From an index perspective, which tokens are likely to be approved for purchase by retail investors in Hong Kong?

Asia may become increasingly capable of迎接 a new wave of cryptocurrency investment.

Asia may become increasingly capable of迎接 a new wave of cryptocurrency investment.Original Author: Colin Wu, Wu Says

According to the latest requirements from the Hong Kong Securities and Futures Commission, licensed platform operators intending to offer virtual assets to retail clients must ensure that the selected virtual assets are qualified large virtual assets and meet the specific token inclusion criteria listed below. "Qualified large virtual assets" refer to virtual assets included in at least two "accepted indices" launched by at least two independent index providers.

The index should be investable, meaning that the constituent virtual assets should have sufficient liquidity. The index should be calculated objectively and based on rules. The index provider should possess the necessary expertise and technical resources to construct, maintain, and review the methodology and rules of the index compilation.

Licensed platform operators should ensure that at least one of the two indices is launched by an index provider with experience in publishing indices for traditional non-virtual asset financial markets, such as those that have launched indices tracked by SFC-recognized index funds.

According to @tier 10 k statistics, currently, five mainstream traditional institutions have launched indices, ranked as recorded in the table. Bitcoin (BTC) and Ethereum (ETH) are recorded in all indices; ranked second are Litecoin (LTC) and Polkadot (DOT), included in four indices; ranked third are Bitcoin Cash (BCH) and SOL, included in three indices; ranked fourth are Cardano, Avalanche, Polygon, and Chainlink, included in two indices. Additionally, EOS, BNB, STOM, FIL, ETC, XLM, UNI, etc., are also included once. However, it is important to note that major indices may increase or decrease with market changes.

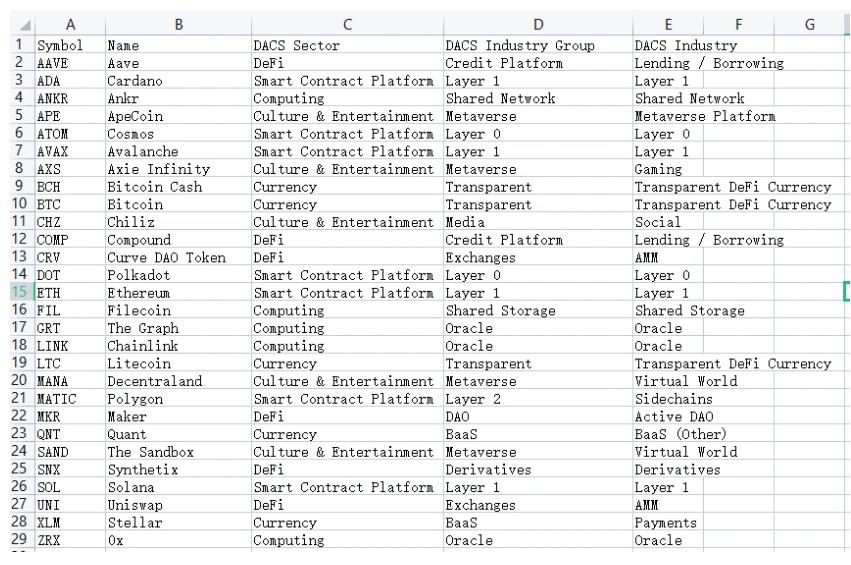

It is noteworthy that the Hong Kong Securities and Futures Commission emphasizes that only inclusion in one traditional index is required, meaning that those included once all have opportunities. For example, the index launched by CoinDesk is relatively broad, including 28 cryptocurrencies. There are also various different categories such as DeFi, entertainment, smart contract platform indices, etc.

Kaiko Research has also discussed this in detail, emphasizing the importance of liquidity:

Merely using market capitalization to measure the value of tokens is insufficient; we need to combine it with other metrics, especially liquidity. Liquidity is one of the criteria for index construction, which is common in traditional finance, and cryptocurrency is no exception. According to Nasdaq, their indices are constructed using "strict liquidity standards." I am not sure how this justifies holding XLM, ETC, or UNI. In December, I ranked the top 28 tokens based on liquidity: XLM was at the bottom, UNI ranked 22nd, while ETC had insufficient liquidity to even be included.

The inclusion of Bitcoin Cash, Polkadot, and Litecoin raises concerns from a liquidity perspective. I believe that if the SFC intends to include large-cap assets, they must choose tokens with higher liquidity. Firstly, these three tokens rank poorly in the 2% market depth, which measures the order volume on the current exchange order book within 2% of the current price.

We need a more robust index construction method that considers liquidity alongside market capitalization. DOGE deserves more consideration from the SFC because it has very superior liquidity. From both a fundamental and liquidity perspective, some tokens that could be considered under the SFC's new rules are not of the highest quality. This is indeed a problem in cryptocurrency index construction, but the SFC needs to properly consider liquidity, as they may exclude some tokens with better fundamentals and liquidity because they are not included in two indices. Any tokens included in the new parameters should see new investments and improved sentiment, and Asia may increasingly be capable of welcoming a new wave of cryptocurrency investment.