Analyzing Wash Trading in the NFT Market from Data

What does the real NFT market look like after removing wash trading? How much of the data in the NFT market is false prosperity? The author of this article has designed a data dashboard "https://dune.com/zoez17/the-real-nft-marketplace-landscap" to present the authentic NFT trading market after filtering out the fakes, providing a value judgment tool for Web3 users and investors' decision-making.

What does the real NFT market look like after removing wash trading? How much of the data in the NFT market is false prosperity? The author of this article has designed a data dashboard "https://dune.com/zoez17/the-real-nft-marketplace-landscap" to present the authentic NFT trading market after filtering out the fakes, providing a value judgment tool for Web3 users and investors' decision-making.Author: Zoe, Puzzle Ventures(@zoezts)

Thanks to Jerry (@JerryZZQ), Eric (@ericych2), Sim (@simbraska), and hildobby (@hildobby). Feel free to reach out to me for discussions (zk, AI/ML, data, etc): zoey@puzzle.ventures

TL; DR

Wash trading is a form of fraudulent trading that creates misleading artificial activity in the market, affecting the value judgments of institutional and individual investors.

The overall weekly trading volume of the NFT market has never exceeded $2 billion, contrary to the $5.6 billion seen on paper.

OpenSea's pricing power in the NFT market may be under challenge.

The main sources of wash trading in the market in 2022 were LooksRare and X2Y2, due to their trading incentive policies, with X2Y2 performing better in reality.

Individual NFT investments also need to consider the wash trading situation of specific projects to avoid artificially inflated trading volumes or prices; the author has created a relevant data query method, in the data dashboard collector detector section, to support decision-making.

The data supporting this article comes from:

The Real NFT Marketplace Landscape: https://dune.com/zoez17/the-real-nft-marketplace-landscap

Wash Trade Filter Study: https://dune.com/zoez17/wash-trade-filter-test

- What is Wash Trading?

- Motivations and Results of Wash Trading in the NFT Market

- Distinguishing the Real from the Fake: The True NFT Market

- How to Filter Out Wash Trading in the Market

Characteristics of Wash Trading: Analyzing Ideas and Practices

How to Identify and Filter Wash Trading Data: A Data-Driven Approach - Other Indicators Worth Noting

- References

1. What is Wash Trading?

Wash trading, also known as wash sales, is a form of fraudulent trading. In wash trading, it appears that there are genuine buy and sell transactions of assets, but the intent is not to establish a real market position, nor is there an intention to execute genuine transactions that face market risk or price competition. (References: CME[1] and CFTC[2] definitions)

For various purposes, certain traders, project parties, or the market itself create misleading artificial activity through wash trading.

The two main components of wash trading include:

Result: Traders buy and sell the same instruments for accounts that have the same or common beneficial ownership at the same or similar prices.

Intent: If there is evidence that the trades were pre-arranged, or if there is evidence that one or more parties knew or should have known that the trades would result in wash trading, then wash trading intent can be inferred from this evidence.

Wash trading is regulated in traditional financial securities markets, such as the rules (Rule 534)[3] of all exchanges under CME and Section 4c of the Commodity Exchange Act[4] by the CFTC, which prohibit wash trading.

2. Motivations and Results of Wash Trading in the NFT Market

The occurrence of wash trading in non-fungible tokens (NFTs) typically has the following motivations:

Traders increase their listing and bidding volumes to gain token incentives;

The market, project parties, or large holders of a specific NFT artificially inflate trading volumes to create a false impression of high demand to deceive buyers;

Project parties artificially raise prices to create news topics and stimulate consumption;

Money laundering (not within the scope of this discussion, please refer to Chainalysis article[5]).

NFT markets, such as LooksRare[6], X2Y2[7], and Blur (Airdrop2[8], Airdrop3[9]), initially attracted listing and bidding behaviors through token airdrops to accumulate users and hoped to create network effects; or incentivized different types of traders and trading behaviors at specific stages (for example, LooksRare's reward mechanism change in October 2022[10] aimed to distribute more incentives to creators).

Some "smart" NFT holders engage in wash trading that aligns with reward mechanisms to secure more token airdrops, while the NFT market is also pleased to see the apparent increase in user numbers and trading volumes. This became the main source of wash trading in the NFT market in 2022.

3. Distinguishing the Real from the Fake: The True NFT Market

As an ordinary Web3 user, before investing in or purchasing a specific NFT project, we want to know what constitutes false prosperity; as an investment institution, we need to understand the true value of an NFT marketplace after removing false transactions. The large number of wash trades in the market has affected value judgments.

So what does the true NFT market look like after removing wash trading? The author has created a data dashboard: Zoe's Dune Dashboard: The Real NFT Marketplace Landscape (https://dune.com/zoez17/the-real-nft-marketplace-landscap).

TL;DR: 1. Overall liquidity and trading volume trends in the NFT market

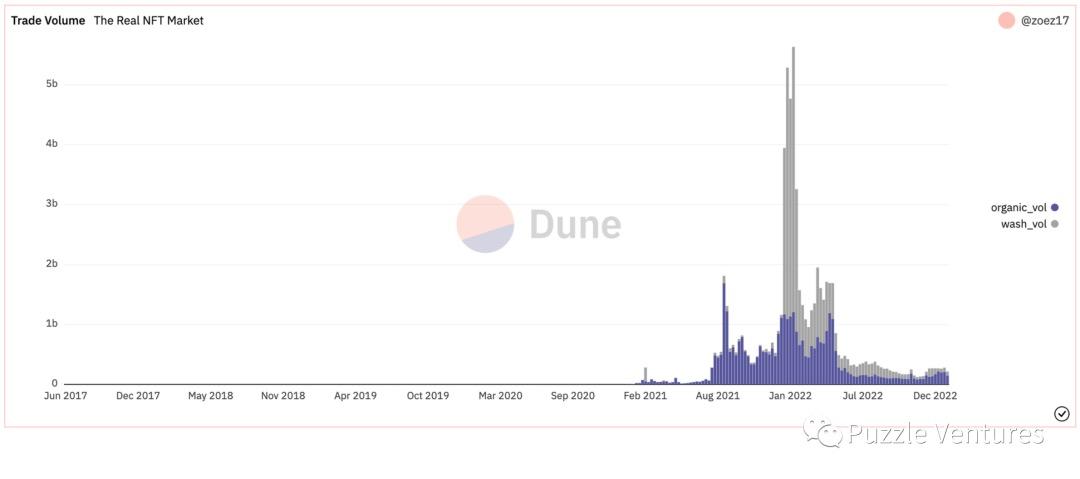

(1) Paper weekly trading volume:

The first NFT transaction occurred in the week of January 22, 2018;

The overall liquidity of the NFT market saw its first increase in June 2021, with the highest paper weekly trading volume reaching approximately $1.8 billion in August 2021;

Liquidity experienced a second explosive growth in December 2021 and January 2022 (mostly due to wash trading), with the highest paper weekly trading volume reaching $5.6 billion in January 2022;

In early May 2022, liquidity shrank due to the Luna crash and overall market weakness.

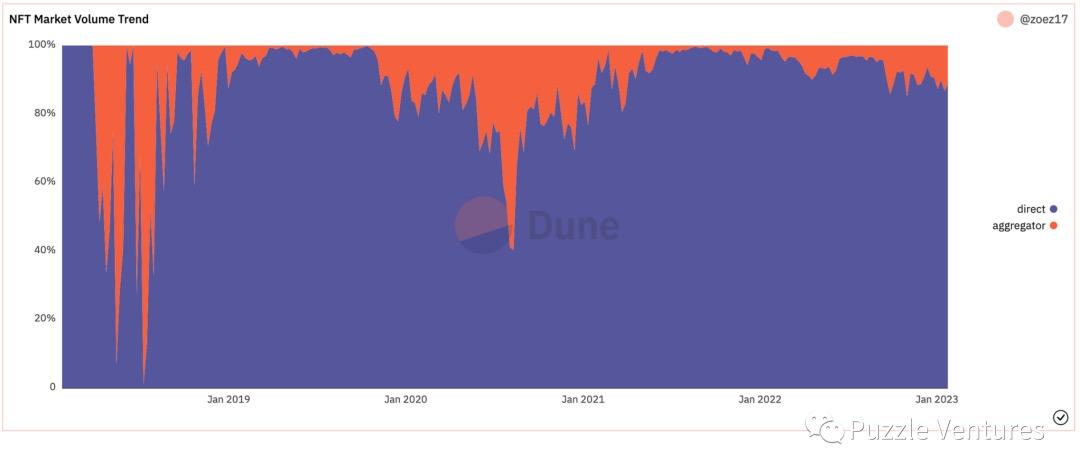

(2) The main trading volume still comes from direct trades on platforms (about 90%), rather than aggregators (about 10%).

(3) Actual weekly trading volume (excluding wash trading)

The first increase in actual weekly trading volume was $1.7 billion;

The second increase in actual weekly trading volume was $1.2 billion;

From May to October 2022, the actual weekly trading volume remained at $100 million to $200 million; from October to November 2022, weekly trading volume did not exceed $100 million; since December, there has been some improvement, with weekly trading volume maintaining at $150 million to $200 million.

All-time total NFT market volume trend: Organic trades (blue) VS. Wash trades (grey). First transaction appears in Jan, 2018. (Source: Zoe's Dune Query)

All-time total NFT market volume trend: Organic trades (blue) VS. Wash trades (grey). First transaction appears in Jan, 2018. (Source: Zoe's Dune Query)

All-time NFT Volume Trend from Direct Marketplaces (blue) VS. Aggregators (orange). (Source: Zoe's Dune Query)

All-time NFT Volume Trend from Direct Marketplaces (blue) VS. Aggregators (orange). (Source: Zoe's Dune Query)

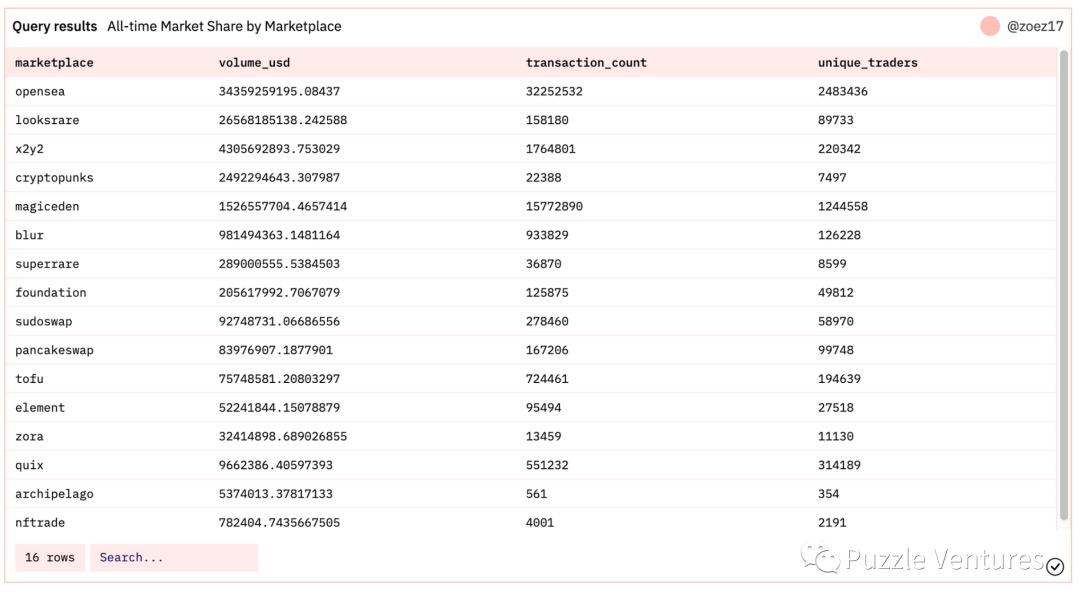

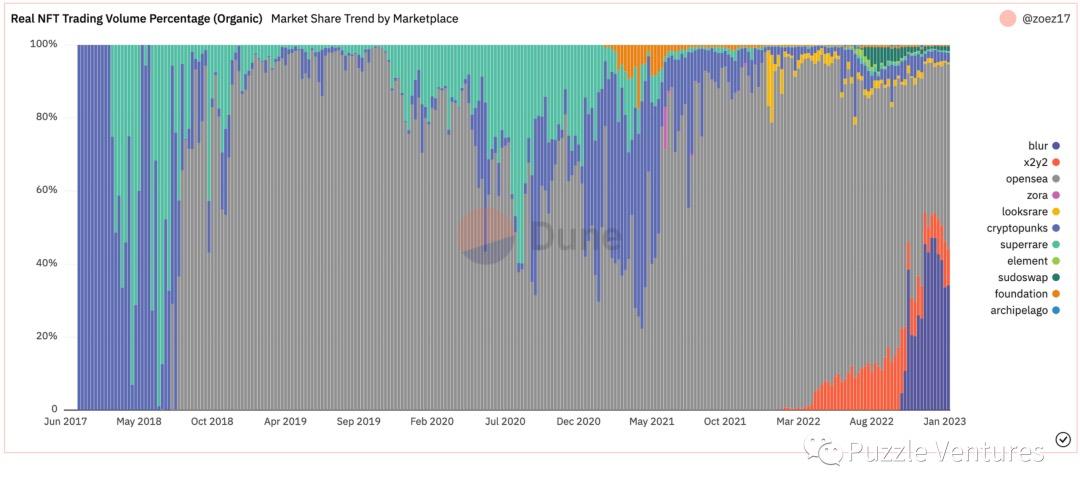

All-time market share by marketplace. No wash trade filters applied. (Source: Zoe's Dune Query)

