Uniwhale Exchange: A Chronicle of the Evolution of DeFi Trading

On-chain trading has evolved from a simple constant product formula to a centralized liquidity automated market-making mechanism, and then to more efficient leveraged trading.

On-chain trading has evolved from a simple constant product formula to a centralized liquidity automated market-making mechanism, and then to more efficient leveraged trading.Author: Uniwhale Exchange

Part One

v0.0 DeFi Genesis

Uniswap was deployed to the Ethereum mainnet in November 2018, marking the beginning of a new era in DeFi from 0 to 1. It achieved non-custodial on-chain spot trading through the use of the constant product formula (x * y = c), which is not only mathematically elegant but also simple enough for any user to perform trustless trades. The protocol is permissionless, opening the door for many projects to raise funds and provide liquidity. However, despite its simple and elegant design, users encountered several issues, such as: 1) significant trading slippage, 2) on-chain bots front-running trades, and 3) high impermanent loss. As a result, many later projects attempted to address these issues using different approaches.

v1.0 Concentrated Liquidity Automated Market Making Mechanism

Curve emerged and attempted to solve the problem of concentrated liquidity. It uses a combination of constant sum (x+y=c) and constant product to provide an efficient token exchange method while maintaining low fees and low slippage by only accommodating liquidity pools composed of related assets. However, like Uniswap V3 (see below), it only addressed the liquidity issues of stablecoin pairs. Non-related pairs are not widely used on Curve.

Uniswap V3 also sought to solve its own problems. It utilizes a concentrated liquidity automated market-making mechanism, allowing LPs to allocate their assets within customized price ranges to reduce impermanent loss. However, for LPs, Uniswap V3 is much more complex than V2. Therefore, although stablecoin pairs accounted for 98% of the overall trading volume on Uniswap after V3, V2 dominated in the number of trades, accounting for 68% of the total trading volume, especially for long-tail assets.

Part Two

DeFi innovations represented by Maker, Uniswap, and Compound gave rise to DeFi summer. A large volume of spot trading was migrated on-chain, and DeFi users were also looking forward to the introduction of derivatives trading on decentralized exchanges. Last year, we saw the emergence of many new public chains (Layer 1). The gas fees on these new public chains are much cheaper than those on the Ethereum mainnet, significantly reducing the cost of leveraged trading and laying the groundwork for the emergence of on-chain derivatives. However, on-chain leveraged trading did not experience the same explosive growth as spot trading during last year's DeFi summer, mainly due to:

- Insufficient liquidity to support large trades, making it difficult for institutions to participate, resulting in a market primarily composed of retail participants;

- Most of the spot trading volume on DEX includes demand for long-tail assets. These long-tail assets are highly volatile and not suitable for leveraged trading. Therefore, there is a lack of demand for leveraged trading in long-tail assets;

- Many new public chains are designed to be more centralized, posing certain security risks when trading large-cap assets like BTC and ETH on these new chains.

This summer, we began to see more derivatives/futures trading DeFi platforms launching different approaches to address the above issues.

v2.0 DYDX - Central Limit Order Book

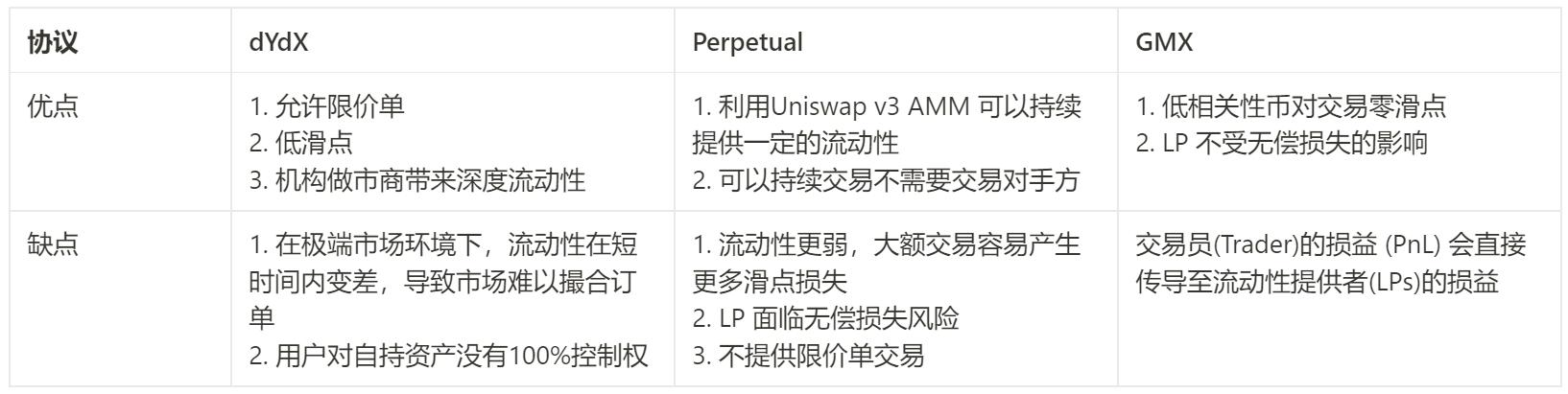

DYDX is built on the L2 protocol StarkWare and uses an order book model for trading, making the trading experience similar to CEX, employing a funding rate mechanism to balance naked positions. The entire trading process is executed off-chain, with only the transfers to and from the margin account occurring on-chain. It introduces professional market makers to enhance liquidity. The entire trading process is a three-party game between market makers and long and short traders.

v2.1 Perp Protocol - vAMM Order Book

The Perpetual Protocol is a decentralized perpetual futures trading protocol built on the L2 protocol Optimism. In the V1 version, the protocol uses a virtual AMM (vAMM) for pricing. The vAMM does not store real assets but facilitates liquidation. When trading, virtual assets are minted in the vAMM. If you open a long position of $100 with 10x leverage, 1000 vUSDC will be minted and deposited into the vAMM. A funding rate mechanism is used to balance naked positions. Since the K value setting in the V1 version greatly affects pricing outcomes, the vAMM was abandoned in the V2 version, adopting the AMM mechanism of Uniswap V3. When users deposit funds to provide liquidity, the funds will be deposited into the treasury, and a set of LPs will be minted in Uniswap V3; when users trade, the margin will be deposited into the treasury, vUSD will be minted, and traded in Uniswap V3. The entire trading process is a game between the LPs of the AMM and both sides of the long and short positions.

v2.2 GMX - Single Liquidity Order Book

GMX is a spot and leveraged trading protocol deployed on the L2 protocol Arbitrum, currently supporting leveraged trading of up to 30x. All trades are countered by the GLP pool. The GLP pool is a multi-token pool composed of BTC, ETH, and other mainstream (large-cap) tokens (mainly stablecoins) in specific weights. Users deposit these tokens and mint GLP tokens to start market making. There is no concept of impermanent loss. Since all trades are countered by the GLP pool, this is a zero-sum game between LPs and traders: the profits or losses of traders will directly cause the price of GLP to increase or decrease. As there is no use of order books and AMM, there is no issue of price slippage, nor is there a need to balance longs and shorts through funding fees. The opening and closing prices are provided by keepers or oracles.

Comparison of the Advantages and Disadvantages of 3 Different Types of Order Books:

Part Three

Uniwhale Exchange

We have seen on-chain trading evolve from simple constant product formulas to concentrated liquidity automated market-making mechanisms, and now to more efficient leveraged trading. All efforts are aimed at solving the following three problems.

- Zero credit risk: fully own and control your assets

- Deeper liquidity: trade at higher leverage with lower slippage costs

- Safer liquidity provision solutions: enabling individual users to participate in liquidity provision, earning trading fees like professional institutions while also reducing impermanent loss.

Uniwhale's design proposal addresses the above issues:

- Relying on our unique oracle aggregator design and strict risk management model, allowing users to trade futures contracts with up to 200x leverage on various mainstream pairs;

- Lower liquidation risk. Uniwhale aggregates prices from multiple oracles to protect positions from pin price impacts;

- Providing deeper liquidity, reducing trading costs and slippage;

- Encouraging any individual user to become a liquidity provider, supplying stablecoin liquidity to the treasury, which not only avoids impermanent loss but also generates passive market-making income;

- Offering NFT-based trading bots, allowing anyone to benefit from liquidation and the profits generated by system trading strategies;

- Achieving complete control for users over their wallets and assets.

Cross-chain liquidity aggregation is something we are working on, and we will launch it soon in the future.

This article comes from Uniwhale Exchange, a multi-chain decentralized derivatives exchange based on oracle prices, supporting futures contracts on various mainstream pairs with up to 200x leverage. Uniwhale Exchange is about to launch a community NFT whitelist event, with all NFTs being free to mint. Feel free to follow us on Twitter and join our Discord to keep an eye on recent activities. NFT holders will also have the opportunity to receive airdrops of the platform's governance tokens.

Risk warning Risk warning

Risk warning Risk warning