Shanghai Upgraded Ethereum: Outlook on the Staking Track and Sell-off Wave

According to the model calculations, when the Ethereum staking amount reaches 44.3M, the staking yield will drop to 2.5%; however, LSD will bring many new gameplay options including circular loans, nested loans, etc.

According to the model calculations, when the Ethereum staking amount reaches 44.3M, the staking yield will drop to 2.5%; however, LSD will bring many new gameplay options including circular loans, nested loans, etc.Author: Darren, Everest Ventures Group

The Shanghai upgrade is tentatively scheduled for April 13, which will allow validators to withdraw and withdraw funds from the beacon chain for the first time. With these expectations in mind, the market is once again focusing on Ethereum liquidity. After the Shanghai upgrade is completed, will there be a sell-off? Will there be significant price fluctuations? What is the future outlook for Ethereum staking? How will staking yields trend? This article analyzes and discusses these issues in conjunction with data on Ethereum's price, deflation rate, staking rate trends, and supply rate trends, with the following conclusions:

- There may be some selling pressure (partial withdrawals) shortly after the Shanghai upgrade is completed, and this selling pressure will have an immediate effect on the market;

- Only 40% of Ethereum stakers (non-liquid stakers) have a willingness to sell; this 40% of Ethereum stakers have relatively low costs, which will bring some selling pressure, but this process is slow, and in extreme cases, it may take 125 days to withdraw all staked Ethereum;

- The staking rate of Ethereum can continue to grow in the coming years, but the growth rate will slow down after reaching a critical value;

- Without considering nested and leveraged staking, the staking yield of Ethereum will decrease as the staking rate rises, but with the continuous development of the blockchain industry and the emergence of more gameplay in the liquid staking sector, Ethereum staking yields will be higher, and correspondingly, the Ethereum staking rate will also be higher than expected.

1. Impact on Ethereum Price

Source: https://dune.com/hildobby/eth2-staking

Currently, about 60% of Ethereum is staked with service providers that offer collateralized liquidity derivatives, while only about 40% of Ethereum belongs to independent validators and staking pools, which will be affected differently by this Shanghai upgrade.

1) Partial Withdrawals and Full Withdrawals

Withdrawals are divided into partial withdrawals and full withdrawals.

Partial withdrawals: This refers to the balance exceeding 32 Ethereum (earned rewards) being directly withdrawn to an Ethereum address, which can be used immediately, while the validator will continue to be part of the beacon chain and validate as expected;

Full withdrawals: This refers to validators completely exiting, no longer being part of the beacon chain, and the entire balance of the validator (32 Ethereum and any other rewards) being unlocked and allowed to be used after the exit mechanism is completed.

It should also be noted that beacon chain validators include a field called withdrawal credentials, the first two bytes of which are called the withdrawal prefix. This value is currently either 0x00 or 0x01, and it is set when deposits are made through the deposit tool; validators with a 0x00 withdrawal credential will not be able to withdraw immediately and will need to migrate to 0x01 to perform partial and full withdrawals.

2) Potential Impact of Partial Withdrawals on Ethereum Price

The rate of partial withdrawals allows for 16 withdrawal requests per block, with a current block time of 12 seconds, resulting in 5 blocks per minute, 300 blocks per hour, and approximately 7.2k blocks per day; thus, assuming every validator updates to 0x11, it is expected that there will be about 115k partial withdrawals per day.

According to data from beaconcha.in, there are currently 558,062 validators, so it will take about 4 to 5 days to achieve partial withdrawal exits. The average balance per validator is about 34 Ethereum, so it is estimated that stakers have earned approximately "(34-32)✖558062 = 1,116,124 Ethereum in staking rewards (counted as 1.1 million). At the current Ethereum price (around $1800), this means that approximately $1.98 billion worth of Ethereum will be released in 4 to 5 days.

As shown in the figure below, according to CoinGecko data, the current total daily spot trading volume of Ethereum is $10.4 billion, so the total value of partial withdrawals is about 19% of Ethereum's daily spot trading volume, averaging a daily release of 3% to 4% of the daily spot trading volume over 5 days.

This part is expected selling pressure because, unlike full withdrawals that can be exchanged for Ethereum through liquid staking derivatives before the Shanghai upgrade, the staking rewards portion (partial withdrawals) can only be extracted after the Shanghai upgrade. Therefore, this part is likely to have some selling pressure, but the impact of partial withdrawals on the price is relatively short-term and will not continuously affect Ethereum's price in the long run; secondly, at the current Ethereum price, considering the other on-chain behaviors of POS participants (who usually continue to compound), a significant portion of long-term Ethereum stakers and holders will not sell at this time.

Source: https://www.coingecko.com/

Furthermore, not all validators actually have a 0x01 credential. As shown in the figure below, according to Data Always data, as of January 29, 2023, about 20% of new validators have not set the 0x01 credential.

Source: https://dataalways.substack.com/p/partial-withdrawals-after-the-shanghai

Additionally, according to animations in the Data Always research, the peak conversion of 0x00 will occur early the day after the Shanghai upgrade is completed and will last for about two days, rather than reaching immediately upon completion of the upgrade; therefore, in the most extreme case, it is expected to see about 110k Ethereum in partial withdrawals on the first day (excluding Lido 0x01 validators).

3) Potential Impact of Full Withdrawals on Ethereum Price:

Full withdrawals and partial withdrawals have the same priority and are in the same withdrawal queue; during the partial withdrawal process, if a validator is marked as "exited," then the entire refund of the balance + rewards will be executed. However, unlike partial withdrawals, the rate of full withdrawals is subject to more restrictions. As shown in the two figures below, the current full withdrawal limit is 8, with a maximum of 57.6k Ethereum withdrawn daily, and currently, about 18M Ethereum is staked, with LSD and CEX accounting for 60%.

Since most of this has secondary market exit channels, it can be assumed that only an additional 40% of Ethereum staking participants are willing to exit after the Shanghai upgrade, which is 7.2M Ethereum. Therefore, assuming in an extreme case that no users deposit after the Shanghai upgrade and the daily withdrawal volume reaches the maximum, it would take 125 days for all staked Ethereum to completely exit.

Source: https://dune.com/queries/1924507/3173695

As mentioned above, the two categories that account for 60% of the supply are LSD and CEX, which have mostly issued collateralized liquidity derivatives such as stETH, cbETH, rETH, bETH, etc.

Taking stETH as an example, the current exchange rate of stETH to ETH is 0.9996, with a very small price difference. Therefore, if stakers want to sell, they can directly exchange liquidity derivatives for Ethereum in the market without having to wait until after the Shanghai upgrade to sell; for this reason, the cost of currently staked Ethereum is actually very dispersed and constantly changing, with many people holding stETH not obtained through staking ETH but rather through trading in the secondary market. For these 60% of stakers, the Shanghai upgrade will not have a significant impact on them, assuming no market selling pressure causes overselling behavior.

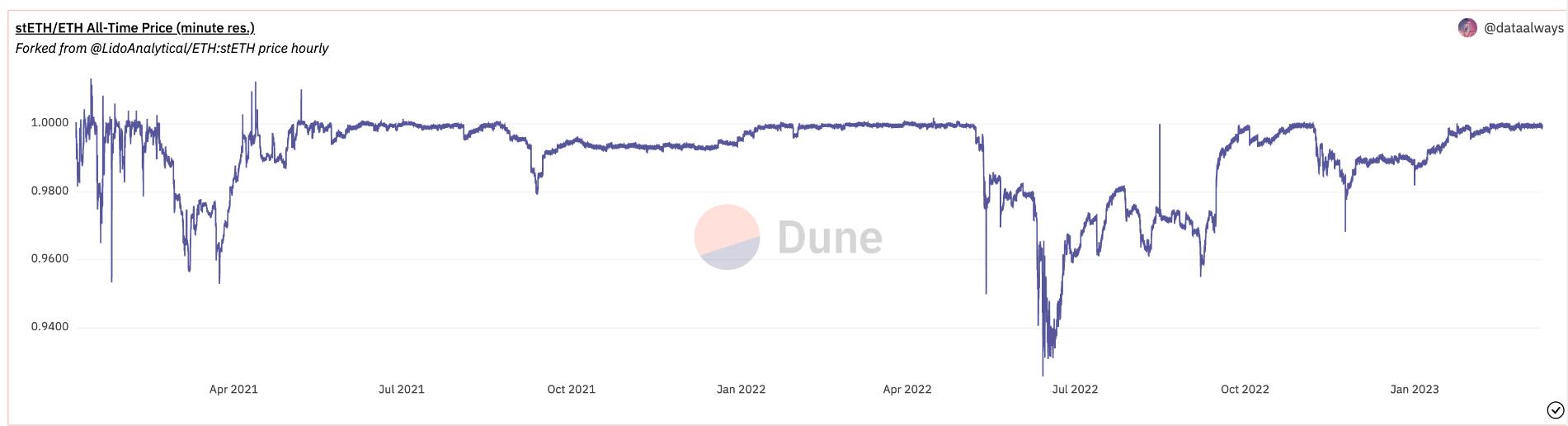

There is also a viewpoint in the market that large stakers may sell due to concerns about insufficient liquidity of derivatives, which may lead to discounts, so they will wait until after the Shanghai upgrade to exit staking before selling. This concern is not unfounded, but if we look back at Ethereum's historical prices, as shown in the figure below, we can see that there were significant discounts during March 2021 and June 2022. In March 2021, this was due to the market being at a high point, and most of the selling was from users who staked at the end of 2020 cashing out; the discount in June 2022 was due to the 3AC and FTX events, which caused some institutions to sell large amounts of stETH, leading to price decoupling. This shows that for large investors, selling behavior still occurs in the case of insufficient liquidity, depending on market conditions rather than concerns about liquidity; therefore, attributing the potential decline of Ethereum entirely to expectations of liquidity tightening is incorrect.

Source: https://dune.com/skynet/lido-stetheth-monitor

4) The Impact of Ethereum Deposit Cost on Price Fluctuations After the Shanghai Upgrade

Source: https://dune.com/hildobby/eth2-staking

As shown in the figure above, there are currently more stakers whose deposit costs are "underwater" than those who are "in profit," leading to two perspectives: one believes that these loss-making stakers will withdraw deposits to stop losses, while the other believes that loss-making stakers are more likely to hold due to "loss aversion" emotions.

In terms of Ethereum staking, for the majority of Ethereum stakers (60%), there is no cost issue, as mentioned above, they can also exchange stETH for ETH and sell it through the secondary market before the Shanghai upgrade, so this does not affect these 60% of stakers.

However, for the other 40%, most of them are early participants in Ethereum POS staking, and this group has a relatively low cost; the Ethereum beacon chain mainnet deposit contract address was first launched in November 2020, when the ETH price was only about $400 to $500, and it wasn't until the end of March 2021 that Ethereum tokens reached today's price. Therefore, it can be speculated that this group of stakers accounts for a large portion of those "In the Money" in the figure above, and such a cost price has increased by 3 to 4 times to today's $1800, so this group may bring some selling pressure. Additionally, due to market sentiment, the selling pressure from this group may cause FUD sentiment in the market, leading the 60% of stakers to panic sell. However, as mentioned above, the exit from Ethereum staking is limited by withdrawal rates, so the selling reaction of these stakers in the market will also be relatively slow.

2. Impact on Ethereum Staking Rate and Staking Yield

The above discusses the potential impact of the Shanghai upgrade on Ethereum's price. Additionally, the impact of the Shanghai upgrade on Ethereum will also be reflected in the staking rate and staking yield of Ethereum.

1) Factors Affecting Ethereum's Staking Rate and Staking Yield

After analysis, we believe that Ethereum's staking rate will be higher after the Shanghai upgrade than it is now, but it will be difficult to reach such high staking rates (60% to 80%) as other public chains; furthermore, as the staking rate rises, the staking yield will decrease without considering nested, LSDFI, and other gameplay.

The following three factors may benefit the growth of Ethereum's staking rate.

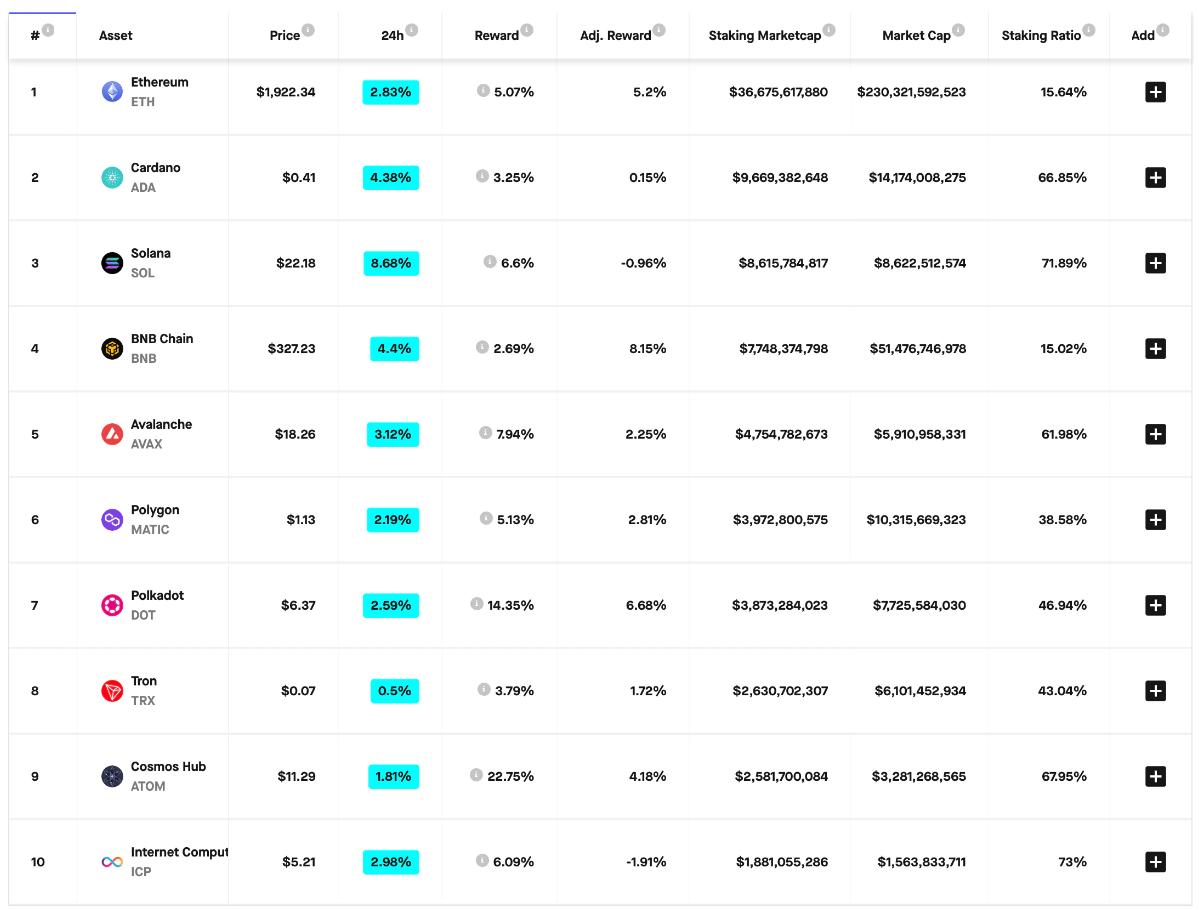

i) As shown in the figure below, Ethereum's current staking rate is only 15.52%, while other public chains have staking rates as high as 73%, so it can be concluded that Ethereum's current staking rate is definitely low and has significant growth potential.

Source: https://www.stakingrewards.com/

ii) Before the Shanghai upgrade is completed, Ethereum staked on the beacon chain cannot be liquid, and a large amount of capital is locked on the beacon chain, leading to inflexible capital utilization, which may reduce users' desire to stake; however, with the completion of the Shanghai upgrade, this liquidity risk issue will be resolved, and Ethereum staking will achieve a closed loop from deposit to withdrawal, with the exchange rate of collateralized liquidity derivative tokens returning to 1:1 with Ethereum tokens, which may attract a large number of institutions and capital to stake. However, this point does not hold much reference value in the current environment dominated by LSD.

iii) Ethereum is currently in a deflationary state, with a current inflation rate of -0.62%. According to supply and demand, this indicates that the value of Ethereum is continuously increasing over time. The high staking rates of other public chains are due to their higher staking yields, which result from continuous token issuance and devaluation. Therefore, from this perspective, for long-term stakers, staking funds in Ethereum may be a more attractive choice; moreover, since the market is currently in a bear phase and relatively inactive, Ethereum is already in a deflationary state, and in the subsequent bull market, the daily gas consumption will be higher, making Ethereum's deflation more significant.

However, Ethereum's staking rate will not grow indefinitely. We believe that:

i) Ethereum cannot provide staking yields as high as those of other public chains, so more users may prefer to stake their assets on chains with higher yields.

ii) In addition to not having an advantage in staking yields compared to other public chains, Ethereum's staking yield will also decrease as the staking rate increases (regardless of nested, LSDFI, and other gameplay). As shown in the two figures below, Ethereum's staking rate and staking yield are in dynamic equilibrium. According to this model, when Ethereum's staking volume reaches 44.3M ETH, the annualized yield will only be 2.5%. The increase from 18.2M to 44.3M staking volume is about 2.5 times; however, the fact is that this staking yield is not sufficient to attract most users. Therefore, this article predicts that Ethereum's staking rate will slow down after doubling from the current rate.

Source: https://ultrasound.money/

2) Predictions for Ethereum Supply, Staking Rate, and Staking Yield

Trends in Ethereum supply and staking rate from February 2021 to March 2023

As shown in the figure above, it can be seen that since September 2022, the growth of Ethereum's supply has gradually stabilized and even shown a downward trend. Since Ethereum opened staking, the amount of Ethereum staked has continuously increased, and currently, the upward trend in Ethereum staking volume does not seem to be slowing down.

Based on this, we believe that:

In a bear market where market trading is not active, the growth of Ethereum's supply is gradually stabilizing and showing a downward trend. It can be expected that with the arrival of a bull market, the significant increase in trading volume and the rise in gas consumption will further accelerate Ethereum's deflation. The Ethereum staking rate will rise against the backdrop of supply deflation; however, as Ethereum's staking rate continues to increase, the staking yield per node will decrease, and when the staking rate reaches a certain value, it will enter a dynamic equilibrium state between the two.

But we believe that with the continuous development of the blockchain industry, liquid staking, as a DeFi Lego component, will build and derive more gameplay on top of it, and correspondingly, Ethereum's staking rate will be higher than expected. According to model calculations, when Ethereum's staking volume reaches 44.3M, the staking yield will drop to 2.5%; however, LSD will bring many new gameplay options, including circular loans, nesting, etc. Therefore, with the development of the LSD sector and the blockchain industry, a more attractive comprehensive staking yield will drive the Ethereum staking sector towards a higher dynamic equilibrium.

References:

[1] Brace Yourselves, Shanghai Is Coming

[2] Partial withdrawals after the Shanghai fork

[3] The Future of ETH Liquid Staking

Risk warning

Risk warning Risk warning

Risk warning