2. Paper market share and real market share of different trading platforms

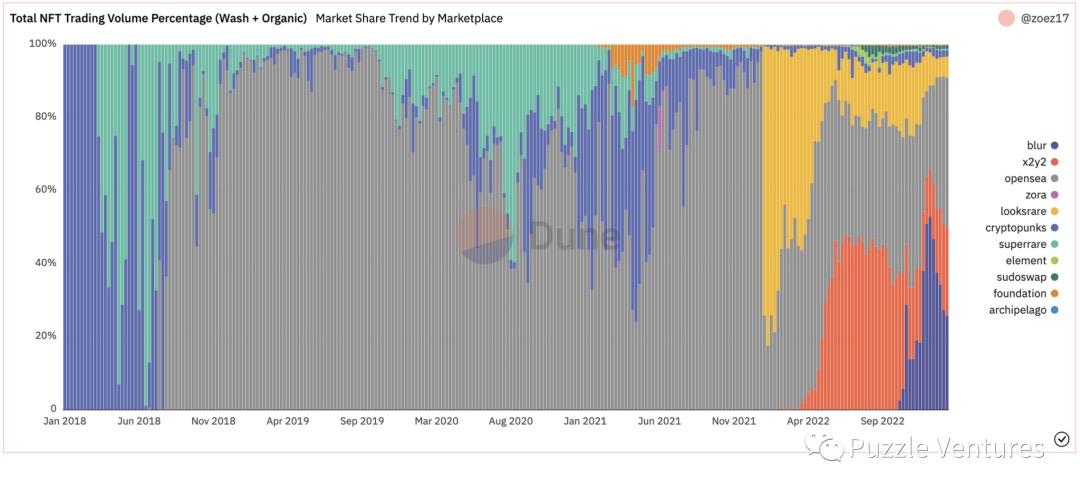

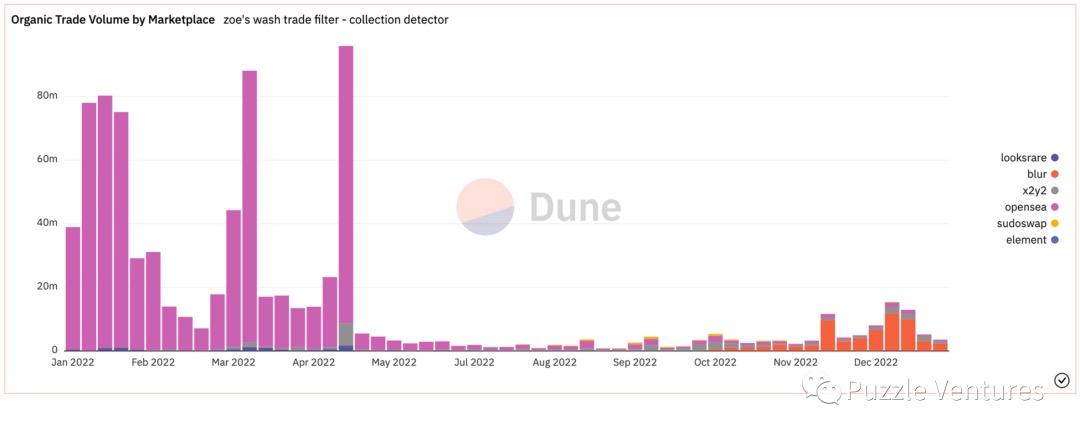

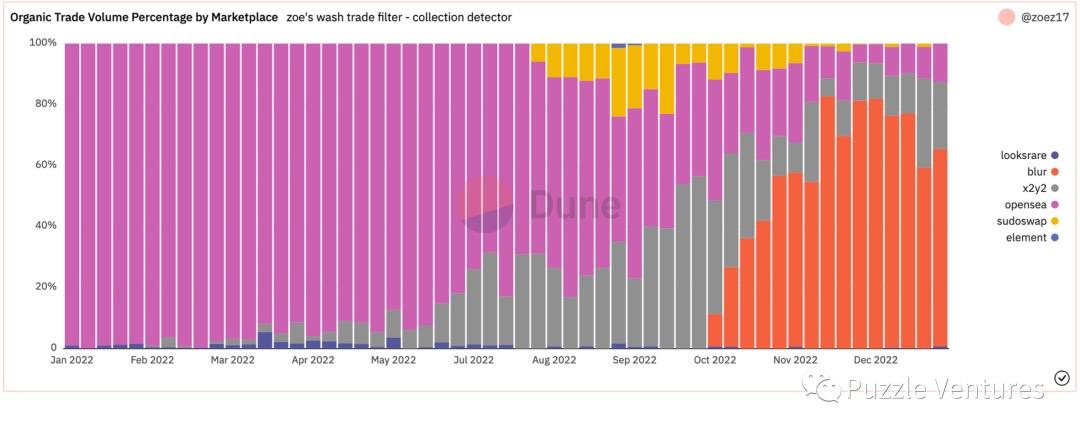

In terms of market share, a relatively large change comes from OpenSea: after removing wash trading from other platforms, its real market share has declined from over 95% at the beginning of 2022 to below 70% since October, and around 50% since December, even dropping to as low as 40% at one point.

LooksRare and X2Y2 are the main sources of wash trading in the market, due to their trading incentive policies, with X2Y2 performing better in reality, maintaining a real market share of about 7-10%; LooksRare performs poorly, with a real market share of less than 2%.

Since mid-October 2022, after removing wash trading, Blur has still performed outstandingly, mainly due to airdrop expectations, lower transaction fees, and optional royalties.

Total (organic trades + wash trades) NFT Trading Volume Market Share. Opensea - grey, LooksRare - yellow, X2Y2 - orange, blur - blue. (Source: Zoe's Dune Query)

Total (organic trades + wash trades) NFT Trading Volume Market Share. Opensea - grey, LooksRare - yellow, X2Y2 - orange, blur - blue. (Source: Zoe's Dune Query)

Real (ONLY organic trades) NFT Trading Volume Market Share. Opensea - grey, LooksRare - yellow, X2Y2 - orange, blur - blue. (Source: Zoe's Dune Query)

Real (ONLY organic trades) NFT Trading Volume Market Share. Opensea - grey, LooksRare - yellow, X2Y2 - orange, blur - blue. (Source: Zoe's Dune Query)

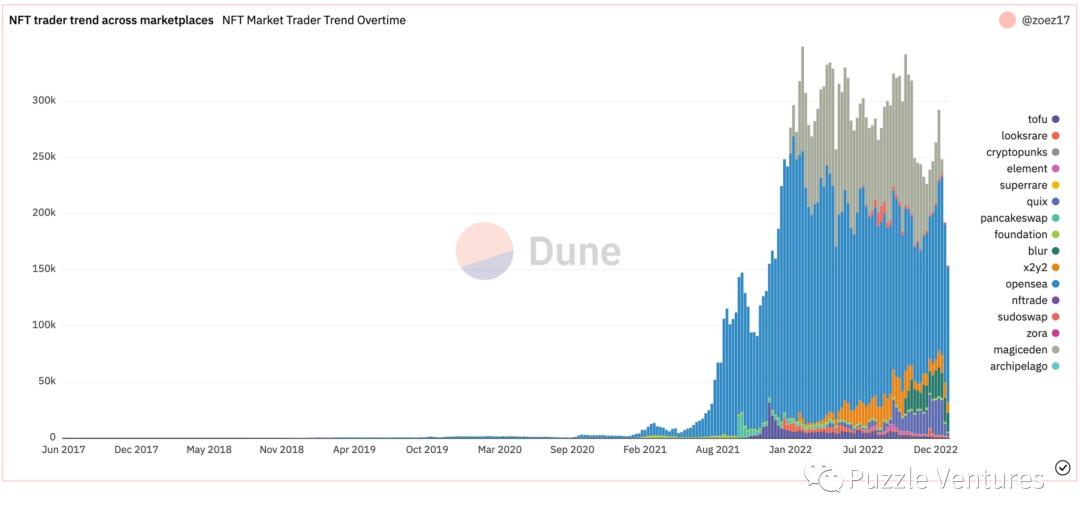

- In terms of the number of traders, the activity on MagicEden (Solana) has not been completely impacted after the FTX incident.

NFT trader trend across marketplaces. MagicEden - top yellowish grey. (Source: Zoe's Dune Query)

NFT trader trend across marketplaces. MagicEden - top yellowish grey. (Source: Zoe's Dune Query)

3. Whether a specific project is worth investing in can mainly be viewed from the following three perspectives:

The overall liquidity of the project

The trading liquidity of the project across different markets

The real trading volume of the project

Taking Azuki (0xed5af388653567af2f388e6224dc7c4b3241c544) as an example for analysis:

Overall liquidity and real trading volume: There was a small peak starting in December, with the real weekly trading volume reaching $15.4 million in the week of January 2 after excluding wash trading, with 720 transactions.

Trading liquidity across different markets: This wave of trading mainly occurred on Blur, accounting for about 70%-80%.

Transaction count trend and proportion: Consistent with trading volume, reaching 2,446 transactions in the past month (from December 5 to January 8).

Azuki's Organic Trade Volume Trend by Marketplace. Opensea - pink, Blur - orange. (Source: Zoe's Dune Query)

Azuki's Organic Trade Volume Market Share. Opensea - pink, Blur - orange. (Source: Zoe's Dune Query)

The Collection Detector at the bottom of the data dashboard provides individual investors a place to look up the real trading data of specific projects to support their decision-making.

For example, if readers find that a hot project in the market has a real trading volume far less than its paper trading volume, this may indicate that the project is creating a false impression of high trading volume to mislead the market; or if you find that a certain project has a trading volume on Blur that far exceeds that on OpenSea, it may be more appropriate to list on Blur, and so on.

【Alert: The following discusses the characteristics of NFT wash trading and how the author filters out NFT wash trading based on these characteristics.】

4. How to Filter Out Wash Trading in the Market

To make forward-looking and reasonable value judgments, we must find a more broadly applicable data method, utilizing existing tools to analyze the market, trading platforms, and projects. The precise mapping used in the aforementioned Chainalysis study is far from sufficient[5], as consumers or investors do not need to analyze specific trading events or require overly precise data.

Our goal is to: identify the trading characteristics and significant data patterns of wash trading, and filter out wash trading in the market while ensuring a certain level of accuracy, to:

Assess the current market situation based on real trading volume and find as genuine signals as possible;

Determine the real trading situation of a specific project and identify investment targets.

With data support, along with fundamental analysis and community observation, doing your homework can help you become a smarter consumer or investor. At the same time, do not forget to trust your own judgment and aesthetic preferences.

✦ Characteristics of Wash Trading: Analyzing Ideas and Practices

1. Buyer Wallet Address = Seller Wallet Address (Buyer = Seller)

Such wash trades are overly simplistic and show no disguise; it sounds unbelievable, and the specific reasons for such trades are unclear, but they can be executed on OpenSea, LooksRare, X2Y2, and Blur, and similar trades can be found.

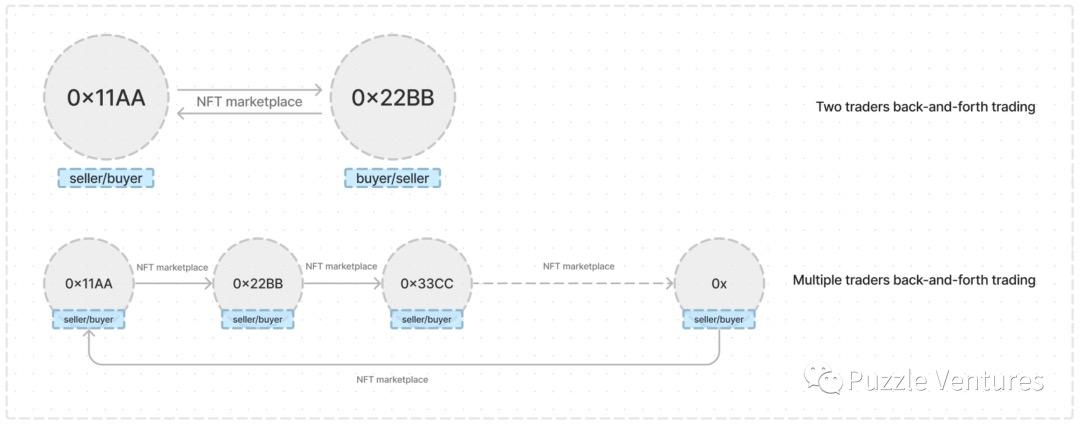

2. Back & Forth Trading involves repeated trading back and forth between two or more wallets, where the actual owner of the wallets may be one or more individuals. This is also one of the most common strategies in wash trading.

2. Back & Forth Trading involves repeated trading back and forth between two or more wallets, where the actual owner of the wallets may be one or more individuals. This is also one of the most common strategies in wash trading.

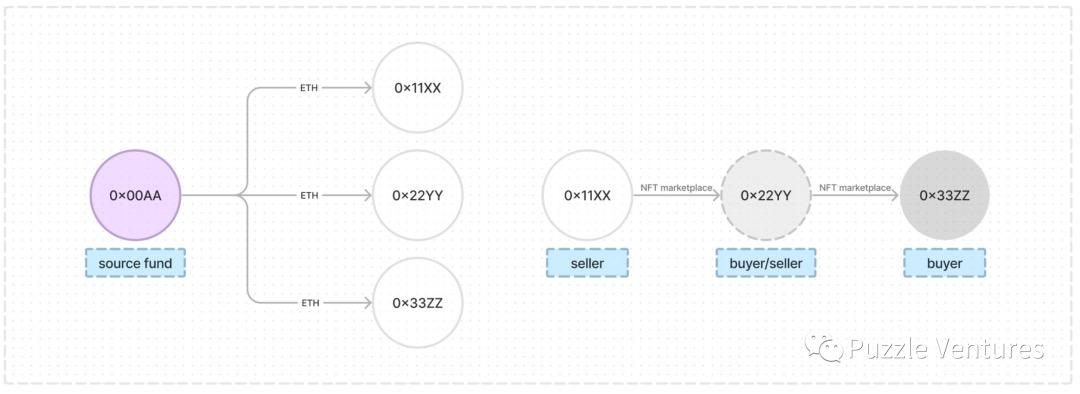

3. Trading Between Different Wallets with the Same Actual Owner (Shared Owner) Although the transactions may occur in different wallets, the actual traders are the same, and no real trading turnover has occurred. One way to prove that multiple wallet addresses have the same actual owner is to check whether the source of the first gas token (ETH) payment received by these wallets is the same.

This situation was mentioned in a recent article on wash trading by Dragonfly data researcher hildobby published on Dune[11], and this data method is often used in wallet mapping to bind wallet connections.

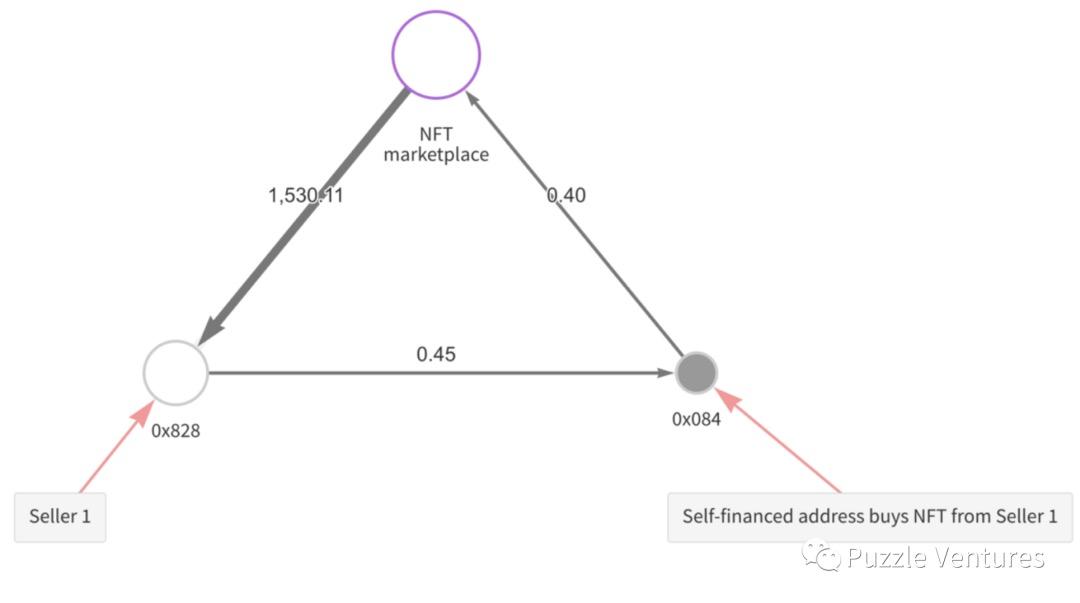

4. Self-financed Wallets Two wallets conspire in advance, with the NFT seller transferring money to the buyer beforehand, who then purchases the NFT in the market. This usually occurs during the bootstrap process of the project, bribing potential buyers, preferably KOLs, to achieve better publicity.

4. Self-financed Wallets Two wallets conspire in advance, with the NFT seller transferring money to the buyer beforehand, who then purchases the NFT in the market. This usually occurs during the bootstrap process of the project, bribing potential buyers, preferably KOLs, to achieve better publicity.

Excerpt from Chainalysis, where this transaction can be found on Etherscan: the seller (0x828) sells a certain NFT to the buyer (0x084) for 0.4E through a certain NFT trading market. However, shortly before the transaction occurred, 0x828 transferred 0.45E to 0x084.*

Judging this type of wash trading is relatively special and requires attention:

Assuming the buyer and seller are two entities, unless the seller has multiple such behaviors, it is difficult to determine a necessary connection between the two transactions;

The amount of money "the seller transfers to the buyer in advance" should be approximately equal to the selling price of the NFT (sometimes including gas or a small incentive), if it is too low, the buyer will not find it worthwhile; if it is too high, the seller will incur a loss. The reasonable range in actual situations may be related to platform incentive expectations, gas, and actual negotiations between the buyer and seller;

The time interval between the two transactions should not be too far apart; otherwise, they may be unrelated transactions;

The time, calculation, and management costs of such wash trading behaviors are relatively high and are not suitable for large-scale wash trading aimed at mining and obtaining trading incentives; they are more likely to be used by project parties as a cold-start tool or for money laundering.

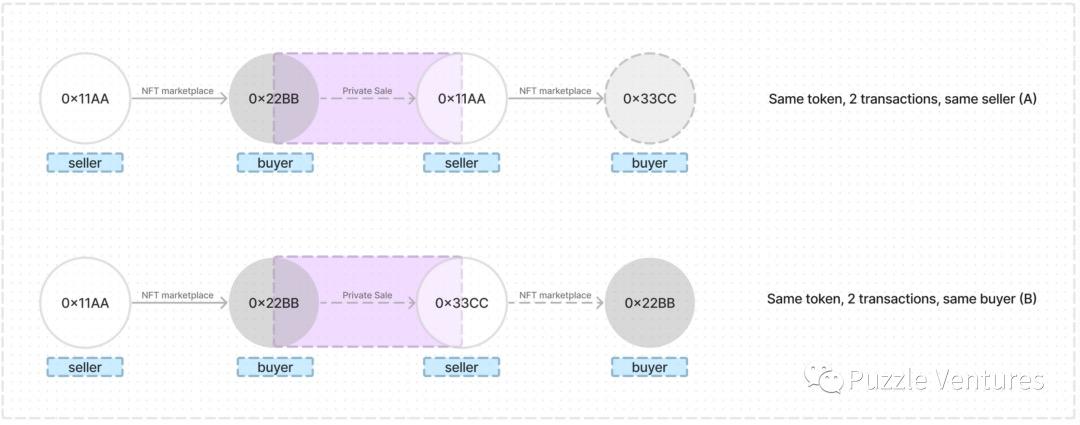

5. Combining Public Market Transactions and Private Transactions (Public Sale + Private Sale)

Some traders may choose this trading strategy to evade wash trading scrutiny or prevent the association of their wallets from being discovered. Typically, one wallet (A) will list on the public market, buy it with another wallet (B), and then conduct a private transfer before listing it again for sale to another wallet.

This form may have various variations. However, regardless of the motivation, when a wallet successfully sells or purchases a specific NFT (same contract address and token_id) multiple times in a relatively short time frame (such as a week), we can consider such transactions to be suspicious of wash trading.

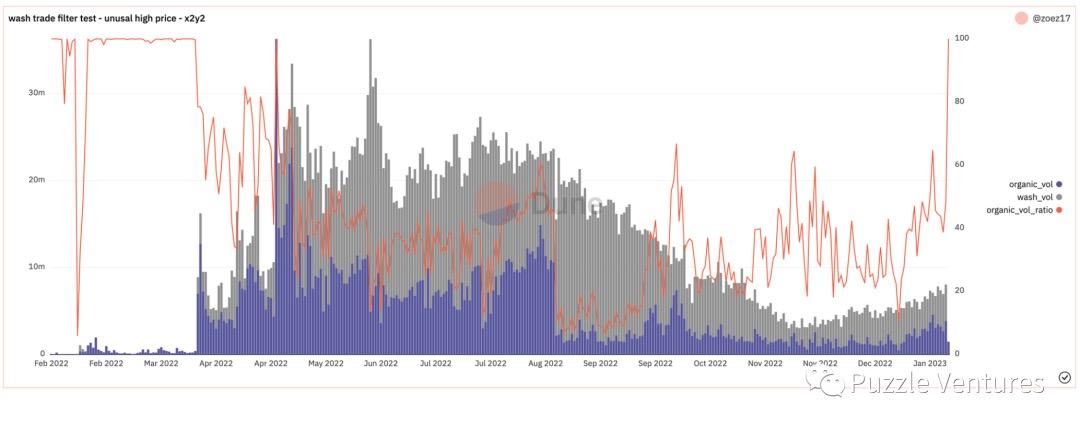

6. Unusually High Prices

At least during most of the period from 2021 to 2022, OpenSea had the vast majority of users and trading volume in the market, stabilizing at over 60%, and at one point in the first half of 2022, it reached as high as 90%, forming a network effect and possessing pricing power. OpenSea has no motivation to engage in wash trading to falsely inflate trading volume (as it is already the highest); traders on its platform also have no motivation to engage in fraudulent buying and selling (as OpenSea has no token incentive policy).

Therefore, we can make a relaxed assumption that OpenSea, as the industry benchmark, reflects the actual market situation more accurately compared to the floor and ceiling prices on other platforms. Considering the current lack of liquidity in the NFT market, if the actual trading price of an NFT exceeds the historical highest price on OpenSea, we can consider that transaction to be fraudulent.

Filtering out wash trades with unusually high prices in the X2Y2 market. Data up to January 13, 2023. (Source: Zoe's Dune Query)

Filtering out wash trades with unusually high prices in the X2Y2 market. Data up to January 13, 2023. (Source: Zoe's Dune Query)

However, through a series of data filtering comparisons (Dune Dashboard: wash trade filter test), we found that using the highest price on OpenSea as a guiding price has become outdated. On one hand, other filtering methods can filter out most of such transactions; on the other hand, OpenSea's pricing power in the NFT market is also constantly being challenged:

Some projects have no transactions or very little liquidity on OpenSea, leading to price distortions, such as Sports Ape Club (0x69b301a08eecbbc522301bf3268f782f19ad1279) and Koungz (0x99b5808e1520c9c1bc970eec98bb712c5c883e4b). Currently, these projects are small enough to be negligible, but it cannot be ruled out that in the future, there may be games, artworks, membership cards, and other NFTs choosing other trading markets to seize their pricing power ------ for example, by innovating NFT AMMs or creating vertical platforms with specific user profiles, or trading platforms with more reasonable transaction fees.

When NFT liquidity is good, new price highs may continually emerge; if real price highs appear in non-OpenSea markets, then the highest price needs to be updated artificially.

Different NFT markets will establish different rules, including commission rates, royalty regulations, etc., which will affect the choices of projects and traders for listing.

Such wash trades with inflated prices do exist, and not in small numbers, for example, Dreadfulz (0x81ae0be3a8044772d04f32398bac1e1b4b215aa8), which is used for large-scale wash trading, with prices often reaching nearly $300,000. This is closely related to the incentive policies of trading platforms; for instance, X2Y2's rewards for sellers are related to transaction fee sharing, so everyone is willing to trade at higher prices.

However, due to the above considerations, no special filters will be set for such transactions. In fact, this decision does not significantly impact the overall filtering effect.

✦ How to Identify and Filter Wash Trading Data: A Data-Driven Approach

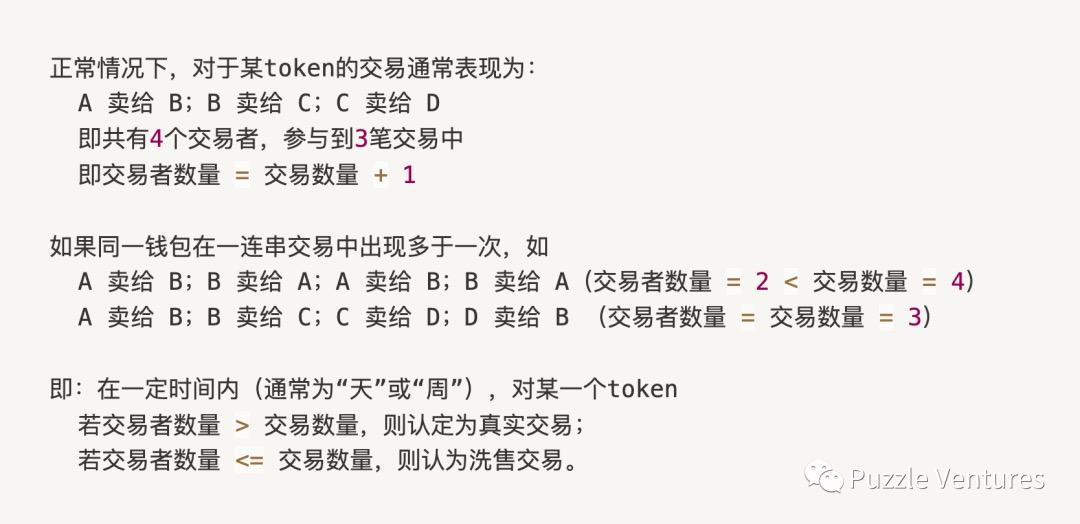

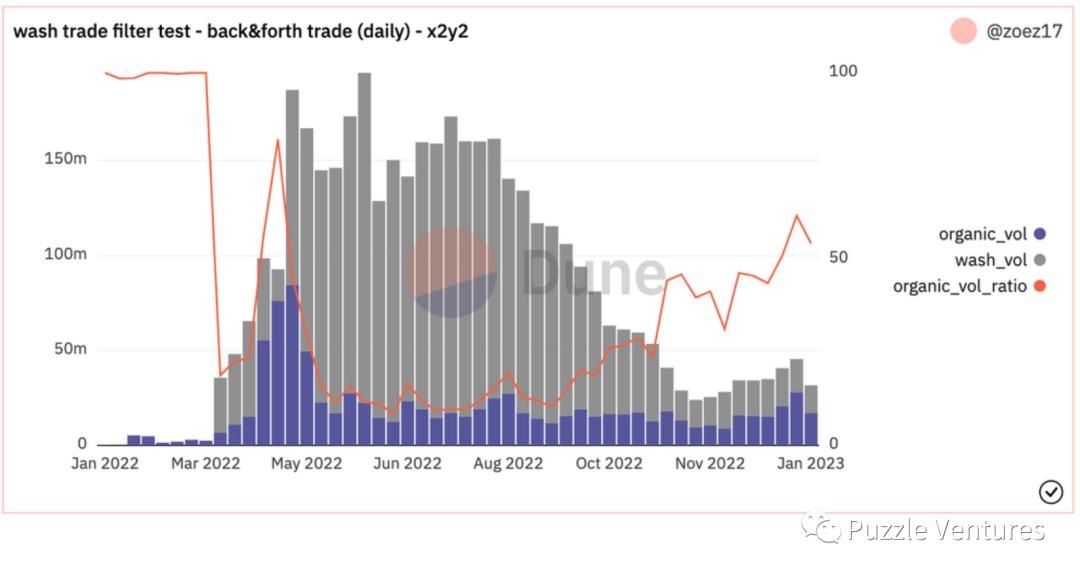

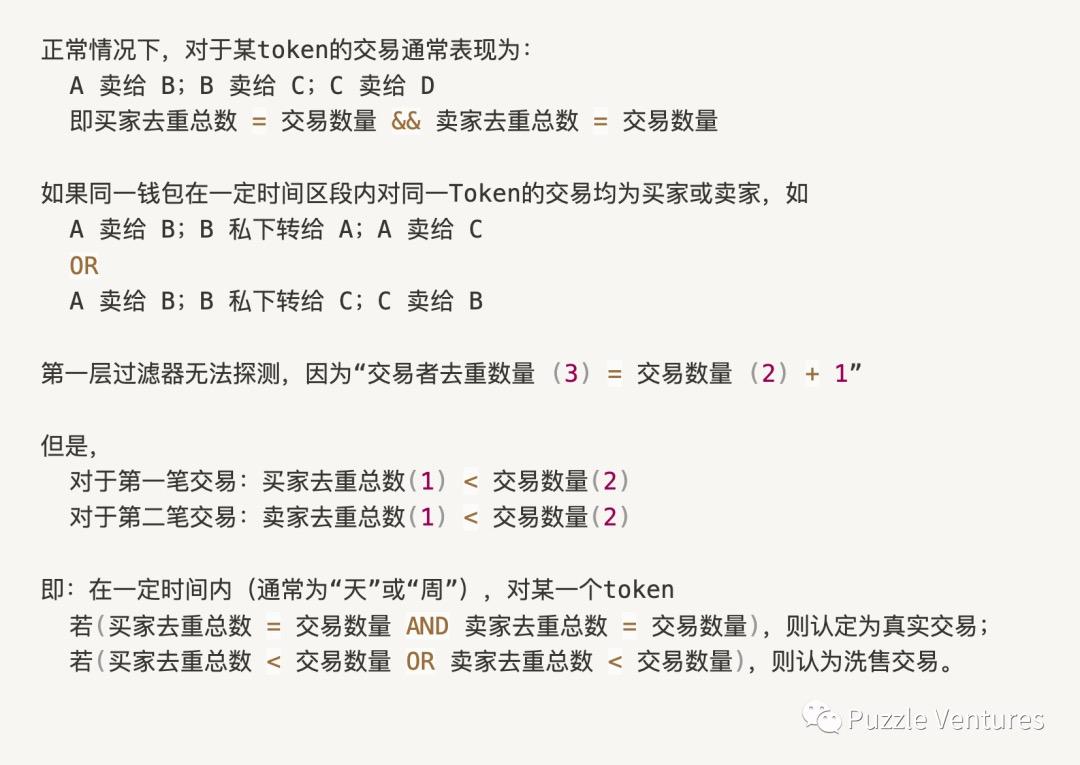

First Layer Filter: Within a Specific Time Frame, the Number of Transfers of a Certain NFT ≥ Number of Traders (transaction count ≥ trader number)

We found that in the aforementioned categories of wash trading (the 1st, 2nd, and 3rd types, with the 6th type also being filterable), they all involve one or more consecutive transactions involving the same person appearing more than once regarding a certain token. That is:

In practical testing, we found that:

Transactions with these characteristics account for the vast majority of wash trading in the NFT market, and the filter's efficiency is also the highest.

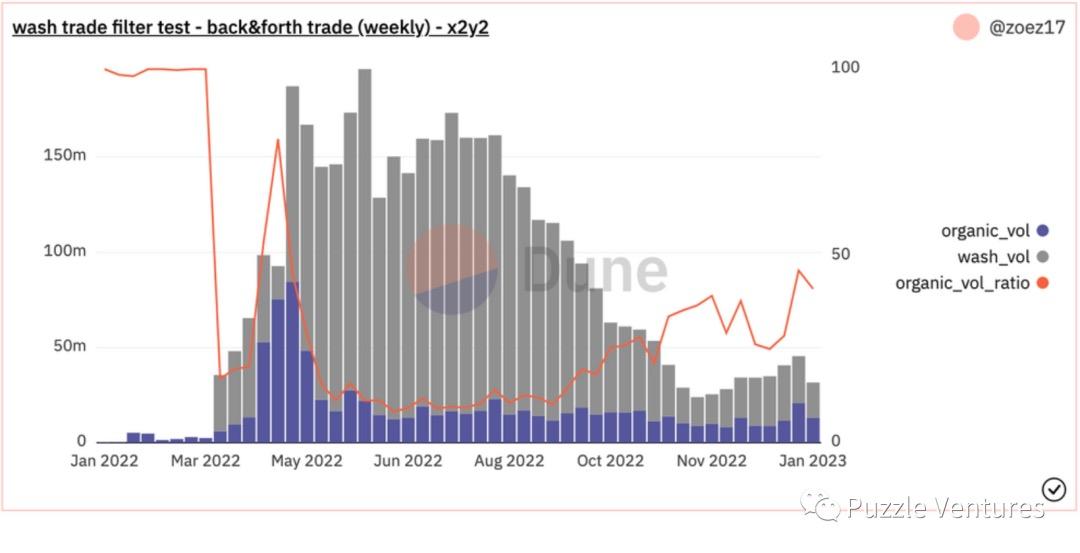

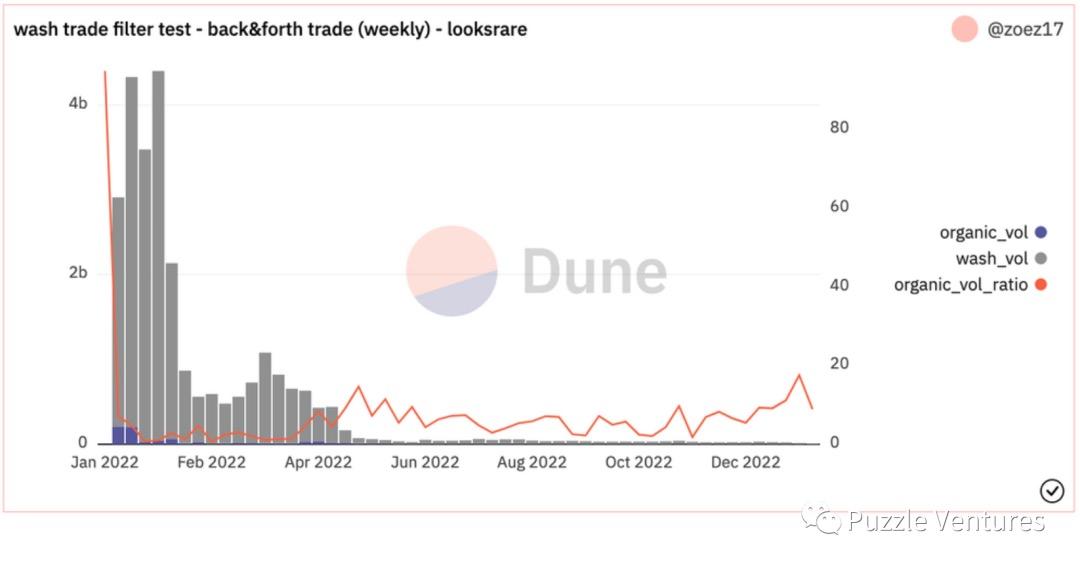

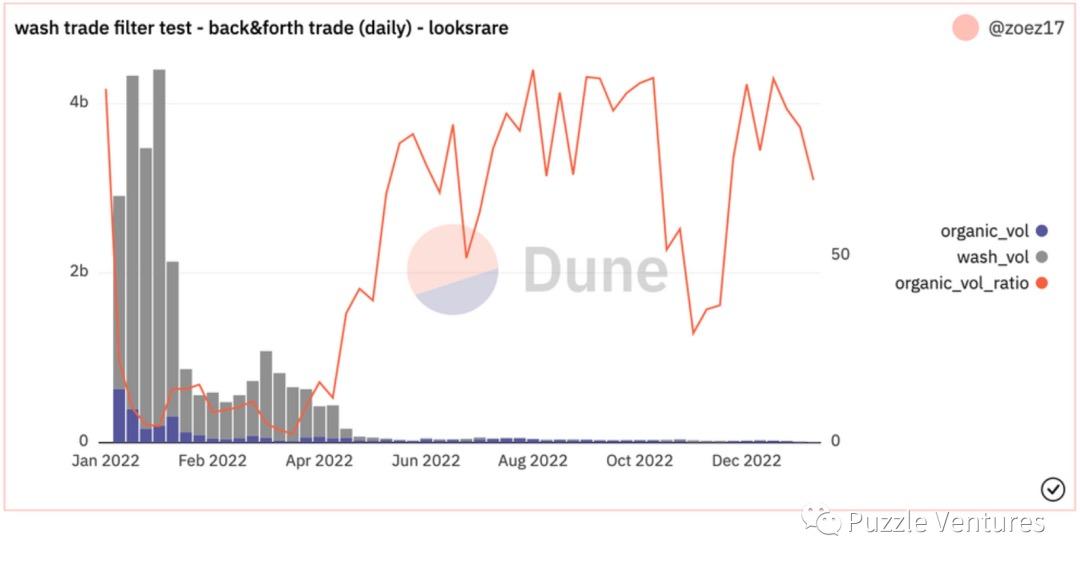

Filtering on a weekly basis is significantly more effective than on a daily basis.

Through verification in two markets (X2Y2 and LooksRare), the author's filter combination and hildobby's filter combination[12][13] have different methods but similar overall trends and final effects, providing mutual verification; the results of the first layer filter alone also show similar trends to the final results, further demonstrating the importance of the first layer.

Filtering the performance of the X2Y2 market using the "first layer filter" on a daily basis (top) and weekly (bottom). The latter shows better recent filtering effects while not losing the wash trades filtered out by the former. (Source: Zoe's Dune Dashboard)

Filtering the performance of the LooksRare market using the "first layer filter" on a daily basis (top) and weekly (bottom). The latter is clearly superior to the former. (Source: Zoe's Dune Dashboard)

Second Layer Filter: Trading Between Different Wallets with the Same Actual Owner (First-funded by the same wallet)

Considering time costs, typically, a wash trade for an NFT (same contract address, same token ID) will always involve transfers within the same wallet, which can be resolved by the first layer filter. However, there may be some outliers ------ some individuals may create a large number of wallets to evade circular trading.

But also due to time or management costs, these numerous different wallets used for wash trading often have their initial funds transferred from the same wallet (excluding funds coming from centralized wallet addresses or from Tornado Cash). Imagine you now create 20 wallet addresses; they all need initial ETH for gas fees, and typically, you might use a small number of main wallets to provide initial funding for gas.

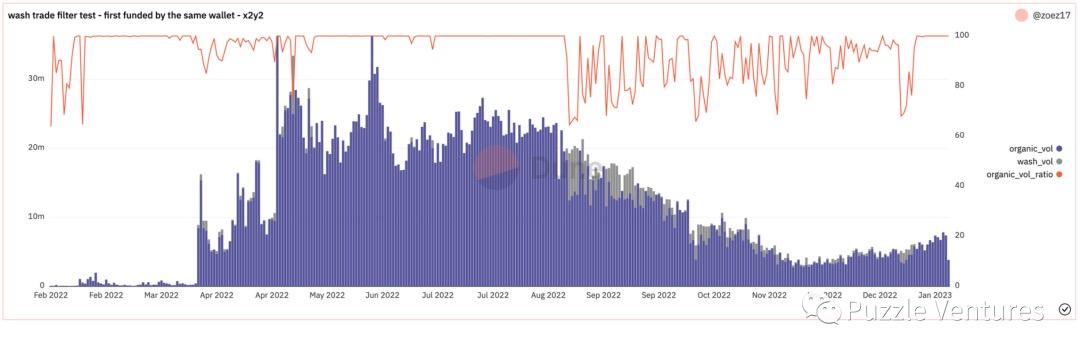

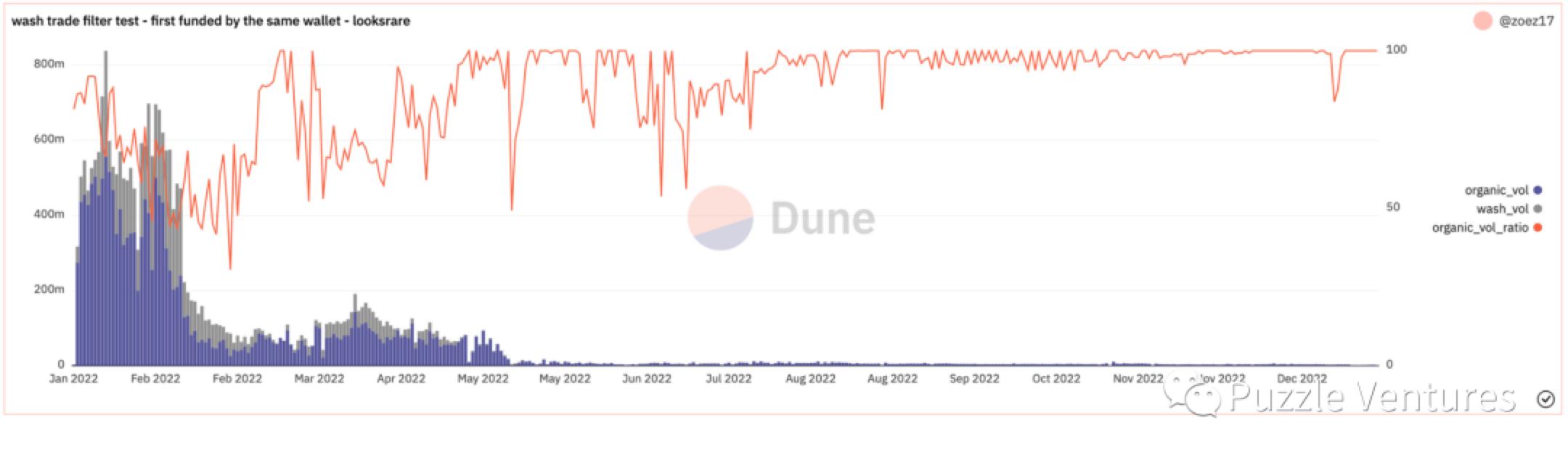

Here, the author directly used hildobby's open-source fourth filter[14], thanking him for this work, which excluded about 500 centralized wallet addresses and Tornado Cash contract addresses.  Using the second layer tracing filter (First-funded by the same wallet) to filter the performance of the X2Y2 market, finding that after August 2022, a small number of such transactions appeared, which accounted for a small proportion from a trading volume perspective. (Source: Zoe's Dune Query)

Using the second layer tracing filter (First-funded by the same wallet) to filter the performance of the X2Y2 market, finding that after August 2022, a small number of such transactions appeared, which accounted for a small proportion from a trading volume perspective. (Source: Zoe's Dune Query)  Using the second layer tracing filter (First-funded by the same wallet) to filter the performance of the LooksRare market, finding that after January 2022, a certain amount of such transactions appeared, which accounted for less than the transactions filtered out by the first layer filter. (Source: Zoe's Dune Query)

Using the second layer tracing filter (First-funded by the same wallet) to filter the performance of the LooksRare market, finding that after January 2022, a certain amount of such transactions appeared, which accounted for less than the transactions filtered out by the first layer filter. (Source: Zoe's Dune Query)

Through the analysis of both X2Y2 and LooksRare markets, we found that when using the "second layer filter" alone, the volume of such transactions is relatively low. Although it cannot reflect the overall trend of wash trading, it can improve filtering accuracy.

As for the method of transferring funds to one's wallet through centralized exchanges, it is currently challenging to find a suitable approach.

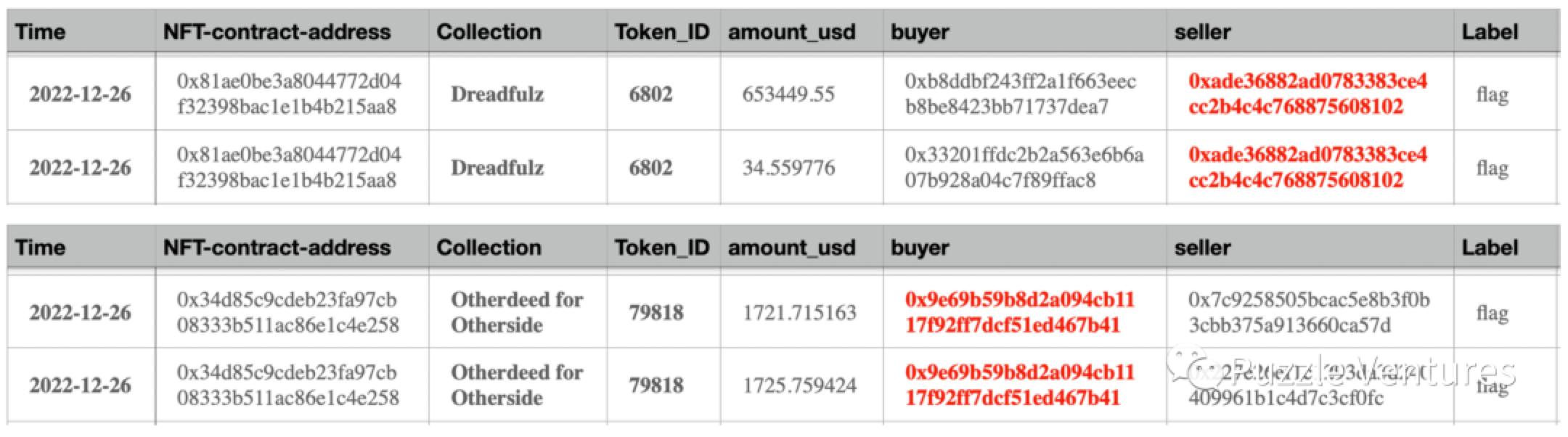

Third Layer Filter: Combining Public Market Transactions and Private Transactions (Public Sale & Private Sale)

While observing NFT transactions, the author discovered a trading behavior that evaded the "first layer filter": for some reason, on the same day, the same token was traded twice on LooksRare, and the trading volume was huge:

For Dreadfulz (token ID: 6802), both transactions had the same seller;

For Otherdeed for Otherside (token ID: 79818), both transactions had the same buyer.

Regardless of the motivation, when a wallet successfully sells or purchases a specific NFT (same contract and token_id) multiple times in a relatively short time frame (such as a week), we can consider such transactions to be suspicious of wash trading.

5. Other Indicators Worth Noting

The number of users on different trading platforms

The vertical market share of different trading platforms

The average number of transactions per user per day

The turnover rate, listing supply, and purchasing demand of a specific NFT project

And more

We will further explore these in the future.

References:

[1] Wash Trades - Definition of a Wash Trade, CME Group, https://www.cmegroup.com/education/courses/market-regulation/wash-trades/definition-of-a-wash-trade.html

[2] CFTC Glossary - Wash Trading, Commodity Futures Trading Commission, https://www.cftc.gov/LearnAndProtect/EducationCenter/CFTCGlossary/glossary_wxyz.html

[3] Market Regulation Advisory Notice (Rule 534), CME Group, https://www.cmegroup.com/rulebook/files/cme-group-Rule-534.pdf

[4]Commodity Exchange Act & Regulations, Commodity Futures Trading Commission, https://www.cftc.gov/sites/default/files/files/foia/comment98/foicf9806b002c.pdf

[5] Crime and NFTs: Chainalysis Detects Significant Wash Trading and Some NFT Money Laundering In this Emerging Asset Class, Chainalysis, https://blog.chainalysis.com/reports/2022-crypto-crime-report-preview-nft-wash-trading-money-laundering/

[6] LooksRare Docs: Trading Rewards, LooksRare, https://docs.looksrare.org/about/rewards/trading-rewards

[7] X2Y2 Docs: Trading Rewards, X2Y2, https://docs.x2y2.io/tokens/rewards/trading-rewards

[8] Blur Airdrop 2, Blur, https://mirror.xyz/blurdao.eth/XgvGOFLwdxpdRIF2BRsQqngvcBw5WMuDOcwUK3KR1AE

[9] Blur Airdrop 3, Blur, https://mirror.xyz/blurdao.eth/BnVAtz6bEr9O4oLIFwyEjCmAGGb02jz8y3G7qJQhA

[10] LooksRare Offers Zero Royalty Trading, Shares Protocol Fees With Creators Instead, LooksRare, https://docs.looksrare.org/blog/looksrare-offers-zero-royalty-trading-shares-protocol-fees-with-creators-instead

[11] NFT Wash Trading on Ethereum, hildobby, https://community.dune.com/blog/nft-wash-trading-on-ethereum

[12] Dune Dashboard: Ethereum NFTs Wash Trading, hildobby, https://dune.com/hildobby/nfts-wash-trading

[13] Github Repository: duneanalytics/spellbook/models/nft/nftwashtrades.sql, hildobby, https://github.com/duneanalytics/spellbook/blob/main/models/nft/nftwashtrades.sql

[14] Github Repository: duneanalytics/spellbook/models/addressesevents/ethereum/addresseseventsethereumfirstfundedby.sql, hildobby, https://github.com/duneanalytics/spellbook/blob/main/models/addressesevents/ethereum/addresseseventsethereumfirstfundedby.sql

Disclaimer: This research report represents the author's independent views based on publicly available information and is for reference and discussion only, not constituting financial, investment, or any other advice.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles