Bankless: Shanghai upgrade may spark a wave of liquid staking, which participants will stand out?

Who can overthrow Lido's dominance?

Who can overthrow Lido's dominance?*Written by: Ben Giove, * Bankless

Compiled by: DeFi Dao

If there is a part of DeFi that has become particularly hot during the cooling period, it is the liquid staking market. Yields may be declining across the board, but bullish signals are emerging for Ethereum's future.

Is anyone close to overthrowing Lido's dominance? Who are the rising stars? What does Lido's dominance mean for Ethereum's censorship regime? This article will explore these questions and more.

The Future of Liquid Staking

Image credit: Logan Craig

There will always be a place for a bull market.

While cryptocurrencies may be in a brutal bear market, Ethereum staking remains a long-term growth area.

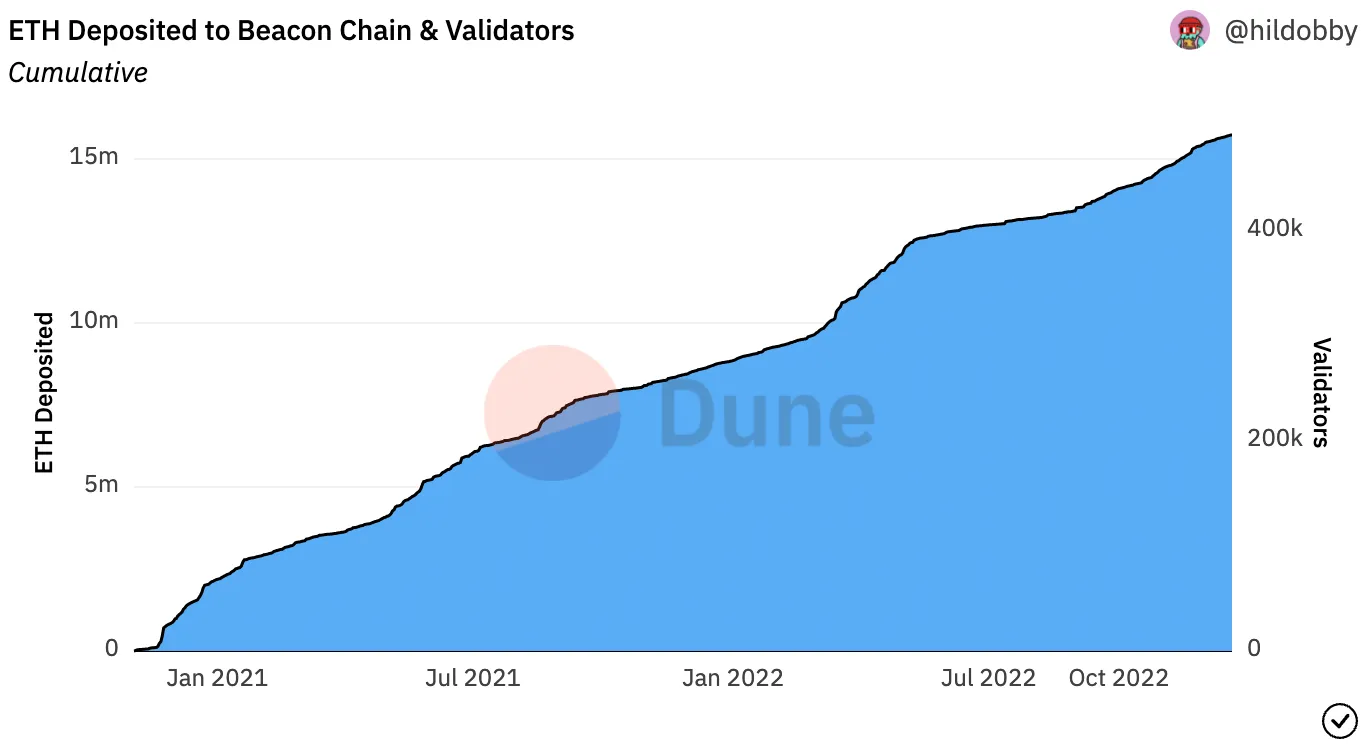

In 2022, the amount of staked ETH surged by 77.9%, with a 14.4% increase since the merge.

ETH Beacon Chain Deposits ------ Source: ++Dune Analytics++

Currently, over 15.7 million ETH are staked, and while this number looks large, it only accounts for 13% of the total supply. This is far below the average staking rate of PoS networks, which is ++61%++.

Due to its highly distributed supply, the staking rate of ETH may never reach this average level, but in any case, the story of Ethereum staking is clearly still in its early stages.

One major catalyst accelerating this staking rate is the Shanghai network upgrade, which will reduce staking risks by allowing users to withdraw their deposits. This could lead to millions of ETH being staked in the months following its expected implementation date of March to April 2023.

The entities most likely to benefit from this wave are liquid staking protocols. These services represent the largest group of stakers, accounting for 32.8% of Beacon Chain deposits.

The industry has found a clear product-market fit by issuing liquid staking derivatives (LSD), which are ERC-20 tokens representing a claim on staked ETH, allowing holders to deploy their assets within DeFi while still earning rewards.

As LSD issuers take a portion of staking rewards as revenue, their business models are influenced by ETH prices and demand for block space, meaning that as the market recovers and on-chain activity returns, their revenue figures will soar with the influx of new staking.

This raises the question… who is best positioned to capitalize on this staking boom? How will the competitive dynamics of staking change after the Shanghai upgrade?

Let’s find those answers below:

The State of Liquid Staking

Lido's dominance is supreme… but how long will it last?

Before we dive deeper into how staking will change and who will capture market share after the Shanghai upgrade, let’s take a look at the current landscape of liquid staking.

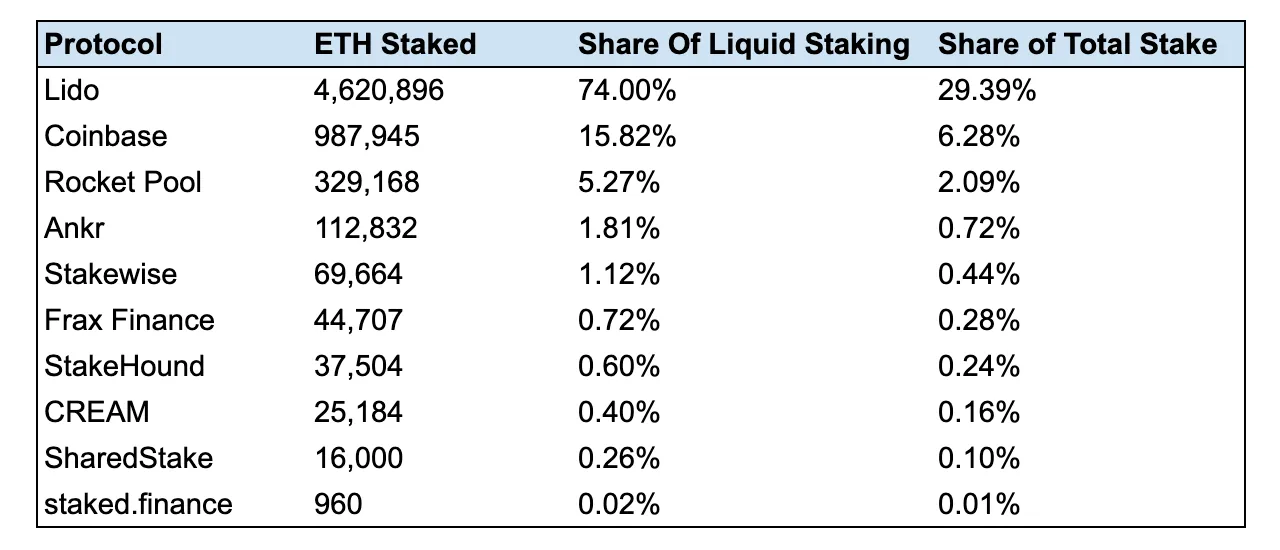

So far, liquid staking has largely been dominated by one player: Lido.

The stETH issuer is the largest entity on the Beacon Chain, holding a 29.4% market share, including 74.0% of the liquid staker share.

Several factors contribute to Lido's dominance.

The protocol benefits from first-mover advantage, as it was the first LSD issuer to launch on a large scale in December 2020. By doing so, they established a critical competitive advantage: deep liquidity.

Before the Shanghai upgrade era, liquidity has been a top priority for stakers, as the secondary market for LSD is the only way to exit positions.

stETH is undoubtedly the most liquid LSD, boasting hundreds of millions in DEX liquidity on Curve, Balancer, and Uniswap. Lido has been able to establish this deep liquidity for stETH through massive incentive programs, having spent $208 million in token incentives from the beginning of 2022 to date.

This helps create a very strong network effect for stETH, as users will want to stake with the most liquid LSD to maximize their exit options, which in turn brings more liquidity to Lido and thus more market share.

This network effect has led to speculation that the protocol will become a monopoly, although the latter is working towards permissionless validation, many point out that Lido could be a centralized vessel for Ethereum, as LDO holders are the only ones who can add/remove node operators.

However, these concerns seem increasingly likely to be unnecessary, as competition for staking has intensified post-merge, revealing cracks in Lido's armor.

Despite having the largest total growth, Lido ranks "only" third in growth rate among major LSD issuers. During this period, the market share of stETH issuers has also shrunk, with liquidity down 3.4% and an overall decline of 1.0%.

Lido's slower growth rate is to be expected, as smaller protocols can grow at a faster pace compared to larger ones. However, when looking at who is attracting new staked ETH deposits post-merge, we can see signs that the protocol's control over liquid staking may be beginning to loosen.

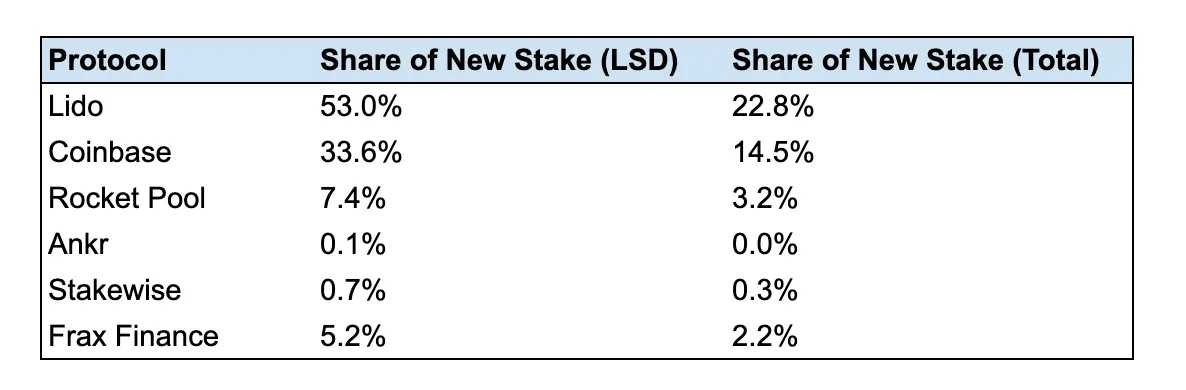

Source: ++Dune Analytics++

While it holds a 29.4% share of all staked ETH, Lido has "only" captured 22.8% of deposits post-merge. Additionally, despite Lido's 74.0% market share in liquid staking, during this period, Lido has attracted 53.0% of deposits to these protocols.

As we can see, this loss of market share can largely be attributed to the growth of Coinbase's cbETH. Since the merge, this CEX-issued LSD has captured 33.6% of the inflow to liquid staking, likely due to its ability to convert its existing staking pool into cbETH. As the largest CEX in the U.S., Coinbase has significant resources at its disposal and is likely to remain competitive in the foreseeable future.

In summary, Lido clearly remains in the lead. However, the diversification of incremental staking suggests that the market may be leaning towards an oligopoly rather than a monopoly.

Yield Commoditization

Another factor that may fuel a liquid staking oligopoly rather than a monopoly is the commoditization of yields.

A common argument for why staking would consolidate is that large pools of capital and professional validators benefit from economies of scale, as they can execute proprietary MEV strategies. By doing so, these entities can generate higher yields relative to smaller stakers, thereby excluding competition and leading to cartelization.

While this may happen to some extent, in the long run, there have been some technical changes at the Ethereum protocol layer and among developers that will democratize staking yields, allowing individual stakers and smaller protocols to generate competitive returns compared to larger competitors.

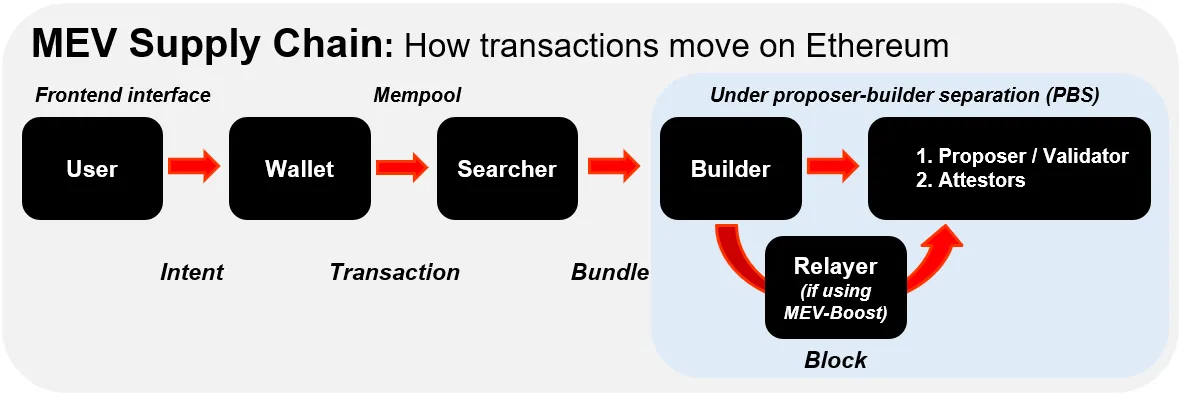

One change is the proposer-builder separation (PBS). PBS aims to separate block production from block validation by creating a new stakeholder called block builders. Block builders are entities that determine which transactions are included in a block, meaning validators do not need to order transactions themselves but only need to select the builder proposing the highest-value block.

Source: Ethereum Censorship Regime Beginner's Guide

By democratizing access to complex MEV, this represents a significant tailwind for yield commoditization. While it will ultimately be reflected at the protocol level, PBS is currently being implemented through relays like MEV-Boost.

The second factor driving yield commoditization is distributed validator technology (DVT). DVT is like a multisig for validators, as it distributes the validator keys across multiple different nodes rather than just one. This, in turn, improves validator uptime and resilience by democratizing failure points and reducing the risk of slashing events. DVT is particularly valuable for individual stakers, who are more likely to encounter maintenance issues that could affect long-term returns. The two main DVT solutions are Obol and SSV, both of which are running on testnets.

Both PBS and DVT are still in their early stages, but once fully implemented, they should help reduce the economies of scale of large staking pools and commoditize the returns of liquid staking providers.

Competitors

As liquidity will become less important after the Shanghai upgrade, and yields may become increasingly commoditized, liquid staking protocols will have to compete on product to attract depositors and validators in the long run.

In other words— the design of the protocol and the LSD itself will actually begin to matter.

There are many product features that will contribute to the success of LSDs:

Validator selection for stakers

Permissionless validation

Slashing protection

LSD capital efficiency

LSD tax efficiency

With that in mind, let’s take a look at a few non-custodial protocols that are ready to seize opportunities in this new competitive environment.

Rocket Pool

Rocket Pool is the second-largest liquid staking provider, holding 5.2% and 2.1% shares in the Beacon Chain and liquid staking deposits, respectively. The protocol's post-merge growth rate is 24.2%, ranking second among all LSD issuers, with total deposits and liquid staking deposits accounting for 3.2% and 7.4%, respectively.

Rocket Pool has been optimized for high decentralization. The protocol was the first to support permissionless validation, as any node operator can validate the network by providing 16 ETH of collateral (½ of a validator) and an RPL bond worth at least 1.6 ETH.

This over-collateralization creates built-in slashing protection for rETH, as the NO bonds will be sold to protect users from slashing events, in which case the validator would lose part of their stake as a penalty for deviating from PoS rules.

Rocket Pool also benefits from tax efficiency, as rETH reflects staking rewards through appreciation (similar to Compound's cTokens) rather than utilizing a rebase model that creates numerous taxable events.

Rocket Pool's main weakness is its low capital efficiency. Capital efficiency has been a significant factor driving the dominance of stETH and cbETH, as each LSD can mint on a 1:1 basis for each underlying ETH deposit (although these LSDs rely on weaker slashing mitigations like insurance).

While the LEB8 proposal will soon lower the collateral requirement for node operators to 8 ETH, this still represents a significant barrier that may make it difficult for the protocol to attract new validators as it scales.

StakeWise

StakeWise is an existing staking protocol that is undergoing a significant transformation.

While it currently uses a dual-token model, the protocol will soon launch StakeWise V3, which will adopt a modular architecture allowing users to stake in separate vaults.

The design of V3 has several clear advantages over single protocols like Lido, Coinbase, and Rocket Pool, such as allowing stakers to choose their validators.

The protocol can also better isolate slashing risks, as losses can be more easily contained within a single vault, while providing further slashing protection through over-collateralization, as users can only mint osETH with the LSD in the protocol, which only constitutes a small portion of their stake.

These features allow validators to join the network permissionlessly with low capital requirements while also providing enhanced customizability for vaults, such as creating whitelists for institutions.

While StakeWise V3 seems disruptive to the overall world order, it faces significant execution risks, as it is essentially launching an entirely new protocol. Additionally, its design introduces more complexity for end-users, as users who choose to "liquidate" their stake rather than simply holding an NFT representing their deposit will have to continuously manage their collateralization ratio to avoid liquidation.

Frax Finance

As the issuer of the FRAX stablecoin, Frax has expanded into liquid staking with the launch of Frax ETH. The protocol's product has grown like weeds, attracting 44,707 ETH deposits while capturing 0.7% of the LSD market.

Frax ETH employs a design similar to StakeWise V2, issuing two tokens to stakers: frxETH, representing their underlying ETH deposits, and sfrxETH, which generates staking rewards. This model provides Frax ETH stakers with higher capital efficiency, allowing them to deploy multiple assets in DeFi to earn yields.

Despite its undeniable growth and significant CVX holdings to attract liquidity on Curve, Frax ETH faces several obstacles that may hinder its ability to gain long-term market share.

One major issue is the inefficiency of the dual-token model, as this disperses liquidity and increases incentive costs for LSD issuers. Additionally, in its current state, Frax ETH is highly centralized, as validators are entirely run by the Frax team, although this may change in the future.

Other Challengers:

Rocket Pool, StakeWise, and Frax are not the only companies seeking to challenge the dominance of Lido and Coinbase.

Many other protocols are set to launch unique products soon, including:

Swell: The first protocol to bring modular, isolated vault design to testnet.

Alluvial: A specialized LSD issuer targeting institutional clients.

Tranchess: A liquid staking protocol based on BSC that is expanding to Ethereum and hopes to incorporate zk-proofs.

Of course, we cannot overlook the "elephant in the room"—Binance. The largest CEX in cryptocurrency seems poised to launch LSD in 2023. Given its influence and resources, its LSD will likely capture a significant market share.

A Rising Tide Lifts (Most) Boats

By enabling withdrawals, the Shanghai upgrade is expected to spark a liquid staking boom and change the dynamics of the industry.

While Lido remains dominant, it faces increasing challenges from CEXs like Coinbase and non-custodial protocols like Rocket Pool, StakeWise, and Swell, which bring product improvements such as enhanced slashing protection, permissionless validation, modularity, and higher tax efficiency.

The disruptive designs of these new challengers mean they should be able to capture market share from Lido and grow at a faster pace in the post-Shanghai upgrade era.

Another factor increasing the chances of success for these solutions is that, due to upgrades and technologies like PBS and DVT, staking providers' yields may become commoditized in the long run.

This is not to say that Lido will not maintain its dominance. The capital efficiency of stETH and the liquidity-based network effect, combined with the potential for withdrawal queue congestion, mean it is unlikely to relinquish its position as market leader.

Additionally, along with other capital-rich LSD issuers like Frax, Coinbase, and potentially Binance, it should be able to leverage their resources to build liquidity-based network effects, even if they are less competitive on product.

In summary, liquid staking seems to be heading towards an oligopoly rather than a monopoly. In this scenario, the post-Shanghai upgrade surge in staking is likely to represent an upward trend that will buoy many "boats" in the short and medium term.

How things will unfold remains to be seen. But it is clearer that stakers, validators, and investors should prepare for a multi-LSD world.

Risk warning

Risk warning Risk warning

Risk warning