Review of the Stablecoin Market After USDC Depegging: Purchasing Power Drops to Short-Term Low, Fiat-Backed Stablecoins Are the Absolute Mainstream

Although the USDC de-pegging crisis was resolved on March 13, this de-pegging has still brought many changes and reflections to the stablecoin market. Did the de-pegging provide an "opportunity" for other types of stablecoins? Has the liquidity of stablecoins in the market decreased or increased? Where did stablecoins primarily flow during the crisis?

Although the USDC de-pegging crisis was resolved on March 13, this de-pegging has still brought many changes and reflections to the stablecoin market. Did the de-pegging provide an "opportunity" for other types of stablecoins? Has the liquidity of stablecoins in the market decreased or increased? Where did stablecoins primarily flow during the crisis?Author: Carol, PANews

Affected by the collapse of partner banks, the USD stablecoin USDC is currently facing a liquidity crisis. According to CoinGecko data, the price of USDC dropped to a low of $0.8788 on March 11, with a daily decline of over 12%. At the same time, the de-pegging of USDC also caused other stablecoins that accepted it as collateral, such as DAI and FRAX, to experience varying degrees of de-pegging.

Although the crisis of USDC was resolved on March 13, the de-pegging of USDC, once the most trusted stablecoin, has brought many changes and reflections to the stablecoin market. Did the de-pegging of centralized fiat-backed stablecoins provide an opportunity for other types of stablecoins? Has the liquidity of stablecoins in the market decreased or increased? Where did stablecoins primarily flow during the crisis? After analyzing the basic overview and market data of stablecoins (March 11-18), PAData found:

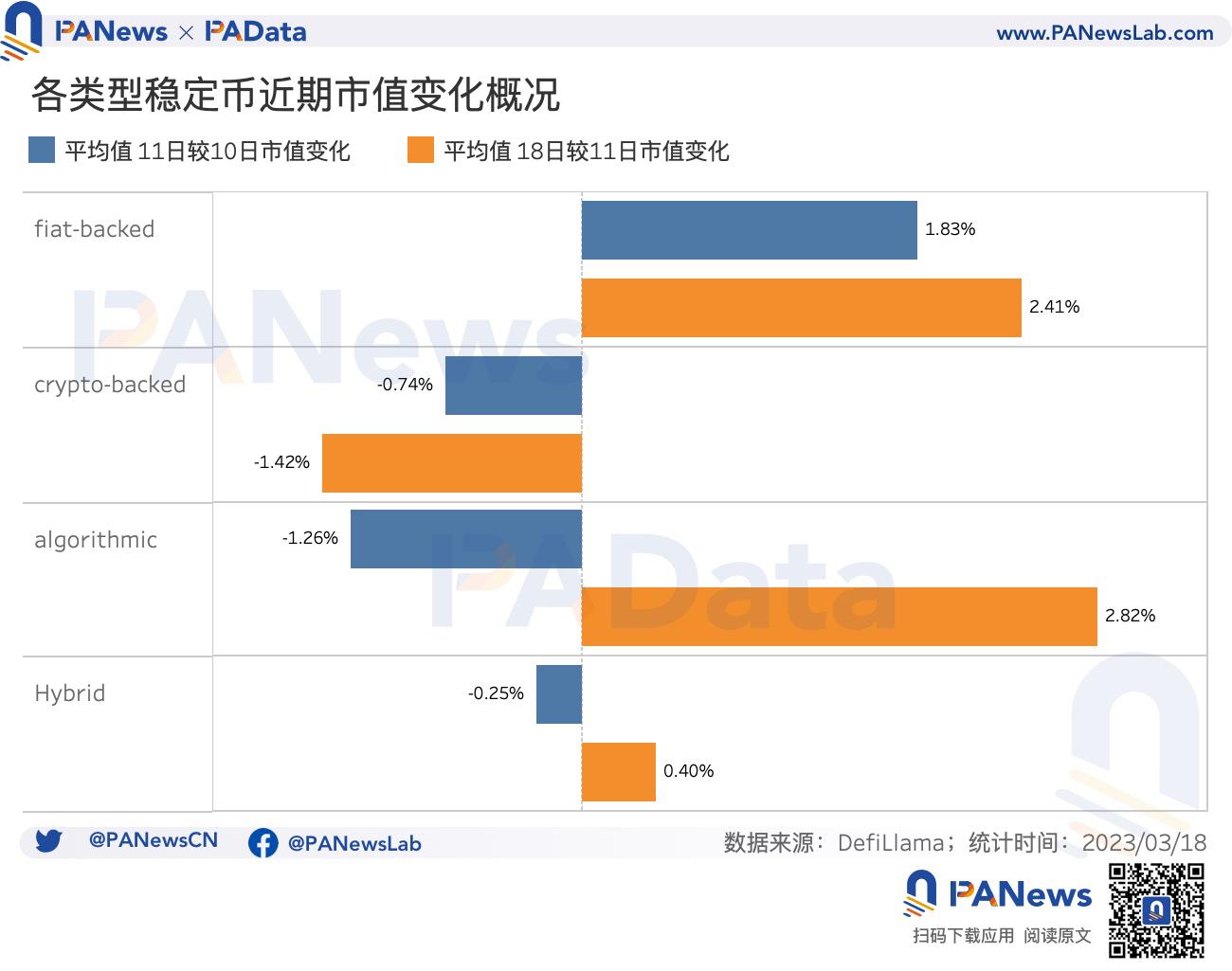

1) The average market value of six fiat-backed stablecoins increased, while the average market value of nine crypto-backed stablecoins decreased, indicating that market confidence in fiat-backed stablecoins remains relatively strong, while crypto-backed stablecoins are more adversely affected.

