2022 Cryptocurrency Industry Investment and Financing Report: Insights into Popular Tracks and Investment Trends from Capital Flow

From the perspective of investment and financing in 2022, infrastructure (including sub-sectors such as Layer 1, Layer 2, developer platforms, wallets, middleware, etc.), NFTs, Web3 social entertainment, and on-chain data analysis are relatively popular fields, and it is highly likely that this trend will continue in 2023.

From the perspective of investment and financing in 2022, infrastructure (including sub-sectors such as Layer 1, Layer 2, developer platforms, wallets, middleware, etc.), NFTs, Web3 social entertainment, and on-chain data analysis are relatively popular fields, and it is highly likely that this trend will continue in 2023.Authors: flowie, Xiangxiang, ChainCatcher

Table of Contents:

- Overview of the Crypto Market in 2022

- Fundraising Situation of Crypto Venture Capital in 2022

- Project Financing Situation in 2022

- Analysis of financing numbers and amounts across various sectors

- Top 10 projects by annual financing amount

- Active Investors in 2022

- Investment Institutions

- Individual Investors

- Conclusion

1. Overview of the Crypto Market in 2022

"Crypto winter" was the keyword for 2022, and this chill was transmitted step by step.

In the macro environment, global inflation in 2022, monetary tightening policies from various central banks, and aggressive interest rate hikes from the Federal Reserve led to price responses across all asset classes: stock markets, currency markets, and government bonds worldwide saw significant declines; the yield curve on 2-year/10-year U.S. Treasury bonds continued to invert at record levels; the tech-heavy Nasdaq index fell continuously.

The crypto industry attracted an overly speculative crowd, with leverage levels higher than in traditional industries, making the deleveraging process more intense against the backdrop of tightening global capital.

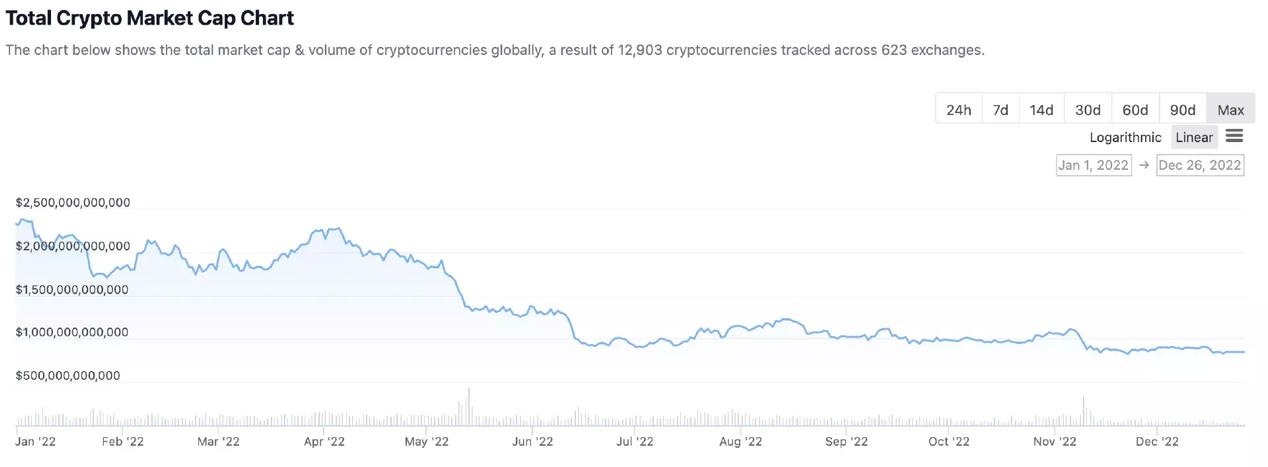

First, the secondary market experienced a crash, confirming that the crypto market had entered a deep bear phase. The total market capitalization of crypto erased about $2 trillion from its peak in November 2021, falling below $1 trillion by the end of 2022. Cryptocurrency prices showed a clear downward trend throughout 2022, with Bitcoin's price plummeting over 60%.

Source link: https://www.coingecko.com/en/global-charts

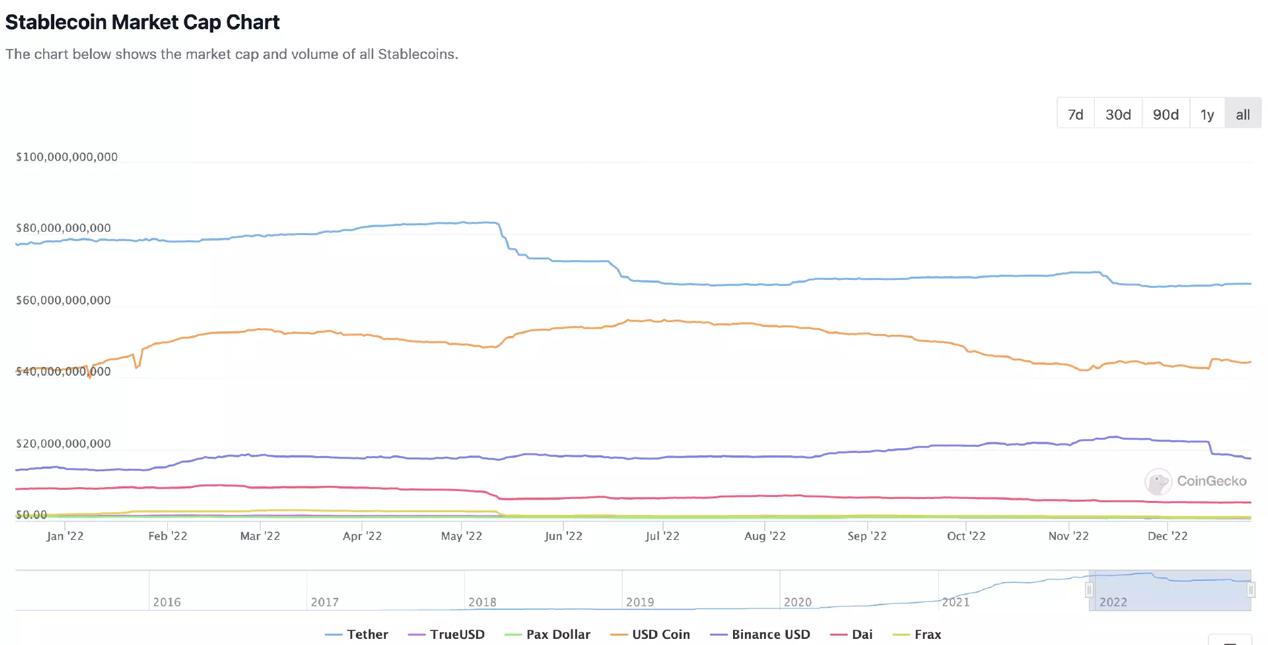

As the cornerstone of the crypto industry, the total supply of stablecoins peaked at $161.5 billion in March 2022 but subsequently saw over $14.3 billion in large-scale redemptions.

Source link: https://www.coingecko.com/en/global-charts

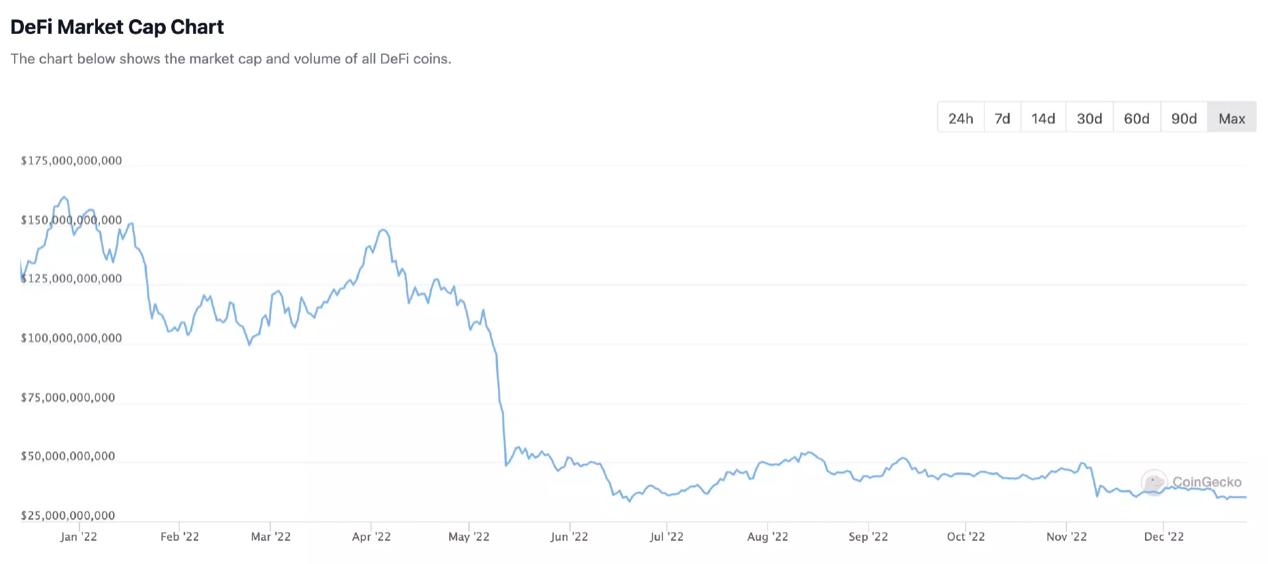

In the DeFi sector, according to Defillama data, the TVL of DeFi fell from $171 billion in January 2022 to a low of $50 billion in October 2022, a decline of nearly 75%. With a series of events like Terra's collapse, DeFi's TVL experienced two significant drops, accelerating the bear market.

Source link: https://www.coingecko.com/en/global-charts

In the NFT sector, as the market continued to cool, NFT trading volumes remained sluggish. The extremely high trading volume in May 2022 was primarily due to the release of Otherdeed in Otherside, which induced FOMO among users. Throughout 2022, the total market capitalization of NFTs fell from about $35 billion to $21 billion, a decline of over 40%.

Secondly, against the backdrop of a continuously bearish secondary market, numerous negative risk events occurred in the crypto market in 2022. We witnessed several crypto giants fall like dominoes: Terra, Three Arrows Capital, Voyager Digital, Celsius, FTX, BlockFi… and this list continues to grow.

The decline in the macro environment, the deep bear market in the secondary market, and multiple black swan events rapidly eroded confidence in the crypto investment and financing market. The Luna collapse in mid-2022 became an important "watershed" for the investment and financing market. The entire venture capital market in the first half of this year basically continued or even surpassed the bullish performance of 2021, but the heat in the second half plummeted, with both institutional fundraising and the rhythm of the investment and financing market slowing down, and this downward trend may continue into the first half of 2023.

What was the investment rhythm of the crypto investment and financing market in 2022, and where did the funds flow? Based on data from crypto data platform Rootdata and others, ChainCatcher compiled the fundraising data of the crypto market in 2022, reviewing the overall situation of the crypto investment and financing market, including overall investment and financing data, distribution of segmented investment and financing tracks, and the most active investors.

2. Fundraising Situation of Crypto Venture Capital in 2022

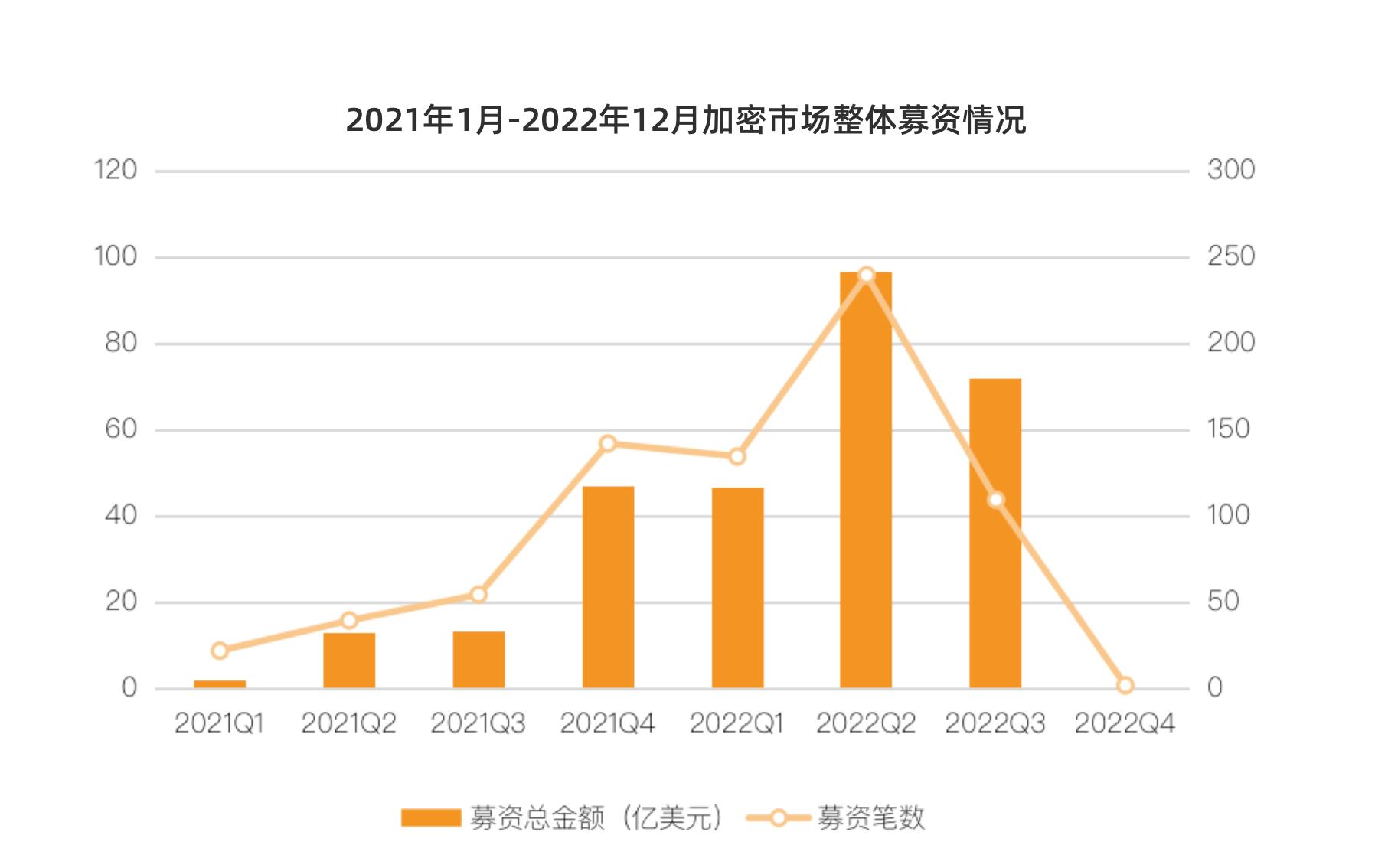

In terms of fundraising, the bullish performance of the crypto market in 2021 led to significant capital entering the crypto market in early 2022. In the first two quarters of 2022, fundraising in the crypto venture capital market saw substantial increases, with 54 fundraising events in Q1 2022, a 500% increase year-on-year compared to 2021, and a total fundraising amount of $11.723 billion, a year-on-year increase of 2245%. In Q2 2022, there were 96 fundraising events, a 500% increase year-on-year, with a total amount of $24.193 billion, a year-on-year increase of 635.12%.

However, with the arrival of the bear market and a series of explosive events like Luna and Three Arrows Capital, the performance of investment institutions was also questioned, and the strong fundraising momentum was quickly curtailed. In Q3 2022, the number of fundraising events and total amounts saw a cliff-like decline, with the number of events dropping by 54.16% compared to Q2, and the total amount decreasing by 25.43%.

By the end of 2022, the FTX black swan event occurred, with top investment funds in the crypto field, such as Sequoia Capital, Paradigm, Temasek, and Multicoin, writing down hundreds of millions of dollars to zero, severely damaging the reputation of crypto investment institutions, and upstream capital allocation to the crypto market became rare. Fundraising activities in Q4 basically came to a halt, with only one fundraising event totaling $150 million.

Overall, despite the market downturn, investment institutions still secured more "ammunition" in 2022, completing 195 fundraising events, an 87.5% year-on-year increase, with a total fundraising scale of $54.105 billion, a year-on-year increase of 186%.

Data source: Messari

From the specific investment and financing data, it can be seen that with the significant pullback in the crypto market and the impact of multiple explosive events, the investment rhythm of the crypto investment and financing market gradually slowed from the first half to the second half of the year, and it is estimated that investment will continue to be cautious in 2023.

3. Project Financing Situation in 2022

This report statistics 1528 investment and financing events across 9 categories in DeFi, CeFi, infrastructure, gaming, NFT, social entertainment, DAO, tools & information services, and others in 2022.

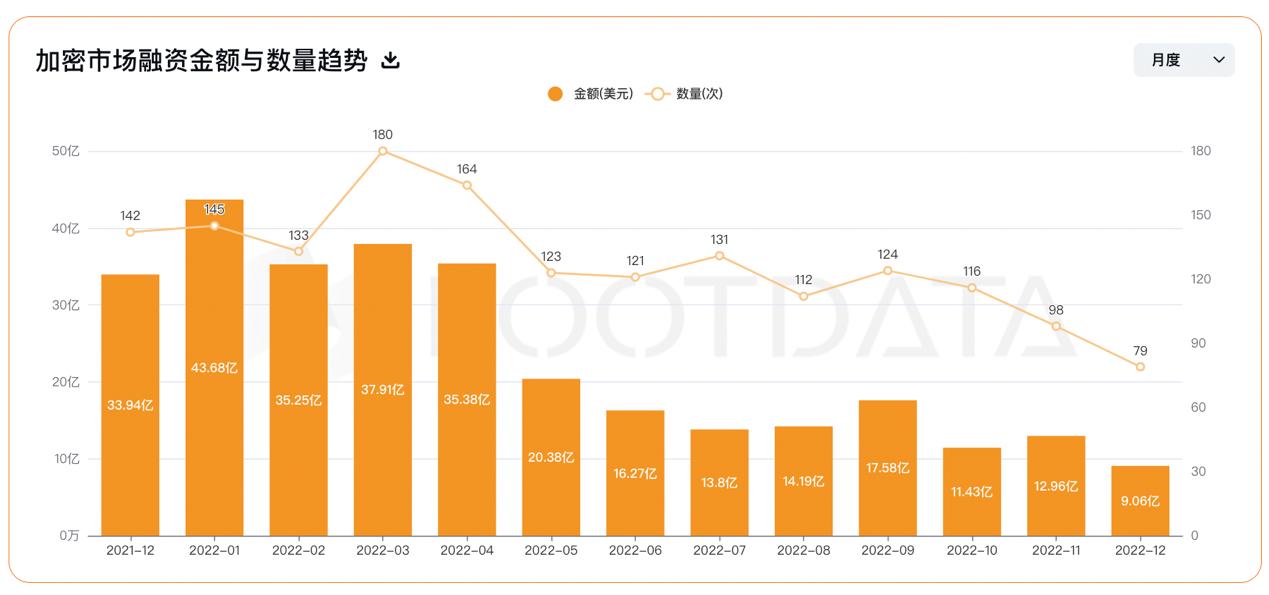

The cumulative disclosed financing amount in the crypto industry in 2022 reached $26.77 billion, with 1528 financing events, a decrease of 4.5% and an increase of 28% compared to 2021, respectively. There were 57 merger and acquisition events that year, of which 10 disclosed acquisition amounts, totaling $1.64 billion.

In Q1 2022, the crypto investment and financing market maintained a total financing amount of $11.686 billion, continuing the record of over $10 billion in single-quarter financing since Q4 2021, with 405 financing events, achieving five consecutive months of positive growth or flat records in both total amount and number of events, marking an unprecedented golden era of crypto investment.

However, starting from Q2 2022, with the Federal Reserve's continued interest rate hikes and frequent explosive events like the Luna collapse, the crypto investment market began to decline sharply. The total financing amounts in Q2, Q3, and Q4 of 2022 were $7.204 billion, $4.558 billion, and $3.346 billion, respectively, with the number of financing events being 358, 329, and 254, showing significant reductions in both total amounts and institutional participation.

Data source: Rootdata

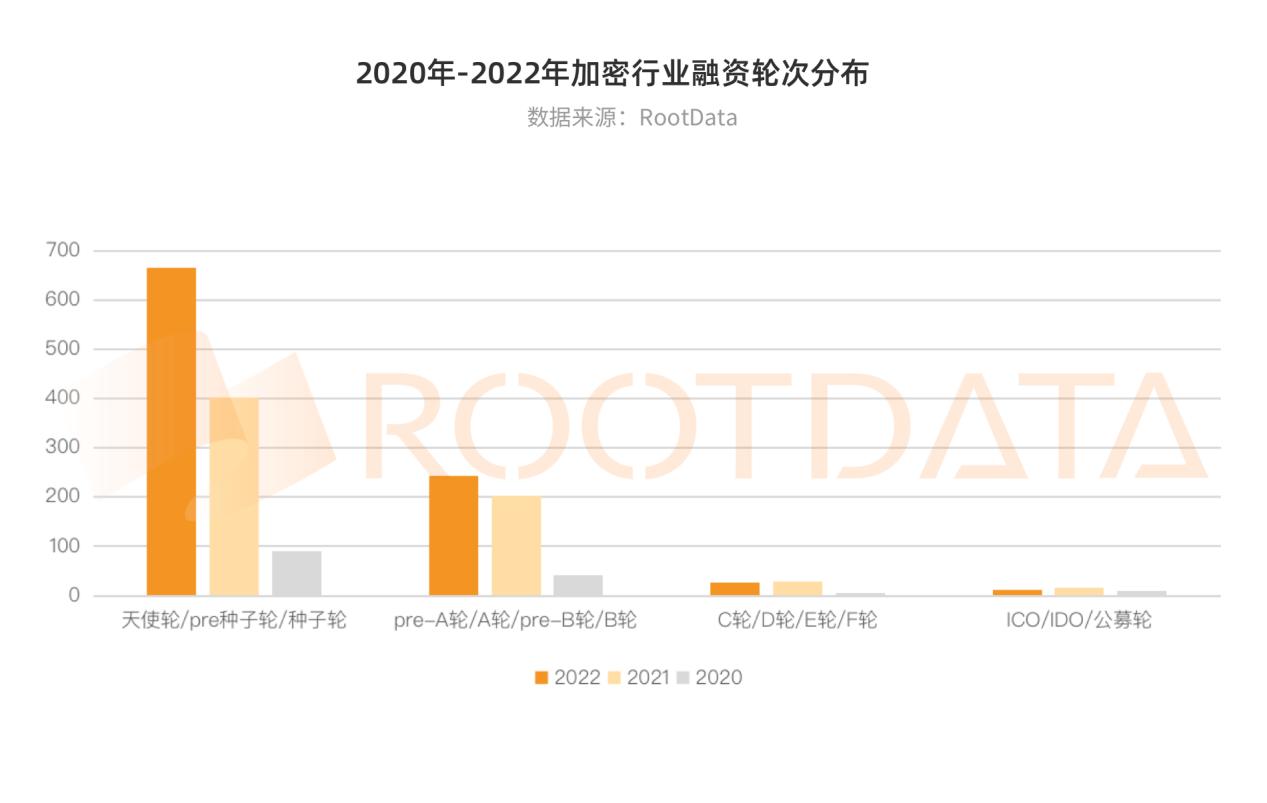

From the segmented financing rounds, it can be seen that the distribution of financing rounds for crypto projects in 2022 was similar to that of 2020 and 2021, still concentrated in early stages such as angel rounds, pre-seed rounds, and seed rounds. This is most evident in the gaming, NFT, and DeFi sectors, where projects receiving early financing accounted for 68%, 65%, and 63%, respectively, indicating that they are still in a vigorous development stage, and the industry landscape is far from solidified.

Where did the funds from crypto venture capital primarily flow in 2022? What changes occurred compared to 2021?

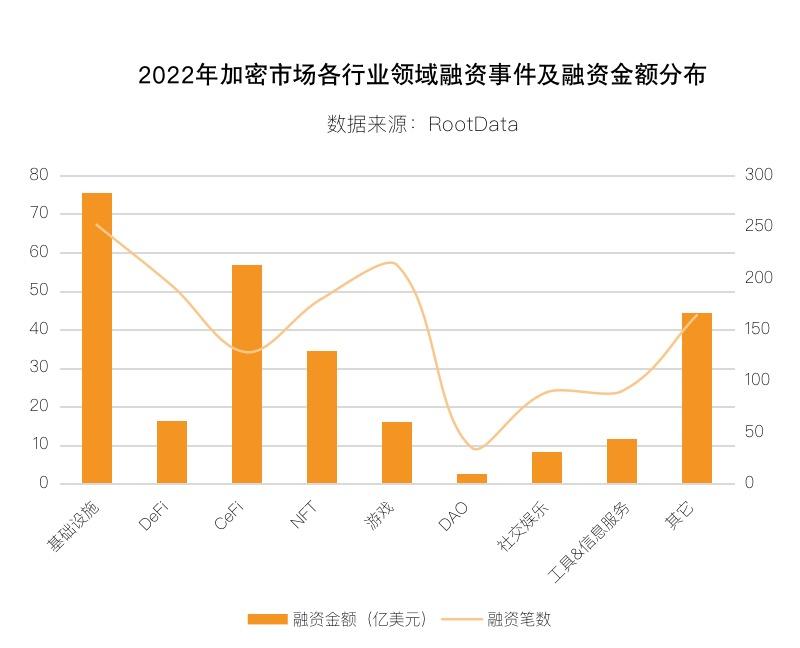

From the distribution of investment and financing fields, the top three sectors by number of financing events in 2022 were infrastructure (252 events), gaming (213 events), and DeFi (193 events), accounting for 16.49%, 13.94%, and 12.63% of total financing events, respectively; the top three sectors by total financing amount were infrastructure ($7.565 billion), CeFi ($5.68 billion), and NFT ($3.456 billion), accounting for 28.20%, 21.22%, and 12.92% of total financing scale, respectively.

Compared to 2021, the total financing amounts and total number of investment and financing events in 2022 saw significant growth, with most growth rates exceeding 50%. Sectors that saw increases in both financing numbers and amounts included infrastructure, NFT, social entertainment, and tools & information services, with financing numbers increasing by 19.4%, 68.2%, 134.2%, and 125%, respectively, and financing amounts increasing by 82.3%, 181.32%, 265.2%, and 78.5%.

In addition, there were 63 financing events in 2022 where the amount exceeded $100 million, with multiple projects securing hundreds of millions in funding through consecutive financing rounds. Among them, Animoca Brands raised a total of $544 million across three rounds, Amber raised $500 million across two rounds, NEAR Protocol raised $500 million across two rounds, Aptos raised $350 million across two disclosed rounds, and Sui raised $315 million across two rounds.

In 2022, the most favored projects by top funds and large financing amounts were primarily concentrated in the infrastructure sector (including sub-sectors such as Layer 1, Layer 2, developer platforms, wallets, middleware, etc.), with 19 financing events exceeding $100 million, mainly concentrated in public chain and scaling sectors. Aside from the previous round of new public chain narratives, Polygon raised $450 million at the beginning of the year, and many new entrants in this sector completed significant financing, such as Aptos raising $350 million, Sui raising $200 million, and zkSync raising $200 million.

Despite the downturn in 2022, the NFT sector, which gained popularity in 2021, still maintained a strong momentum. There were 12 financing events in the NFT sector that exceeded $100 million, mainly concentrated in mid-to-late stage leading projects. Notable financing projects included Animoca Brands ($544 million across three rounds), Yuga Labs ($450 million), Opensea ($350 million), and Dapper Labs ($305 million).

In the social entertainment and tools & information services sectors, both the number of financing events and the amount of financing saw significant increases. Social entertainment (often seen as one of the content entry points for Web3 user growth) saw topics like "decentralized social," "Web3 social networks," and "Web3 music" become hot topics in 2022, with new concepts like soul binding emerging. Following Elon Musk's high-profile acquisition of Twitter, discussions around Web3 social surged again. However, as this sector is still in its early development stage and the direction remains somewhat unclear, no high-growth platforms have emerged. In 2022, the social entertainment sector mainly saw investments in seed rounds, totaling 56 events, with few large financings. A typical financing event was the decentralized social protocol Farcaster, which completed a $30 million round led by a16z.

In the tools & information services sector, projects mainly concentrated in the seed round stage, with a total of 53 events. The sub-sector related to crypto data & analysis was the most active, with 36 financing events, accounting for 36.73% of the total financing in this field. Projects exceeding $100 million included blockchain data analysis company Chainalysis ($170 million) and crypto asset software company Lukka ($110 million). Additionally, with several leading projects experiencing crises this year, tools or solutions related to crypto project taxation and accounting have attracted significant investment interest, with well-known institutions like Tiger Global and Sequoia Capital entering the space.

While the number of financing events in the CeFi, DAO, and gaming sectors saw slight increases, the total financing amounts significantly decreased, with year-on-year reductions of 54.2%, 17.2%, and 46%, respectively. In the DeFi sector, both the number of financing events and the total amounts saw slight declines, with year-on-year reductions of 27.2% and 9.3%.

In the CeFi sector, prior to the mid-year crises of Luna and Celsius, leading players like FTX and Amber completed multiple large financings. However, by Q3, this momentum had largely dissipated, with significant declines in both the number of financing events and amounts. Following FTX's collapse, many related CeFi institutions faced crises, and Q4 financing in the CeFi sector remained sluggish. The maturity of the CeFi sector is relatively high, with 38 early-stage projects and 33 A-round projects, showing a relatively balanced ratio. The most active vertical in the CeFi sector was exchanges, with other popular areas including payments, market making, savings, and asset management.

Although CeFi faced setbacks, leading DeFi protocols like Uniswap and dYdX performed well during various collapse events, leading the market to generally believe that DeFi would usher in a new wave of dividends. However, in 2022, there were no major innovative protocols emerging in the DeFi sector, and the primary market did not see a new wave of financing heat, with only Uniswap completing a financing event exceeding $100 million, raising $165 million in October 2022.

Compared to the steady development of NFTs, blockchain gaming, which also surged in 2021, saw a clear weakening in momentum in 2022. With leading projects like Axie and STEPN facing severe setbacks and scrutiny, no new concept games similar to Axie or STEPN emerged. Although there was some investment interest around AAA blockchain games, NFT games, and metaverse concepts, the significant decline in total financing amounts indicates that investment institutions are being more cautious in this field.

In 2021, the DAO was viewed as the next hot theme following NFTs, but in 2022, it not only failed to explode as expected but also hardly made any "splash," remaining relatively quiet in terms of market discussions, project progress, and primary market investment and financing performance.

1. Detailed Financing Data for Each Sub-sector:

Infrastructure

The infrastructure sector includes Layer 1, Layer 2, developer platforms, wallets, middleware, and many other fields. In 2022, there were 252 investment and financing events in the infrastructure sector, raising a total of $7.55 billion, ranking first among all sectors. The number of financing events increased by 19.4% year-on-year, and the total amount increased by 82.3%. In terms of financing rounds, there were 115 early-stage projects and 48 A-round projects in the infrastructure sector in 2022.

DeFi

The DeFi sector includes DEX, lending, asset management, yield farming, stablecoins, etc. In 2022, there were 193 investment and financing events in the DeFi sector, raising a total of $1.65 billion. The number of financing events decreased by 27.2% year-on-year, and the total amount decreased by 9.3%. The majority of projects receiving investment in DeFi were in the seed round stage, totaling 110 events.

CeFi

In the CeFi sector, there were 128 investment and financing events in 2022, raising a total of $5.68 billion, ranking second among all sectors. The number of financing events increased by 7.6% year-on-year, while the total amount decreased by 54.2% year-on-year.

NFT

In the NFT sector, there were 180 investment and financing events in 2022, raising $3.46 billion. The number of financing events increased by 68.2% year-on-year, and the total amount increased by 181.3% year-on-year. Since 2021, both the total financing amount and the number of events in the NFT sector have generally maintained an upward trend. The majority of projects receiving investment in NFTs were in the seed round stage, totaling 100 events.

Gaming

In the gaming sector, there were 213 investment and financing events in 2022, raising a total of $1.61 billion. The number of financing events increased by 80.5% year-on-year, while the total amount decreased by 46.0% year-on-year. Most projects receiving investment in the gaming sector were in the seed round, totaling 113 events.

DAO

In the DAO sector, there were 35 investment and financing events in 2022, raising a total of $270 million. The number of financing events increased by 25% year-on-year, while the total amount decreased by 17.2% year-on-year. The majority of projects receiving investment in the DAO sector were in the seed round stage, totaling 12 events.

Social Entertainment

In the social entertainment sector, there were 89 investment and financing events in 2022, raising a total of $840 million. The number of financing events increased by 134.2% year-on-year, while the total amount increased by 265.2% year-on-year. Most projects receiving investment in social entertainment were in the seed round stage, totaling 56 events.

Tools & Information Services

In the tools & information services sector, there were 90 investment and financing events in 2022, raising a total of $1.16 billion, ranking first among all sectors. The number of financing events increased by 125% year-on-year, while the total amount increased by 78.5% year-on-year. Most projects receiving investment in this sector were in the seed round stage, totaling 53 events.

Others

In other sectors, there were 164 investment and financing events in 2022, raising a total of $4.43 billion, ranking third among all sectors. The number of financing events increased by 51.9% year-on-year, while the total amount increased by 2.5% year-on-year. Most projects receiving investment in this sector were in the seed round stage, totaling 61 events.

2. Top 10 Financing Projects of 2022:

Source: Rootdata

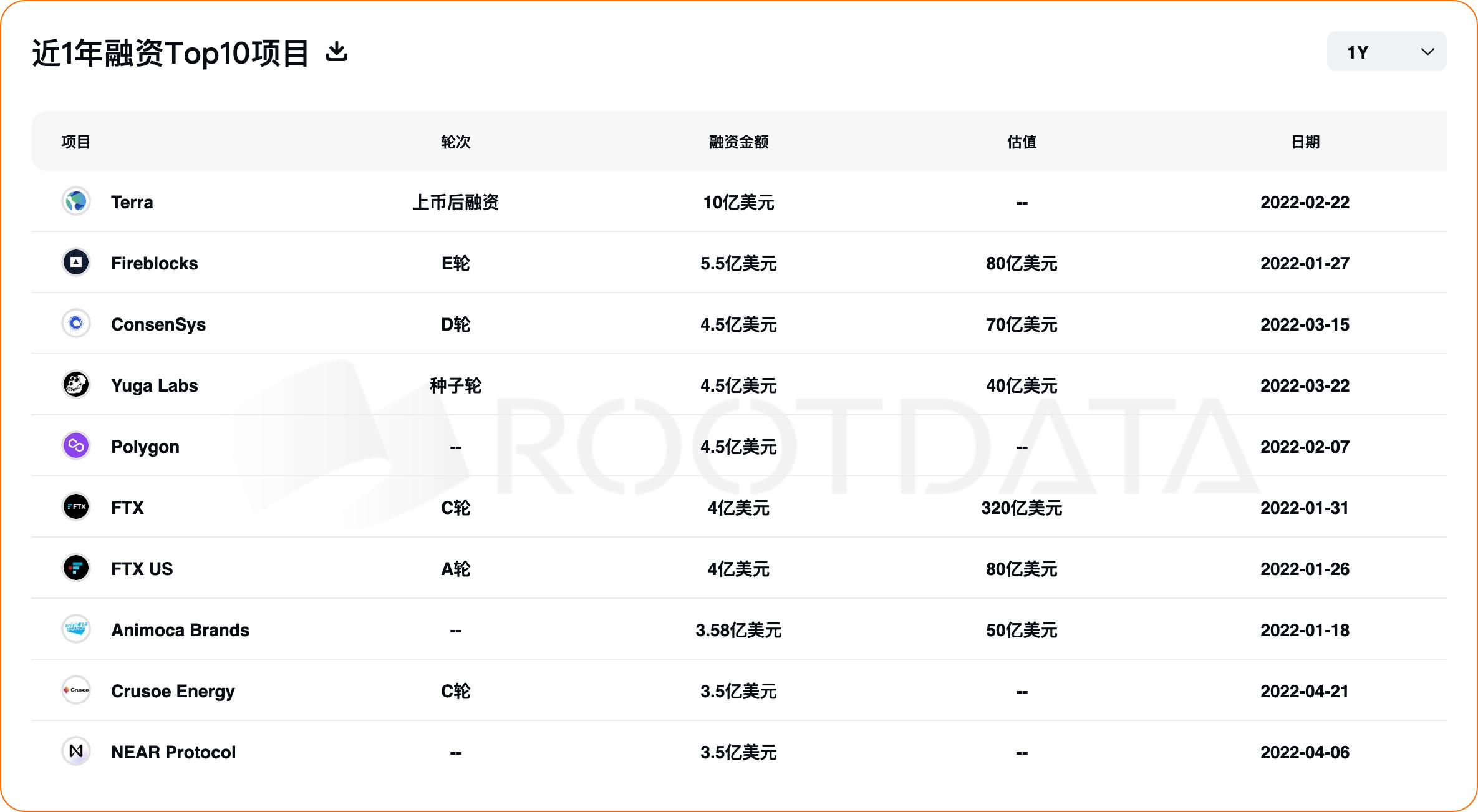

The top 10 projects with the highest single financing amounts in the crypto sector in 2022 were the public chain Terra ($1 billion), digital asset custody platform Fireblocks ($550 million), Ethereum infrastructure development company ConsenSys ($450 million), BAYC developer Yuga Labs ($450 million), Ethereum scaling project Polygon ($450 million), crypto exchange FTX ($400 million), crypto exchange FTX US ($400 million), Web3 gaming software company and venture capital firm Animoca Brands ($358 million), green mining company Crusoe Energy ($350 million), and public chain NEAR Protocol ($350 million), and Flow developer Dapper Labs ($305 million).

It is lamentable that among the top ten projects by financing amount, Terra, FTX, and FTX US all experienced collapses this year, causing a huge impact on the entire crypto market. This highlights the significant bubbles and risk hazards created during the previous bull market.

4. Active Investors in 2022

For top funds with ample capital, compared to being swept up by FOMO in the bull market, the gradual deflation of bubbles and return to fundamentals in the crypto market during the bear market may present a better opportunity for investment as project valuations return to rational levels.

In terms of the activity level of investment institutions based on the number of investments, the top ten investment institutions in 2022 were Coinbase Ventures, Animoca Brands, Shima Capital, GSR, Spartan Group, Dragonfly, Solana Ventures, Alameda Research, a16z, and Jump Crypto.

Source: Rootdata

Among them, those with over 100 investments include Coinbase Ventures (119) and Animoca Brands (118). Coinbase Ventures significantly accelerated its investment pace in 2022, with a total of 259 investments since 2018, and in 2022 alone, it made 119 investments, accounting for nearly half of the total number of investments. In terms of investment distribution, Coinbase Ventures mainly focused on infrastructure and DeFi sectors, with investment proportions of 30% and 24%, respectively. Among the projects it participated in that exceeded $100 million, there were only five: Yuga Labs ($200 million), Sui ($300 million), Aptos and Layer Zero ($135 million), and Gnosis Safe ($100 million).

Animoca Brands had 118 investments in 2022, with gaming remaining its core focus, accounting for over 60% of all its investment projects. Among the projects with financing exceeding $100 million, there were six: Yuga Labs ($450 million), Polygon ($450 million), football media platform OneFootball ($300 million), Web3 gaming service provider Immutable ($200 million), cricket NFT platform Rario ($120 million), and cross-chain infrastructure LayerZero ($135 million).

Investment institutions with over 50 investments included Shima Capital (88), GSR (76), Spartan Group (63), Dragonfly (61), Alameda Research (59), Solana Ventures (59), a16z (56), and Jump Crypto (55).

Among them, the top venture capital firm a16z, with a larger asset scale, had a relatively balanced distribution of investment fields, with not much difference in the number of investments across various sectors, mainly distributed in infrastructure, NFT, and gaming. In terms of investment stages, a16z preferred more mature crypto startups, making a total of 57 investments in 2022, with 18 projects exceeding $100 million, including Yuga Labs, Aptos, Sui, LayerZero, and centralized wireless hotspot network Helium, accounting for nearly 30% of the total number of investments, far exceeding Coinbase Ventures and Animoca Brands. Many of the large projects it participated in were in the public chain and scaling sectors.

Shima Capital, a crypto-native fund established in 2021, had 86 investments, mainly focusing on early-stage projects, with nearly 80% of its investments in 2022 being in projects under $10 million, and it did not invest in any projects exceeding $100 million. GSR, a crypto market maker established in 2013, had 76 investments, mostly in early to mid-stage projects, with nearly 64% of its investments in 2022 being in projects under $10 million. It participated in two projects exceeding $100 million, including Gnosis Safe ($100 million) and Terra (which raised $1 billion post-IPO before its collapse in 2022).

Dragonfly, another crypto-native fund established in 2018, focused on DeFi, infrastructure, and CeFi sectors, with a preference for early-stage investments. In 2022, it participated in three projects exceeding $100 million: Ethereum scaling solution zkSync/Matter Labs ($200 million), NEAR Protocol (raising $350 million and $100 million across two rounds), and Polygon ($450 million).

Solana Ventures, primarily investing in the Solana ecosystem, focused on DeFi and gaming sectors, with a preference for early-stage investments. In 2022, it participated in 73% of its investments being in projects under $10 million. Jump Crypto participated in projects exceeding $100 million in 2022, including Sui ($300 million), Aptos ($150 million), and crypto exchange Kucoin ($150 million).

Overall, top funds favored injecting capital into infrastructure, DeFi, and gaming sectors, especially public chain and scaling sectors, which have become tracks that top funds cannot afford to miss.

In addition to investment institutions, individual investors in the primary market of the crypto industry cannot be overlooked. In 2022, angel investors with over 10 investments included Balaji Srinivasan (44), Sandeep Nailwal (37), Sebastien Borget (14), Santiago Roel Santos (14), Jaynti Kanani (14), Stani Kulechov (11), and Ryan Selkis (11).

Source: Rootdata

Among them, the most active angel investor Balaji Srinivasan** made** 44 investments. Balaji Srinivasan was the CTO of Coinbase and a general partner at a16z, and he is an early investor in many successful tech companies and crypto protocols, including Alchemy, Ava Labs, Bitcoin, Cameo, Chainlink, Clubhouse, Dapper Labs, Ethereum, Instadapp, NEAR Protocol, OnDeck, Opensea, Solana, Soylent, Superhuman, Synthesis, and Zora. Balaji Srinivasan has also founded three companies, Earn.com, Counsyl, and Teleport, which were acquired by Coinbase, Myriad, and Topia, respectively. Additionally, Balaji Srinivasan is the proponent of the concept of "network states."

In 2022, Balaji Srinivasan primarily invested in tools & information services, infrastructure, and DAO sectors, with five projects in his investment portfolio exceeding $20 million, including modular blockchain Celestia ($50 million), Web3 data index Nxyz ($40 million), decentralized social platform Farcaster ($30 million), and decentralized trading platform Hashflow ($26 million).

Sandeep Nailwal, co-founder of Polygon, was the second most active individual investor, making 37 investments in 2022, primarily in infrastructure and NFT sectors. Among his investment projects, those exceeding $20 million included interoperability protocol LayerZero ($135 million), African Web3 super app Jambo ($30 million), and crypto banking and payment company Zamp ($20 million).

5. Conclusion

Overall, the market bubbles and risk hazards accumulated during the 2021 bull market were punctured in 2022. With the successive bankruptcies of crypto giants, many mainstream crypto investment institutions paid a heavy price, and the rhythm of investment and financing in the crypto market rapidly slowed down, with funds likely favoring long-term valuable crypto "new infrastructure."

From the investment and financing situation in 2022, infrastructure (including sub-sectors such as Layer 1, Layer 2, developer platforms, wallets, middleware, etc.), NFT, Web3 social entertainment, and data analysis were relatively hot fields, likely to maintain their popularity in 2023.

It is worth mentioning that in 2022, industries related to Bitcoin payment technology and the Lightning Network are gaining attention. Although the financing amounts are far less than those of infrastructure and NFT projects, they are still worth continuous attention in 2023.

So, how do other authoritative institutions predict the trends for 2023?

As usual, a16z, Messari, Pantera, and other analysis and venture capital institutions have made their predictions for investment trends in 2023. Among them, a16z mentioned that projects related to mobile blockchain, multi-party computation, and zk technology will continue to receive attention. Messari expects that crypto infrastructure will maintain the heat of 2022, and due to the frequent on-chain security incidents in 2022, security audit companies will continue to receive financing. Messari is bearish on the overly hyped GameFi sector.

Ryan Selkis, the founder of Messari, leans towards decentralized social (DeSoc). Paul Veradittakit, a partner at Pantera Capital, mentioned zk technology and on-chain data analysis in his predictions. Zhao Changpeng also noted that infrastructure and data tools will continue to develop, and non-custodial and multi-chain wallets will rise.

Risk warning

Risk warning Risk warning

Risk warning