DefiLlama 2022 Year-End Review of DeFi: Innovation and Challenges Coexist

DeFi has made significant progress, but the asset class is still relatively small compared to the traditional financial services industry. The total value locked in DeFi ($54 billion) accounts for only a small fraction of the total assets managed by the banking system. However, in the next decade, DeFi will play an important role in the financial sector.

DeFi has made significant progress, but the asset class is still relatively small compared to the traditional financial services industry. The total value locked in DeFi ($54 billion) accounts for only a small fraction of the total assets managed by the banking system. However, in the next decade, DeFi will play an important role in the financial sector.Original Title: 《2022 DeFi Year In Review》

Author: DefiLlama

Compiled by: Qianwen, Biscuit, ChainCatcher

(ChainCatcher made appropriate reductions during compilation)

In 2009, when Satoshi Nakamoto introduced blockchain to the world, cryptocurrency was the first use case. Bitcoin proved that blockchain could be used to demonstrate true ownership of digital currency. More than a decade after Bitcoin's launch, DeFi is proving that blockchain has many other use cases.

With the global economy declining, DeFi has faced severe setbacks this year, but nonetheless, it has come a long way. From an innovative product on Ethereum (MakerDAO created the first stablecoin) to a global industry worth billions of dollars, it has impacted hundreds of thousands of consumers.

This report aims to provide a comprehensive data-driven view of DeFi for those who want to gain a deeper understanding of the industry.

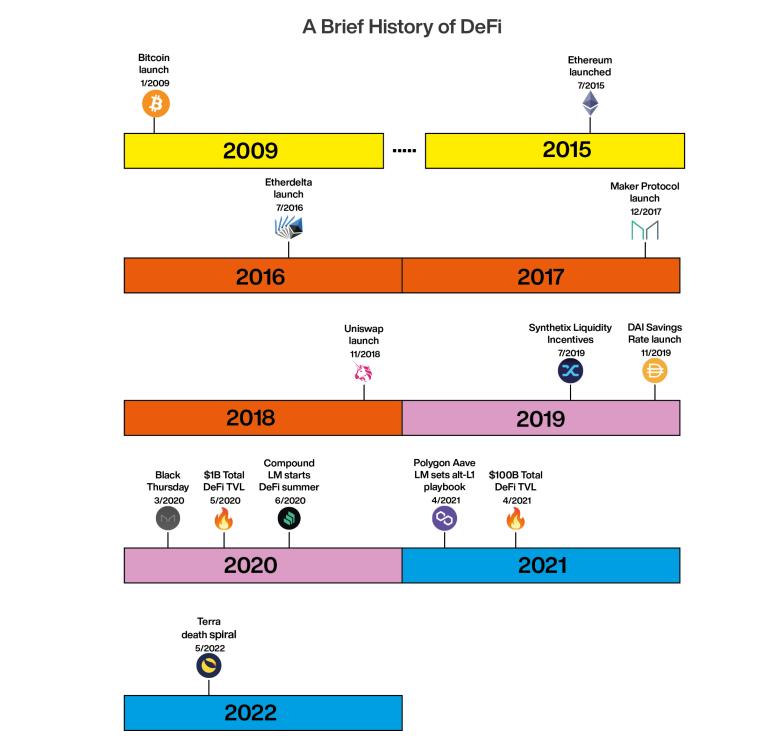

1. DeFi Historical Timeline

2009 : Bitcoin

Bitcoin proved that people could have true ownership of digital financial assets and make international instant payments without using trusted third parties.

2015 : Ethereum

In July 2015, the Ethereum blockchain was launched, introducing smart contracts to cryptocurrency, allowing developers to start building applications and realizing blockchain use cases beyond currency and payments.

2016 : EtherDelta

EtherDelta was the first decentralized exchange launched on Ethereum. The protocol allowed users to trade tokens on-chain without permission. It used an order book model to connect buyers and sellers. In 2017, EtherDelta users lost $1.4 million in a phishing attack, and its founder was charged by the U.S. Securities and Exchange Commission for operating an unregulated securities exchange. Influenced by other factors, the protocol was eventually shut down.

2017 : Maker

Three years after its establishment, Maker was deployed on Ethereum as the first DeFi stablecoin protocol. Maker allows users to provide collateral and mint stablecoins. A stablecoin is a token that ties its value to another asset. The Maker stablecoin DAI tracks the price of the U.S. dollar.

2018 : Uniswap

Uniswap launched in 2018 as one of the earliest decentralized exchanges to use automated market makers instead of order books.

2019 : Synthetix Liquidity Incentives

Synthetix is a derivatives trading protocol that launched a project in July 2019, allowing users who provided collateral to the protocol to earn trading fees and the protocol's native token SNX simultaneously. This technique of incentivizing users to add liquidity to the protocol with tokens would become a key driver of the DeFi boom in 2020.

2020 : Black Thursday

On March 12, 2020, the price of ETH dropped more than 30% in a single day. This sudden drop had a huge impact on the DeFi ecosystem. The Maker protocol failed to quickly liquidate the falling positions, resulting in millions of dollars in losses. The protocol had to create and auction a large number of its native token MKR to cover the losses.

2020 : DeFi Summer

In June 2020, the Compound protocol launched a liquidity mining program that rewarded users who borrowed on the protocol with COMP tokens, leading to a surge in activity on Compound. Other protocols quickly adopted liquidity mining, and the massive incentives caused DeFi activity to grow exponentially. Of course, this state was not sustainable. The value of DeFi tokens plummeted at the end of the year, leading to a decline in the yields of incentive programs.

2021 to Present: Odyssey Era

Since DeFi Summer, the industry has witnessed a burst of innovations and new challenges. We are still in the early stages of this movement. From now on, it will only get crazier.

2. Market Conditions in 2022

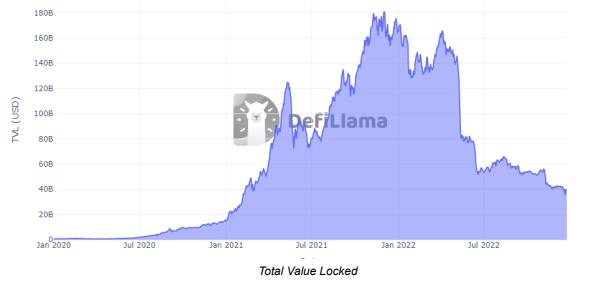

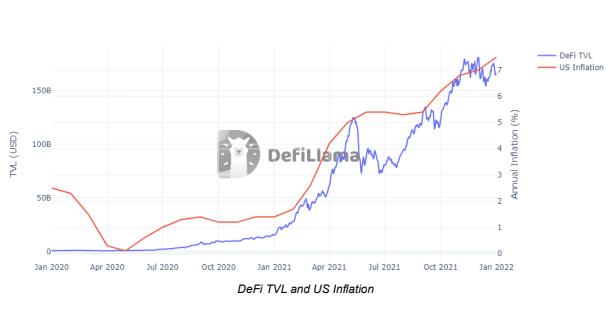

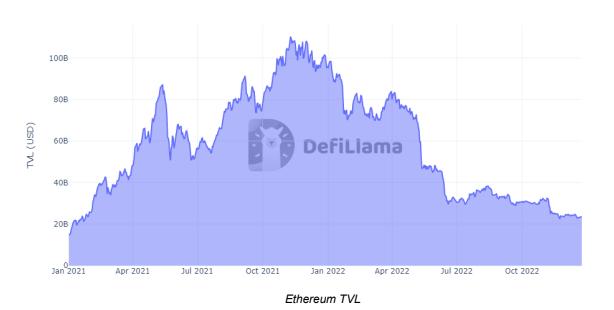

Total Value Locked (TVL) refers to the total value of all assets locked in DeFi products. Since the beginning of this year, the total DeFi TVL has been on a downward trend, but the new floor price is still well above the levels before the last bull market.

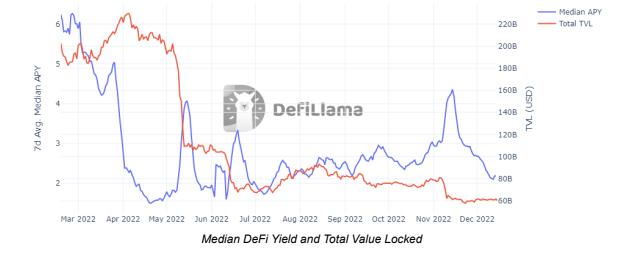

How DeFi Yields Drive DeFi TVL

DeFi TVL is related to DeFi yields, as investors provide capital to DeFi protocols to earn returns. The sources of DeFi yields are diverse. For example, some protocols lend funds to borrowers, charge interest, and pay that interest to liquidity providers.

When yields are high, investors rush to deposit capital into DeFi protocols for lucrative returns. When yields are low, investors shift their funds to other opportunities that offer better returns. As we can see in the chart below, the median DeFi yield plummeted in early 2022, followed closely by a sharp decline in DeFi TVL.

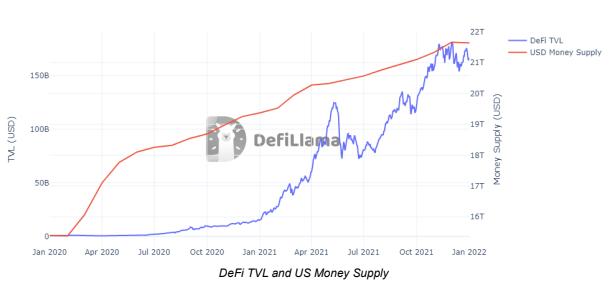

How U.S. Monetary Expansion Drives This Cycle?

During the 2020-2022 cryptocurrency market cycle, the volatility of DeFi yields and the resulting boom and bust of TVL were caused by several interrelated factors. One of the biggest causes of this cycle was the rise in inflation due to the U.S. government's aggressive monetary expansion policies.

Americans are among the largest populations of cryptocurrency holders globally, and their purchasing power is relatively high. Therefore, Americans have a significant influence on the cryptocurrency market.

In 2020, the U.S. government printed money through stimulus measures to respond to the economic recession caused by the COVID-19 pandemic. That year, the money supply increased by 26%. Consumers had more money to spend, and their demand drove up the prices of goods and services. This led to a sharp rise in inflation in 2021.

As inflation rose, mature investors bought risk assets, such as growth stocks and cryptocurrencies, to offset the impact of inflation. The popular saying at the time was, "My cash is depreciating due to inflation. I need to buy assets that appreciate faster than the inflation rate." With the introduction of stimulus measures, retail investors' disposable income increased, so they also spent more on risk assets.

As a result, demand for cryptocurrencies surged, leading to skyrocketing prices of crypto tokens. The rise in crypto asset prices meant that the tokens earned by investors in DeFi protocols became more valuable. Thus, yields were higher. Monetary expansion drove inflation, which in turn drove up crypto token prices and yields.

Capital flowed into DeFi protocols to earn more yields. In this process, the bull market entered full swing. As we see in the chart below, the boom in DeFi TVL closely followed the surge in the money supply and inflation in the U.S.

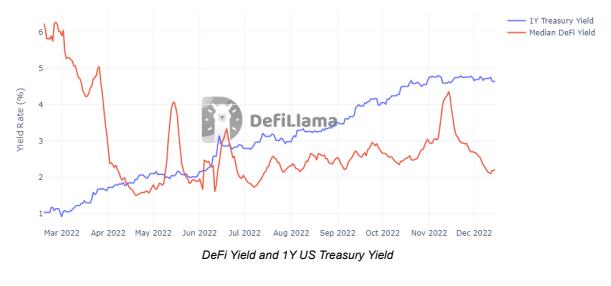

But good times are always short-lived. The inflation rate rose to excessively high levels, forcing the U.S. Federal Reserve to raise interest rates in 2022. When interest rates are high, borrowing costs increase, causing investors and consumers to cut back on spending. High interest rates also lead to rising Treasury yields, prompting investors to shift funds from other assets into Treasuries.

The Fed achieved its goals of reducing spending and combating inflation. But this pushed token prices down, which in turn drove down DeFi yields and TVL.

We can pinpoint the exact moments when traditional market yields surpassed DeFi yields by analyzing historical data. Let's look at how the trade-off between DeFi yields and U.S. Treasury yields played out. The chart below shows that in April 2022, the median DeFi yield fell below the yield of U.S. one-year Treasury bills.

At this point, those (1) harvesting DeFi yields and (2) having the opportunity to access U.S. Treasuries would need to decide whether to reallocate capital or miss out on potential returns. If they could earn more money in relatively risk-free Treasuries, why take risks in DeFi?

Next Chapter

This story does not end here. The alternating bear and bull markets are the norm in the cryptocurrency market. During speculative bubbles, greedy capital floods into cryptocurrencies and DeFi products, taking advantage of ever-rising asset prices and yields. During bear markets, economic activity declines, unsustainable systems collapse, but some of the new capital, talent, and user base that flowed in during the bull market are retained. Ultimately, the industry will be more resilient and stronger than before the crypto boom.

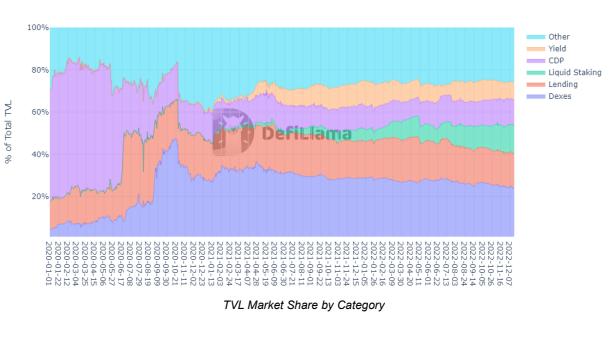

3. Popular DeFi Categories

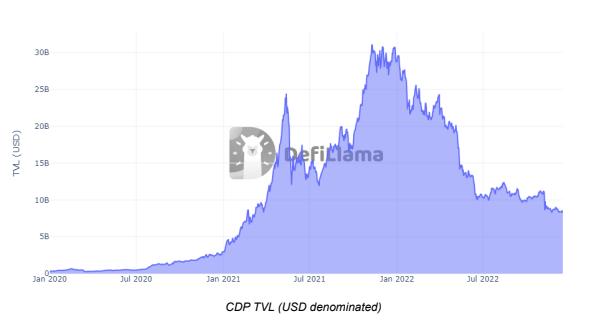

By categorizing DeFi TVL, we can see that at the beginning of 2020, before the last bull market, most of the TVL was in Collateralized Debt Position (CDP) protocols. Using collateral, these CDP protocols mint stablecoins (tokens tied to external assets).

1. CDP

At the beginning of 2020, Maker accounted for most of the CDP TVL because at that time, using cryptocurrency collateral to obtain DAI was the best DeFi option for borrowing cryptocurrency. Another factor contributing to Maker's dominance was the Dai Savings Rate launched in November 2019. This product allowed users to deposit DAI to earn a portion of the interest on Maker loans, becoming the most popular interest-bearing account option in DeFi.

As DeFi Summer began in mid-2020, other categories started to capture more of the CDP TVL market share as many different protocols launched liquidity mining programs. They used token rewards to incentivize users to deposit funds. However, in terms of TVL, by December 2022, Maker remained the largest DeFi protocol, holding 15% of all DeFi TVL.

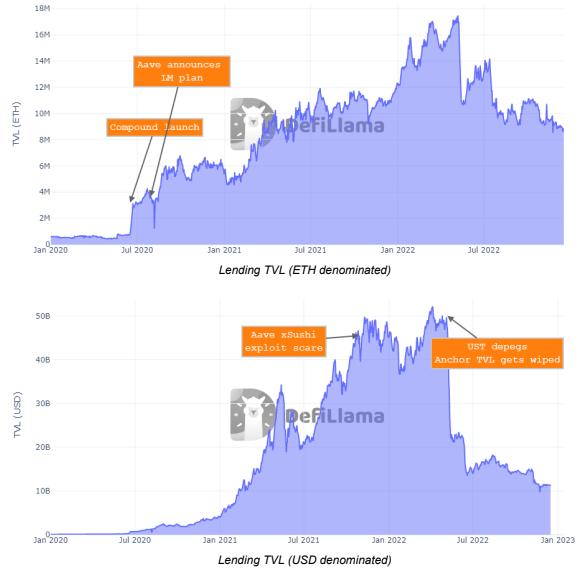

2. Lending

Compound is a popular lending protocol that kicked off liquidity mining with a very successful token incentive program in June 2020. The success of Compound caused the lending TVL market share to soar from 16% to 43% within a week.

Aave is the most popular lending protocol and subsequently launched its own liquidity mining program, solidifying its position as a market leader.

The chart below shows that these events caused a stair-step change in lending TVL in 2020. In 2021, with explosive growth in token prices and lending yields, this category experienced rapid growth.

I present the lending TVL in both ETH and USD, as the token prices rose too quickly in 2021, making it difficult to see the key peaks of 2020 in the USD-denominated chart.

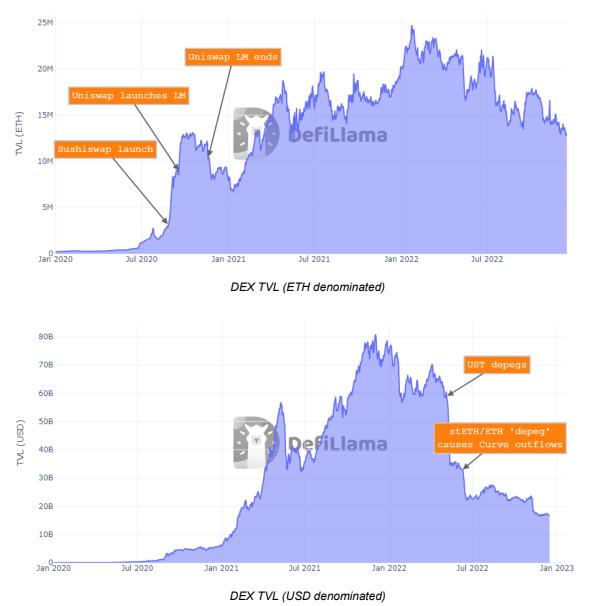

3. DEX

Decentralized exchanges (DEX) were the next category to see a surge in TVL in 2020. SushiSwap launched a large token incentive program in September 2020, attracting many liquidity providers (LPs).

LPs deposit funds into DEX liquidity pools, which help facilitate trading. In exchange, LPs can earn trading fees.

SushiSwap's program attracted a large number of LPs originally from Uniswap, which was the most popular DEX at the time. To combat this "vampire attack," Uniswap launched its own incentives. The introduction of these programs ultimately led to the DEX TVL market share rising from 18% to a peak of 47% within two months.

The chart below shows that in September 2020, as DEX TVL surged, DEX captured a significant amount of trading volume market share from centralized exchanges.

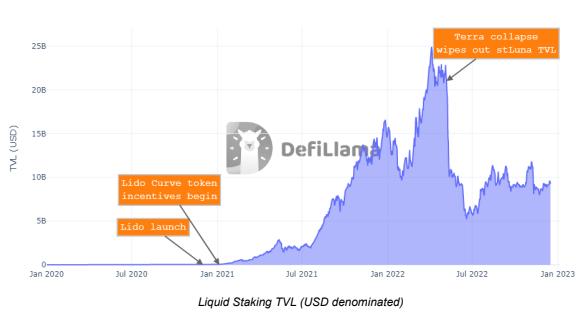

4. Liquid Staking

In 2021 and 2022, liquid staking attracted a significant market share, primarily driven by the Lido protocol.

On blockchains using Proof of Stake (PoS) consensus, validating nodes stake the blockchain's native tokens to gain the right to process transaction blocks and earn block rewards.

Liquid staking protocols allow users to stake the native assets of the blockchain in exchange for staking rewards and tradable tokens representing their staking positions.

In December 2020, Ethereum's Beacon Chain launched. Before the Ethereum main chain transitioned to PoS, the Beacon Chain served as a testing ground for the new PoS consensus logic of Ethereum. In September 2022, the Beacon Chain merged with the original Ethereum Proof of Work (PoW) chain, making the Ethereum mainnet a PoS chain.

Lido launched in December 2020, enabling users to easily earn Ethereum staking rewards without running a validating node. After using Lido, Ethereum users no longer had to choose between DeFi yields and staking yields. They could stake on Lido to earn both yields and then use their stETH earned in DeFi.

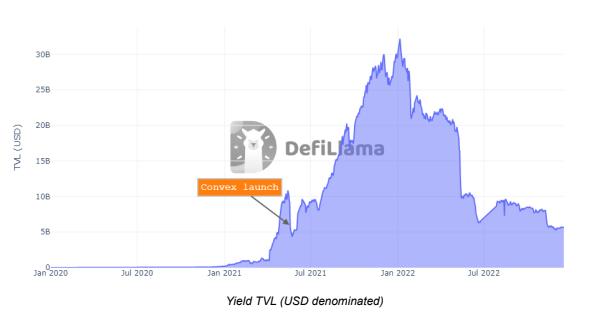

5. Yield

In the past two years, yield protocols have also seen significant growth in TVL. These protocols reward users for staking or providing liquidity on their platforms rather than directly on the target protocol. The growth of TVL in this category has been primarily driven by a series of events known as the "Curve Wars."

Curve is a very popular DEX designed for trading between stablecoins and trading between pegged assets like ETH and stETH. In August 2020, Curve implemented a "vote-escrowed" token system. This system allows users to lock their Curve tokens (CRV) in a smart contract to earn veCRV. veCRV grants holders the right to vote on the parameters of Curve's liquidity pools, most importantly, which pools receive the most CRV incentive rewards for LPs.

Different protocols and communities began competing to accumulate the most veCRV tokens and voting power. Convex—the largest yield protocol—ultimately won this battle and became the largest holder of veCRV. Users who deposited CRV into Convex received crvCVX token rewards (these tokens have the same voting power as veCRV but are tradable, unlike veCRV) and more CRV tokens along with Curve trading fees.

One important driver of Convex's success was their bribery system. Holders of Convex tokens (CVX) could vote to determine Curve token rewards for each veCRV locked in the protocol. Therefore, project teams bribed CVX holders to incentivize the trading pools they desired. As people sought to gain cash flow from the bribes, Convex's TVL grew rapidly. Thus, the total TVL in the yield category was siphoned off.

At the peak in January 2022, Convex held $20 billion of the $32 billion in yield protocols.

4. Public Chains and L2

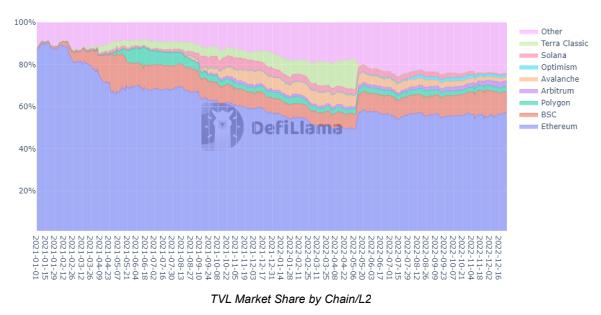

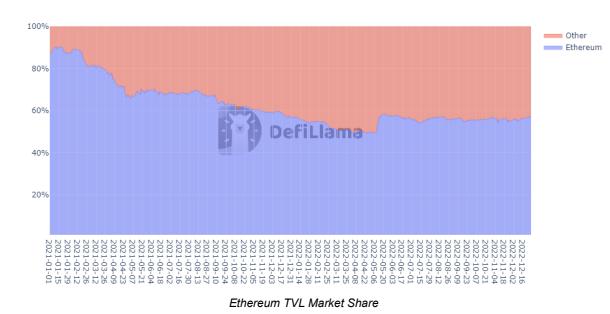

One of the biggest trends in the recent cryptocurrency market cycle has been the adoption of new smart contract chains that offer faster and cheaper alternatives to Ethereum (alt-L1). By categorizing historical TVL data by chain, we see that at the beginning of 2021, most of the DeFi TVL was concentrated on Ethereum, after which Ethereum's dominance began to wane.

1. Ethereum

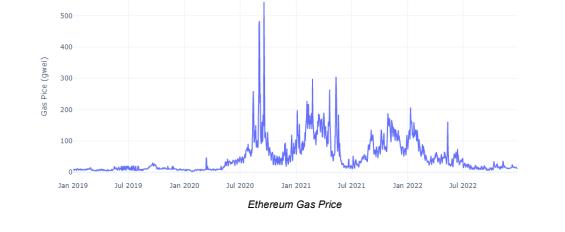

As we see in the chart above, a key driver of the change in market share was the skyrocketing fees on Ethereum during the bull market, which made it inaccessible for most users. These fees are the costs users pay to conduct transactions on the blockchain.

During the peak of high Ethereum fees, the cost of a single ETH transfer could reach as high as $20. As shown in the chart below, there were multiple peaks in fee prices during the DeFi Summer of 2020.

Alt-L1s have significantly lower costs than Ethereum and are faster, as they innovate in design or sacrifice decentralization for performance. These Alt-L1s successfully captured Ethereum's TVL market share, with Ethereum's TVL market share dropping from 87% at the beginning of 2021 to 57% by December 2022.

Of course, there are many factors beyond fees that have contributed to the attention certain alt-L1s have received at different times. We will explore these catalysts in the following sections.

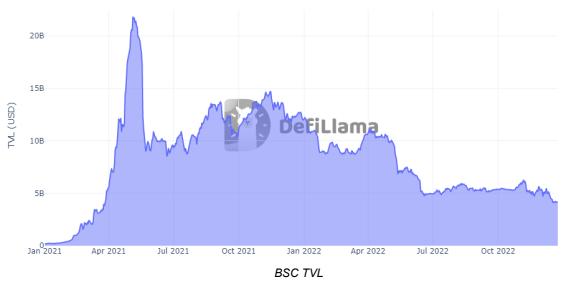

2. Binance Smart Chain

In 2021, Binance Smart Chain saw widespread adoption among retail investors looking to trade STC tokens (tokens with no value other than speculation) on a cheaper and faster chain.

By entering early in the token issuance and quickly hyping it up, profits could be made. Some projects offered huge yields to liquidity providers on DEXs, attracting many, but this temporary loss (impermanent loss) was often not a good strategy.

These drivers led to a significant drop in TVL for PancakeSwap, the most popular exchange on BSC, and Venus, the most popular lending platform on BSC. In May 2021, BSC's TVL market share reached an all-time high of 18.6%.

BNB is the native token of BSC; it is used to pay transaction fees when using the chain. As users rushed to use the network and trade tokens, the price of BNB skyrocketed. This surge made the saying "investing in hot alt-L1s is a good way to make money" popular, driving the subsequent alt-L1 boom.

In 2022, with the collapse of token prices and declining yields, BSC's TVL was impacted. By the end of 2022, its TVL market share was 10%, down 46% from its historical peak. Despite the decline in data, BSC remains the second-largest public chain by TVL.

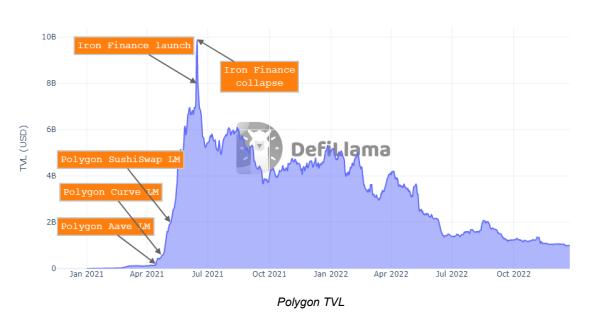

3. Polygon

The Ethereum sidechain Polygon became the next popular blockchain. Its catalyst was the Polygon Foundation starting to collaborate with popular DeFi protocols to deploy their products on Polygon and launch joint liquidity mining programs with these protocols.

The first step in these joint liquidity mining programs included Aave deployed on Polygon. In April 2021, Polygon offered $40 million worth of native token MATIC to lenders and borrowers on Polygon Aave. Users rushed to transfer funds to Polygon to use Aave to earn these rewards. As a result, the TVL of Polygon Aave grew rapidly.

The Polygon Foundation repeated this strategy with many popular protocols, such as Curve and SushiSwap. The price of MATIC tokens soared as the chain gained adoption.

In June 2021, the TVL market share reached an all-time high of 10.3%.

As the market turned bearish, Polygon's TVL declined. By the end of 2022, Polygon's market share was 2.4% (down 77% from its historical peak), making it the fifth-largest public chain by TVL.

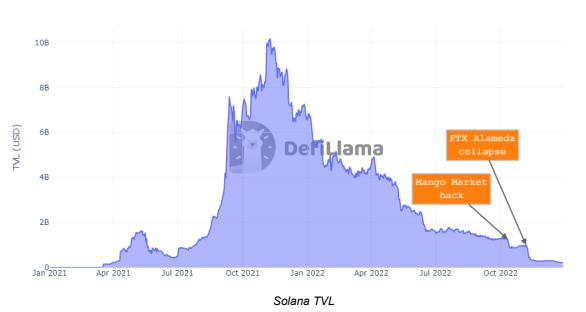

4. Solana

Alt-L1s were later succeeded by Solana. The chain saw a massive increase in TVL in August 2021. Liquidity mining programs, high Ethereum fees, and slow Ethereum transaction speeds accelerated Solana's rise. The chain's TVL market share reached an all-time high of 6% in September 2021.

One unique factor driving Solana's early success was the support from FTX and Alameda. Before its bankruptcy in November 2022, FTX was the second-largest cryptocurrency exchange in the world, and Alameda was one of the most well-known cryptocurrency hedge funds. FTX and Alameda directly influenced Solana's TVL by establishing, investing in, and providing liquidity for applications like Serum DEX. Indirectly, their promotion helped attract capital and talent to Solana.

As Solana began to rise, Ian and Dylan Macalinao concocted a double-counting scheme. They launched 11 protocols under 11 anonymized names and encouraged users to move collateral from one protocol to another. This meant the same collateral was counted multiple times, making it appear that Solana's ecosystem had more TVL than it actually did, making $1 look like $6.

In September 2021, Macalinao's projects accounted for more than half of Solana's TVL. This prompted the DefiLlama team to filter out double-counting when viewing TVL on the website. The chart below shows Solana's TVL and the combined TVL of some protocols controlled by Macalinao (Saber, Sunny, Cashio, Quarry, Arrow, and aSol) without filtering out double-counting.

During the bear market, Solana's TVL market share declined more than that of Polygon and BSC. By the end of 2022, its TVL market share was 0.53%, down 91% from its peak, ranking 11th by TVL.

In addition to poor market conditions, Solana was also negatively impacted by the FTX and Alameda events. In November 2022, it was revealed that $10 billion of FTX customer funds had been fraudulently siphoned to Alameda and used for bad investments. That year, Solana also suffered from three network outages, rendering the blockchain unusable for several days.

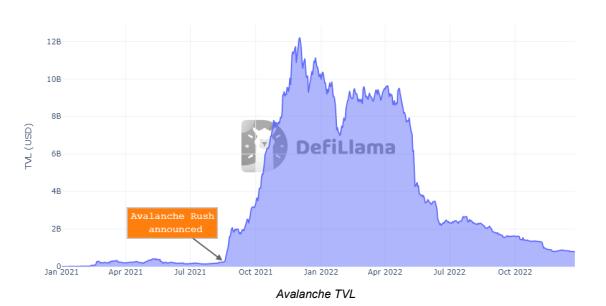

5. Avalanche

Similar to Polygon's promotion strategy, Avalanche ran joint liquidity mining with mainstream protocols to increase user adoption. The Avalanche Rush program allocated $180 million worth of AVAX to incentivize protocols like Aave, Curve, Benqi, and TraderJoe. Within four months, Avalanche's TVL market share peaked at 6.8%.

By December 2022, Avalanche's TVL market share had dropped to 1.9%, down 72% from its peak, currently ranking 6th by TVL.

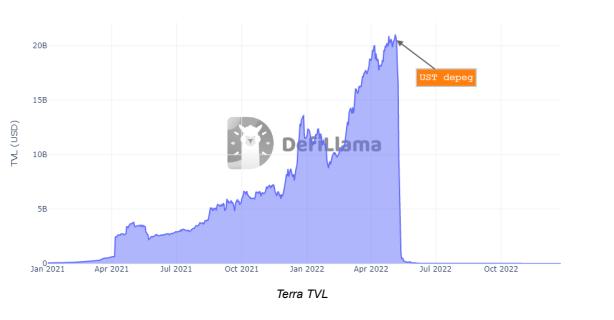

6. Terra

From late 2021 to early 2022, Terra attracted significant attention from cryptocurrency users. The most popular product on Terra was a stablecoin called UST, which was backed by the chain's native token LUNA.

The reason for this growth was that Terraform Labs deployed a large-scale incentive program with the Anchor Protocol. Users could deposit their UST into Anchor to earn a fixed annual yield of 20%. The Anchor Reserve Fund heavily subsidized the yield. A small portion of the yield came from the interest paid by borrowers in the Anchor lending market, as well as the returns from staking the collateral of borrowing users. This incentive program attracted a massive influx of users and capital seeking this incredible fixed savings rate.

Supporting stable assets with unstable endogenous assets (assets from the same system) proved to be unsustainable. Such models had failed many times before, such as Iron Finance, Empty Set Dollar, and Basis Cash (which was later confirmed to be founded by Terra's founder Do Kwon). The model was doomed to fail again.

In early May 2022, UST lost its peg, experiencing massive sell-offs over the weekend, and subsequently failed to recover its $1 peg. UST holders could exchange UST worth less than $1 for LUNA worth $1. As more users redeemed, the supply of LUNA increased, causing its value to drop. In the following week, holders of UST and LUNA raced to reduce their positions. As the price of UST fell, more Luna was minted. Meanwhile, the decline in Luna's price severely undermined confidence in UST. The resulting death spiral drove both tokens' values close to zero.

The collapse of the Terra ecosystem caused DeFi to evaporate $20 billion in TVL. At its peak before the collapse, Terra held a 15% market share.

The collapse of Terra had ripple effects on other crypto projects for the remainder of the year, leading to the bankruptcy of several centralized crypto projects such as Celsius and Voyager. These crypto projects were poorly managed and unprepared for the economic downturn.

7. Optimism and Arbitrum

Arbitrum and Optimism are Rollups networks built on Ethereum, also known as L2. These networks help scale the blockchain and support faster and cheaper transactions by offloading some computations off-chain while keeping part of the data for each transaction on-chain. Arbitrum and Optimism saw an increase in TVL market share in 2022.

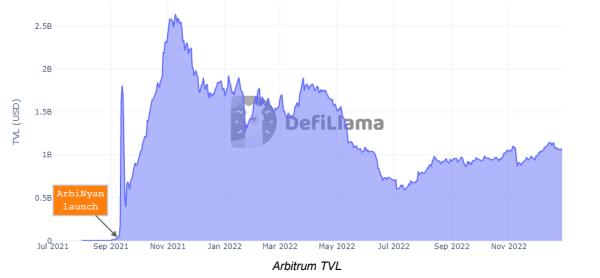

Arbitrum

When Arbitrum launched in September 2021, its TVL surged significantly, reaching a peak of $2.6 billion within two months. Initially, capital flowed into Arbitrum to participate in meme coin mining projects like ArbiNyan, whose TVL soared to $1.5 billion the day before the collapse. A fork project of ArbiNyan, Carbon, similarly reached a peak of $300 million in TVL for a brief period. However, this capital subsequently shifted to popular DeFi protocols like Curve and Abracadabra.

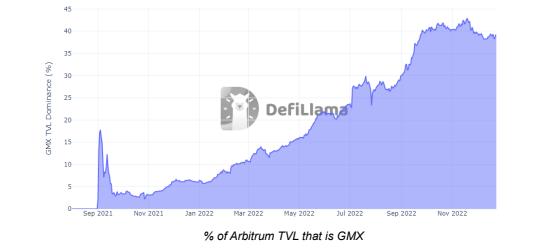

Over time, Arbitrum's TVL has largely been driven by GMX, a decentralized spot and derivatives exchange. Arbitrum currently does not have a token, so the influx of funds into the network may be due to participants seeking to earn future airdrop tokens by engaging with the ecosystem.

By the end of 2022, Arbitrum's TVL market share was 2.6%, ranking 4th by TVL.

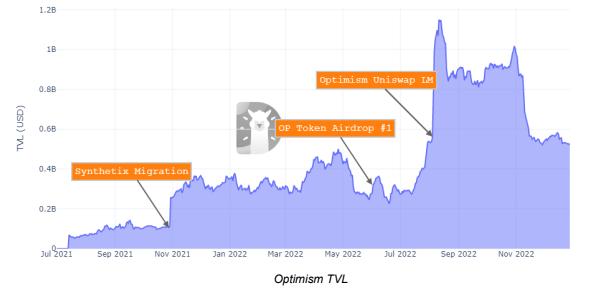

Optimism

When Optimism launched in July, its TVL growth rate was slower. The Optimism Foundation intentionally limited early growth rates so they could test the network in a controlled manner. Until December 2021, developers had to be whitelisted to deploy applications on Optimism.

In the early days, the introduction of the Synthetix protocol played a significant role in TVL growth. Synthetix was the first large DeFi protocol deployed on L2, and they built a bridge to make it easy for users to migrate their SNX tokens to Optimism.

Similar to Arbitrum, Optimism's TVL was also influenced by users' expectations of its token airdrop. In May 2022, Optimism airdropped OP tokens to users. Since then, the Optimism Collective community has begun running joint liquidity mining programs for different protocols to stimulate growth in adoption.

By the end of 2022, Optimism's TVL market share was 1.3%, ranking 7th by TVL.

8. Looking Ahead

Now that the crypto market has entered a bear phase, the narrative around mainstream public chains seems to have cooled, and many metrics from the previous round of excellent public chains have plummeted from historical highs. New public chains are trying to leverage the same narrative, such as Aptos, but there hasn't been a frenzy like previous public chains.

Despite clearly losing market share, Ethereum remains the market leader in DeFi with high profit margins, and its L2s are rapidly climbing the rankings. For the foreseeable future, the Ethereum ecosystem seems set to remain the primary habitat for DeFi.

5. Review of Key Events

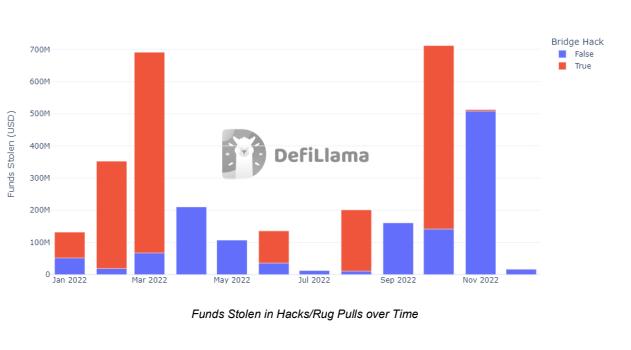

- Hacks

2022 was the worst year for cryptocurrency hacks. $3.2 billion was stolen in hacks. The most attractive targets for hackers were cross-chain bridges, accounting for 59% of the stolen funds in 2022.

Security is one of the biggest obstacles to the development and adoption of DeFi. Users can only enjoy the benefits of DeFi when smart contracts have no exploitable vulnerabilities.

2. Stablecoins

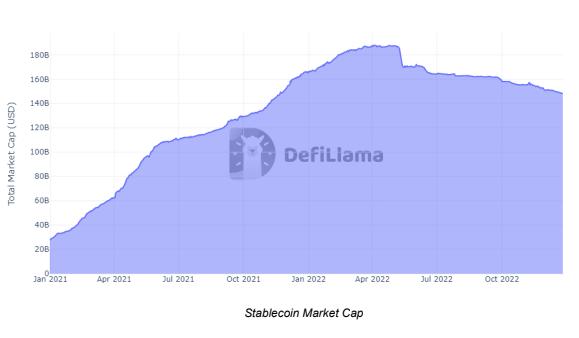

In 2022, the total market capitalization of stablecoins reached a historic high of $187.5 billion.

During the bear market, the decline in stablecoin market capitalization was much milder than that of other DeFi protocols, even including the total losses from UST. The market capitalization of stablecoins has fallen to $148 billion, down 21% from its historical peak.

Stablecoins remain the most popular use case for transitioning real-world assets to blockchain assets.

USDT is currently the market leader, accounting for 47% of the stablecoin market capitalization.

3. The Merge

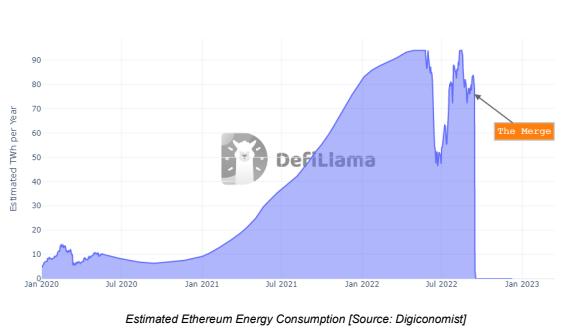

After five years of research and development, on September 15, the Ethereum blockchain transitioned from Proof of Work (PoW) to Proof of Stake (PoS).

In the old consensus system PoW, Ethereum miners competed to solve mathematical puzzles. The winning miner in each block could earn ETH rewards.

In the new consensus system PoS, Ethereum validating nodes stake ETH, and a node is randomly selected to process new blocks in each time slot. The selected node receives block rewards. If a node behaves maliciously, its stake is slashed. This system is more energy-efficient and supports many future innovations listed in Ethereum's roadmap. It is estimated that Ethereum's merge reduced global energy consumption by 0.2%.

The chart below shows that Ethereum's energy consumption is expected to decrease by 99.99% after the merge.

Now, the vast majority of DeFi activities are taking place on chains protected by PoS. This shift marks a significant step forward in terms of DeFi's carbon footprint and security.

6. Predictions for Emerging Trends

Here are some growth trends that members of the DefiLlama team are focusing on in the new year:

DeFi protocols will leverage their core functionalities to allow participants to choose more risk costs to improve capital efficiency. Two examples are Uniswapv3 and Aave v3, which have high LTVs on related assets.

- Oxngmi: Boss llama

Utilizing ZK proofs and privacy technologies. A killer app should be a seamless Web3 entry point that integrates smooth DeFi protocols and prioritizes mobile support.

- Strobie: Deferred Liquidation

I'm watching the trend towards privacy-focused DeFi (e.g., Aztec). I also believe the use of stablecoins will continue to expand, as they are currently primarily used by residents of Europe and the U.S. Aggregators may be a killer app.

- Vrotend: Yield Adapters PRs and Meta DEX Aggregators

DeFi needs real yields. People will find it easier to understand where their yields come from. A killer app will be the Bloomberg of cryptocurrency.

- Bentura: DEX

I'm observing trading volumes on DEXs, which continue to grow, and analyzing which dApps are growing in this category will be interesting. Excellent DEXs are key to the growth and competition of any public chain. A killer app could be a consistently profitable P2E game.

- realShaman: Blockchain Verification

I'm interested in using blockchain for verification. A few years ago, people were interested in supply chain cryptocurrencies, but there has been no progress in this area. I believe verification applications are a truly useful area for blockchain. A killer app will be a swish wallet where users can send transactions directly from dApps without needing a browser extension like Metamask.

- wavnebruce: NFT and Oracle API

Protocols providing delta-neutral yield strategies will become a major trend. A killer app will be privacy-focused wallets, more convenient entry and exit channels, mobile payments, etc.

- slasher: Yield Dashboards

Privacy will be an important trend. I'm excited about Aztec, even though this track has not yet emerged. Perhaps the adoption of Ethereum L2 will increase. Additionally, I'm looking forward to a leading cross-chain DEX/aggregator emerging.

- ulvsses:TVL Changes

After the collapse of CeFi lending platforms, it will be interesting to develop a product that meets users' demand for "safe" yields. There is a lot of untapped potential in crypto social media. If we rely solely on apps like "TikTok to make money," it indicates that the industry has not progressed.

- cocoahmology: Stablecoins and Cross-Chain Bridges

Uncollateralized loans are interesting, and I am eager to see how different projects address the uncollateralized dilemma. A killer app will be lending based on user assets.

- nemusona:Llamapay, Llamalend and Waifus

Governance minimization and "code and law" protocols will see an upward trend, as these protocols can better withstand the upcoming regulatory pressure. A killer app will be a capital-efficient insurance protocol.

- intern:TVL Changes

The trend I am most interested in is the adoption rate of prediction markets. A killer app will be atomic swap protocols and aggregated cross-chain protocols.

- mintdart:Universal Frontend

I believe there are still many interesting areas to observe in crypto gaming. A killer app will be an integrated multi-chain dApp that combines DEX, yield farming, privacy cross-chain bridges, subscriptions, and flow payments.

- Oxtawa: DEX Trading Volume, Revenue, Fees

A killer app will be a system that allows users to easily obtain collateralized loans without KYC.

- Oxgnek:TVL Adapters

I am excited to see improvements in DeFi security. Currently, security is viewed as an event-based practice (testing -> peer review -> auditing), while excellent crypto teams will view it as a continuous process: static analysis and fuzz testing of every piece of code added to the codebase, using automated threat response monitoring systems, and hiring security specialists.

- Kofi: Hacks and Trend Contracts

Conclusion

DeFi has made significant progress, but the asset class remains small compared to the traditional financial services industry. The total value locked in DeFi ($54 billion) is only a small fraction of the total assets managed by the banking system.

I believe that in the next decade, DeFi will occupy an important position in finance. In 2023, we will continue to move towards this goal:

- More DeFi teams will build products accessible to ordinary users. This will attract more mainstream assets to the category and further normalize DeFi's position as a global financial participant.

- Centralized cryptocurrency exchanges (Coinbase, Binance, Kraken, etc.) will recognize the importance of proving their on-chain reserves and transparently allowing users to access DeFi services. The bridges they build will make it easier for those outside the crypto ecosystem to interact with DeFi for the first time.

- DeFi activity will thrive on Ethereum L2, bringing a cheap, fast, and secure DeFi experience to more people.

The DeFi industry in 2022 was filled with innovation, challenges, and breakthroughs.

2023 will be even more exciting.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles