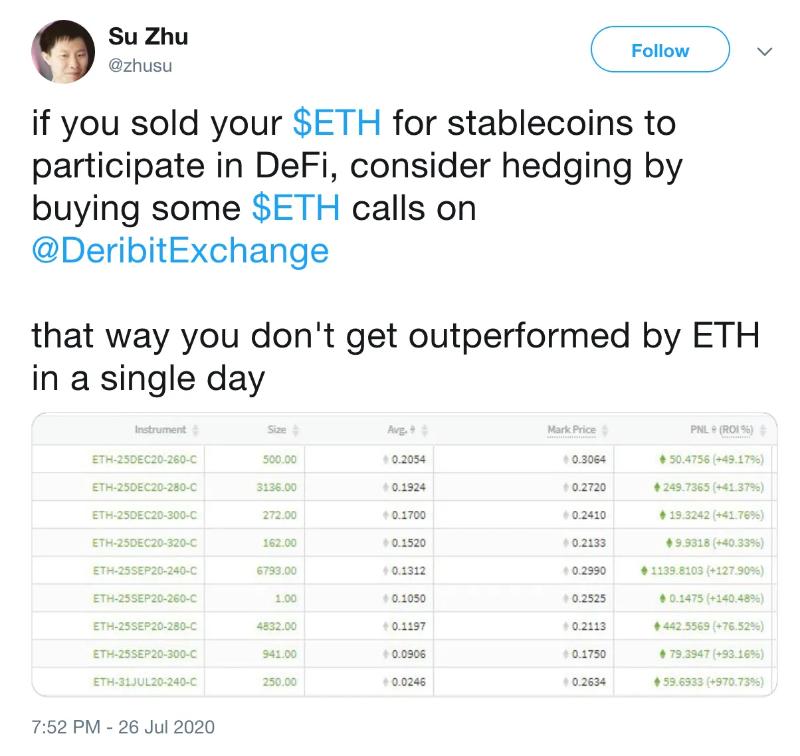

This is a now-deleted tweet from the head of Three Arrows Capital (3AC).

This is a snapshot from 3AC's books (possibly hedged), where they were continuously increasing their long positions. According to the image, Zhu's screenshot reflects that he had opened a contract of about 2,340 ETH. The total amount at the time was just about $1 million.

For a multi-billion dollar hedge fund, this might be a very small position. But at that time, 3AC was not yet a billion-dollar hedge fund.

According to a quote from a report by nymag, which cited 3AC's annual report, "According to its annual report, Three Arrows' main fund returned over 5,900%. By the end of that year, it managed over $2.6 billion in assets and $1.9 billion in liabilities."

This means 3AC made about $700 million… which also means that the profits of these two companies exceeded 5,900% at some point in 2020, managing about $11.5 million.

This makes the screenshot more reflective of an oversized bet built on belief.

As the fact that 3AC was uninterested in hedging came to light, this ETH position was an indicator of what 3AC wanted to do. We didn’t even know what BTC call options looked like ------ that was a more liquid options market.

I believe his BTC options position was much larger because anyone trading on Deribit at the time could attest to the existence of huge price discrepancies. For anyone establishing a position of seven figures or more, it would take quite a while to fill, especially on illiquid ETH options contracts.

That’s why we saw so many contracts and expiration dates in the snippet above.

Well, then, delving deeper into this position, we also know some things that happened before that tweet was posted.

First, 3AC purchased over 21 million shares of the Grayscale Bitcoin Trust (GBTC). We know this thanks to a filing with the U.S. Securities and Exchange Commission on June 2, 2020.

Grayscale is an entity of Digital Currency Group that has taken over the market, accumulating a total of 536,000 BTC so far.

Their unique structure is the reason this is possible. Its structure is essentially designed to hoard Bitcoin. BTC and USD (which is then used to purchase BTC) flow in and cannot be withdrawn.

Grayscale achieves this one-way flow by the way they allocate shares. Accredited investors or "wealthy individuals" can register for a private placement to receive shares.

Then, these accredited investors can provide Grayscale with BTC or USD. In exchange, Grayscale gives them shares of equal value. If each share equals 0.001 BTC (actually 0.00095085), then for every BTC given to Grayscale, the accredited investor receives 1,000 GBTC (minus a small fee).

The catch is that private investors must wait six months to sell GBTC on the market. This is where non-accredited retail investors speculate, those less wealthy buyers.

Exchanging stocks for BTC seems fair, but in reality, it is not. This is because GBTC almost always trades at a premium. Non-accredited investors or retail investors seeking pure investment in BTC on the stock market are not paying fair value.

This is what I mean… recently GBTC closed at $28.25. According to the BraveNewCoin liquidity index, Bitcoin closed at $22,830. According to Grayscale's website, each GBTC share equals 0.00095085 BTC. This means the fair value of GBTC is $21.71. The current price has a 30% premium, simply because buyers are not wealthy. This 30% premium flows directly to the qualified investors who hand over BTC.

This strategy is how Grayscale creates trusts, where Bitcoin essentially enters the trust in a one-way flow. Which qualified investors holding Bitcoin are not interested in increasing their Bitcoin balance? It doesn’t matter if the price is $5,000 or $20,000. As long as there is a premium, the value of BTC will grow.

Within six months, this is an almost risk-free return, with a 30% return rate, and a 69% return over a year.

This is quite substantial, and natural economic pressure should bring this premium down to 0%. However, for some reason, we have not seen this happen yet.

This means that 3AC likely purchased Bitcoin before submitting the filing on June 2. We can estimate the period shown below based on the approximately 30 days it took for Su Zhu to tweet on December 5, 2020, and submit the next disclosure document on December 31, 2020. The time below is just over 30 days.

But remember, Zhu held some ETH call options for July. They had a strike price of 240, with a cost of 0.0246 ETH per contract.

If these contracts were purchased 1.5 months or longer in advance, it means that for the contract to be profitable, the price needs to rise by over 20% to 40% (estimated).

Currently, we can assume these positions were entered during this timeframe.

The point here is that 3AC likely purchased their BTC in the spot market before buying call options, then sent the tokens to Grayscale and filled out SEC filings. This makes sense because you can profit from your spot purchases, as 21 million shares (~1000 GBTC shares = 1 BTC) is about 21,000 Bitcoins.

So many Bitcoins at the time were worth $150 million to $200 million, which means this was a borrowed amount (from the lender Genesis) according to 3AC's assets and liabilities.

Now, if we take a step back, we can time it more accurately…

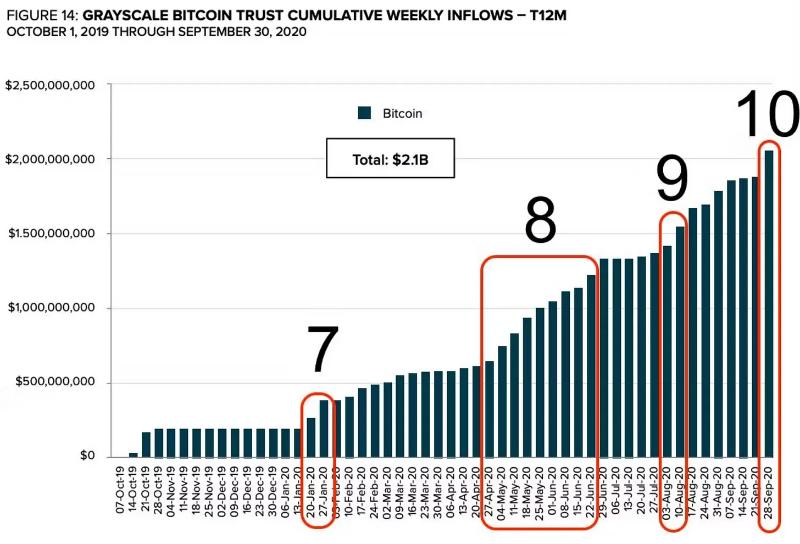

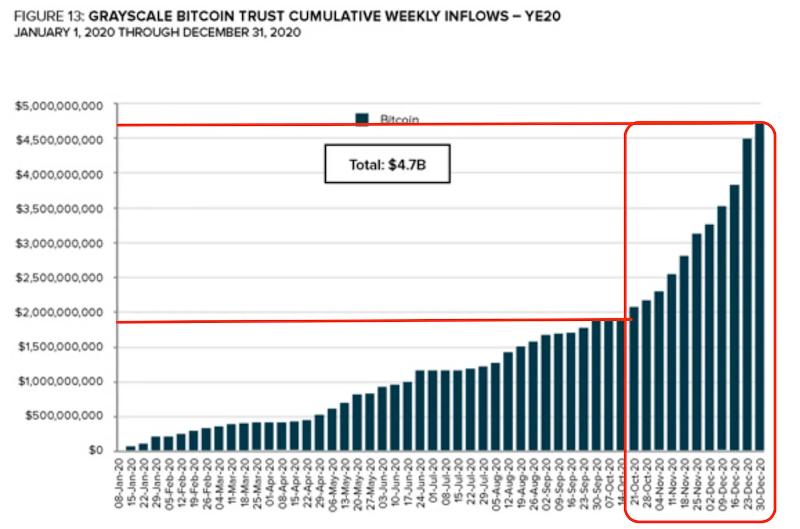

Here is a screenshot of the weekly cumulative inflows for Grayscale.

This tells us that inflows may have started as early as the week of May 11. This places us at the starting point of the two boxes in the previous candlestick chart. It also provides more support for the significant movements at the end of April and early May, as it stemmed from the 3AC<>Grayscale dynamic.

This section basically summarizes the first act of Su Zhu.

But interestingly, in the first act, we can see Su Zhu exhibiting fear in his directional bets. He wanted to lock in the GBTC premium but was worried it would disappear.

Here, he requested SBF from FTX to create a tool around Grayscale's GBTC Trust. We can only assume this was to allow 3AC to exit positions in the trust without waiting six months.

This tweet shows the unease caused by the timing. 3AC submitted their filing to the SEC on June 2, and their potential premium profits during June dropped from about 23% to single digits.

While the premium still exists… it foreshadows the end.

Act Two ------ Increasing Leverage

My initial theory was that 3AC would hold its GBTC for at least six months before selling.

This would mean that in December, 21 million GBTC would enter the market.

But thanks to some digging by Data Finnovation in this article, my initial view seems to be incorrect. When we look at the GBTC charts and volumes, it also appears consistent… the volume of 21 million shares seems to be nonexistent. After Genesis, the lending subsidiary of Grayscale's parent company, lent out Bitcoin, throwing out 21 million shares… I highly doubt they would want to create such volatility.

Instead…

Why did 3AC go the opposite way and add more leverage? After all, Bitcoin had already risen, and the premium was increasing… so here, taking cash out seems like a good choice. We have heard stories that lenders wouldn’t even conduct due diligence on 3AC.

So if 3AC were to increase leverage, the conversation might have occurred at the end of November or early December. The reason is that we can see Zhu becoming increasingly confident about what was about to happen.

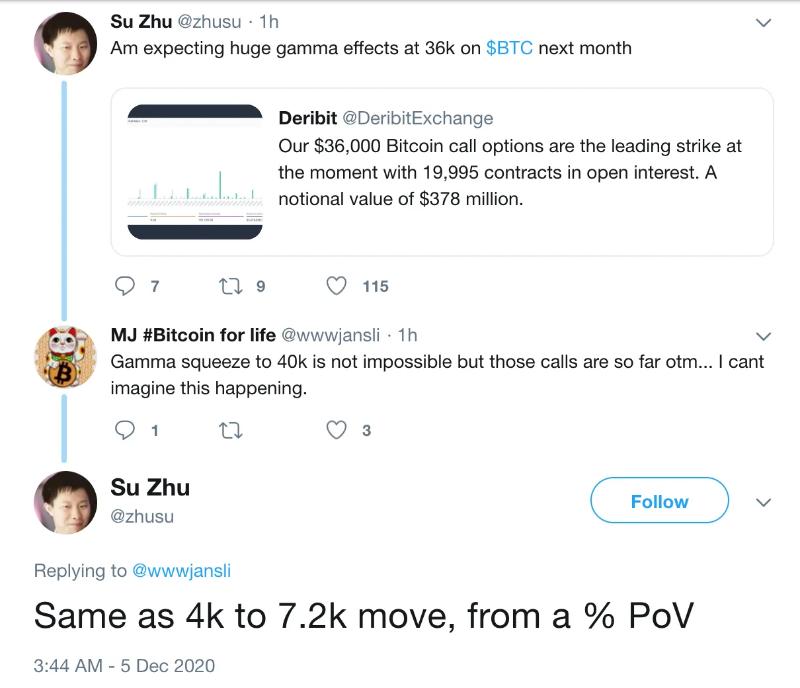

Below is a deleted tweet indicating he believed a Gamma squeeze was about to happen at the end of the month. Remember, Zhu held call options at the time.

And Su Zhu having so many forward-looking call options might indicate that the call to continue increasing leverage for 3AC might have actually occurred in the summer of 2020.

So stepping back…

Su Zhu was confident on December 5, 2020, stating he expected Gamma to push BTC above $36,000. At that time, the price was $18.6k, meaning this required a 100% return in about four weeks. Meanwhile, BTC had not yet reached an all-time high, making this again a daunting task.

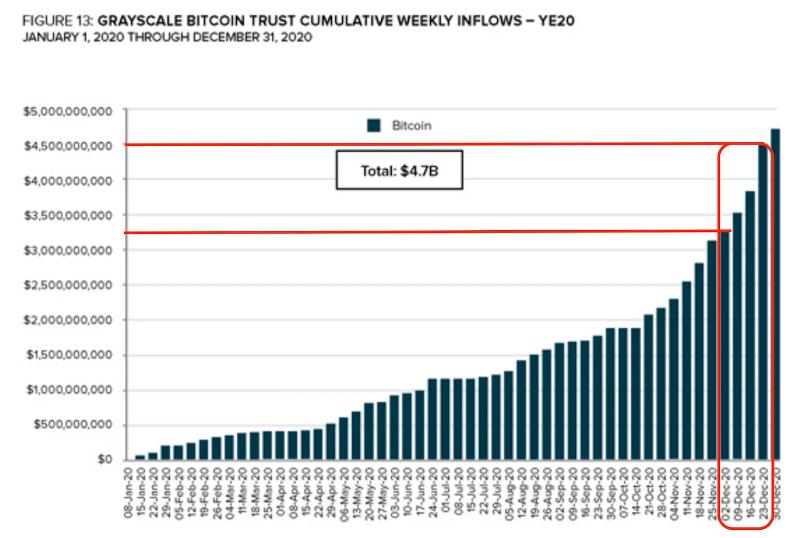

This confidence aligns with the filing submitted to the SEC on December 31, 2020, which stated that 3AC held 38,888,888 shares of GBTC at that time.

This means that from June 2 to December 31, 2020, 3AC increased its holdings by 17.8 million shares.

This is capital flowing into the trust, providing significant space for 3AC and other companies. And the largest inflows coincidentally occurred when the market was hot. If I had to guess, the largest increase occurred when 3AC took action to attempt the Gamma squeeze mentioned on December 5.

And to be honest, if the story's protagonist, a Bitcoin options trader, turned $638,000 into $4 million in five weeks, I wouldn't be surprised if it was 3AC. This timing would again be an undeniable coincidence.

So now it’s the end of 2020, and 3AC has $2.6 billion in assets and $1.9 billion in liabilities. With 38.8 million GBTC shares, at around $32 per share, we get about $1.25 billion, nearly half of their books.

With about $700 million in profits earlier this year, we can assume that 3AC was entirely surviving on the Grayscale effect. The entire market was rising. In trades that accounted for half of 3AC's books, non-hedged trades yielded over 60 times returns.

Given that 3AC had $1.9 billion in liabilities on its books, we can assume they were also borrowing BTC to engage in the Grayscale trades we have been discussing so far.

Borrowing money from one DCG subsidiary to help another subsidiary earn massive management fee income.

It’s like allowing lenders to open shops for homebuyers in the upcoming community. These homebuyers actually don’t want to live there. So the bank gives them money to buy houses… new houses primarily wait six months to be built.

Meanwhile, the home builders earn a percentage of profit from all the houses.

The key here is that there are no other home builders in the area… or in other words, there are no other ways to buy Bitcoin.

So looking back, lenders earned about 10% on loans. Home builders earned 2-3% profit on each house. And no homebuyers intended to actually live in the houses.

This means that for the plan to work, new buyers must enter the market and cannot purchase from the original home builders.

How can this be achieved?

Act Three ------ The Narrative

In the first quarter of 2021, we began to see a shift in the narrative. To prevent Grayscale's premium from turning negative… more buyers were needed.

This meant reaching out to the masses. The key here is that individuals cannot purchase houses from home builders (i.e., directly from Grayscale). They need to buy GBTC from the market.

This is where the large number of retail investors comes in.

And they couldn’t attract users willing to learn the trading curve by using exchanges like Coinbase, Kraken, or Gemini.

This is where the "Drop Gold" campaign comes into play. It was initially launched in May 2019, precisely the crowd Grayscale needed to entice. More importantly, if you do some searching online, you will find that it was at the end of 2020 and the beginning of 2021 that users outside of cryptocurrency embraced this advertisement.

Then, to layer a narrative on top of the narrative, Zhu began his supercycle narrative in the first quarter, suggesting that people needed to pay a high price for cryptocurrency because it would only go up.

The hype was in full swing.

However, this was not enough. Grayscale saw inflows of over $2.5 billion in the last 10 weeks of 2020.

It was preparing to go public as soon as mid-April. These 10 weeks witnessed more capital entering the trust than in the previous seven years combined. Read that again… in these 10 weeks, the capital entering the trust was more than in the previous seven years.

This period coincided with the trust's net asset value (NAV) turning negative. The inflows in August caused the stock price to drop below the level at which the trust could be redeemed ------ if the trust allowed redemptions.

This was not just a hassle… it was the real beginning of the crash. Just as over $2.5 billion of GBTC was about to enter the market, how would Grayscale save its negative net asset value?

Act Four ------ The End

On April 5, Grayscale continued to announce its intention to convert the trust into an ETF. If successful, the net asset value would return to standard value.

To restore the trust to par, Grayscale needed to sell BTC to the market. This meant that if someone bought GBTC at a price lower than the net asset value, they would profit.

This was the beginning of the end for the trust. When Bitcoin rebounded in the third quarter of 2021, the net asset value nearly recovered… but the net asset value never turned positive again, and it was clear that the trust was becoming weak.

Grayscale, DCG, Genesis, and 3AC were all pigs at the trough. If life has taught me one lesson, it’s to never be a pig, because pigs get slaughtered.

And that’s exactly what happened when the market began to turn in 2022.

In any case, this is why we now see Grayscale, Genesis, and DCG struggling. Barry Silbert has indeed done a lot of good in this space.

But he and his massive entity became greedy. If we look closely, we might see that the roots of Grayscale/DCG are connected to almost all explosive events in cryptocurrency. This industry is indeed that small.

Perhaps he was good at first, but now it has become harmful to the industry. Don’t worry about its demise. If we find that Grayscale <> DCG <> Genesis (and perhaps more entities like BlockFi) have also died off, I wouldn’t be surprised.

Whatever the current bill is, it heralds the end of the current cycle. Perhaps, it brings us a little closer to the next cycle.

Risk warning

Risk warning Risk warning

Risk warning