Unveiling Trade Joe V2: How to Capture a Large Share of Arb Trades from Uniswap?

Trade Joe V2 became popular because it seized a large share of Arb trading from Uniswap, causing the coin price to double rapidly.

Trade Joe V2 became popular because it seized a large share of Arb trading from Uniswap, causing the coin price to double rapidly.Author: CapitalismLab

Recently, Trade Joe V2 has gained popularity by seizing a large share of Arb trading from Uniswap, causing its token price to double rapidly. How did it achieve this? What should be noted when providing liquidity?

This article will take you through the mechanisms of Joe V2, analyze how it can capture a large share in $ARB trading, and discuss the advantages and disadvantages of the product to help you better understand DEX.

A brief overview of Trade Joe V2:

AMM is similar to an order book, using discontinuous liquidity.

Minimum price precision is based on a ratio rather than a fixed value.

Vertical aggregation of liquidity brings better composability.

Liquidity incentives are based on the trading fees earned by LPs and effective TVL.

1. AMM Mechanism

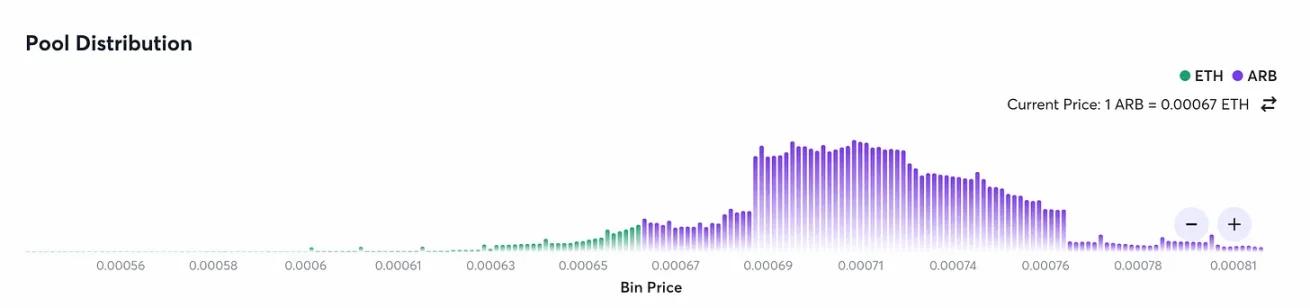

Next, let's take the ARB/ETH 20 bps pool in Joe V2 as an example for in-depth analysis. First, we look at the liquidity distribution of the pool, which at first glance resembles UNI V3.

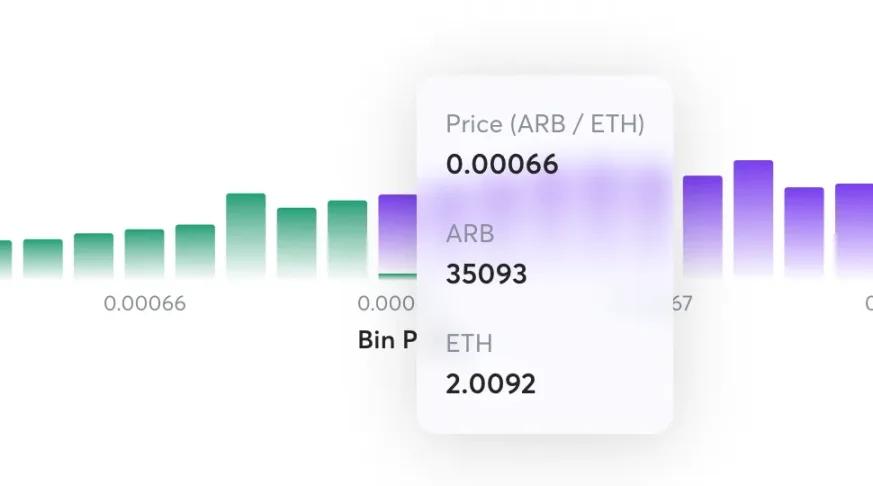

So, what is the fundamental difference? A long bar (bin) in Joe V2 corresponds to a single price point, meaning that unless you exhaust the liquidity of this bin, the price will not change. For example, in the image below, we can see that there are about 35k Arb and 2 ETH in this bin. If someone sells Arb worth 2 E at 0.00066, the trading bin will move left by one position, and the price will change.

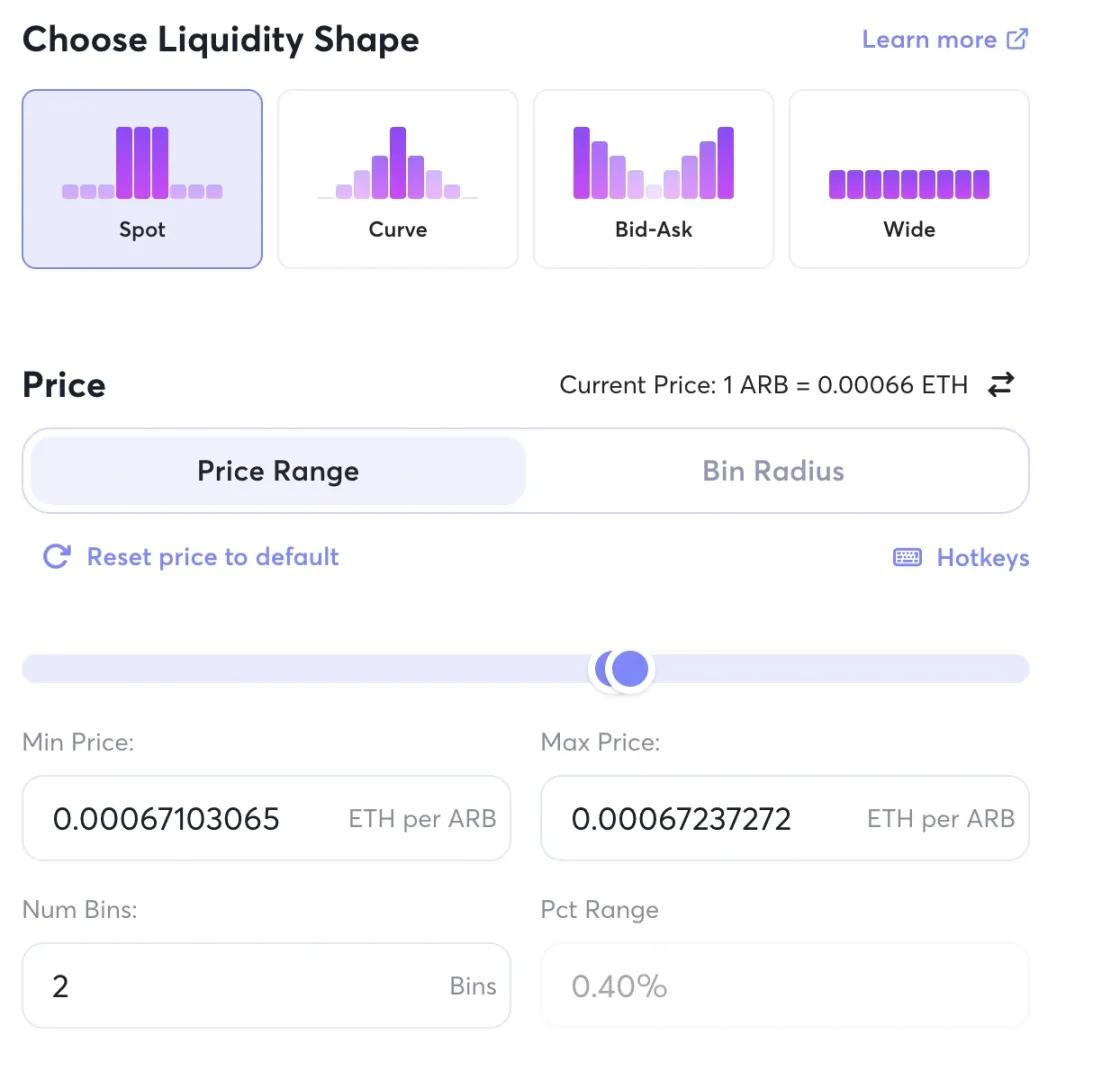

Let's try adding liquidity to this pool and find that we can add single-point liquidity, meaning the added liquidity is at a single price, which is essentially like placing a Maker order in an order book. So what about the Pct Rage = 0.20% next to it?

If we slightly move the slider on the right to expand the price range to 2B in, we can calculate the relative difference between the two prices.

(0.00067237272 - 0.00067103065) / 0.00067103065 = 0.20%

This means that 0.20% is the minimum price precision.

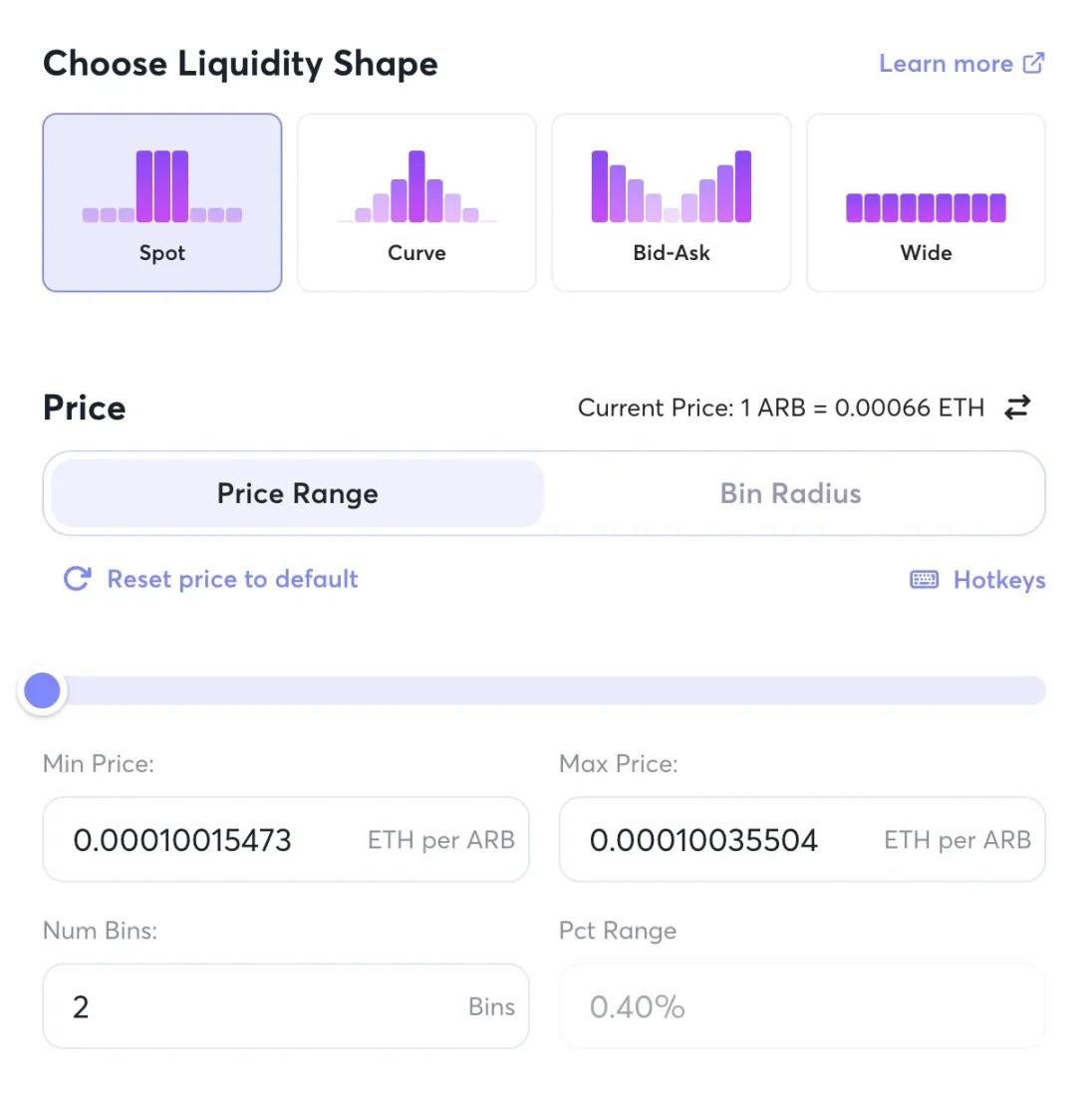

Now let's look at a situation where the price deviates significantly from the current price, such as at ARB/ETH = 0.0001. We can conclude that

(0.00010035504 - 0.00010015473) / 0.00010015473 = 0.20%

Indeed, it can be understood that the price difference at any position is 0.2%, based on a ratio rather than a fixed value. This is quite different from traditional order books, which typically provide a fixed minimum precision, such as 0.01 USDT.

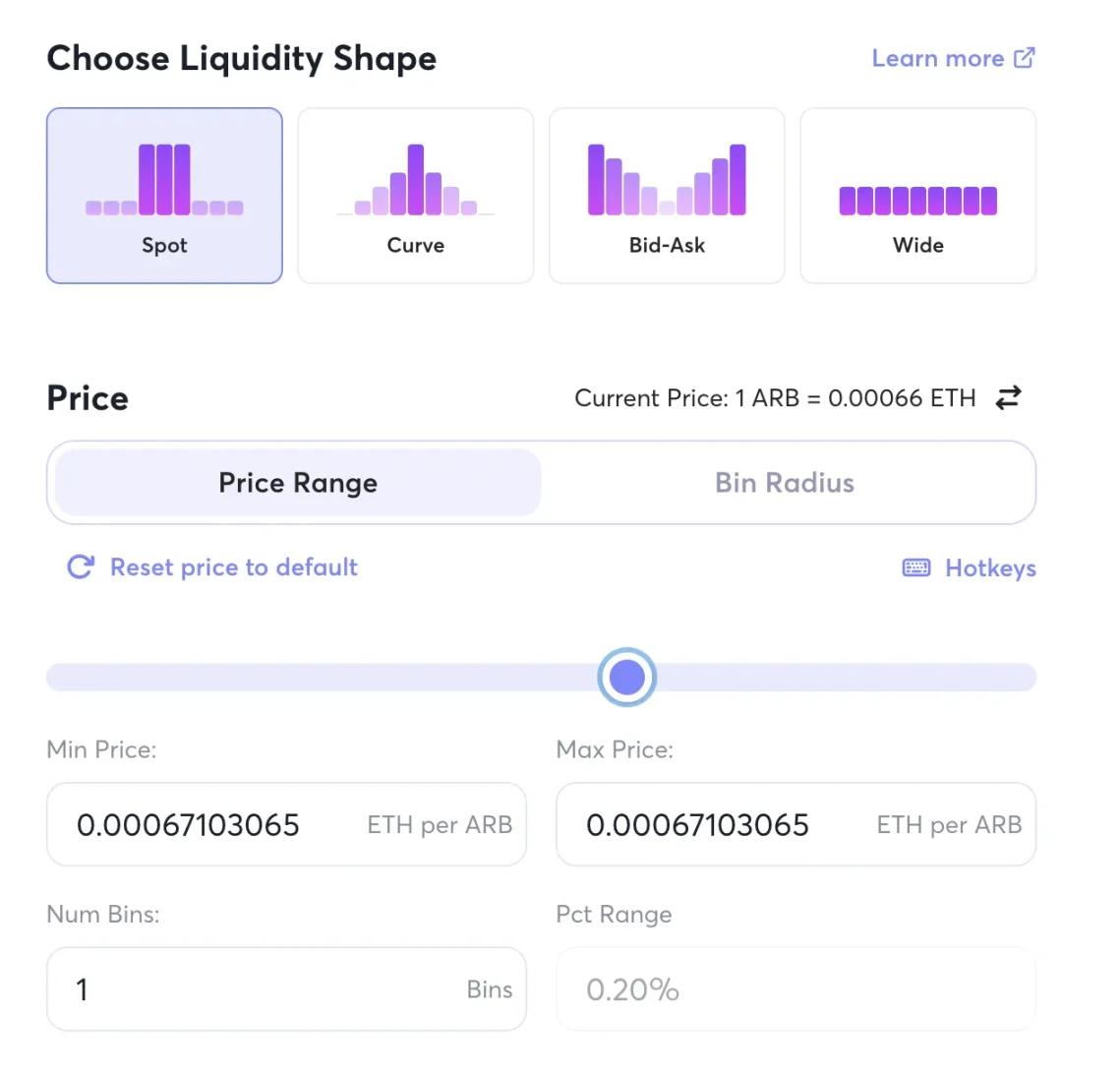

Joe's UI also provides four ways to add liquidity. By clicking the "learn more" in the upper right corner of the image, you can learn about their detailed definitions. However, aside from Spot, the other four methods use parameters set by the official and are uncontrollable. Therefore, I recommend using Spot, which is similar to UNI V3; at most, you can deposit several different price ranges. Additionally, Joe V2 currently has liquidity incentives, which must be considered for returns.

2. Liquidity Incentives

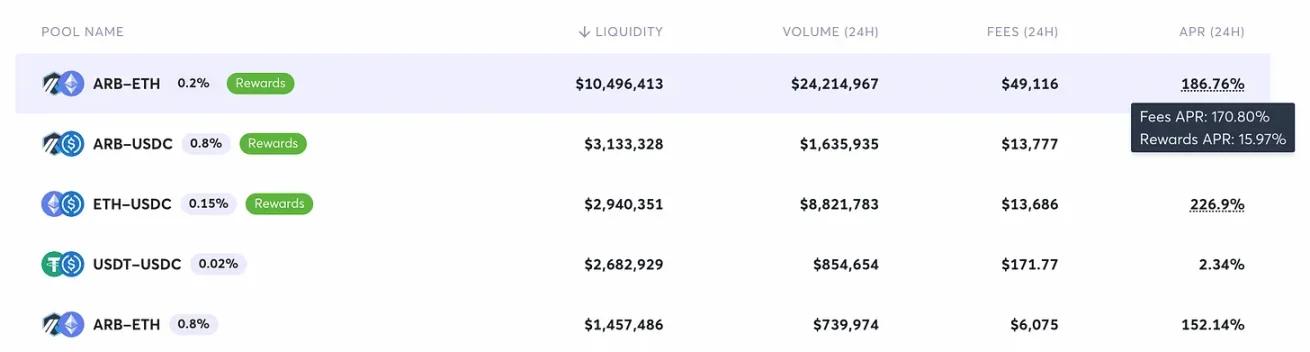

Currently, pools with the "Rewards" label have liquidity mining incentives.

The liquidity mining incentive distribution model of Joe V2:

Scores are calculated based on the actual trading fees earned by LPs and MakerTVL, as shown in the image below.

MakerTVL currently only considers the TVL within the current price ± 5 bins. For example, in the case of Arb/ETH with a 0.2% bin width, only the TVL within ±1% of the current price will be counted.

At the end of an Epoch, the scores within that Epoch are tallied and distributed proportionally.

This means that if you want to obtain liquidity incentives, you still need to provide liquidity relatively concentratedly.

For more details, see the documentation.

3. Why $ARB Trading Captured a Large Share

Assuming the current market is continuously buying Arb, Uniswap Arb/USDC = 1.005, and let's say Joe V2's price precision is 1%, with bin distribution as [0.99, 1.00, 1.01 …]. At this time, Joe's current bin should be 1.00, which is 0.5% cheaper than Uni. As long as the trading fee is less than this difference, buying Arb through aggregators like 1inch will naturally prioritize Joe; conversely, if selling Arb, Joe has no advantage. This means it has an advantage in one-sided markets during high volatility, while it performs relatively mediocre in low volatility markets.

Additionally, Joe has set a fee of 0.2% for the ARB/ETH trading pair, while at that time, due to high volatility expectations, UNI could only set fees of 0.01% / 0.05% / 0.3% / 1%, with most LPs positioned above 0.3%, which is a disadvantage compared to Joe's 0.2%.

The frequent exchange rate advantage during high volatility + relatively low fees allowed Joe V2 to capture a large share at the beginning of ARB 0.00. Currently, as volatility decreases, its exchange rate no longer has a frequent advantage; UNI V3 LPs returning to 0.05% fee pools have also basically lost their fee advantage. Fortunately, Joe has built a reputation, and with a good incentive mechanism, it has provided the project team with greater operational space.

4. Product Advantages and Disadvantages

In fact, the advantages and disadvantages brought by its AMM mechanism have already been explained in the discussion of Arb trading shares. This section discusses other aspects:

Advantages:

Vertical aggregation of liquidity brings better composability.

High efficiency + support for incentives can attract incentives from partners, such as potential benefits from the LSD war.

Disadvantages:

Lack of mature mechanisms for token empowerment like Bribe, resulting in limited benefits for token holders.

Relatively large impermanent loss.

5. Advantage: Composability

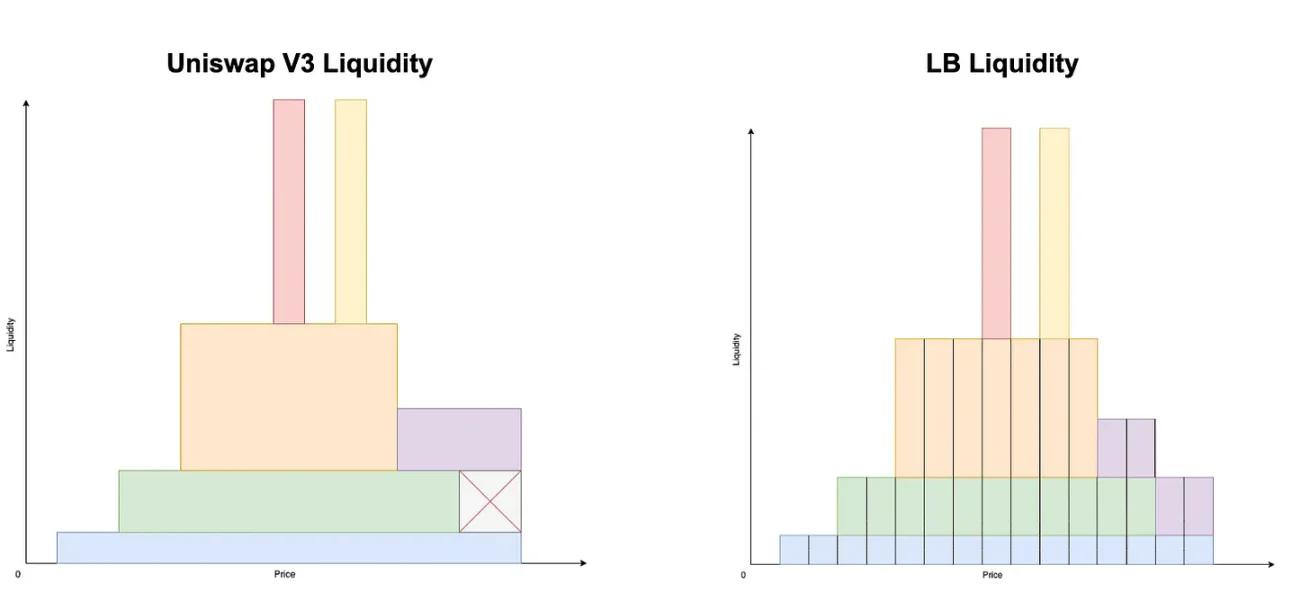

In Joe V2, liquidity is vertically aggregated by each bin, while in Uniswap V3, liquidity is horizontally aggregated. The main benefit of vertical aggregation is that it allows liquidity to be interchangeable.

Looking at a specific transaction of adding liquidity, we find that after the user adds ETH/USDC, Joe returns a large number of different Token IDs of ERC-1155 LBT to the user, reflecting the user's liquidity distribution at different price levels.

This is quite different from returning a single NFT in UNI V3. Because the same Token ID represents liquidity at a single Bin/price level, it is homogeneous and has better composability.

Advantage: Expectations for Partner Incentives

High efficiency of concentrated liquidity + support for incentives is expected to attract partners with liquidity needs, such as LSD, to provide incentives. For example, the previous UNI V3+ incentive model Kyberswap obtained incentive distribution second only to Curve from Lido (see the tweet below) and captured a significant share of LSD trading volume in Alt-L1/L2.

Thus, Joe V2 theoretically has the opportunity to provide similar value, thereby increasing TVL and trading volume.

6. Disadvantage: Token Empowerment Issues

As I mentioned in my previous tweet, pure spot DEXs find it quite difficult without additional empowerment mechanisms like bribes, having TVL and trading volume but unable to convert them into benefits for token holders.

Currently, Joe generates revenue through fee sharing, but taking too much may inevitably affect its share. Although Joe has Ve Joe, it does not replicate Curve's path of going down the Bribe route, and it does not seem to be very successful at present, so token empowerment remains an issue.

Disadvantage: Relatively Large Impermanent Loss

As mentioned earlier, in one-sided markets, Joe V2 has a frequent exchange rate advantage, but this actually incurs greater impermanent loss for LPs, equivalent to selling coins at a cheaper price.

Joe will reasonably set fees to compensate for this, such as a 0.8% fee for ARB/USDC with a 1% bin width and a 0.2% fee for ARB/ETH with a 0.2% bin width. Additionally, this point is not easy to notice, so it's not too bad (laugh).

Conclusion

Trade Joe V2 has achieved differentiated advantages in specific scenarios compared to UNI V3 in terms of efficiency, and the advantage of high composability heavily relies on its own scale. Therefore, future attention should be paid to the project team's BD operations to see if they can BD enough cooperative incentives to build a growth flywheel.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles