AC Capital: With the upgrade in Shanghai imminent, why is LSD highly anticipated?

How will the LSD agreement evolve?

How will the LSD agreement evolve?Written by: Bittracy, AC Capital Research

The decentralized world has just experienced a historic bull market, presenting us with countless innovations. Compared to the chaos after the bull-bear transition in 2018, this time the decentralized world has various foundational setups such as DeFi, NFT, derivatives, Launchpad, and Incubator. As protocols like Layer2, LSD, and ZK gradually mature, the on-chain world is showcasing richer content. After 2023, on-chain activity has significantly increased, and the rise in asset prices has driven up trading volumes. The switch in market volatility is quite interesting; from a macro perspective, the prices of digital assets like BTC show a correlation with the Nasdaq index. After the decline in the vitality of the U.S. economy, the Federal Reserve's firm stance on interest rate hikes, due to existing inflationary pressures, has created some suppression on market sentiment.

Market Environment for the Rise of LSD

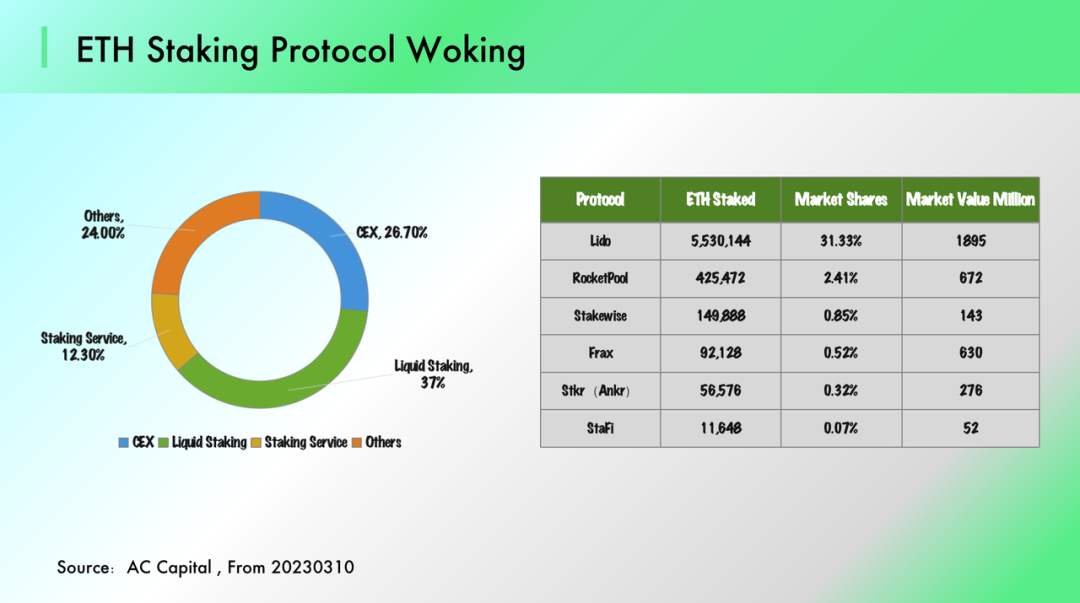

In Q4 of 2022, practitioners could clearly see investors' preferences: institutions were more inclined towards infrastructure rather than heavily liquidity-dependent agreements like GameFi and NFT; projects like MPC wallets, cross-chain bridges, ZK, and middleware were the most sought after in the market. It is worth mentioning that there is a clear differentiation among infrastructure agreements. After experiencing black swan events like Terra and FTX, investors' risk appetite has been significantly suppressed, and everyone hopes to see agreements that can generate positive returns to support their own development rather than reaching out for money from investors. From a business model perspective, the revenue growth of agreements like ZK and wallets relies on active on-chain transactions, and agreements with strong beta attributes find it difficult to generate sufficient revenue during bear markets. Against this backdrop, LSD agreements represented by Lido have rapidly developed, benefiting from a clear business model and established revenue capabilities. Before the market warmed up, Lido's market capitalization had already surpassed MakerDao, ranking within the top 50.

The Rise of LSD Protocols

Looking back at the last bull market, DeFi, Layer 1, and GameFi took turns leading the market. At the beginning of 2023, LSD (Liquid Staking Derivatives) performed brilliantly in the secondary market, becoming the focus of investors. First, the staking rewards of Ethereum itself are incredibly enticing. From an absolute scale perspective, GAS/MEV and staking rewards provide developers with enough market space to capture value. "A broad market space (valuation) + rapid TVL growth (performance)" indicates a high certainty investment opportunity, which is why we have seen LSD agreements represented by Lido and Frax shine in the past three months. This article will focus on analyzing the operational models of LSD protocols and discussing and analyzing high-quality LSD protocols.

What is an LSD Protocol? LSD (Liquid Staking Derivatives) refers to liquid staking derivatives, which aim to help tokens already staked on-chain release liquidity and expand returns. In the blockchain world, network interactions need to be achieved through consensus mechanisms, and POS protocols require nodes to obtain the right to validate transactions by staking tokens. Taking Ethereum as an example, in the ETH 2.0 setup, users need to stake 32 ETH and run an independent node server to become a validating node and earn staking rewards. First, the requirement of 32 ETH poses a high demand on users' capital, and independently maintaining node equipment requires considerable effort. At the same time, staked ETH cannot be withdrawn before the Shanghai upgrade, which creates liquidity pressure for Ethereum stakers. To address these issues, LSD protocols help users obtain staking rewards and release liquidity of locked tokens by creating derivative tokens.

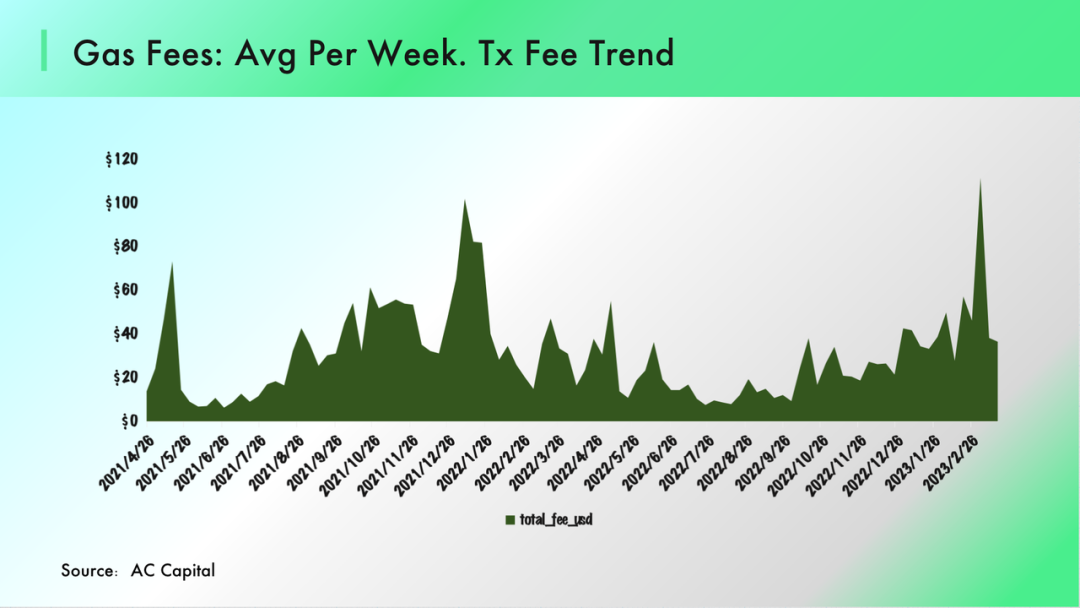

Why does the LSD Protocol present investment opportunities? Currently, Ethereum's staking rate is only 14%, compared to the staking ratios of other POS public chains (over 50%), the market space for Ethereum nodes' staking has not been fully opened. The earnings of Ethereum nodes come from the amount staked and fee income. Assuming a neutral hypothesis, if after the Shanghai upgrade, Ethereum's staking rate can reach 50%, this would represent a 257% increase from the current level, and the Consensus Layer Reward for operating nodes is expected to increase by over 60% (the Consensus Layer Reward is not linearly related to the amount staked). At the same time, after the Shanghai upgrade, a more flexible mechanism will further compress the price difference between ETH and its derivatives, helping to activate the ecological applications of LSD tokens. Therefore, in the foreseeable future, the profit margins and development potential of LSD protocols are expected to increase.

How to Evaluate LSD

How should we define a good LSD protocol? This section will answer this question by breaking down and analyzing what we consider to be high-quality LSD protocols.

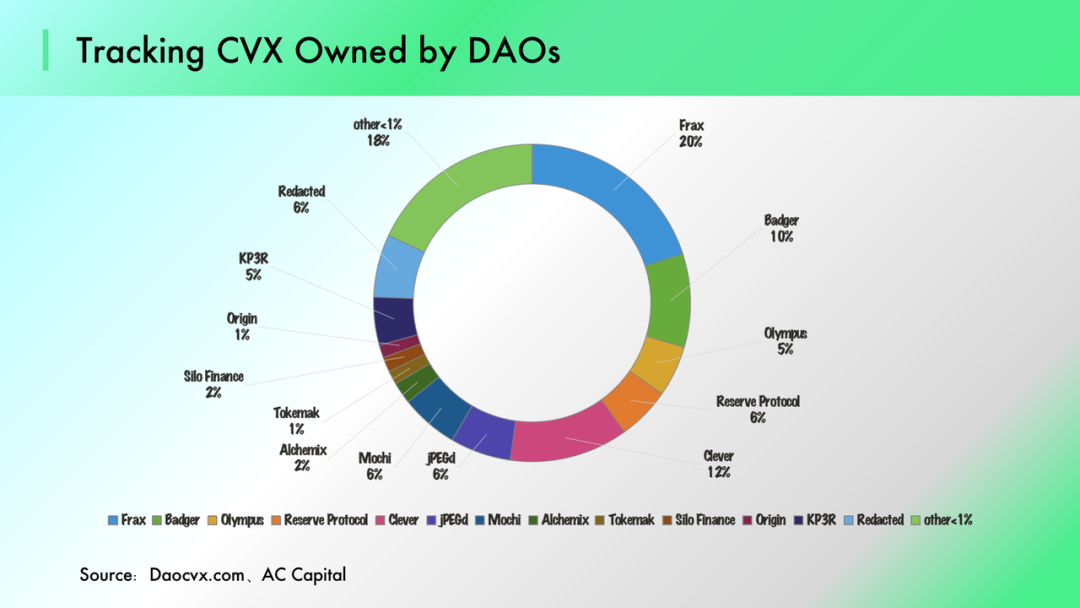

(1) What makes a good LSD protocol - Taking Convex as an example

The core value of LSD protocols lies in helping to solve the pain points of foundational protocols: Due to Curve's unique business model and token economics, several issues arise in practical use. For investors, obtaining investment returns from holding CRV tokens is very challenging. If they want to avoid dilution of their token holdings, they must lock CRV for a long time to gain Boost Revenue (a lock-up period of 4 years is required to achieve maximum returns), which means investors will sacrifice a lot of time and become deeply bound to Curve. For ecosystem builders, Curve provides a trading venue for DeFi protocols and participates in CRV distribution, but this requires developers to hold a large amount of VeCRV to ensure the effectiveness of their participation (ensuring CRV emissions for opening pools), which places a significant financial burden and conversion cost on protocols in their early development.

The development of LSD is built on the prosperity of foundational protocols: The operational model of LSD protocols involves disassembling the economic model of the underlying protocol to help token holders achieve better returns and convenience. Therefore, the scale of the underlying protocol determines the development space of LSD protocols. Curve, as an important stablecoin trading venue on Ethereum, accumulates massive liquidity and trading volume, becoming a crucial site for deploying DeFi protocol liquidity pools. During the "DeFi Summer" development period, a large number of liquidity pools gathered on Curve, with trading fees and CRV rewards providing developers with ample market space.

Curve's dilemma and Convex's solution: Convex effectively addresses the two issues mentioned above. First, regarding the problem of Curve's excessive inflationary attributes, Convex locks a large amount of CRV through CRV/cvxCRV (LSD model), allowing investors to achieve Max Boost Revenue while immediately obtaining cvxCRV to release liquidity. Secondly, concerning Curve's governance issues, Convex separates Voting Power from VeCRV and maps governance rights to CVX, allowing developers who wish to open liquidity pools on Curve to trade governance rights through a Bribe Marketplace. In this way, Convex firmly grasps the control of Curve, where the strong continue to strengthen in boosting yield, continuously attracting users to deposit CRV into Convex. Meanwhile, the Bribe Marketplace brings a steady stream of income to Convex, which has disassembled and reconstructed the economic model and operational mechanism of the underlying protocol, helping users maximize their staking returns while creating a sufficiently liquid secondary market for LSD. Bittracy believes this may be the most successful LSD protocol of 2021.

(2) Core advantages of the LSD track development - Taking Frax as an example

Frax was initially launched in 2019. Compared to MakerDao, Frax's biggest difference lies in its dual-token mechanism supporting fractional-algorithmic stablecoins (partially collateralized). To achieve value anchoring for stablecoin governance and improve capital utilization efficiency, Frax Finance innovatively introduced an automated market operation (AMO) mechanism in its V2 version. Under this mechanism, AMO can flexibly adjust the ratio of USDC and FRAX in the FRAX3CRV Curve, thereby ensuring the anchoring relationship between FRAX and USDC.

In the past three months, we can clearly see that Frax Finance's TVL has rapidly increased at a steep rate. If Lido enhances user staking yields through multi-layer nesting with AAVE, then Frax achieves user yield enhancement through its binding with Convex.

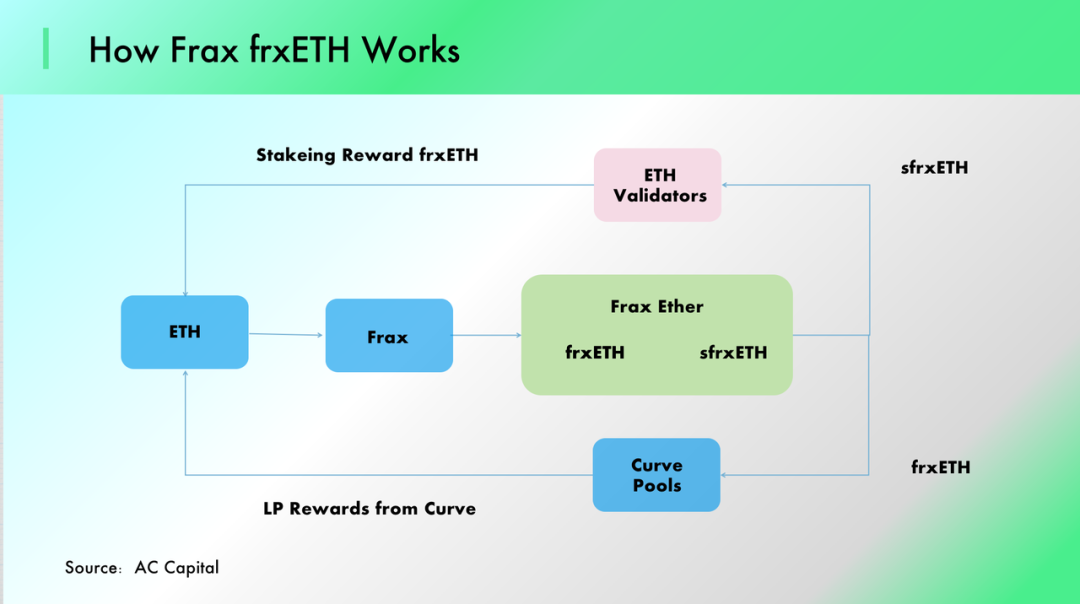

Frax's LSD model: Participants stake ETH in Frax Finance to obtain frxETH, after which they have two choices;

Choice one: Convert frxETH into sfrxETH to obtain ETH staking rewards;

Choice two: Stake frxETH and ETH into the Curve pool to earn mining rewards;

Frax provides higher yields for users by enhancing CRV emissions through Convex, competing directly with other LSD protocols based on yield advantages (price wars). In the early stages of protocol development, this approach has proven effective (the amount of ETH staked on the Frax protocol has rapidly increased). As previously mentioned, Curve's emission rights are determined by Convex, and Frax's advantage lies in holding the largest amount of CVX, thus achieving control over CVX. On the other hand, participants entering the Curve pool inadvertently provide sufficient liquidity for frxETH/ETH, ensuring that frxETH can anchor the value of ETH in the secondary market, which is the foundation for the widespread liquidity of LSD tokens.

Conclusion

LSD protocols are innovations based on mature protocols, and the scale of the protocol determines the development space of LSD: For example, Lido exists to maximize staking returns for Ethereum network stakers, while CVX captures the value of Curve. Therefore, the scale of the foundational protocol largely determines the ceiling for LSD protocols, and promising LSDs need to be built on successful foundational protocols.

Boosting yield determines the core competitiveness of LSD protocols: Value will ultimately stabilize through its ability to earn a share of protocol income when staked in staking contracts. The battlefield for LSD lies in which can capture the most foundational tokens. Thus, the core competitive advantage of LSD lies in capturing and locking, while the revenue capability and token mechanism determine the capturing and locking ability of LSD protocols.

LSD protocols need to have a solid moat: Such protocols face the target market of underlying protocols, and if the moat is not strong enough, they can easily be surpassed by newcomers. Convex has set a one-way exchange for CRV/VeCRV in its model, ensuring that Convex's position in Curve will not be weakened, thus avoiding being dismantled by competitors. Compared to Curve's staking ecology, Ethereum's staking nodes can also be disassembled into different segmented node markets, and currently, EigenLayers seems to exhibit this potential.

How will LSD protocols develop?

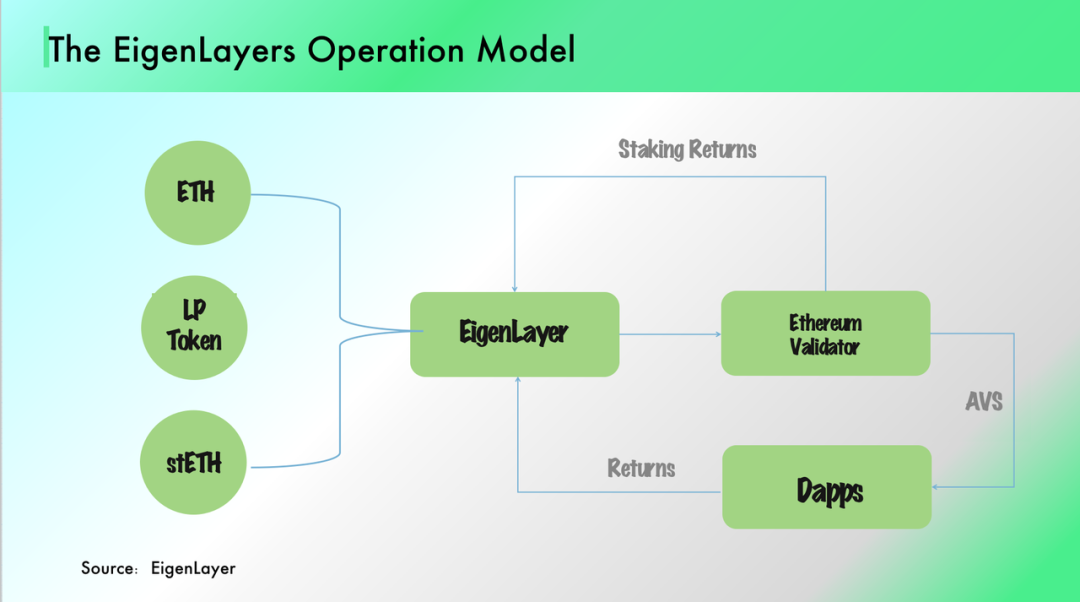

Security & decentralization become important development directions: With Lido's staking income continuously increasing, the robust operation and security of nodes are being valued by the market. SSV and EigenLayer are undoubtedly the most outstanding protocols. SSV Network decouples node deployment and validation confirmation through DVT (Distributed Validator Technology). Specifically, SSV establishes a network through sharded keys, integrating multiple nodes to execute the work of validators together, making network validation more decentralized and secure. EigenLayer, on the other hand, provides a super fluid staking method, supporting various liquid staking options including ETH, ETH LP, and ETH LSD, offering staking services to more users. More importantly, EigenLayer introduces the concept of ReStaking, allowing users to delegate their staking node choices to EigenLayer, enabling already staked tokens to change their applications, thus enhancing the extensibility of Ethereum's trust, and users can also gain additional income from providing staking validation for other ecosystems.

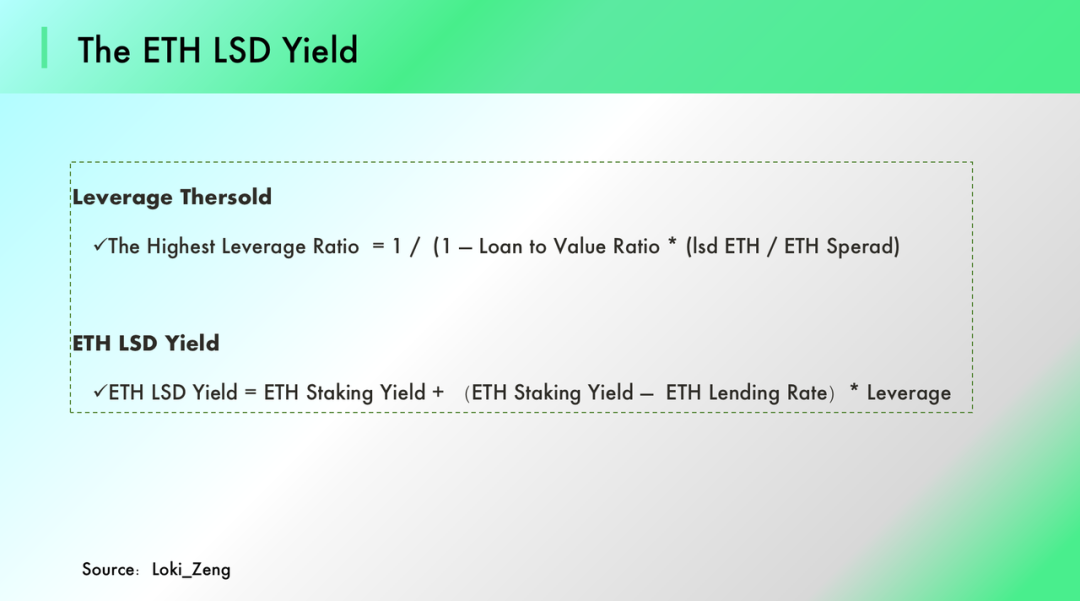

Lending protocols will benefit from the Shanghai upgrade: The development of LSD protocols comes from ETH staking rewards and lending rates. After the Shanghai upgrade, the ETH redemption mechanism will be activated, and the interest rate spread between ETH and stETH will significantly narrow, allowing users to achieve higher leverage. ETH farming yield comes from staking rewards and the interest rate spread under leverage, so we cannot accurately determine whether LSD can provide better returns for stakers after the Shanghai upgrade, but the TVL of lending protocols may see significant growth. We can draw a somewhat unexpected conclusion that lending protocols may be the biggest beneficiaries of the Shanghai upgrade.

Loki_Zeng: The interest rate spread between staking and lending essentially represents liquidity premium and risk exposure premium. Choosing staking requires sacrificing asset liquidity and bearing greater losses. The reason why high returns of 10%-20% can now be achieved through leverage is mainly due to the uncertainty surrounding the ETH Shanghai upgrade. The longer the uncertainty lasts, the higher the volatility risk of stETH. Therefore, once ETH opens for staking redemption, a highly certain outcome is the narrowing of the interest rate spread, ultimately forming a balance, and the returns from leveraged staking will return to a reasonable range. Another highly certain outcome is that lending becomes one of the ways to leverage staking, making the LSD lending market more prosperous. As pointed out in the Capitalism Lab article, lending becomes the hidden winner of LSD.

Conclusion

Through the disassembly of Frax and Convex, Bittracy believes the core advantage of LSD protocols lies in leveraging yield boosting combined with token models to achieve the (capture & lock) of foundational tokens, while binding to the DeFi ecosystem to realize the widespread application of LSD tokens (price anchoring). The current development of LSD protocols seems to have just begun. As GMX trading volume continues to rise, GLP's ability to accumulate value from transaction fees is impressive, and numerous LSD protocols based on GMX are emerging. Jones DAO locks yield tokens through GLP/jGLP, and the platform even includes jETH and jUSDC. Plutus has also established GLP/Plv GLP to ensure the protocol captures GLP/GMX and indicates that users achieve automatic reinvestment. More importantly, Plutus targets the governance rights of GMX, ensuring its voice in GMX by controlling the governance tokens of DPX and JONES. It is believed that with the joint efforts of builders, more LSD innovations will continue to emerge in the future.

References

1.https://tokeninsight.com/en/research/analysts-pick/jglp-from-jonesdao-how-it-offers-higher-yield-for-glp-holders

2.https://tokeninsight.com/en/research/analysts-pick/jglp-from-jonesdao-how-it-offers-higher-yield-for-glp-holders

3.https://foresightnews.pro/article/detail/19689

Risk warning

Risk warning Risk warning

Risk warning