Vitalik: Five Exciting Applications of the Ethereum Application Ecosystem

Money, DeFi, identity systems, DAO, and hybrid applications.

Money, DeFi, identity systems, DAO, and hybrid applications.Original: 《What in the Ethereum application ecosystem excites me》

Author: Vitalik Buterin

Compiled by: Qianwen, ChainCatcher

Special thanks to Matt Huang, Santi Siri, and Tina Zhen for their feedback and comments.

Ten years, five years, or even two years ago, my views on what Ethereum and blockchain could do for the world were very abstract. I would say, "This is a general-purpose technology, just like C++." Of course, it has specific attributes such as decentralization, openness, and censorship resistance, but beyond that, it was too early to say which specific applications would have the most significance.

The world today is no longer the world it was back then. By now, there are almost no ideas that we haven't fully explored: if something is a great success, it is likely a version that has been discussed multiple times on blogs, forums, and conferences. We are also increasingly able to identify the fundamental limitations of this field. Many DAOs are welcomed by participants, although they also face inconveniences and cost barriers, and many DAOs perform poorly. Applications in industrial supply chains have not been fully realized, and a decentralized Amazon on the blockchain has yet to materialize. But we have also seen some key applications being continuously adopted, which are meeting real needs—these are the applications we need to focus on.

Thus, I have changed my perspective: what interests me about Ethereum is no longer the undiscovered unknown potential but rather several specific applications that have already been validated and will become increasingly powerful. What are these applications, and which applications am I no longer optimistic about? This is the content of this article.

1. Money: The First and Most Important Application

When I visited Argentina for the first time last December, I was wandering around on Christmas Day, and almost all the stores were closed. I was looking for a coffee shop, and after passing five closed cafes, we finally found one that was open. When we walked in, the owner recognized me and immediately showed me the ETH and other crypto assets in his Binance account. We ordered tea and snacks and asked the owner if we could pay with ETH. The coffee shop owner agreed and showed me the QR code for his Binance deposit address, and I sent him about $20 worth of ETH from my Status wallet on my phone.

Of course, this was not the most meaningful application of cryptocurrency in the country. Many people are using it to save money, make international transfers, and pay for large and important transactions, etc. But even so, the fact that I randomly found a coffee shop that happened to accept cryptocurrency demonstrates the widespread adoption of cryptocurrency. In wealthy countries like the United States, financial transactions are easy to conduct, and 8% inflation is considered extreme, while in Argentina and many other countries around the world, their connections to the global financial system are more limited, experiencing extreme inflation daily. At this moment, cryptocurrency is a lifeline.

In addition to Binance, there are more and more local exchanges, and you can see their advertisements everywhere, including at the airport.

One issue with my coffee transaction is that it didn't have real practical significance. Because the fees were high, about a third of the transaction value, and it took several minutes for the transaction to be confirmed. At that time, Status did not support sending EIP-1559 transactions, which could be more reliable and faster. If I had a Binance wallet like many other Argentine cryptocurrency users, the transfer would have been free and instantaneous.

However, a year later, things are very different. After the merge, transactions are being included much faster, and the blockchain is more stable, requiring fewer confirmations for secure transactions. Scaling technologies such as Optimistic and ZK Rollups are rapidly developing. With "account abstraction," "social recovery, and multi-signature wallets" are becoming more practical. As technology evolves, it will take years to realize these trends, but progress has already been made. At the same time, there is an important "push factor" driving interest in on-chain transactions—the collapse of FTX, which reminded everyone, including people in Latin America, that even the most trustworthy centralized services can ultimately betray people's trust.

Cryptocurrency in Wealthy Countries

In wealthy countries, the more extreme use cases around how to survive high inflation and conduct basic financial activities often do not apply. But cryptocurrency still holds significant value. I use it to donate (to quite normal organizations in many countries), and I can personally attest that it is much more convenient than traditional banking. It is also valuable for industries and activities that may be banned from participating in payment activities—these industries include many that are entirely legal under the laws of most countries.

Cryptocurrency as private money is also a more important and broader philosophical use case: many governments are taking advantage of the transition to a "cashless society" to introduce levels of financial surveillance that people could not have imagined a century ago. Cryptocurrency is currently the only invention that can effectively combine the privacy of digitization and cash.

But in any case, cryptocurrency is far from perfect. Even if all the technical, user experience, and account security issues are resolved, the volatility of cryptocurrency remains a fact, and this volatility makes it difficult to use for savings and commerce. Hence, we have stablecoins.

Stablecoins

The value of stablecoins has been discussed in the Ethereum community for a long time, quoting a blog post from 2014:

"In the past 11 months, Bitcoin holders have lost about 67% of their wealth, and at many times, its price has fluctuated by as much as 25% within a week. In the face of these concerns, people are increasingly interested in a simple question: can we have the best of both worlds? Can we have the complete decentralization offered by a crypto payment network while also having a higher level of price stability without enduring such extreme ups and downs?"

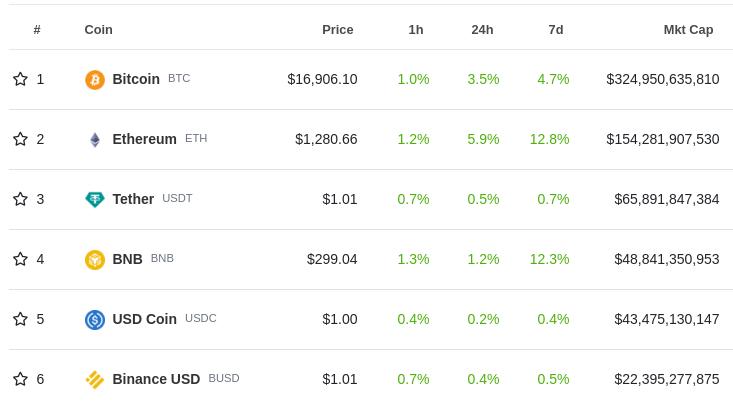

In fact, stablecoins are very popular among today's pragmatic cryptocurrency users. That is to say, contrary to the core of cryptocurrency—today's most successful stablecoins are centralized, primarily USDC, USDT, and BUSD.

Top cryptocurrency market capitalization, from CoinGecko data, as of 2022-11-30, three of the top six are centralized stablecoins.

On-chain issued stablecoins have many convenient features: they are open for anyone to use, they can resist the most massive and opaque forms of censorship (the issuer can blacklist and freeze addresses, but this blacklist is transparent, and freezing each address incurs literal transaction costs), and they interact well with on-chain infrastructure (accounts, DEXs, etc.). However, it is still unclear how long this status will last, so it is necessary to continue exploring other alternatives.

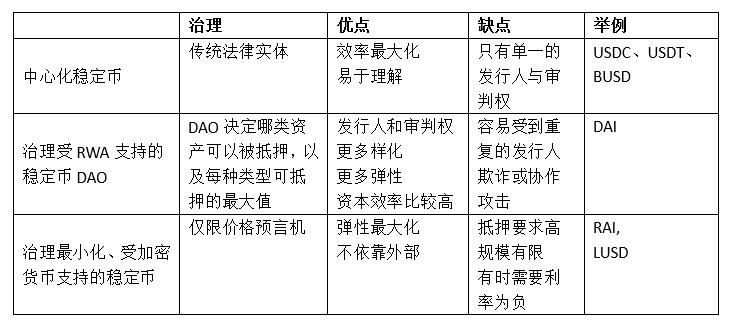

I believe the design space for stablecoins can be fundamentally divided into three distinct categories: centralized stablecoins, DAO-governed real-world asset-backed stablecoins, and governance-minimized cryptocurrency-backed stablecoins.

From the user's perspective, these three types of tokens balance efficiency and resilience. USDC is effective in the long term, but its continued stability depends on the macroeconomic and political stability of the United States, whether the regulatory environment continues to support providing USDC to everyone, and the credibility of the issuing institution.

On the other hand, RAI can withstand all these risks, but it has a negative interest rate: at the time of writing this article, it was -6.7%. To stabilize the system (to avoid collapsing easily like LUNA), every RAI holder must be paired with a negative RAI holder (also known as a "borrower" or "CDP holder") who puts up ETH as collateral. If more people engage in arbitrage, holding negative RAI and balancing it with positive USDC or even interest-bearing bank deposits, this interest rate will improve, but the rate of RAI will always be lower than the rates in a normally functioning banking system. Moreover, negative interest rates always exist, and the potential user experience issues they bring will persist in the long term.

The RAI model is ultimately the ideal choice for more pessimistic experimenters (lunarpurk): it avoids all connections with the non-crypto financial system, making it harder to attack. The negative interest rate prevents it from being a convenient alternative to the dollar, but it also requires accepting all disconnections: a governance-minimized stablecoin could track some non-monetary assets, such as the global average CPI index, and promote itself as representing an abstract "effort to stabilize price." This would also reduce inherent regulatory risks, as this asset would not attempt to provide a "digital dollar" (or other currencies).

DAO-managed, RWA-backed stablecoins could be a worthy medium if they can operate well. Such stablecoins could combine enough robustness, censorship resistance, scale, and economic practicality to meet the needs of a large number of real-world cryptocurrency users. But to achieve this, both real-world legal work is needed to ensure the stability of issuers and healthy, resilience-oriented DAO governance.

In any case, the good operation of any stablecoin will benefit various currency and savings applications, which today already provide utility to millions of people.

2. DeFi: Keeping It Simple

Decentralized finance started with great glory, but its development has also been limited, evolving into an over-capitalized monster that relies on unsustainable yield farming, and is now in its early stages, likely to develop into a stable medium that enhances security and refocuses on some particularly valuable applications. Decentralized stablecoins are now, and may forever be, the most important DeFi products, but there are also some other products that need attention.

- Prediction Markets: Since the launch of Augur in 2015, these markets have been a niche but stable pillar of decentralized finance. Since then, their adoption rate has been quietly growing. In the 2020 U.S. elections, prediction markets demonstrated their value and limitations, and in 2022, cryptocurrency prediction markets like Polymarket and game funding markets like Metaculus have gained increasing popularity. Prediction markets are valuable as a tool for understanding, and using cryptocurrency can make these markets more trustworthy and easier to adopt globally. I expect prediction markets will not experience extreme multi-billion dollar explosions but will continue to grow steadily and become more useful over time.

- Other Synthetic Assets: The formula behind stablecoins can, in principle, be replicated for other real-world assets, including major stock indices and real estate. The latter is limited by the inherent heterogeneity and complexity of space, requiring more time to yield substantial results, but they may still be valuable. The main question is whether someone can balance centralization and efficiency to allow users to obtain these assets at a reasonable return rate.

- Glue Layers for Efficient Trading Between Other Assets: On-chain, there are assets that people want to use, including ETH, centralized or decentralized stablecoins, more advanced synthetic assets, etc. A glue layer that allows users to easily trade between them is very valuable. Some users may want to hold USDC and pay transaction fees in USDC. Others may hold some assets but wish to convert them immediately into other assets to pay others. Another area for development is using one asset as collateral to loan another asset. Such projects are most likely to succeed if they maintain very limited leverage (e.g., no more than 2x).

3. Identity Ecosystem: ENS, SIWE, PoH, POAP, SBT

"Identity" is a complex concept that means many things, such as:

- Basic Authentication: Simply proving that action A (e.g., sending a transaction or logging into a website) is authorized by an agent with a certain identifier, such as an ETH address or public key, without trying to explain who the agent is, etc.

- Proof: Proving claims made by other agents about an agent ("Bob proves he knows Alice," "The Canadian government proves Charlie is a citizen").

- Names: Establishing consensus that a specific human-readable name is used to refer to a specific agent.

- Personhood Proof: Proving that an agent is human and ensuring that each human can only obtain one identity through a personhood proof system (this is often done alongside proof, so it is not a completely independent category, but it is a very important special case).

For a long time, I have been optimistic about blockchain identity but not about blockchain identity platforms. The use cases mentioned above are indeed important for many blockchain applications, and blockchain is valuable for identity applications because of its independence from institutions and its interoperability advantages. However, trying to create a centralized platform to achieve all these tasks from scratch is unfeasible; a more effective approach is to take it step by step, with many projects currently dedicated to specific valuable tasks and gradually increasing interoperability over time.

And that is exactly what has happened since then. The Sign In With Ethereum (SIWE) standard allows users to log into (traditional) websites just like you can today with a Google or Facebook account. This is actually very useful: it allows you to interact with websites without Google or Facebook accessing your private information or taking over or locking your account. Technologies like social recovery can help users recover their accounts when they forget their passwords, which is much better than the services provided by centralized companies today. Today, SIWE is supported by many applications, including Blockscan chat, end-to-end encrypted email and note service Skiff, and various blockchain-based alternative social media projects.

ENS allows users to have usernames. For example, I have vitalik.eth. Personhood proof and other personal identification systems allow users to prove they are unique humans, which is useful in applications like airdrops and governance. POAP ("Proof of Attendance Protocol") is a universal protocol for issuing tokens that represent proof: Did you complete an educational course? Did you attend an event? Did you meet a specific person? POAP can be part of personal identification protocols and can also be used to try to determine whether someone is a member of a particular community (valuable for governance or airdrops).

An NFC card containing my ENS name and a POAP you received can prove that you have met me. I'm not sure if I want to further incentivize people to come to me repeatedly to get my POAP, but the idea seems interesting and useful for others.

Each of these applications is useful. However, what makes them truly powerful is the degree to which they work together. When I log into Blockscan chat, I log in with Ethereum. This means my name vitalik.eth (my ENS name) is immediately visible to anyone chatting with me. In the future, to combat spam, Blockscan chat could check on-chain activity or POAPs to verify accounts. The lowest level of verification is to verify that the account has sent at least one on-chain transaction or received funds (since this requires paying fees). Higher levels of verification could involve checking balances of specific tokens, ownership of specific POAPs, personal identification, or meta-aggregators like Gitcoin Passport.

The network effects of these different services combine to create an ecosystem that offers some very powerful options for users and applications. An Ethereum-based Twitter alternative (like Farcaster) could use POAPs and other on-chain activity proofs to create a verification function that does not require traditional KYC, allowing anonymous users to participate. These platforms could create rooms that are only open to members of specific communities or adopt a hybrid approach where only community members can speak, but anyone can listen. This is akin to Twitter polls being restricted to specific communities.

Equally important, there are more straightforward applications that help people make a living: proving verification can make it easier for people to demonstrate their trustworthiness to obtain rent, employment, or loans.

The significant challenge this ecosystem faces in the future is privacy. Currently, a large amount of information is placed on-chain, which will eventually lead to problems, perhaps not a direct risk for many, but combining on-chain and off-chain information and extensively using ZK-SNARKs can address this issue, though it requires effort; projects like Sismo and HeyAnon are early attempts. Scalability is also a challenge that can be addressed through rollups and potential verification. Privacy issues are more intractable, as each application must specifically address them.

4. DAOs

DAOs are a powerful term that represents many hopes and dreams of people entering the cryptocurrency space—establishing more democratic, resilient, and efficient forms of governance. It is also a very broad term whose meaning has changed significantly over the years. Most commonly, a DAO is a smart contract that represents ownership or control over certain assets or processes. But this structure can be anything from a low-level multi-signature wallet to highly complex multi-chamber governance mechanisms, such as those envisioned for the Optimism Collective. Some of these structures are effective, while others are ineffective or at least very misaligned with the goals they are trying to achieve.

There are two questions that need to be answered:

- What kind of governance structure is meaningful, and for what use cases?

- Is it meaningful to implement these structures as DAOs or through conventional companies and legal contracts?

A particularly subtle question is that the term decentralization is sometimes used to refer to both aspects: if the decisions of a governance structure require a large group of participants to decide, then it is decentralized; if the implementation of a governance structure is based on a decentralized structure like a blockchain and does not rely on the legal system of any single nation-state, then it is decentralized.

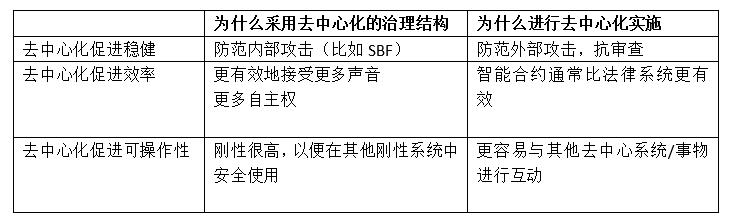

Decentralization Promotes Robustness

This means that decentralized governance structures can prevent internal attackers, while decentralized implementation can prevent powerful external attackers ("censorship resistance").

For example:

The Pirate Bay and Sci-Hub are important case studies; they have censorship resistance but do not require decentralization. Sci-Hub is primarily managed by one person, and if certain parts of the Sci-Hub infrastructure are censored, the manager can simply move it elsewhere. Over the years, Sci-Hub's URLs have changed many times. The Pirate Bay is a hybrid: it relies on BitTorrent, which is decentralized, but The Pirate Bay itself is a centralized convenience layer on top.

The difference between these two examples and blockchain projects is that they do not protect users from the platform itself. If Sci-Hub or The Pirate Bay wanted to harm their users, the worst they could do is provide bad outcomes or shut down the platform—both of which would only cause minor inconveniences, and then their users would turn to other alternatives, which would inevitably arise when they could not supply enough. They could also disclose users' IP addresses, but even if they did, the overall harm to users would still be much lower than other actions, such as stealing all users' funds.

Stablecoins are not like that. Stablecoins attempt to create stable, trustworthy, neutral global commercial infrastructure, which requires not relying on a single centralized actor externally and protecting against internal attackers. If a stablecoin's governance is poorly designed, attacks on governance could lead to users losing billions of dollars.

At the time of writing this article, MakerDAO has $7.8 billion in collateral, which is more than 17 times the market cap of the profit token MKR. Therefore, if governance is decided by MKR holders without any safeguards, someone could buy half of the MKR and use it to manipulate price oracles to steal a large portion of the collateral for themselves. In fact, this situation has occurred with a smaller stablecoin! This has not happened with MKR, primarily because MKR holdings are still relatively concentrated, with most MKR held by a fairly small group that is unwilling to sell because they believe in the project. This is a model that applies to the early adoption of stablecoins, but it is not a sustainable long-term model. Therefore, to ensure the long-term operation of decentralized stablecoins, innovation in decentralized governance is needed to eliminate such flaws.

Two possible directions include:

- Some form of non-financial governance, or perhaps a bicameral hybrid, where decisions need to be passed not only by token holders but also by other categories of users (e.g., Optimism Citizens' House, StETH holders, as proposed in Lido's bicameral governance).

- Intentional friction, making certain types of decisions only take effect after a sufficiently long delay, allowing users to see the bad outcomes and exit the system.

When conducting effective governance to optimize robustness, there are many subtle aspects to consider. If the robustness of the system depends on pathways that will only be activated in extreme situations, then the system may even want to intentionally test these pathways occasionally to ensure they work properly—just like the Ise Grand Shrine reconstruction that occurs every 20 years. This aspect of decentralized robustness still requires more careful thought and development.

Decentralization Promotes Efficiency

Decentralization for efficiency is a different school of thought: this governance structure is valuable because it can incorporate different opinions at different scales, and its implementation is valuable because it is sometimes more efficient and cost-effective than traditional legal system-based approaches.

This implies different styles of decentralization. Governance decentralized for robustness emphasizes having a large number of decision-makers to ensure alignment with pre-set goals and intentionally makes actions more difficult. Governance decentralized for efficiency retains the ability to act quickly and adjust when needed but tries to remove decision-making from the top to avoid the organization becoming a rigid bureaucracy.

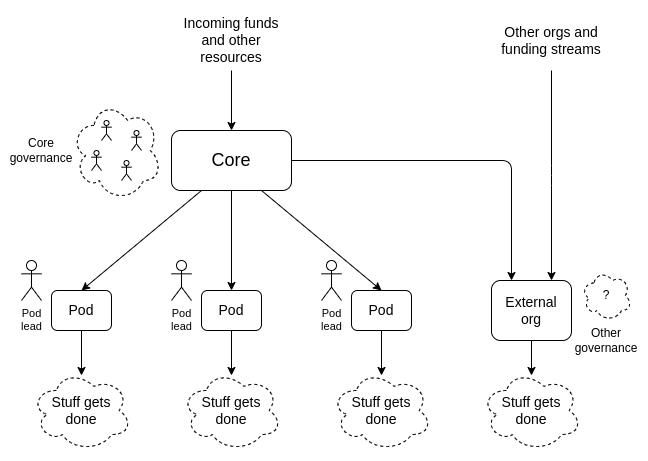

The "pod" based governance in the Ukraine DAO, which enhances efficiency by maximizing autonomy.

Decentralized implementations designed for robustness and those designed for efficiency are similar in one aspect: they both involve putting assets into smart contracts. But decentralized implementations designed for efficiency are much simpler: generally, a basic multi-signature wallet is sufficient.

It is worth noting that "decentralization for efficiency" does not hold up for large projects in the same wealthy country. But it is more valid for very small-scale projects, highly internationalized projects, and those governed by inefficient institutions and weak rule of law in their countries. Many "decentralization for efficiency" applications could also be accomplished on a central bank chain operating in a stable large country; I am not sure whether decentralized or centralized approaches are good enough, and which one becomes dominant depends on which approach first becomes a viable dependency path.

Decentralization Promotes Interoperability

This is a rather boring reason for decentralization, but it is still important: interactions between on-chain items are easier and safer than interactions with off-chain systems, as the latter inevitably requires a (vulnerable to attack) bridging layer.

If a large organization operating in a direct democracy holds 10,000 ETH in its reserves, this would be a decentralized governance decision-making process, but it is not a decentralized implementation: in practice, this country would have a few people managing the keys, and this storage system could be attacked.

From a governance perspective: if a system provides services to other DAOs that do not have the ability to change quickly, then that system itself is best not to have the ability to change quickly either, to avoid "rigid mismatches," where a system's dependencies break, and the rigidity of that system makes it unable to adapt to that break.

These three "decentralization theories" can be summarized in the following chart:

Decentralization and Novel Governance Mechanisms

In the past few decades, we have seen some new attempts at governance mechanisms:

- Quadratic Voting

- Futarchy

- Liquid Democracy

- Decentralized dialogue tools like Pol.is

These ideas are an important part of the DAO story, and they hold value for both robustness and efficiency. The case for quadratic voting relies on a mathematical argument to make accurate trade-offs between more powerful proposals and more popular but less powerful proposals (or wealthy actors). However, those who have used this method have found that it can also enhance robustness. Some novel ideas, like pair matching, intentionally sacrifice mathematically provable optimality for robustness when the assumptions of mathematical models are broken.

Case Study: Gitcoin Grants

We can analyze different styles of decentralization through an interesting edge case. Should Gitcoin Grants be an on-chain DAO, or should it just be a centralized organization?

Here are some possible arguments for Gitcoin Grants being a DAO:

- It holds and processes cryptocurrency, as most of its users and funders are Ethereum users.

- Secure quadratic funding works best on-chain, so if voting results directly feed back into the system, it reduces security risks.

- It interacts with communities around the world, benefiting from trusted neutrality rather than being centered on a single country.

- Its benefit is that users can trust it will still exist in five years, so public goods funders can invest in projects now and hope for returns later.

These arguments tend to favor decentralization for robustness and interoperability of the upper structure, although individual rounds of quadratic funding lean more towards the "decentralization for efficiency" school (the theory behind Gitcoin Grants is that quadratic funding is a more effective way to fund public goods).

If the arguments for robustness and interoperability do not apply, then simply considering Gitcoin Grants as a regular company may be better. But they do apply, so it can be argued that Gitcoin Grants is a DAO.

There are many other examples that illustrate the applicability of this argument, including DAOs that people increasingly rely on in daily life and "meta-DAOs" that provide services to other DAOs:

- Proofofhumanity (quadratic funding design scheme)

- Kleros (decentralized arbitration protocol for economic disputes)

- Chainlink (oracle protocol LINK)

- Stablecoins

- Governance of blockchain layer two protocols

I do not know enough about all these systems to prove that they have all optimized for robustness through decentralization sufficiently, but they should be.

The ones that perform poorly are mainly those DAOs where central capabilities conflict with robustness, as they do not have enough cases to "decentralize for efficiency." A major example would be large companies that primarily interface with U.S. users. When creating a DAO, it is essential to first determine whether it is worth structuring the project as a DAO, and secondly, to determine whether its goal is robustness or efficiency: if it is the former, then deep thought must be given to governance design; if it is the latter, then either innovate governance through mechanisms like quadratic funding or use multi-signature wallets.

5. Hybrid Applications

There are many applications that are not entirely on-chain but leverage the advantages of both blockchain and other systems to improve their trust models.

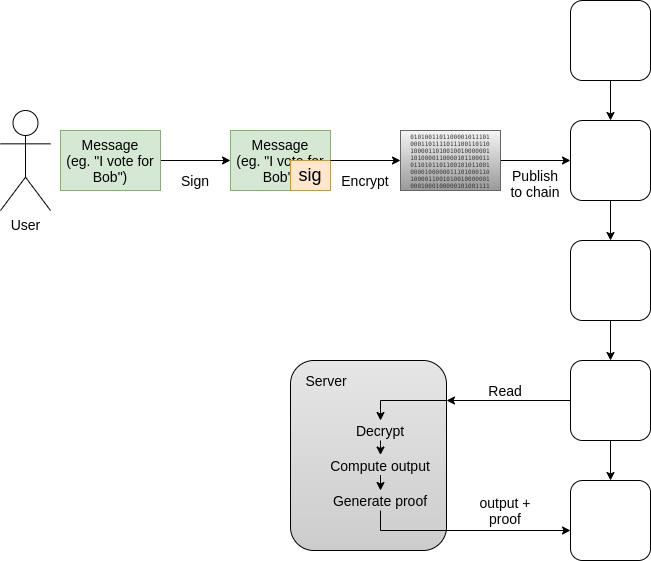

Voting is a great example. High guarantees of censorship resistance, auditability, and privacy are all necessary, and systems like MACI effectively combine blockchain, ZK-SNARKs, and limited centralization (or M-of-N) layers to achieve scalability and enforceability of all these guarantees. Voting is published on the blockchain, so users have an independent way to ensure their votes are included, but the votes are encrypted to protect privacy and use ZK-SNARK-based solutions to ensure the final results are the correct calculation of the votes.

Diagram of how MACI works, combining blockchain for censorship resistance, privacy encryption, and ZK-SNARKs to ensure results are correct without compromising other goals.

In existing national elections, voting is already a highly guaranteed process, and it takes a long time for governments and citizens to feel satisfied with the security guarantees of any electronic voting method (whether blockchain or otherwise). But such technology can quickly add value in two other areas:

- Increasing the guarantees of electronic voting processes that are already happening today (e.g., social media voting, polls, petitions).

- Creating new forms of voting that allow citizens or group members to provide quick feedback and provide high guarantees for these votes from the start.

Beyond voting, there is an entire potential field of "auditable centralized services" that could be well-served through some form of hybrid off-chain verification architecture. The simplest example is proof of solvency for exchanges, but there are many other possible examples:

- Government registries

- Corporate accounting

- Gaming (see examples in "The Dark Forest").

- Supply chain applications

- Tracking access authorization

- …

As we look further down, we find that the value of use cases decreases, but it is important to remember that the costs of these use cases are also quite low. Validiums do not need to publish everything on-chain. Instead, they can be simple wrappers for existing software, maintaining the Merkle root (or other commitments) of a database, occasionally publishing the root on-chain and using SNARKs to prove their updates are correct. This is a significant improvement over existing systems, as it opens the door for cross-institutional proof and public audits.

How Do We Achieve This?

Today, many such applications are being built, although the use of many of these applications is limited due to current technological constraints. Blockchains are not scalable, transactions take a considerable amount of time to be reliably included on-chain, and current wallets force users to choose between low convenience and low security. In the long run, many of these applications will need to overcome privacy issues.

These are all solvable problems, and we have strong incentives to solve them. The collapse of FTX has made many people realize the importance of truly decentralized solutions for holding funds, and the rise of ERC-4337 and account abstraction wallets has given us an opportunity to create such alternatives. Rollup technology is rapidly advancing to address scalability, and transactions are being included on-chain faster than three years ago.

But equally important is determining the development direction of the application ecosystem itself. Many more stable and straightforward applications have not been built because there is less excitement and short-term profit surrounding them: LUNA's market cap reached over $30 billion, while stablecoins that strive for robustness and simplicity are often largely ignored for years. Non-financial applications often cannot earn $30 billion because they do not have tokens at all. However, in the long run, it is these applications that are the most valuable to the ecosystem and will bring the most lasting value to their users and those who build and support them.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles