A Detailed Explanation of the Current Status of Stablecoins and Other Derivatives

After the sudden shock brought by the predicament of FTX, participants in the cryptocurrency market continue to readjust.

After the sudden shock brought by the predicament of FTX, participants in the cryptocurrency market continue to readjust.Original Title: 《Coin Metrics' State of the Network: Issue 183》

Written by: Kyle Waters, Matías Andrade

Compiled by: Lynn, MarsBit News

Perspectives on Stablecoins and Other On-Chain Derivatives

Following the sudden shock brought about by the FTX debacle, cryptocurrency market participants continue to readjust. As we noted in the recent edition of the "State of the Network," Alameda's wallet has a long and extensive on-chain footprint across many cryptocurrency assets and blockchains. Therefore, the impact is significant and evolving. We believe a particularly noteworthy area to focus on is stablecoins.

Stablecoins are digital tokens issued on public blockchains that track underlying assets, predominantly the U.S. dollar today. In the most popular fiat-backed model, issuers like USD Coin's Circle hold reserves to back the tokens, which can be redeemed for the underlying dollars.

This year, stablecoins have come under intense scrutiny following the malignant spiral of the algorithmic stablecoin Terra USD, yet they remain a significant area of development in the digital asset industry. How has the stablecoin ecosystem been maintained after the collapse of FTX?

Adoption

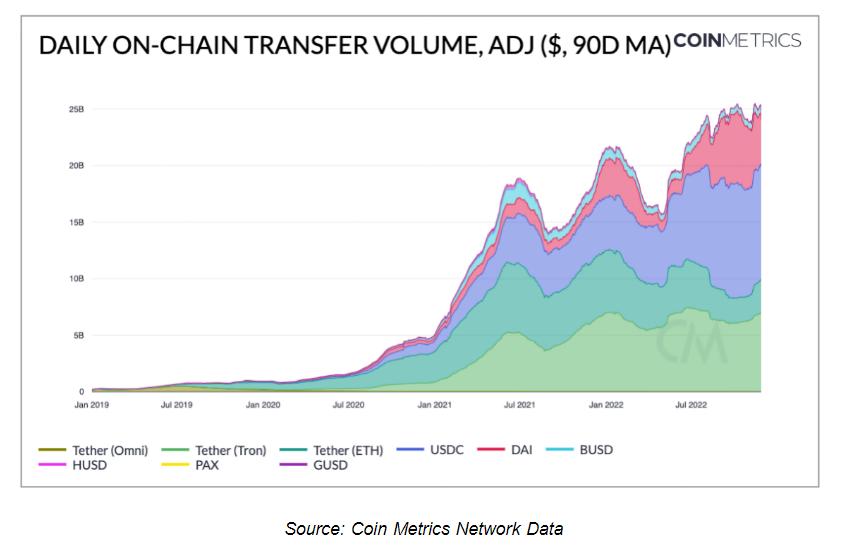

A simple metric for measuring adoption is the value of on-chain transfers. Using a relatively long 90-day moving average window, the value exchanged daily on the blockchain with stablecoins is nearing historical highs, at around $25 billion per day. About $20 billion of this comes from transfers of USDC (on Ethereum) and Tether (on Ethereum and Tron).

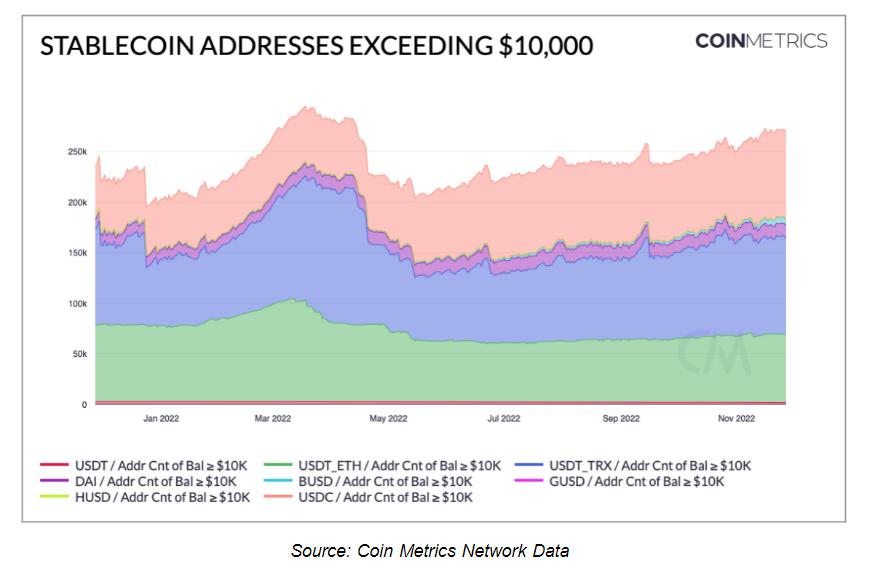

It is also worth considering the role stablecoins play in allowing users to withdraw funds from exchanges to reduce their counterparty risk. We can note that in recent months, the number of addresses holding various stablecoins valued at over $10,000 has increased; particularly, USDC has seen a significant rise since early November, from 76,000 to 86,000 addresses.

Free-Floating Supply and Redemptions

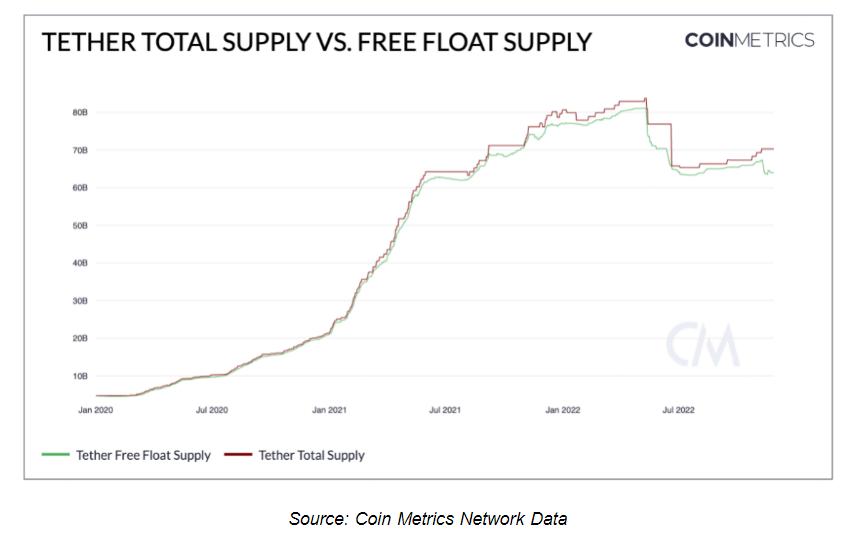

Coin Metrics has calculated a free-floating supply metric that better captures the liquid supply in circulation not held by treasury or redemption accounts.

This is especially important for Tether, whose redemption model includes a treasury address holding USDT for redemptions. This USDT should not be considered part of the circulating supply, so it is important to look at the free-floating supply to accurately assess supply trends. Since November 8, the supply of USDT (on Ethereum, Tron, Omni) has decreased by about $4 billion, from $67 billion to $63 billion.

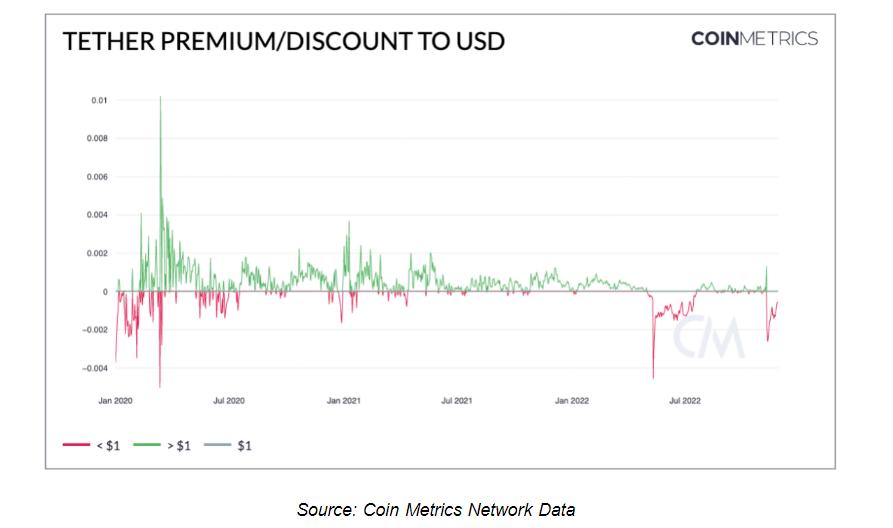

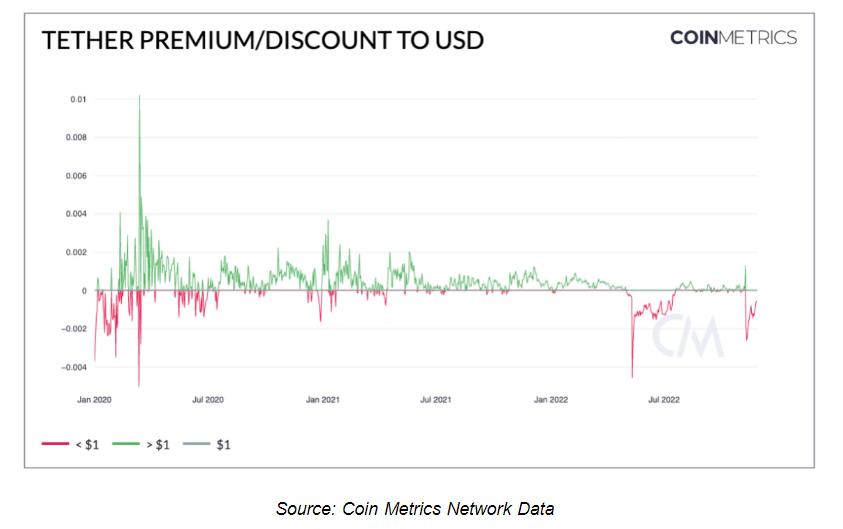

Redemptions have occurred with Tether's price slightly below its $1 peg. This created an arbitrage opportunity for some larger market participants: they could buy USDT at a price below $1 and redeem it at face value. However, the pace of redemptions has not been as intense as in the spring of this year, reflecting that the discount to the $1 peg is not as severe.

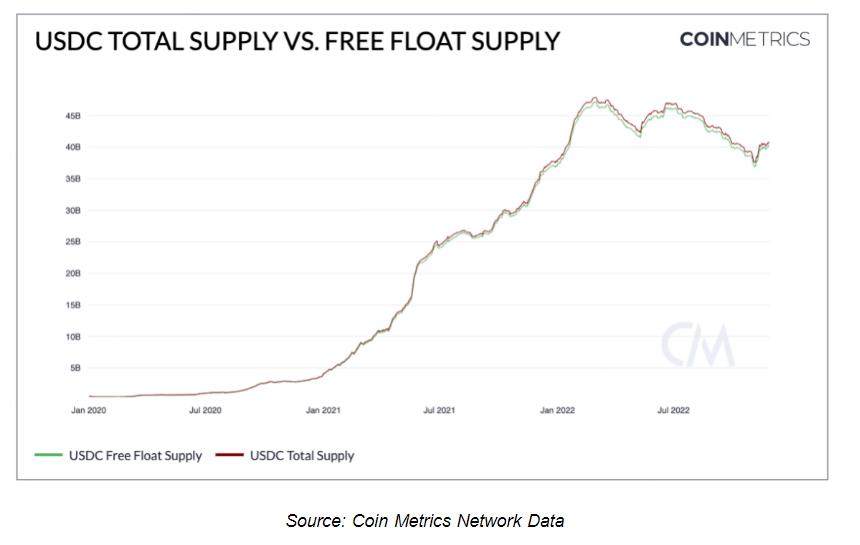

Meanwhile, another fiat-backed stablecoin stalwart, USDC, has experienced a slight increase in free-floating supply since November 8, rising from $37 billion to $40 billion.

Outlook on wBTC

While stablecoins have been the most adopted on-chain derivatives so far, there are also "wrapped" assets, which are tokens used to interact with underlying assets that cannot be addressed within smart contracts. Wrapped Bitcoin (wBTC) is a Bitcoin derivative used on Ethereum, managed by depositing BTC with a custodian that issues wBTC tokens, ensuring a 1:1 correspondence between the two. Recently, the multi-signature address managing most of the wBTC funds was adjusted to remove inactive signers (including FTX's Blockfolio), reducing from 18 addresses to only 11, requiring 8 signatures to approve transactions.

Shortly after the FTX debacle, one of the main custodians supporting wBTC, a company called BitGo, temporarily halted withdrawals, causing the price of wBTC to deviate from the price of underlying BTC. Since then, the price of wBTC has begun to recover but remains below the reference rate of BTC. The supply of wBTC has decreased, and the pace of redemptions has accelerated.

Conclusion

As the market and participants seek to learn and recover from recent events, we must closely monitor the financial infrastructure that supports many of the most popular uses of cryptocurrencies. Additionally, we can gather a wealth of information by focusing on stablecoins as market participants strive to reduce their risk exposure and protect their assets.