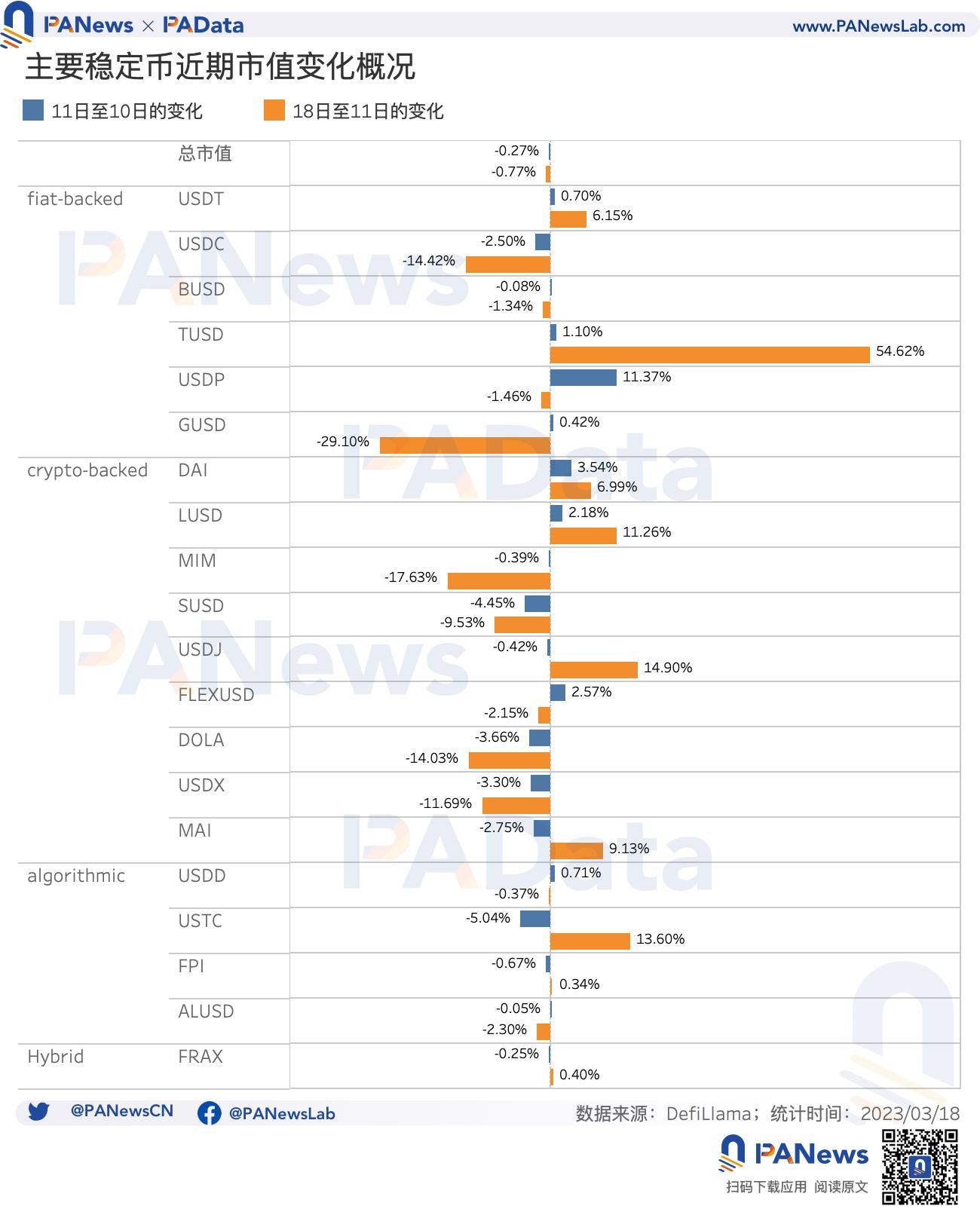

2) The current market value of USDC is about 47% of USDT, less than half. The market value of TUSD increased by over 54%, the largest increase. The market values of USDT, DAI, LUSD, USDP, GUSD, FLEXUSD, and USDD also saw growth.

3) On March 18, the stock of stablecoins on exchanges was approximately $21.461 billion, down 11.02% from $24.120 billion on March 11, indicating a rapid outflow.

4) The total locked value of 13 major stablecoins in three protocols—Uniswap v3, Curve, and AAVE v2—dropped from $3.464 billion on March 11 to $3.297 billion on March 18, a decline of about 4.83%.

5) On March 11, the total trading volume of stablecoin pairs on DEX reached $23.17 billion, far exceeding the average daily volume of around $1 billion at the beginning of the month. The trading between USDC, USDT, and DAI constituted the main liquidity path for stablecoins in DeFi during the crisis. This change also reflects users' confidence in fiat-backed stablecoins.

01. TUSD's Recent Market Value Surged Over 54%, USDC Crisis Further Adversely Affects Stablecoins Using It as Collateral

The de-pegging of USDC caused significant fluctuations in its own market value and that of other stablecoins. From the market value changes on March 11 compared to March 10, it can be observed that major stablecoins mostly declined. The "first domino" to fall in this chain reaction, USDC, saw its market value drop by 2.5%, but SUSD, DOLA, MAI, and USTC were more adversely affected, with market value declines ranging from 2.8% to 5.0%. Additionally, ALUSD, BUSD, FRAX, MIM, USDJ, and FPI also experienced slight declines in market value. Conversely, nine other stablecoins saw increases in market value that day, with USDP having the largest increase of over 11%. DAI, FLEXUSD, LUSD, and TUSD saw increases ranging from 1.0% to 3.5%.

The market value changes on March 18 largely continued the trends observed on March 11. For instance, the market values of USDT, TUSD, DAI, and LUSD continued to rise on March 18 compared to March 11, with TUSD seeing the highest increase of over 54%, and USDT rising by more than 6%. Meanwhile, the market values of USDC, BUSD, MIM, SUSD, DOLA, USDX, and ALUSD continued to decline on March 18 compared to March 11, with MIM experiencing the largest drop of over 17%, and USDC falling by more than 14%. Additionally, some stablecoins saw their market values shift from rising to falling after the crisis, such as USDP, GUSD, FLEXUSD, and USDD.

From the average market value changes of various types of stablecoins during these two periods, it is evident that the USDC crisis did not lead to a collective collapse of fiat-backed stablecoins. In fact, both on March 11 compared to March 10 and on March 18 compared to March 11, the average market value of the six fiat-backed stablecoins increased, with average increases of 1.83% and 2.41%, respectively. This indicates that market confidence in fiat-backed stablecoins remains relatively strong.

However, the USDC crisis has continuously adversely affected crypto-backed stablecoins, especially those that include USDC as collateral. In both the market value changes from March 11 to March 10 and from March 18 to March 11, the average market value of nine crypto-backed stablecoins decreased, with average declines of 0.74% and 1.42%, respectively.

Additionally, algorithmic stablecoins demonstrated a certain degree of resilience during this crisis. Although the average market value of four algorithmic stablecoins declined by 1.26% from March 11 to March 10, this was the largest average decline during that period. However, from March 18 to March 11, their average market value increased by 2.82%, marking the largest average increase during that time.

02. After the Crisis, USDC's Market Value is Less Than Half of USDT, Fiat-Backed Stablecoins are the Absolute Mainstream Among Over 100 Stablecoins

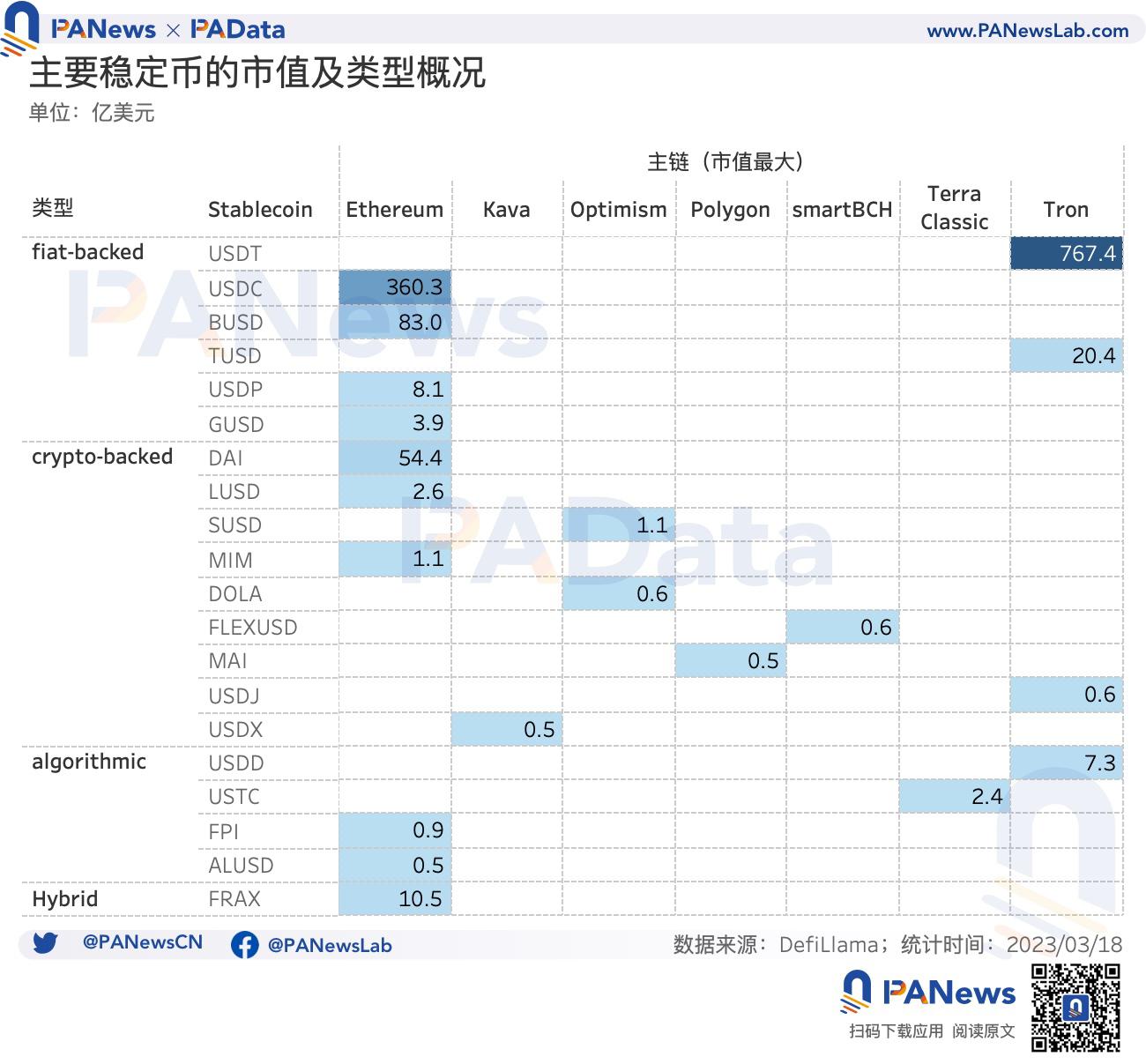

According to DefiLlama data, there are currently over 100 types of stablecoins in the market, with a total market value of approximately $133.388 billion. As of March 18, USDT remains the "leader" among stablecoins, with a market value of about $76.74 billion. USDC follows with a market value of approximately $36.03 billion. Together, they account for a total market value of $112.764 billion, approximately 85% of the total market value of stablecoins. After this crisis, the current market value of USDC is about 47% of USDT, which is less than half.

This still reflects a market with a clear "80/20 effect," so PAData will focus on analyzing the 20 stablecoins with the highest market values going forward.

Among these major stablecoins, besides USDT and USDC, the other stablecoins with market values exceeding $1 billion include BUSD, DAI, TUSD, and FRAX, with market values accounting for approximately 6.22%, 4.08%, 1.53%, and 0.78% of the total market value of stablecoins, respectively. Additionally, stablecoins with market values exceeding $100 million include USDP, USDD, GUSD, LUSD, USTC, MIM, and SUSD, while other stablecoins have market values ranging from $48 million to $88 million.

In terms of stablecoin types, these major stablecoins fall into four categories: fiat-backed stablecoins, crypto-backed stablecoins, algorithmic stablecoins, and hybrid stablecoins that are collateralized by crypto assets and algorithms.

Currently, the highest market value is still held by fiat-backed stablecoins, but among the high-value stablecoins, the largest number is crypto-backed stablecoins, totaling nine types. However, crypto-backed stablecoins typically accept fiat-backed stablecoins as collateral, so in this sense, these two types of stablecoins share a common origin.

Another new phenomenon is that besides Ethereum, which remains the main chain (the chain with the largest market value) for various major stablecoins including USDC, DAI, and FRAX, there are also several public chains with relatively large stablecoins. For example, due to transaction fee impacts, Tron has surpassed Ethereum to become the main chain for USDT, and it is also the main chain for TUSD, USDD, and USDJ. Additionally, there are significant stablecoins on Optimism, Polygon, and Kava. As a medium of liquidity, stablecoins are increasingly appearing on different public chains, which has positive implications for the development of DeFi on various public chains.

03. Exchange Stock Dropped to $21.4 Billion, Stablecoin Purchasing Power at a Short-Term Low

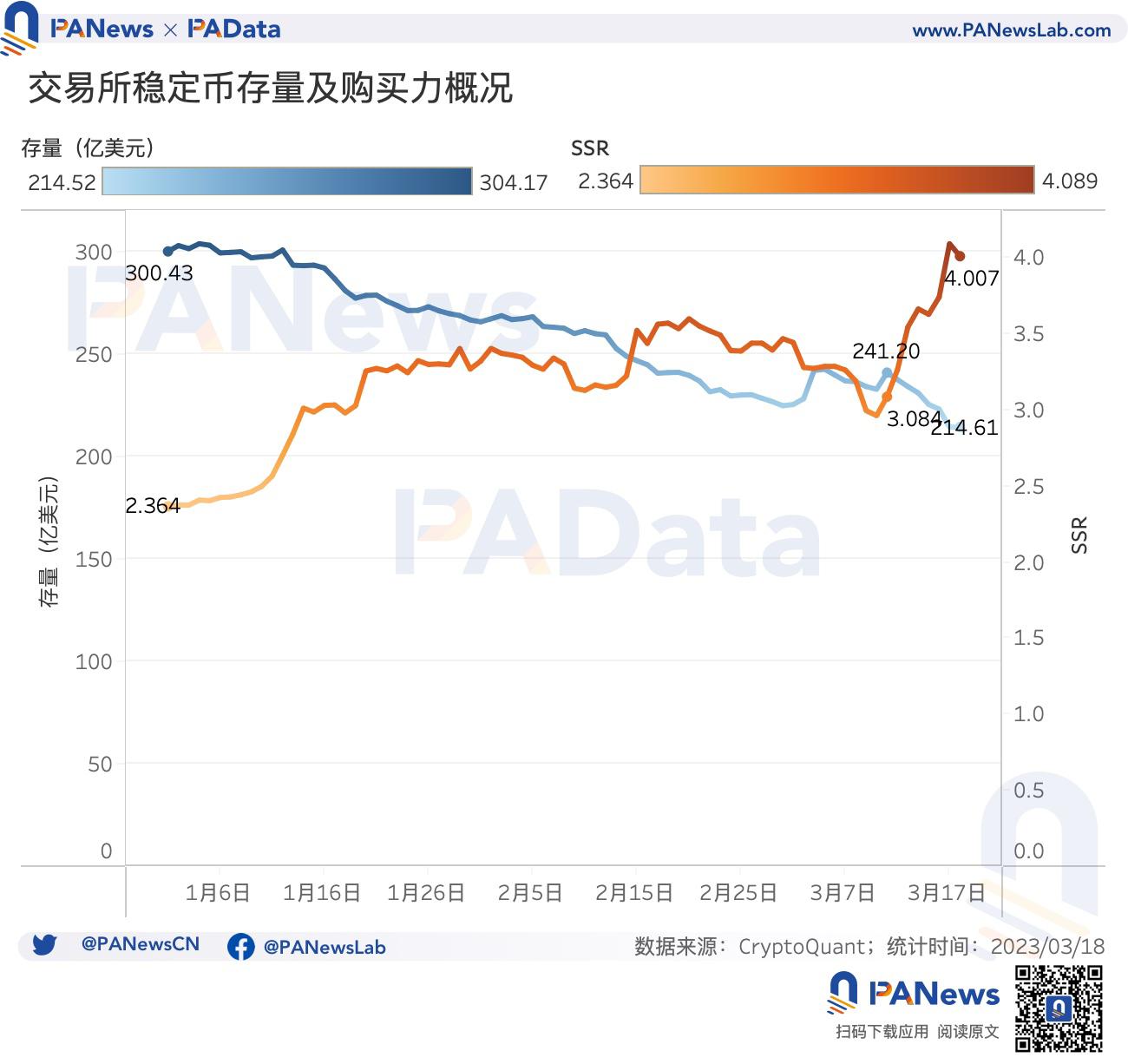

Blockchain analysis company Chainalysis published a blog post on the 16th stating that during market turmoil, capital outflows from centralized exchanges often surge, as users may worry about not being able to access their funds if the exchange collapses. According to CryptoQuant's monitoring of stablecoin stock on exchanges, this statement is indeed corroborated.

Statistics show that on March 18, the stock of stablecoins on exchanges was approximately $21.461 billion, down 11.02% from $24.120 billion on March 11, the day USDC de-pegged, indicating a rapid outflow. Interestingly, however, the stock of stablecoins on exchanges increased by 3.49% on March 11 compared to March 10, adding $814 million. This may be related to users seeking safety by exchanging stablecoins on the exchange on March 11.

Additionally, this stablecoin crisis has also impacted the purchasing power of stablecoins. The Stablecoin Supply Ratio (SSR) is a commonly used indicator to measure the market's potential purchasing power, representing the ratio of BTC market value to the total market value of all stablecoins. A lower SSR indicates a more ample supply of stablecoins, stronger potential purchasing pressure, and a higher likelihood of price increases.

As of March 18, the SSR was approximately 4, near the upper Bollinger Band (200, 2), and had risen about 30% from 3.08 on March 11. This recent increase is significant. This is related to the recent rebound in BTC prices; in the context of a rapid short-term increase in asset prices, the overall market value of stablecoins has declined due to the de-pegging crisis, resulting in a slight increase in SSR while actual purchasing power has decreased. This adds more uncertainty to the market's return to a bull market.

04. Trading Volume of Stablecoins on DEX Surged to $23.1 Billion, Current Lending Rates Dropped to Early Month Levels

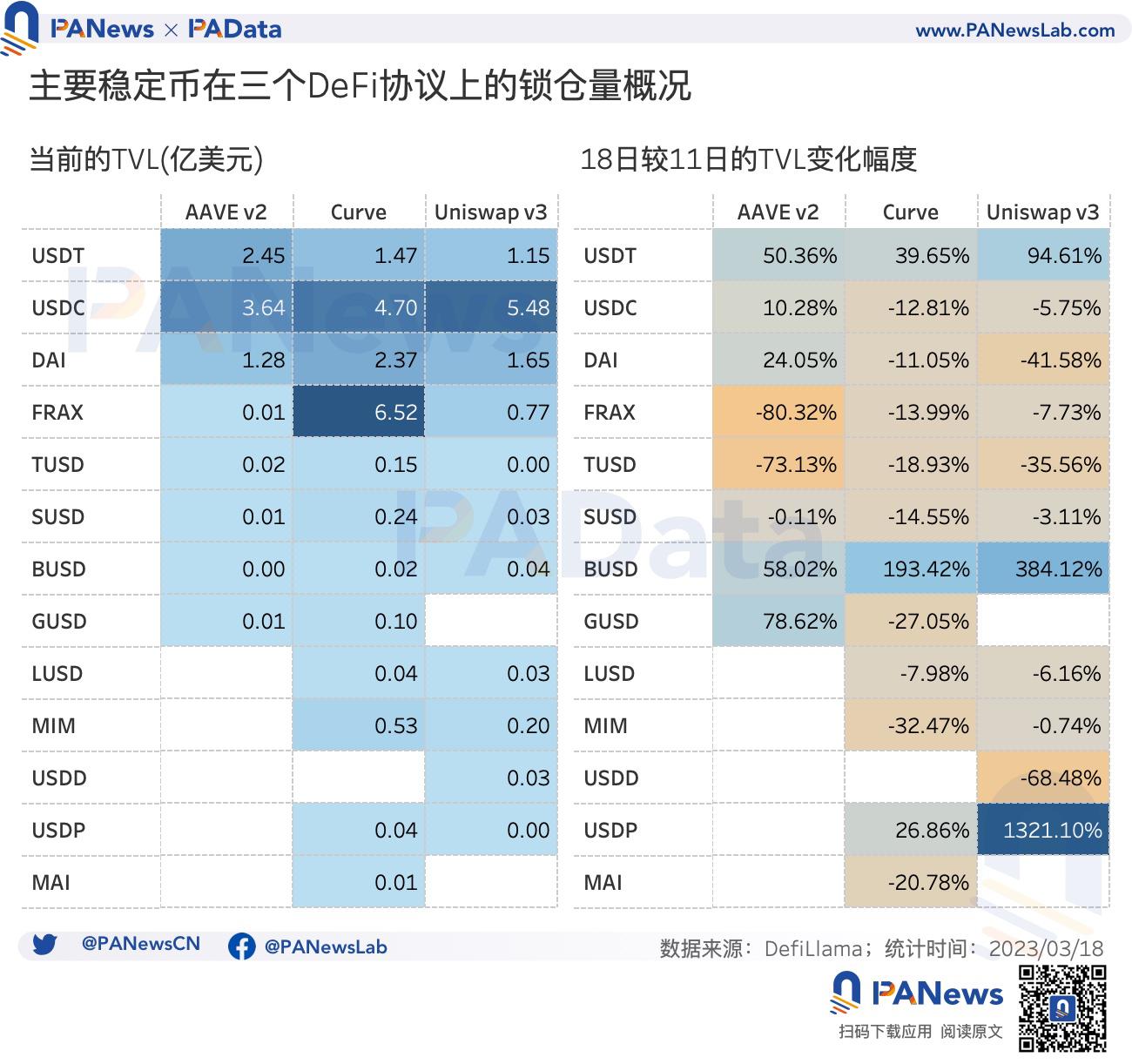

Under the crisis, not only did stablecoins flow out of exchanges in large quantities, but the total locked value of stablecoins in three DeFi protocols closely related to stablecoin trading—Uniswap v3, Curve, and AAVE v2—also decreased, though to a much lesser extent. According to statistics, the total locked value of 13 major stablecoins in these three DeFi protocols dropped from $3.464 billion on March 11 to $3.297 billion on March 18, a decline of about 4.83%.

Among these, some stablecoins' locked values on March 18 compared to March 11 are noteworthy. For instance, during this period, USDT's locked value in the three DeFi protocols significantly increased, with the highest increase exceeding 94% in Uniswap v3 and nearly 40% in Curve. In contrast, USDC's locked value decreased in both Uniswap v3 and Curve, with a significant decline.

Moreover, the locked values of FRAX, TUSD, SUSD, LUSD, MIM, USDD, and MAI all decreased in these three protocols, with FRAX and TUSD experiencing over a 70% drop in AAVE v2. Conversely, the locked values of fiat-backed stablecoins BUSD and GUSD increased.

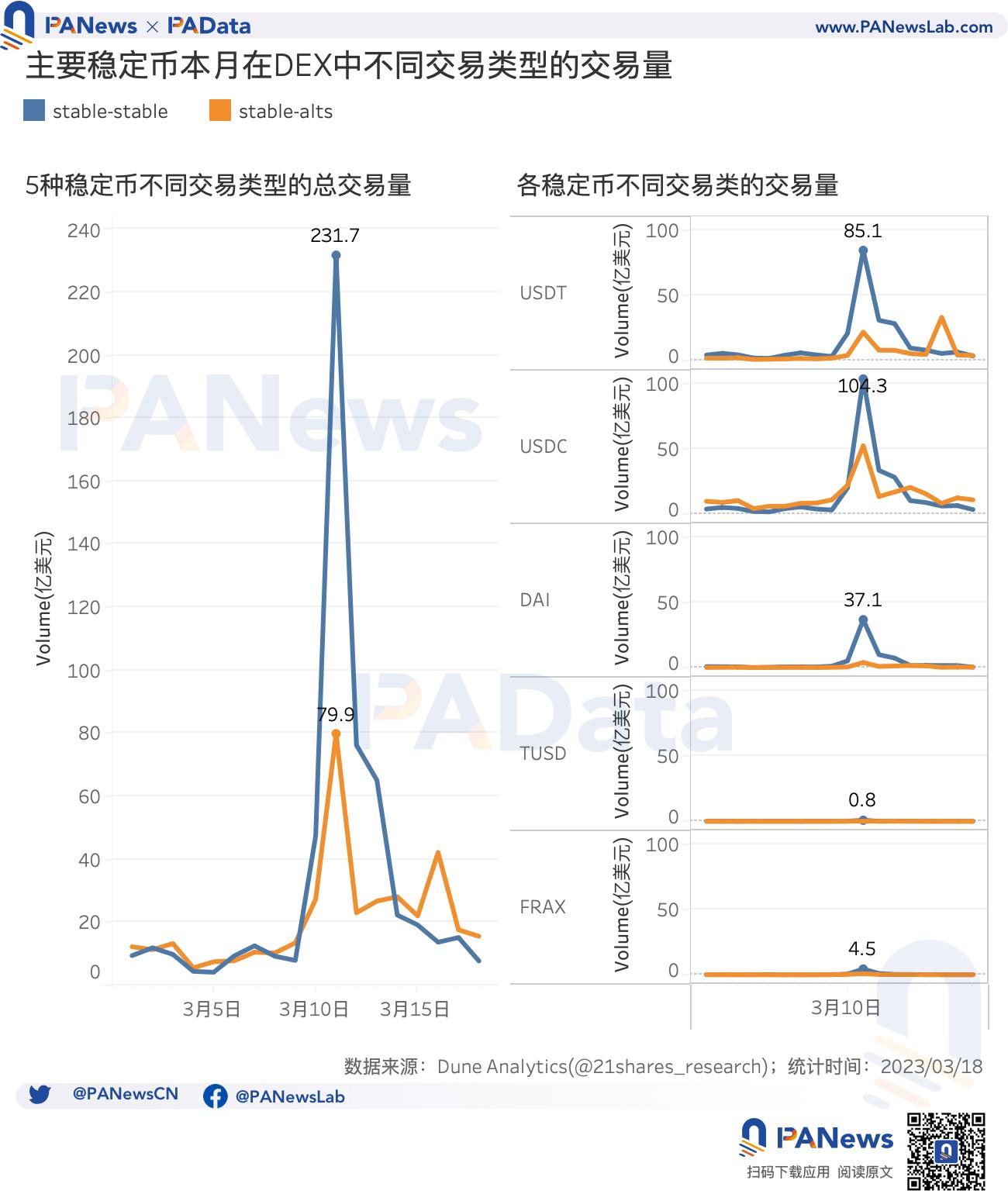

The types of stablecoin trading pairs on DEX can more accurately capture the recent flow of stablecoins in DeFi. On March 11, the total trading volume of stablecoin pairs (stable-stable) on DEX reached $23.17 billion, far exceeding the average daily volume of around $1 billion at the beginning of the month. Additionally, the total trading volume of stablecoins against other tokens (stable-alts) on that day also reached $7.99 billion, creating a small peak.

Overall, after the de-pegging of USDC, trading between stablecoins became extremely active. If we further observe the trading volume of stablecoin pairs among major stablecoins, we can see that on March 11, the trading volume of USDC stablecoin pairs reached $10.43 billion, while USDT reached $8.51 billion, and DAI approximately $3.71 billion. It is reasonable to speculate that trading among these three stablecoins constituted the main liquidity path for stablecoins in DeFi during the crisis.

This aligns with Chainalysis's earlier viewpoint that the surge in USDC purchases on DEX was due to confidence in fiat-backed stablecoins, with some users buying when USDC was relatively cheap, betting that it would re-peg to the dollar.

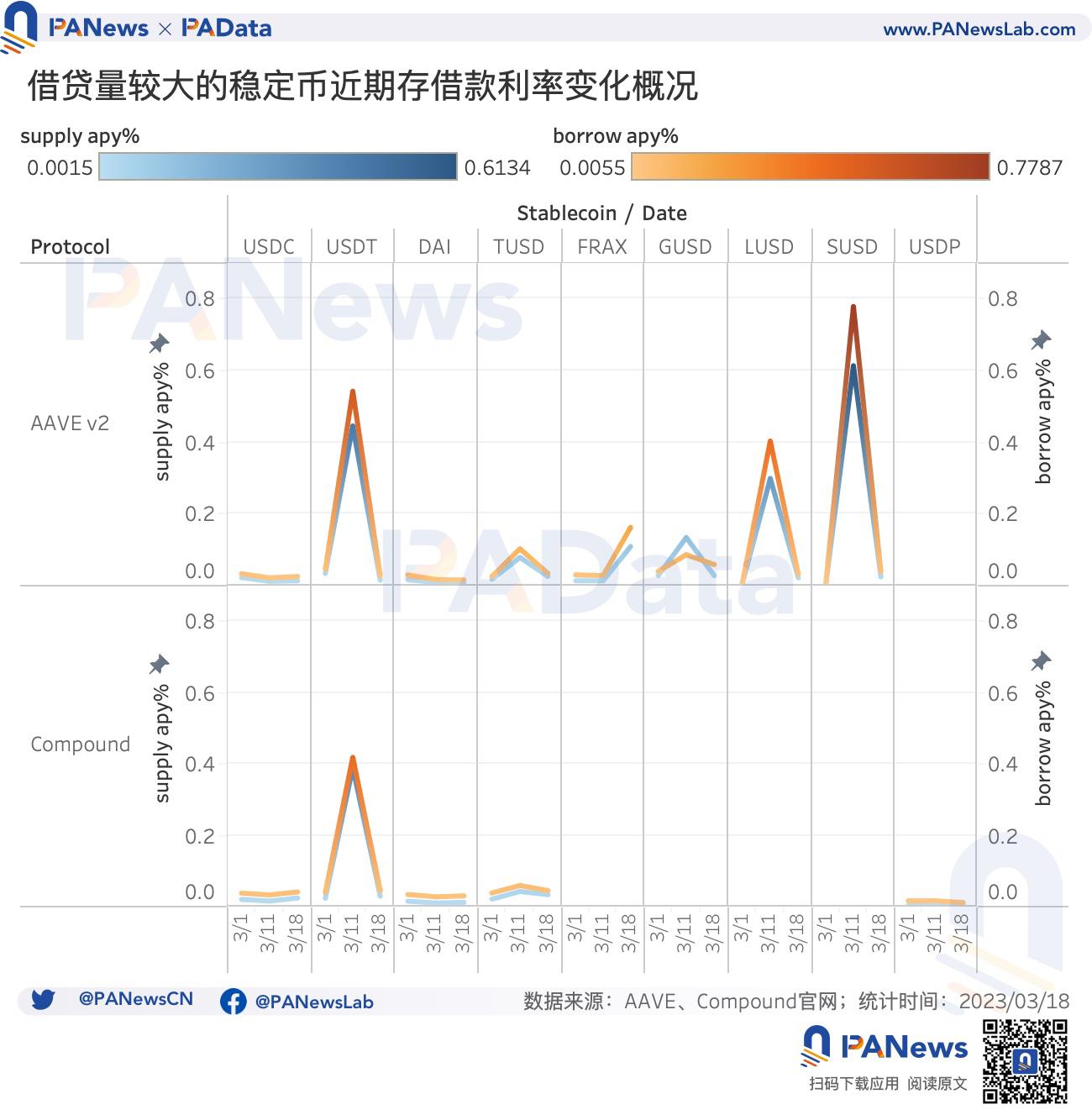

The de-pegging of USDC also had a significant impact on the lending market's deposit and borrowing rates. The trends in deposit and borrowing rates for USDC and DAI were similar to a "V" shape, indicating that changes in borrowing demand were comparable to or smaller than changes in deposit volume, but overall fluctuations were not large. In contrast, the deposit and borrowing rates for USDT, TUSD, GUSD, LUSD, and SUSD exhibited a "Λ" shape, indicating that during the crisis, changes in borrowing demand were greater than changes in deposit volume, leading to relative liquidity shortages. However, the deposit and borrowing rates in the lending market have now returned to early month levels.

Stablecoins serve as the primary "bridge" between the crypto world and fiat currencies, and components that are more closely linked to the real world, such as regulated USD stablecoins, are more likely to become points of vulnerability in the system. However, because of this, their ability to withstand risks is stronger than purely crypto-based upper-layer assets, as centralized management can more effectively mitigate such risks. Just as USDC was saved from crisis due to multi-party investments in SVB, this is the source of user confidence in regulated fiat-backed stablecoins and also the reason why stablecoins are increasingly being scrutinized by regulatory authorities.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles